- Summary

- Table Of Content

- Methodology

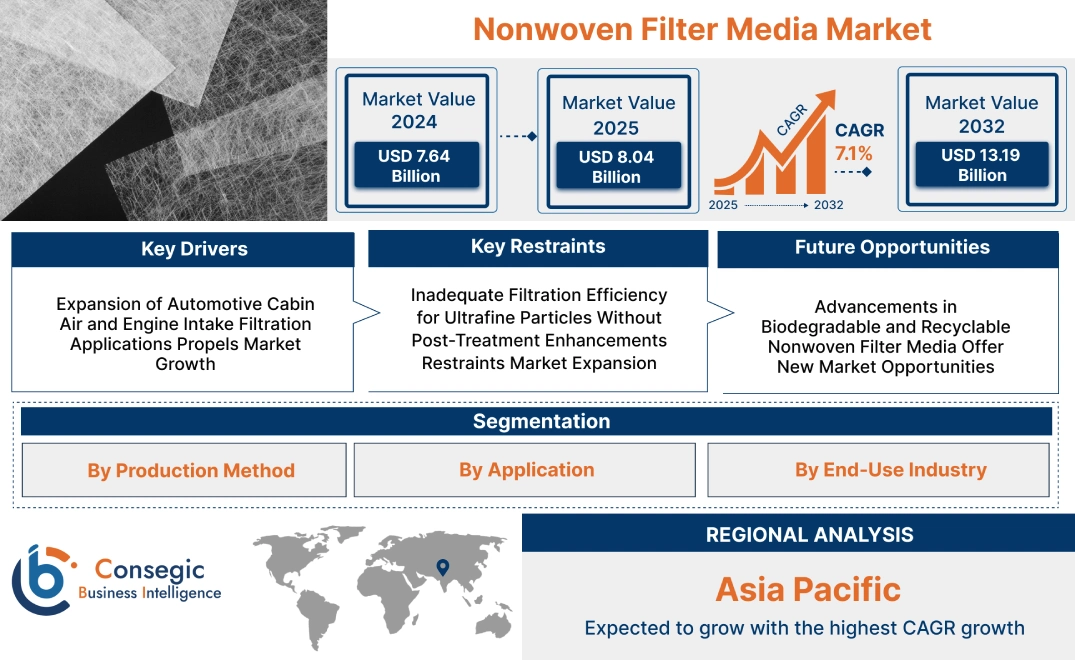

Nonwoven Filter Media Market Size:

Nonwoven Filter Media Market size is estimated to reach over USD 13.19 Billion by 2032 from a value of USD 7.64 Billion in 2024 and is projected to grow by USD 8.04 Billion in 2025, growing at a CAGR of 7.1% from 2025 to 2032.

Nonwoven Filter Media Market Scope & Overview:

Nonwoven filter media are engineered textiles that consist of synthetic or natural fibers bonded by mechanical, thermal, or chemical means, without knitting or weaving. They find widespread applications in air, liquid, and gas filtration processes in industries like healthcare, automobile, water treatment, and industrial processing.

The key characteristics of these fabrics are consistent pore structure, high permeability, lightweight composition, and alterable thickness. These enable effective particle capture, long service life, and resistance to chemical and heat stress. Its form varies from meltblown and spunbond to needle-punched, each adapted for a particular need.

It improves process efficiency by providing uniform filtration performance and minimizing pressure drop. It is compatible with disposable and reusable filtration systems and is thus an adaptable option for single-use items and permanent installations. Its versatility in accommodating diversified environments and regulations makes it a vital element of contemporary filtration systems.

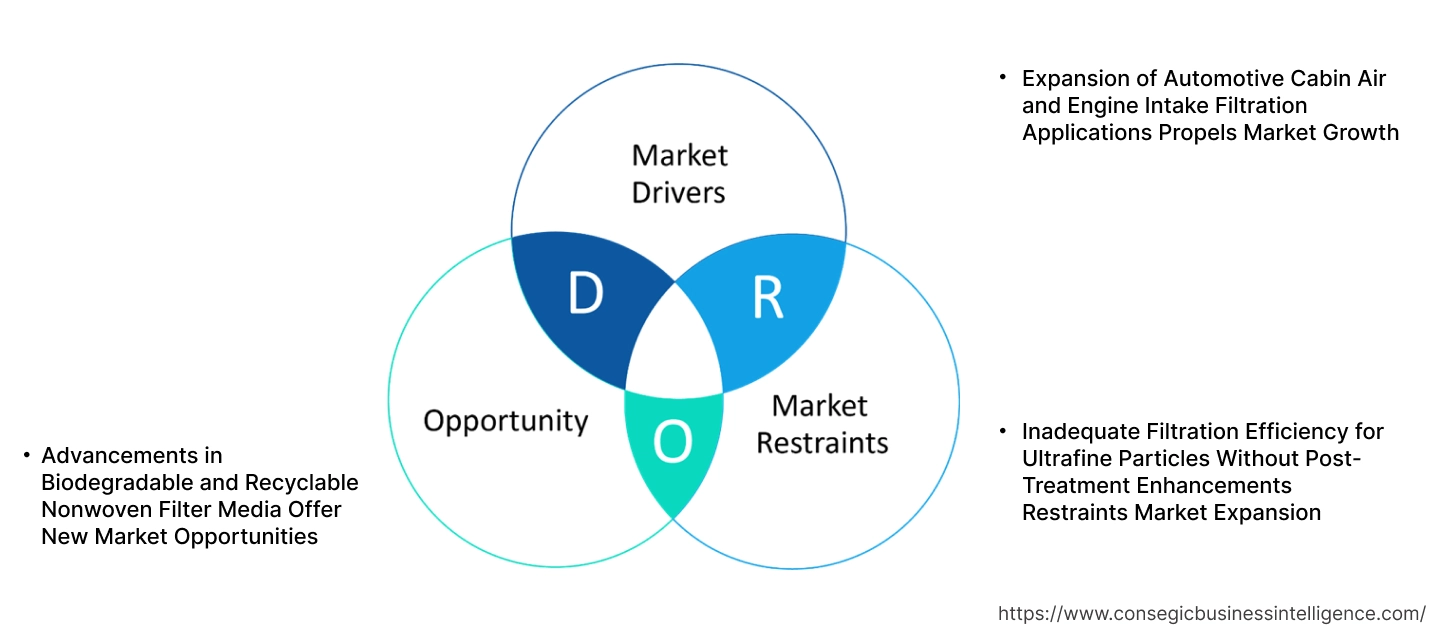

Nonwoven Filter Media Market Dynamics - (DRO):

Key Drivers:

Expansion of Automotive Cabin Air and Engine Intake Filtration Applications Propels Market Growth

The automotive sector is increasingly adopting advanced filtration technologies to improve air quality inside vehicle cabins and safeguard internal combustion and electric powertrain systems. Nonwoven filter media are used in cabin air filters due to their low airflow resistance, consistent particle retention, and capacity to support multilayer composite structures. In engine air intake systems, the materials provide durability and high dust-holding capacity under fluctuating thermal and mechanical stress. The increasing focus on occupant well-being, governmental regulations for particulate control, and customer aspirations for high-quality in-cabin environments are speeding up the application of HEPA-grade and PM2.5 cabin air filters. In EVs, nonwoven media are also being applied in battery cooling and HVAC modules to support thermal efficiency as well as clean air.

- For instance, in June 2024, Mann+Hummel launched the Mann-Filter FreciousPlus with nanofibers for cabin air filtration. In addition to the PM10 and PM2.5 particles, the nanofibers in this product can remove 90% of the finer PM1 class and up to 80% of ultra-fine particles. For best performance, it is recommended to replace these filters once a year or every 15,000 km.

As global vehicle producers focus on performance, comfort, and air quality, filtration system demand is mounting across automotive classes. These forces are playing a direct role in propelling the nonwoven filter media market expansion.

Key Restraints:

Inadequate Filtration Efficiency for Ultrafine Particles Without Post-Treatment Enhancements Restraints Market Expansion

Ordinary nonwoven filter media tend to fail in collecting ultrafine particles of less than 0.3 microns without secondary surface treatment or composite layering. At high-precision applications like cleanroom environments, pharmaceutical processing, and microelectronics, this limited performance requires secondary improvements such as electrostatic charging, nanofiber deposition, or activated carbon incorporation. Post-treatment procedures add production complexity and increase material costs. In those applications where ultrafiltration or biocontaminant retention is paramount, membrane-based or hybrid technologies tend to be chosen over traditional nonwoven formats. The reliance on companion treatment technologies constrains the independent effectiveness of base media and hinders scalability in cost-conscious sectors. This performance limitation confers a diminution of use cases without technical adaptation. Consequently, the limitations of filtration at the sub-micron level pose a distinct challenge to nonwoven filter media market growth, even as wider usage occurs for general-purpose filtration.

Future Opportunities:

Advancements in Biodegradable and Recyclable Nonwoven Filter Media Offer New Market Opportunities

Sustainability has emerged as a strategic imperative for filtration product manufacturers and end-users, compelling innovation in recyclable and biodegradable nonwoven filter media. Advances in material science are making it possible to create high-performance filter substrates from polylactic acid (PLA), cellulose, and bio-polyesters with comparable mechanical properties and filtration efficiency to their synthetic fiber equivalents. These substitutes minimize landfill burden and support regulatory efforts aimed at reducing single-use plastics. Sustainable filtration products are becoming increasingly demanded, particularly for use in air purifiers, HVAC equipment, and liquid process filters in healthcare, food, and packaging industries. Green procurement policies and extended producer responsibility regimes are also promoting commercial uptake. Companies that invest in biodegradable filter media can realize competitive edge in public sector tenders and ESG-driven markets. These material advancements are building solid nonwoven filter media market opportunities based on sustainability-linked product differentiation and environmental compliance expansion.

Nonwoven Filter Media Market Segmental Analysis :

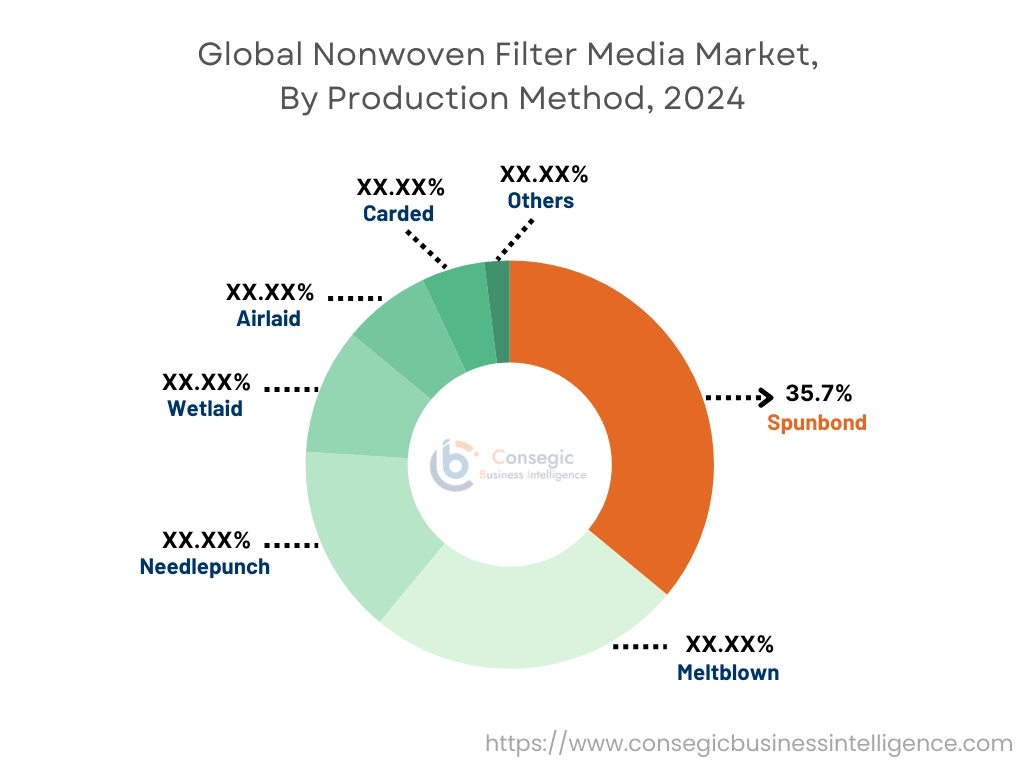

By Production Method:

Based on production method, the market is segmented into spunbond, meltblown, needlepunch, wetlaid, airlaid, carded, and others.

The spunbond segment held the largest nonwoven filter media market share of 35.7% in 2024.

- Spunbond fabric provide high tensile strength, dimensional stability, and cost-effectiveness, making them suitable for both air and liquid filtration applications.

- This method enables continuous fiber production and is widely used in automotive cabin filters, HVAC systems, and protective medical fabrics.

- The segment benefits from robust manufacturing throughput and low energy consumption, offering a competitive advantage in large-scale operations.

- As per nonwoven filter media market analysis, increased need for efficient and lightweight filtration materials across industries drives this segment.

The meltblown segment is projected to experience the highest CAGR during the forecast period.

- Meltblown nonwoven media exhibit ultrafine fibers with superior filtration efficiency, especially in capturing submicron particles in air and liquid systems.

- Growing adoption in healthcare PPE, face masks, and high-efficiency particulate air (HEPA) filters underpins segment expansion.

- Meltblown technology is a core enabler of advanced filter media required in both industrial and consumer applications.

- For instance, in October 2024, Gessner unveiled new air filter media with activated carbon. The NeenahPure™ meltblown nonwoven product range is designed for pleatable and bag filters in HVAC, air purification & air pollution control applications to ensure clean indoor air for enhanced protection.

- According to nonwoven filter media market trends, the rising need for air pollution control and personal protection is accelerating meltblown media need.

By Application:

Based on application, the market is bifurcated into air filtration and liquid filtration.

The air filtration segment held the dominant market position in 2024.

- Air filtration applications rely on nonwoven filter media for HVAC systems, automotive cabin filters, and industrial dust collectors due to their structural integrity and filtration performance.

- Demand is rising due to growing health concerns, air quality regulations, and industrial emissions control.

- Key advantages include high dust-holding capacity, low pressure drop, and customizable porosity.

- As noted in nonwoven filter media market analysis, increased deployment of air filtration units in commercial and residential infrastructure continues to drive this segment.

The liquid filtration segment is expected to register the fastest CAGR.

- Liquid filtration applications span water purification, food & beverage processing, chemical filtration, and wastewater treatment.

- They offer superior retention of suspended solids and microorganisms, ensuring process efficiency and hygiene.

- The flexibility of nonwoven materials enables compatibility with various filter formats, including depth filters and cartridges.

- The rising investment in water treatment infrastructure, as well as regulatory compliance, is fueling the nonwoven filter media market growth.

By End-Use Industry:

Based on end-use industry, the market is segmented into automotive, healthcare & medical, food & beverage, water & wastewater treatment, oil & gas, chemical, HVAC, electronics, and others.

The healthcare & medical segment accounted for the largest nonwoven filter media market share in 2024.

- Nonwoven filter media are integral to sterile filtration, respiratory protection (e.g., N95 masks), and medical equipment air intake.

- Their high barrier properties, breathability, and compatibility with sterilization methods support widespread adoption.

- The segment saw accelerated growth during and post-pandemic, driven by heightened global awareness of infection control.

- As per nonwoven filter media market trends, ongoing innovation in biocompatible and antimicrobial nonwovens further enhances this segment.

The water & wastewater treatment segment is expected to grow at the fastest CAGR.

- The need for clean water in municipal, industrial, and residential settings drives the adoption of nonwoven filtration media.

- These media are used in depth filtration systems and membrane prefilters, offering low pressure drop and extended service life.

- Market growth is supported by stricter environmental regulations and the reuse of treated water in agriculture and industry.

- Thus, the increased investment in decentralized treatment plants supports the nonwoven filter media market expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

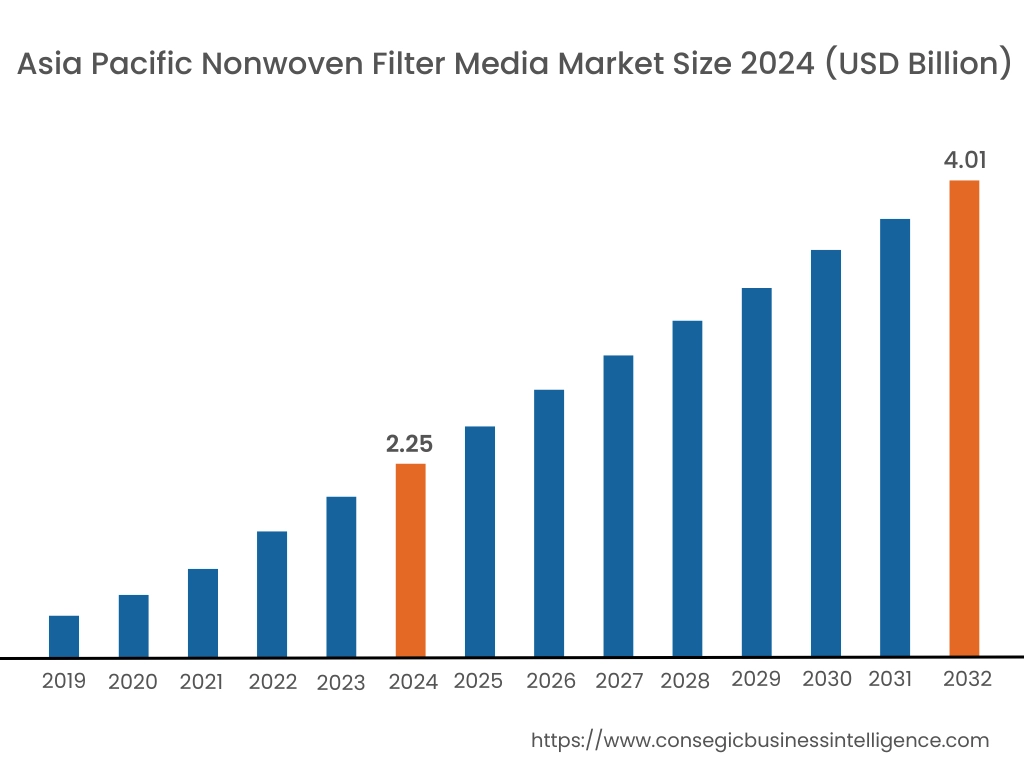

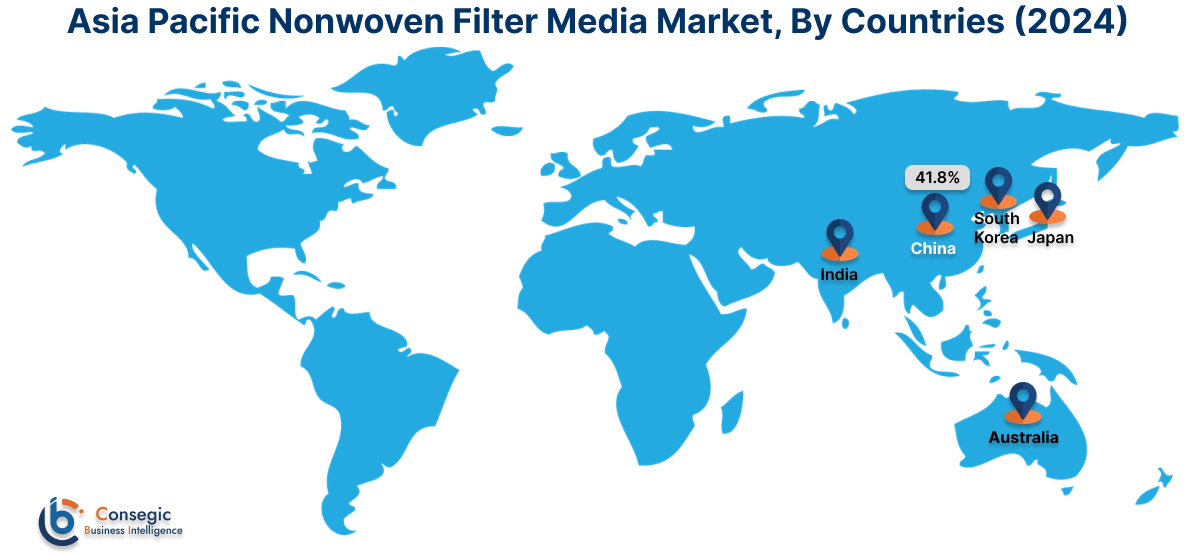

Asia Pacific region was valued at USD 2.25 Billion in 2024. Moreover, it is projected to grow by USD 2.38 Billion in 2025 and reach over USD 4.01 Billion by 2032. Out of this, China accounted for the maximum revenue share of 41.8%. This region is experiencing rapid expansion in the nonwoven filter media industry, driven by industrialization, urbanization, and rising awareness about the environment. Automotive, water treatment, face masks, and home appliances are driving strong requirement in China, India, Japan, and South Korea. Regional analysis confirms that rising pollution levels, alongside government regulations requiring cleaner production and public health policies, are placing a greater strain on filtration demands. Middle-income households and the development of healthcare infrastructure also support market penetration. Meanwhile, local industry is increasing domestic production of meltblown and spunbond material to meet domestic consumption as well as export potential.

North America is estimated to reach over USD 4.27 Billion by 2032 from a value of USD 2.53 Billion in 2024 and is projected to grow by USD 2.66 Billion in 2025. The region maintains a dominant position in the market, powered by robust demand across healthcare, HVAC, and industrial applications. The United States and Canada demonstrate stable uptake of high-performance filter media in air cleaning, automotive cabin filtration, and water treatment systems. Market research identifies the region's tight air quality regulations and focus on indoor environmental safety as prime drivers sustaining continuous product innovation. Further, growth in pharmaceutical production and cleanroom activities continues to drive the nonwoven filter media market demand. Increasing awareness among consumers for airborne contaminants and energy-saving ventilation systems further fosters regional market expansion.

Europe is a technologically advanced and regulation-oriented market where sustainability targets and circular economy measures shape the selection of materials and manufacturing techniques. Germany, France, and Italy are among the world's leading users of nonwoven filter media for industrial as well as environmental filtration applications.

- For instance, in November 2024, Johns Manville invested in a new micro fiberglass production line for Evalith filtration materials situated in Wertheim, Germany. This expansion aims to meet the growing need for high-efficiency filter media to improve indoor air quality in vital environments like hospitals, schools, offices, etc. The product is able to capture the most minuscule particles including viruses, bacteria, and dust, down to just one micrometer.

Research indicates that continuous infrastructure retrofitting and automobile electrification drive the need for high-efficiency lightweight filter materials. In addition, EU emissions directives and occupational health directives have intensified replacement cycles for industrial filtration systems. The area's emphasis on recyclable and biodegradable nonwovens also offers an upcoming space of innovation in the value chain of filtration.

Latin America is becoming a developing market, with Brazil, Mexico, and Argentina leading demand in municipal water treatment, mining, and medical supplies markets. Market analysis identifies that although take-up of high-quality filter media remains emerging, public sector expenditure on sanitation and air quality management is underpinning incremental growth. As the region recovers from economic uncertainty, enhancements in regulatory systems and greater emphasis on healthcare resilience are likely to support long-term market momentum. Manufacturers bringing cost-effective and resilient nonwovens designed to address regional infrastructure limitations could find a substantial nonwoven filter media market opportunity.

In the Middle East and Africa, the nonwoven filter media market demand is picking up steam in certain industries like oil & gas, HVAC systems, and urban infrastructure. Saudi Arabia, the UAE, and South Africa are adopting advanced filtration technologies in smart city schemes and industrial safety systems. As per local analysis, growing focus on water reuse, clean air regulations, and infection control practices in the health sector is laying the groundwork for wider application. Challenges still exist in local manufacturing capability and accessibility of the product. Development will be based on increasing investment in supply chain creation and public-private partnerships with goals of sustainability and health outcomes.

Top Key Players & Market Share Insights:

The nonwoven filter media market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global nonwoven filter media market. Key players in the nonwoven filter media industry include -

- Ahlstrom (Finland)

- Freudenberg Group (Germany)

- Mann+Hummel (Germany)

- Hollingsworth & Vose (USA)

- Lydall Performance Materials (USA)

- Mogul (Turkey)

- Sandler AG (Germany)

- Berry Global Inc. (USA)

- Johns Manville (USA)

- Kimberly-Clark Worldwide, Inc. (USA)

Recent Industry Developments :

Product Launches:

- In January 2025, Monadnock Non-Wovens unveiled higher efficiency, eco-friendly, meltblown air filtration media called the Monadnock HPAQ 3F™. Designed for application in respirators, HVAC and air purification filters, the HPAQ 3F meets all international filtration standards: ASHRAE 52-2, ASTM 2100, EN-149, HEPA, MERV 10-16, and NIOSH. It captures more dust, pollen, allergens, viruses, and smoke with a lower pressure drop.

Acquisitions:

- In September 2024, Wind Point Partners acquired Clean Solutions Group. This involved Wind Point investing in CSG for continued growth, innovation and execution of their shared vision of value creation.

Partnerships:

- In March 2025, Acme Mills partnered with Vietnam Producers to offer high-quality non-woven textiles, circumventing tariffs to meet market demand. This move ensures the delivery of premium quality textiles to clients at competitive prices.

Nonwoven Filter Media Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 13.19 Billion |

| CAGR (2025-2032) | 7.1% |

| By Production Method |

|

| By Application |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Nonwoven Filter Media Market? +

Nonwoven Filter Media Market size is estimated to reach over USD 13.19 Billion by 2032 from a value of USD 7.64 Billion in 2024 and is projected to grow by USD 8.04 Billion in 2025, growing at a CAGR of 7.1% from 2025 to 2032.

What specific segmentation details are covered in the Nonwoven Filter Media Market report? +

The Nonwoven Filter Media market report includes specific segmentation details for production method, application and end-use industries.

What are the end-use industries in the Nonwoven Filter Media Market? +

The end-use industries of the Nonwoven Filter Media Market are automotive, healthcare & medical, food & beverage, water & wastewater treatment, oil & gas, chemical, HVAC, electronics, and others.

Who are the major players in the Nonwoven Filter Media Market? +

The key participants in the Nonwoven Filter Media market are Ahlstrom (Finland), Freudenberg Group (Germany), Mogul (Turkey), Sandler AG (Germany), Berry Global Inc. (USA), Johns Manville (USA), Kimberly-Clark Worldwide, Inc. (USA), Mann+Hummel (Germany), Hollingsworth & Vose (USA) and Lydall Performance Materials (USA).