- Summary

- Table Of Content

- Methodology

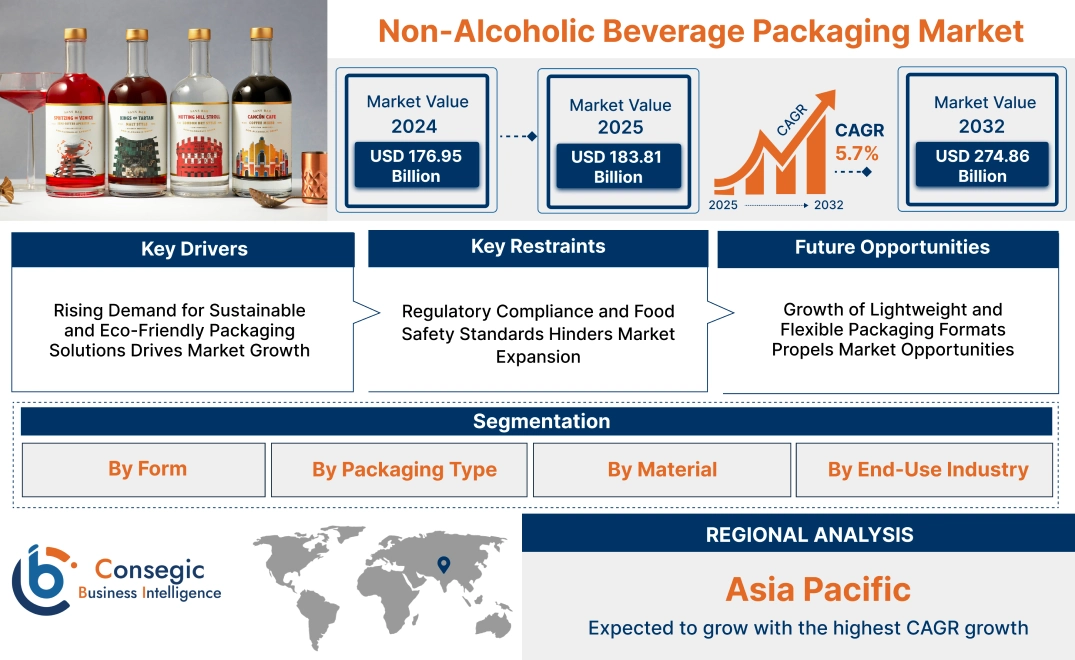

Non-Alcoholic Beverage Packaging Market Size:

Non-Alcoholic Beverage Packaging Market size is estimated to reach over USD 274.86 Billion by 2032 from a value of USD 176.95 Billion in 2024 and is projected to grow by USD 183.81 Billion in 2025, growing at a CAGR of 5.7% from 2025 to 2032.

Non-Alcoholic Beverage Packaging Market Scope & Overview:

Non-alcoholic beverage packaging encompasses a range of materials and designs used to preserve and distribute soft drinks, juices, dairy-based beverages, and functional drinks. It ensures product integrity, extends shelf life, and enhances convenience for consumers. Common packaging formats include bottles, cans, cartons, and pouches, manufactured from materials such as plastic, glass, metal, and paperboard.

Key features include durability, barrier protection, and lightweight construction, ensuring resistance to external contaminants while maintaining product freshness. Advanced sealing and tamper-proof technologies enhance safety, while ergonomic designs improve handling and storage efficiency. Customizable labeling and branding options further support market differentiation.

Beverage manufacturers, food service providers, and retailers utilize innovative packaging solutions to optimize product presentation and maintain regulatory compliance. Continuous advancements in materials and production techniques improve packaging efficiency, ensuring effective preservation and enhanced consumer appeal across diverse beverage categories.

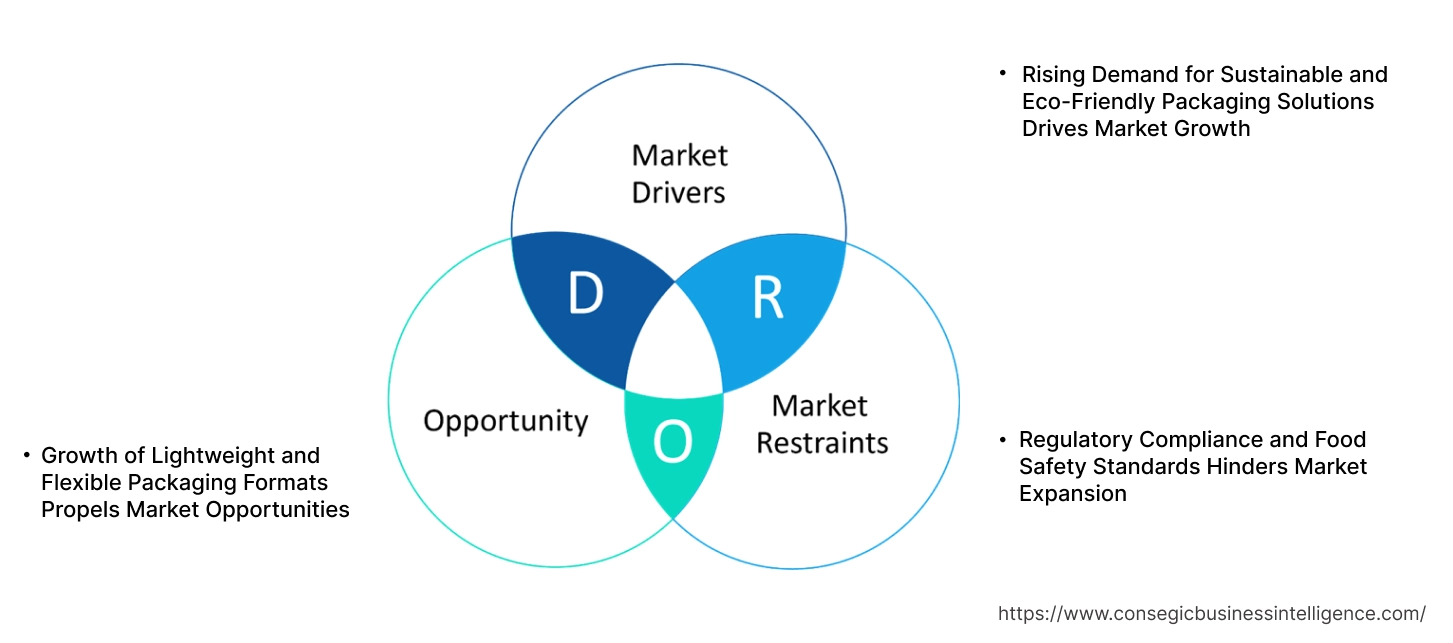

Non-Alcoholic Beverage Packaging Market Dynamics - (DRO):

Key Drivers:

Rising Demand for Sustainable and Eco-Friendly Packaging Solutions Drives Market Growth

Consumers and regulatory bodies are pushing brands to adopt biodegradable, recyclable, and plant-based packaging materials to minimize environmental impact. With rising concerns over plastic pollution and carbon emissions, companies are transitioning to recycled PET, compostable bio-plastics, and paper-based cartons to align with sustainability goals. Governments worldwide are introducing bans on single-use plastics and promoting circular economy initiatives, further accelerating the shift toward green packaging alternatives. Additionally, advancements in water-soluble films, seaweed-based bottles, and refillable packaging systems are opening new opportunities for eco-conscious brands. As companies invest in innovative materials and closed-loop recycling programs, they enhance their brand reputation while meeting consumer expectations for sustainability. These factors are expected to contribute significantly to non-alcoholic beverage packaging market expansion, reinforcing the industry's commitment to environmentally responsible solutions.

Key Restraints:

Regulatory Compliance and Food Safety Standards Hinders Market Expansion

Regulatory bodies such as the FDA, EU Commission, and food safety authorities impose stringent standards on material safety, chemical migration limits, and labeling requirements to ensure consumer protection. Manufacturers must invest in BPA-free, food-grade materials and advanced testing protocols, increasing production costs. Additionally, variations in regional food safety regulations complicate international distribution, requiring brands to adapt packaging formulations and labeling for different markets. Sustainability regulations further mandate the use of recyclable and eco-friendly materials, adding complexity to packaging development and supply chain management. Companies that fail to comply with evolving standards risk legal penalties, product recalls, and reputational damage. Addressing these regulatory challenges through investment in food-safe innovations and sustainability-driven packaging solutions is crucial for ensuring non-alcoholic beverage packaging market growth in the evolving global marketplace.

Future Opportunities:

Growth of Lightweight and Flexible Packaging Formats Propels Market Opportunities

Consumers seek single-serve, resealable, and portable packaging solutions that enhance ease of use while reducing storage and transportation costs. Flexible packaging formats such as stand-up pouches, tetra packs, and collapsible bottles offer superior durability, extended shelf life, and lower material waste, making them ideal for ready-to-drink coffees, flavored waters, and functional beverages. Additionally, manufacturers are developing lightweight materials with enhanced barrier properties, ensuring product freshness while minimizing packaging footprint. The growth of e-commerce and direct-to-consumer beverage sales is further increasing the demand for spill-resistant, compact packaging options that improve shipping efficiency. As companies explore innovative material combinations and sustainable alternatives, these advancements are expected to drive non-alcoholic beverage packaging market opportunities, enhancing industry sustainability and consumer convenience.

Non-Alcoholic Beverage Packaging Market Segmental Analysis :

By Form:

By form, the market is divided into rigid and flexible.

The rigid segment held the largest non-alcoholic beverage packaging market share in 2024.

- Rigid packaging, including bottles, cans, and cartons, dominates the market due to its durability, product protection, and premium appearance.

- The need for strong, tamper-resistant packaging is increasing, particularly in carbonated soft drinks, juices, and dairy-based beverages.

- Non-alcoholic beverage packaging market analysis highlights that rigid packaging ensures longer shelf life and improved brand presentation, making it the preferred choice for manufacturers.

- As per segmental trends, innovations in lightweight and recyclable rigid packaging materials are boosting adoption.

The flexible segment is expected to experience the fastest CAGR during the forecast period.

- Flexible packaging, including pouches, sachets, and biodegradable films, is gaining popularity due to its lightweight nature and reduced material usage.

- The need for eco-friendly and cost-effective packaging solutions is rising, particularly in ready-to-drink beverages and functional drink categories.

- Market trends indicate that resealable pouches and smart packaging innovations are driving the shift toward flexible formats.

- For instance, Huhtamaki offers flexible packaging options for milk, juice and other non-aerated drinks, such as recyclable laminates, standup and pre-made pouches along with holographic or metallic printing and decorative labelling.

- Therefore, with growing consumer preference for on-the-go beverages, flexible packaging is contributing to non-alcoholic beverage packaging market growth.

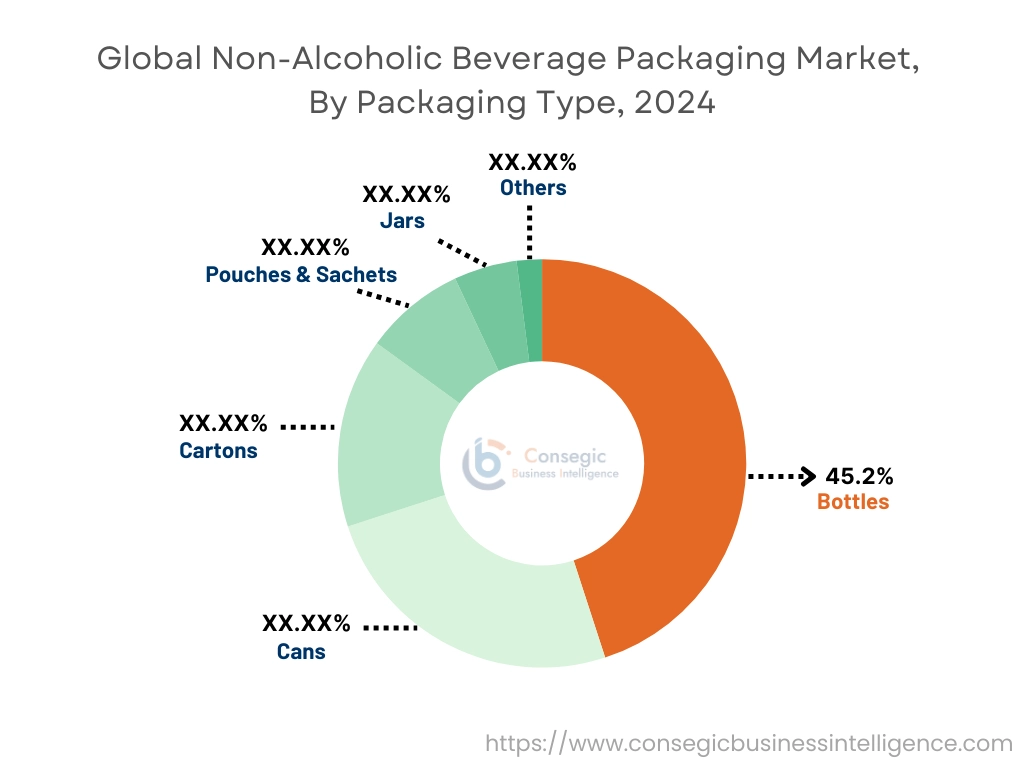

By Packaging Type:

By packaging type, the market is segmented into bottles, cans, cartons, pouches & sachets, jars, and others.

The bottles segment held the largest share of 45.2% in 2024.

- Bottles remain the most widely used packaging type for non-alcoholic beverages, particularly in water, soft drinks, and dairy beverages.

- The need for PET and glass bottles is increasing, driven by consumer preference for convenience and reusability.

- For instance, TricorBraun offers a variety of glass bottles specifically for mocktails.

- Segmental analysis highlights that brands are investing in sustainable bottle designs, including biodegradable and lightweight PET solutions.

- As per non-alcoholic beverage packaging market trends, smart bottles with QR codes and digital engagement features are reshaping consumer interaction.

The pouches & sachets segment is expected to achieve the fastest CAGR during the forecast period.

- Pouches and sachets are gaining traction in functional and energy drinks, as well as in emerging markets where cost-effective packaging is essential.

- The need for lightweight, portable, and sustainable packaging solutions is increasing in health-focused beverage categories.

- Market trends highlight that resealable and compostable pouches are gaining popularity, enhancing sustainability efforts.

- Thus, with increasing focus on waste reduction, flexible packaging solutions are contributing to non-alcoholic beverage packaging market expansion.

By Material:

Based on material, the market is categorized into plastic, glass, metal, paperboard, and biodegradable materials.

The plastic segment held the largest non-alcoholic beverage packaging market share in 2024.

- Plastic packaging, particularly PET bottles, dominates the non-alcoholic beverage industry, offering affordability and versatility.

- The need for lightweight, shatterproof, and cost-effective beverage packaging is increasing across all segments.

- Market analysis highlights that manufacturers are focusing on recyclable and biodegradable plastic alternatives to meet sustainability goals.

- As per segmental trends, refillable and recycled PET initiatives are gaining momentum, reducing plastic waste.

The biodegradable materials segment is expected to experience the fastest CAGR during the forecast period.

- Biodegradable packaging, including plant-based plastics and paper-based alternatives, is gaining popularity among environmentally conscious brands.

- The need for sustainable and compostable beverage packaging is rising as regulations on single-use plastics tighten.

- Non-alcoholic beverage packaging market trends indicate that biodegradable materials are increasingly being used in premium and organic beverage categories.

- Thus, with growing environmental concerns, this segment is driving market growth.

By End-Use Industry:

By end-use industry, the market is segmented into food & beverage manufacturers, retail & supermarkets, catering & foodservice, and others.

The food & beverage manufacturers segment held the largest share in 2024.

- Beverage companies are the primary users of non-alcoholic beverage packaging, ensuring their dominance in the market.

- The demand for customizable, brand-centric packaging solutions is increasing as manufacturers seek to differentiate their products.

- Non-alcoholic beverage packaging market analysis highlights that investment in packaging innovation is enhancing shelf appeal and consumer engagement.

- As per segmental trends, smart and interactive packaging solutions are gaining popularity, particularly in the RTD beverage segment.

The retail & supermarkets segment is expected to have the fastest CAGR during the forecast period.

- Retailers are adopting sustainable and innovative packaging to align with changing consumer preferences.

- The need for convenient, resealable, and visually appealing packaging is increasing in supermarkets and convenience stores.

- Market trends indicate that packaging designed for e-commerce and direct-to-consumer brands is on the rise.

- Thus, with the expansion of digital retail channels, this segment is contributing to non-alcoholic beverage packaging market demand.

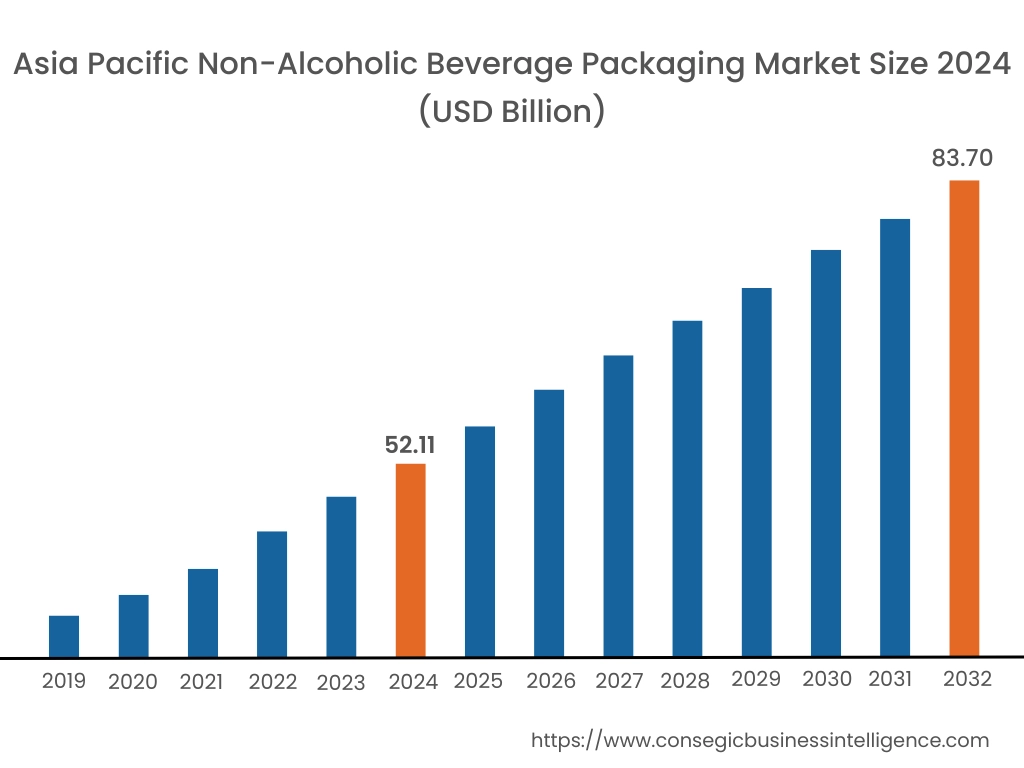

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

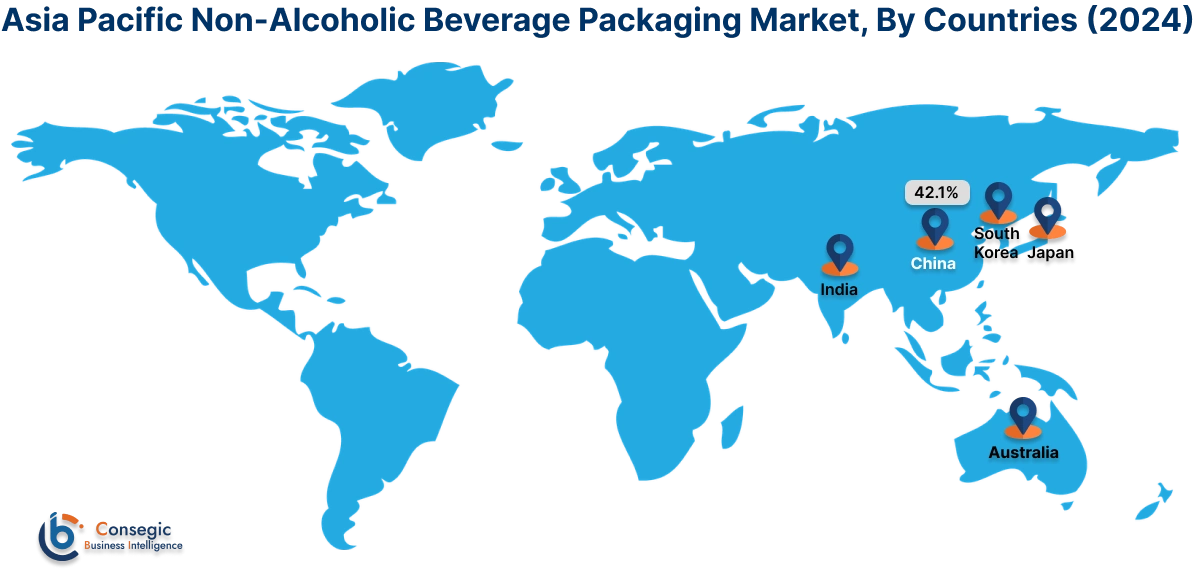

Asia Pacific region was valued at USD 52.11 Billion in 2024. Moreover, it is projected to grow by USD 54.29 Billion in 2025 and reach over USD 83.70 Billion by 2032. Out of this, China accounted for the maximum revenue share of 42.1%. The Asia-Pacific region leads the non-alcoholic beverage packaging industry due to rapid urbanization, rising disposable incomes, and a growing middle-class population. These factors contribute to increased consumption of non-alcoholic beverages, thereby boosting the need for innovative packaging solutions. The region's focus on sustainability and convenience presents a substantial non-alcoholic beverage packaging market opportunity for manufacturers aiming to introduce eco-friendly and functional packaging options.

North America is estimated to reach over USD 89.08 Billion by 2032 from a value of USD 58.70 Billion in 2024 and is projected to grow by USD 60.86 Billion in 2025. North America exhibits a strong non-alcoholic beverage packaging market demand bolstered by sustainable and health-conscious beverage packaging. The presence of major beverage brands and a robust retail infrastructure further support this need in diverse packaging formats, including bottles, cans, and cartons. The region's emphasis on recycling and environmental responsibility also influences packaging choices, aligning with consumer expectations for eco-friendly products.

Europe showcases a mature market with a heightened focus on sustainability and innovation in beverage packaging. Stringent regulations and a strong commitment to reducing environmental impact drive the adoption of recyclable and biodegradable materials. The region's diverse consumer base and evolving lifestyle trends contribute to the demand for convenient and aesthetically appealing packaging solutions, reflecting a sophisticated market landscape.

In Latin America, the market is expanding due to increasing urbanization and a growing young population. The rising popularity of functional and flavored beverages fuels the need for attractive and practical packaging. Manufacturers have the opportunity to cater to this dynamic market by offering cost-effective and innovative packaging solutions that resonate with local preferences and cultural nuances.

The market demand in the Middle East and Africa region is emerging, with significant growth potential. Economic development and a burgeoning middle class drive the consumption of non-alcoholic beverages, leading to increased need for appropriate packaging. Challenges such as varying climatic conditions necessitate durable and protective packaging solutions, offering manufacturers the chance to develop region-specific products that ensure quality and appeal to consumers.

Top Key Players & Market Share Insights:

The non-alcoholic beverage packaging market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global non-alcoholic beverage packaging market. Key players in the non-alcoholic beverage packaging industry include -

- Amcor Group GmbH (Switzerland)

- Tetra Pak Group (Switzerland)

- Crown Holdings, Inc. (USA)

- Mondi PLC (UK)

- O-I Glass, Inc. (USA)

- Ball Corporation (USA)

- Ardagh Group S.A. (Ireland)

- Verallia SA (France)

- Vidrala S.A. (Spain)

- CPMC Holdings Limited (China)

Recent Industry Developments :

Product Launches:

- In December 2024, Lohr Vineyards & Wines announced a new brand identity and packaging for ARIEL Vineyards. This fresh branding aims to reach a new generation of consumers choosing non-alcoholic beverages.

- In November 2024, Ardagh Glass Packaging expanded its Peak bottle collection on its website by launching two new colors of Emerald and Amber. This collection provides manufacturers the flexibility to use the bottles for different beverages without adjustments.

Acquisitions:

- In December 2024, Sonoco Products Company acquired Eviosys, Europe’s leading food cans, ends and closures manufacturer, from KPS Capital Partners. This move supports Sonoco’s strategy to simplify and realign its portfolio to achieve long term growth.

Non-Alcoholic Beverage Packaging Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 274.86 Billion |

| CAGR (2025-2032) | 5.7% |

| By Form |

|

| By Packaging Type |

|

| By Material |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Non-Alcoholic Beverage Packaging Market? +

Non-Alcoholic Beverage Packaging Market size is estimated to reach over USD 274.86 Billion by 2032 from a value of USD 176.95 Billion in 2024 and is projected to grow by USD 183.81 Billion in 2025, growing at a CAGR of 5.7% from 2025 to 2032.

What specific segmentation details are covered in the Non-Alcoholic Beverage Packaging Market report? +

The Non-Alcoholic Beverage Packaging market report includes specific segmentation details for form, packaging type, material and end-use industry.

What are the end-use industry in the Non-Alcoholic Beverage Packaging Market? +

The end-use industry of the Non-Alcoholic Beverage Packaging market are food & beverage manufacturers, retail & supermarkets, catering & foodservice, others.

Who are the major players in the Non-Alcoholic Beverage Packaging Market? +

The key participants in the Non-Alcoholic Beverage Packaging market are Amcor Group GmbH (Switzerland), Tetra Pak Group (Switzerland), Crown Holdings, Inc. (USA), Ball Corporation (USA), Ardagh Group S.A. (Ireland), Verallia SA (France), Vidrala S.A. (Spain), CPMC Holdings Limited (China), Mondi PLC (UK) and O-I Glass, Inc. (USA).