- Summary

- Table Of Content

- Methodology

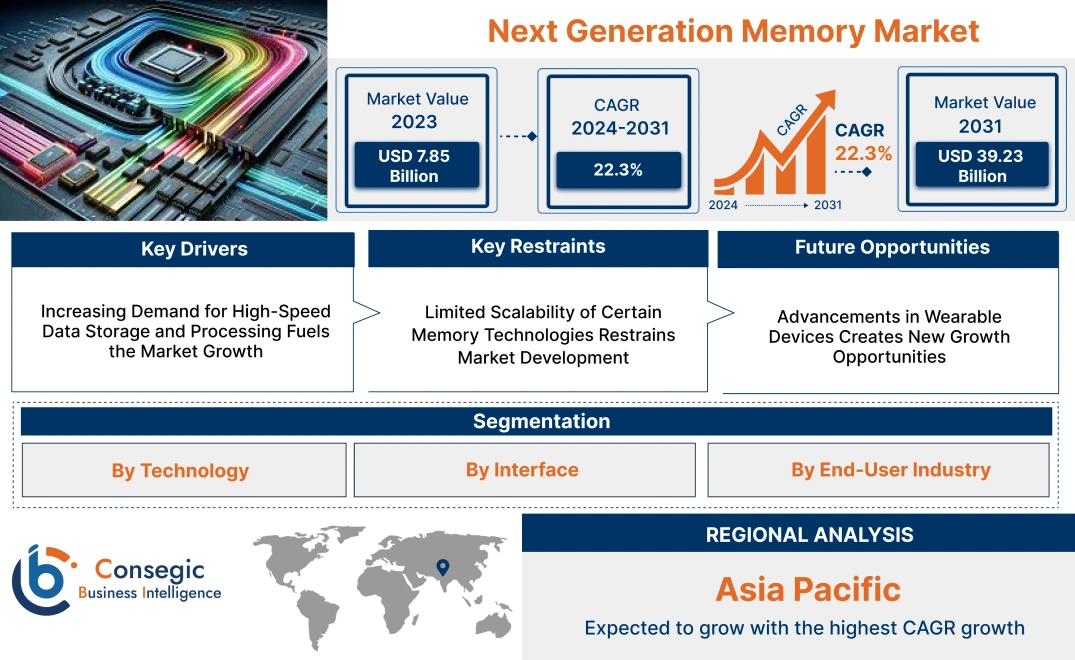

Next Generation Memory Market Size:

Next Generation Memory Market size is estimated to reach over USD 39.23 Billion by 2031 from a value of USD 7.85 Billion in 2023 and is projected to grow by USD 9.46 Billion in 2024, growing at a CAGR of 22.3% from 2024 to 2031.

Next Generation Memory Market Scope & Overview:

Next generation memory encompasses advanced storage technologies designed to overcome the limitations of traditional memory systems in terms of speed, scalability, and energy efficiency. These memory solutions, including MRAM, RRAM, and 3D XPoint, provide high-performance data storage and retrieval capabilities for modern computing applications. They offer non-volatile storage, ensuring data retention even in the absence of power, and are engineered to deliver faster processing speeds and higher endurance compared to conventional memory technologies.

These memory technologies are widely utilized across diverse sectors such as data centers, consumer electronics, automotive systems, and industrial automation. Their architectures are designed to support high-speed computing and large-scale data handling while minimizing power consumption. Furthermore, next generation memory integrates seamlessly with modern processors and systems, enabling compatibility with advanced technologies such as artificial intelligence, machine learning, and IoT devices.

End-users of these memory systems include IT infrastructure providers, consumer electronics manufacturers, and automotive developers, all of whom require efficient, reliable, and scalable memory solutions to enhance system performance and meet the demands of evolving technological ecosystems.

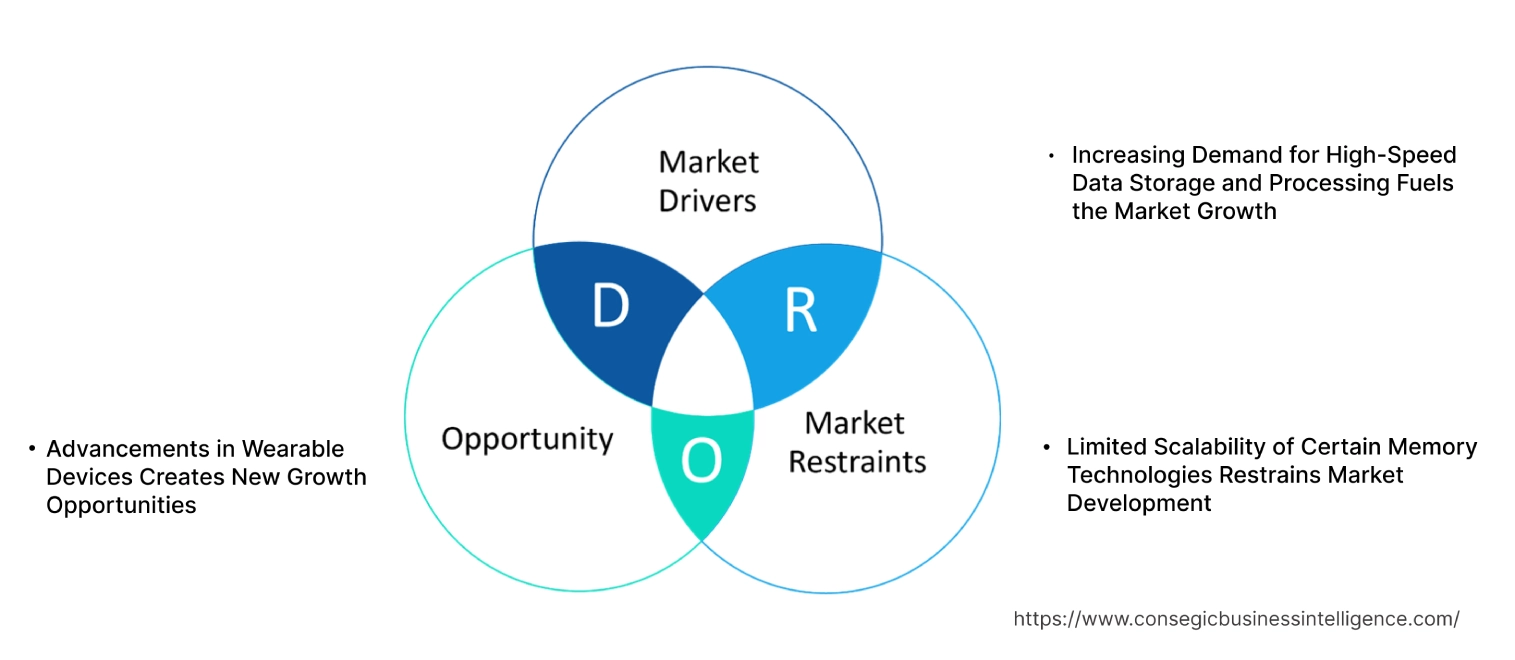

Next Generation Memory MarketDynamics - (DRO) :

Key Drivers:

Increasing Demand for High-Speed Data Storage and Processing Fuels the Market Growth

The rising need for high-speed data storage and processing is a significant driver for the adoption of advanced memory technologies across various industries. Data centers, telecommunications, and financial services handle massive volumes of data that require memory solutions capable of delivering ultra-fast read/write speeds and low latency. For example, data centers supporting cloud computing and virtualization need high-speed memory to process real-time workloads efficiently and ensure seamless user experiences. In financial services, high-frequency trading relies on memory technologies that process large datasets instantly, as even microsecond delays leads to significant financial losses.

Similarly, industries deploying AI and machine learning workloads need memory solutions like MRAM, PCM, and ReRAM, which outperform traditional DRAM and NAND in terms of speed and endurance, making them ideal for real-time data processing and iterative computations. Emerging applications, such as real-time analytics in healthcare and predictive maintenance in manufacturing, also require memory solutions with high bandwidth and low latency. These technologies are becoming indispensable for applications where speed and reliability directly impact operational efficiency and decision-making, driving the next generation memory market growth.

Key Restraints :

Limited Scalability of Certain Memory Technologies Restrains Market Development

Advanced memory technologies, such as Phase Change Memory (PCM) and Resistive RAM (ReRAM), face significant scalability issues when transitioning to higher-density solutions required for data-intensive applications. Unlike traditional memory types like NAND and DRAM, these next-generation technologies encounter difficulties in maintaining material stability at smaller process nodes, which are critical for achieving higher storage capacities. For example, PCM’s reliance on phase-change materials becomes problematic as device scaling introduces variability in switching behavior, reducing performance consistency.

In addition to material constraints, write endurance limitations are a major barrier. Technologies like ReRAM degrade faster with repeated write cycles, which restricts their usability in applications requiring frequent data updates, such as enterprise storage and real-time analytics. These endurance issues hinder their ability to serve as a reliable replacement for well-established memory solutions in high-write environments. Furthermore, the high manufacturing complexity of these advanced technologies exacerbates scalability issues. Achieving consistent yields for higher-capacity devices requires precise control over fabrication processes, increasing production costs and limiting widespread adoption. Consequently, these scalability constraints restrict their competitiveness in markets demanding both high capacity and cost-effectiveness, hampering the next generation memory market demand.

Future Opportunities :

Advancements in Wearable Devices Creates New Growth Opportunities

The rising adoption of advanced wearable devices, such as smartwatches, fitness trackers, AR/VR smart glasses, and medical monitoring devices, offers significant growth opportunities for advanced memory solutions. These devices require compact, energy-efficient memory technologies to support features like real-time data processing, continuous monitoring, and seamless connectivity. Memory solutions such as MRAM and ReRAM are gaining traction due to their low power consumption and fast read/write capabilities, enabling longer battery life and enhanced performance in wearables.

With the increasing need for healthcare-focused wearables, memory technologies are playing a crucial role in storing and processing biometric data, including heart rate, blood oxygen levels, and movement patterns. In AR/VR devices, high-bandwidth memory supports immersive experiences, such as rendering complex visuals and providing real-time interactivity. Furthermore, wearable devices are becoming central to the Internet of Things (IoT) ecosystem, requiring memory that facilitates efficient communication and data exchange. As manufacturers innovate to integrate advanced features into smaller, lightweight devices, the demand for cutting-edge memory technologies tailored for wearables is expected to grow, significantly creating next generation memory market opportunities.

Next Generation Memory Market Segmental Analysis :

By Technology:

Based on technology, the market is segmented into Non-Volatile Memory (ReRAM, MRAM, PCRAM, 3D XPoint) and Volatile Memory (DRAM, SRAM, Others).

The Non-Volatile Memory segment held the largest revenue of share in 2023.

- Non-volatile memory types, such as ReRAM, MRAM, and PCRAM, are widely used in applications requiring data retention without a power supply, including enterprise storage and automotive systems.

- 3D XPoint technology offers high-speed data access and enhanced endurance, making it ideal for advanced computing and AI applications.

- These memory technologies are gaining popularity in sectors like healthcare and aerospace, where reliable and high-capacity storage solutions are essential.

- As per segmental trends analysis, the dominance of non-volatile memory segment is due to its ability to bridge the performance gap between traditional DRAM and NAND storage solutions, boosting the next generation memory market expansion.

The Volatile Memory segment is expected to register the fastest CAGR during the forecast period.

- DRAM and SRAM are widely adopted in consumer electronics and IT applications due to their high-speed data access capabilities.

- These memory types are integral to devices requiring rapid data processing, such as smartphones, gaming consoles, and high-performance computing systems.

- Innovations in volatile memory technologies, such as LPDDR5 and DDR6, are improving performance and energy efficiency, driving adoption in power-sensitive devices.

- As per next generation memory market analysis, the rapid growth of this segment reflects its importance in meeting the increasing performance requirements of modern computing applications.

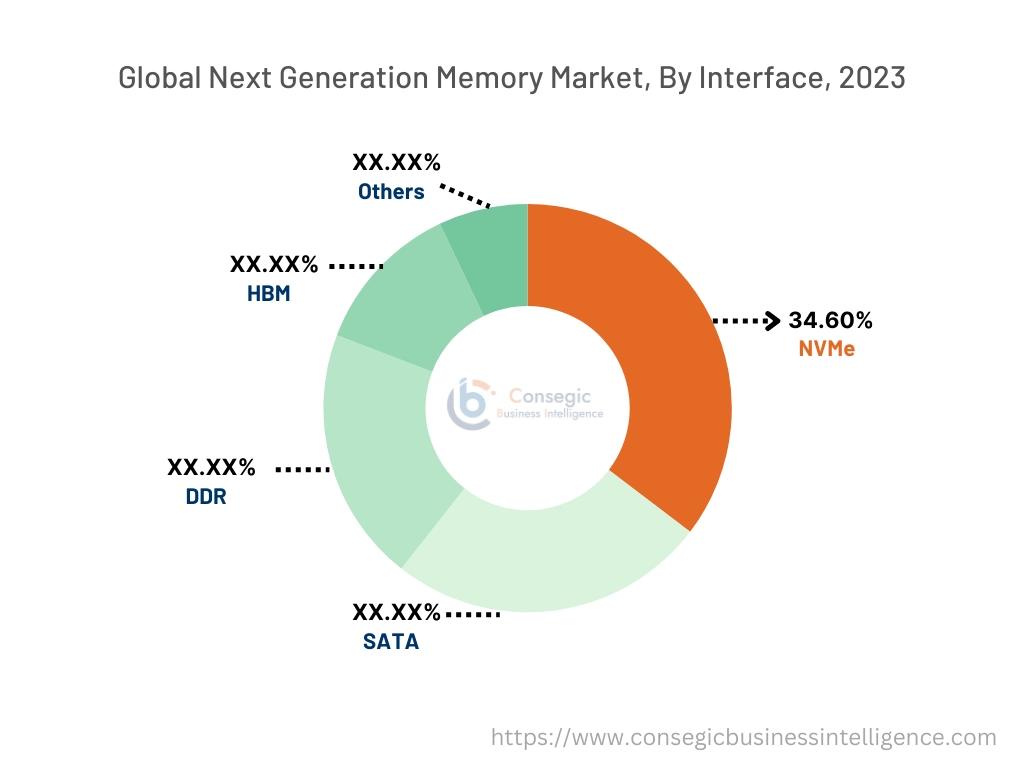

By Interface:

Based on interface, the market is segmented into NVMe, SATA, DDR, HBM, and Others.

The NVMe segment accounted for the largest revenue of 34.60% of the total next generation memory market share in 2023.

- NVMe (Non-Volatile Memory Express) is a high-performance storage interface optimized for SSDs, offering low latency and high throughput.

- The adoption of NVMe is driven by trends in data-intensive applications, including enterprise storage, cloud computing, and big data analytics.

- NVMe-enabled memory solutions are widely used in IT and telecom industries, supporting the growing need for high-speed data transfer in 5G infrastructure.

- As per next generation memory market trends, segment’s dominance reflects its ability to enhance storage performance, making it a preferred choice for modern data centers.

The HBM (High Bandwidth Memory) segment is expected to register the fastest CAGR during the forecast period.

- HBM technology provides ultra-high bandwidth and energy-efficient memory solutions, making it essential for AI, machine learning, and graphics-intensive applications.

- Industries such as automotive and aerospace are adopting HBM for advanced driver assistance systems (ADAS) and simulation technologies.

- The rapid development of this segment is supported by advancements in semiconductor packaging, such as 3D stacking, which improves memory density and performance.

- As per market trends analysis, the adoption of HBM reflects its critical role in enabling next-generation computing and high-performance workloads further contributing to next generation memory market growth.

By End-User Industry:

Based on end-user industry, the market is segmented into IT & Telecom, Healthcare, Automotive, Aerospace & Defense, Consumer Electronics, and Others.

The IT & Telecom segment held the largest revenue of the total next generation memory market share in 2023.

- The IT and telecom sector relies heavily on advanced memory technologies for data centers, cloud storage, and high-speed networking equipment.

- Memory solutions such as NVMe and DDR are essential for supporting 5G infrastructure and edge computing applications.

- Trends in digital transformation and cloud migration are driving the adoption of high-performance memory solutions in this sector.

- As per the market trends analysis, the dominance of this segment reflects its critical role in enabling seamless data management and connectivity across global networks, facilitating the next generation memory market demand.

The Automotive segment is expected to register the fastest CAGR during the forecast period.

- Automotive manufacturers are adopting advanced memory solutions for applications such as autonomous driving, ADAS, and in-car infotainment systems.

- Non-volatile memory types, such as MRAM and 3D XPoint, are gaining traction in automotive applications due to their durability and high-speed data access.

- The segment’s rapid growth is fueled by innovations in electric vehicles (EVs) and connected car technologies, which require efficient memory solutions for real-time data processing.

- The next generation memory market analysis highlights the increasing integration of memory solutions in automotive systems to enhance safety, performance, and user experience.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

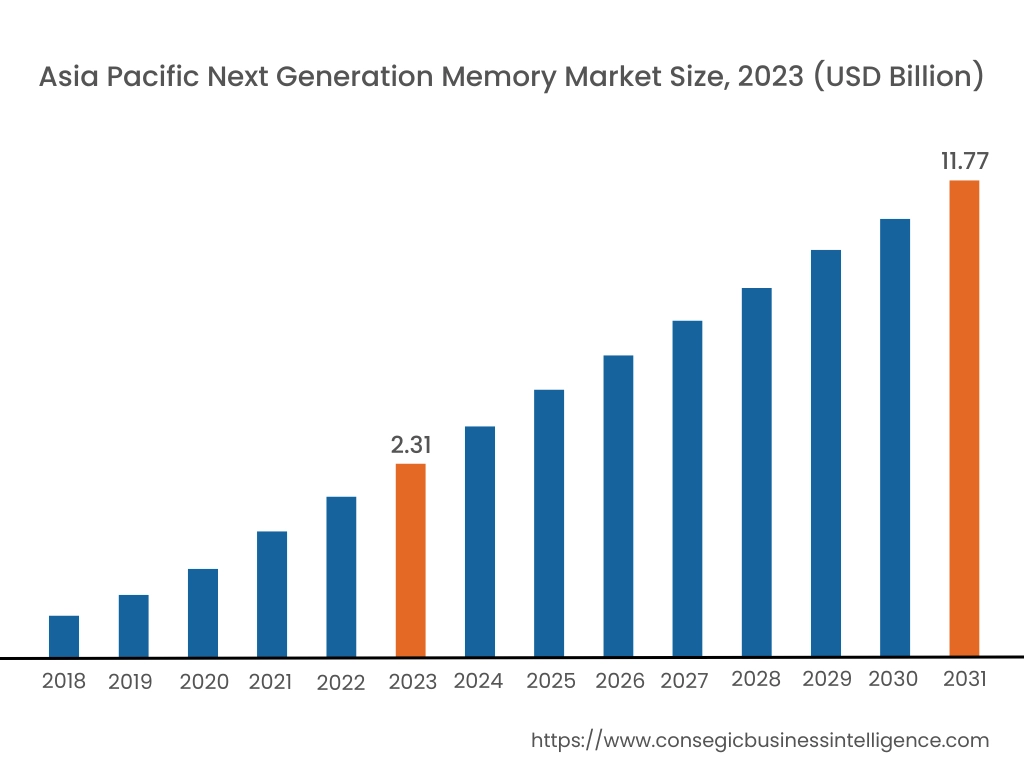

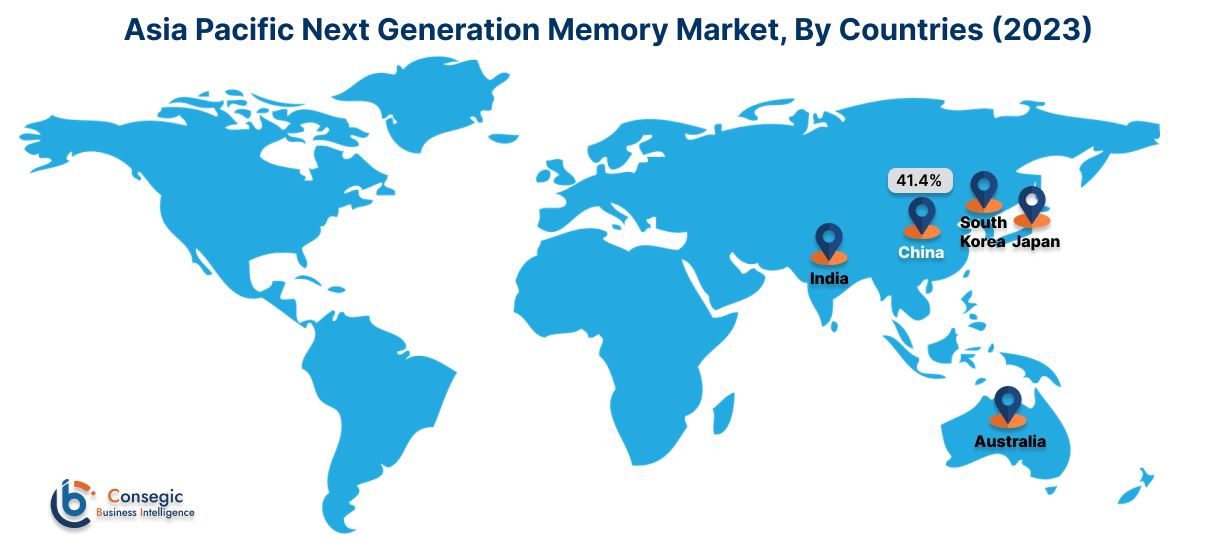

Asia Pacific region was valued at USD 2.31 Billion in 2023. Moreover, it is projected to grow by USD 2.79 Billion in 2024 and reach over USD 11.77 Billion by 2031. Out of these, China accounted for the largest share of 41.4% in 2023. Asia-Pacific emerges as a dynamic hub for next-generation memory technologies, propelled by rapid industrialization and the expansion of consumer electronics markets in countries like China, Japan, and South Korea. The region's focus on developing smart devices and IoT applications has led to increased utilization of advanced memory solutions. Government support and substantial investments in semiconductor manufacturing have further bolstered the next generation memory market opportunities.

North America is estimated to reach over USD 12.91 Billion by 2031 from a value of USD 2.61 Billion in 2023 and is projected to grow by USD 3.14 Billion in 2024. This region maintains a significant position in the next-generation memory sector, primarily due to its robust technological infrastructure and the presence of leading semiconductor companies. The United States, in particular, has seen substantial investments in research and development, fostering innovations in memory technologies such as MRAM and ReRAM. As per next generation memory market trends, the integration of these advanced memory solutions into data centers and enterprise storage systems is prevalent, driven by the need for high-performance computing.

Europe plays a pivotal role in the next-generation memory landscape, with countries like Germany, France, and the United Kingdom leading in technological adoption. The region's emphasis on energy efficiency and data security has accelerated the implementation of non-volatile memory solutions in automotive and industrial applications. As per the market trends analysis, collaborative initiatives between research institutions and industry players have been instrumental in advancing memory technologies.

The Middle East & Africa region is gradually integrating next-generation memory technologies, particularly in sectors like telecommunications and energy. Countries such as the United Arab Emirates and South Africa are investing in digital infrastructure, contributing to the next generation memory market expansion.

Latin America is exploring the potential of next-generation memory solutions, with Brazil and Mexico at the forefront. The growing IT and telecommunications sectors in these countries are recognizing the benefits of advanced memory technologies for enhancing data processing capabilities.

Top Key Players & Market Share Insights:

The next generation memory market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global next generation memory market. Key players in the next generation memory industry include –

- Samsung Electronics Co., Ltd. (South Korea)

- Micron Technology, Inc. (USA)

- SK hynix Inc. (South Korea)

- Intel Corporation (USA)

- Fujitsu Limited (Japan)

- Kioxia Holdings Corporation (Japan)

- Western Digital Corporation (USA)

- Seagate Technology Holdings PLC (USA)

- Toshiba Corporation (Japan)

- NVIDIA Corporation (USA)

Recent Industry Developments :

Product Launches:

- In November 2024, Renesas unveiled the industry's first complete memory interface chipset solutions, featuring second-generation DDR5 memory. The solution, designed for high-performance computing and AI, improves memory bandwidth and efficiency. With optimized power management and reduced latency, these chipsets support advanced applications, such as data centers and autonomous systems. The innovative design ensures compatibility with DDR5 memory modules, offering faster data processing, and scalability, crucial for next-gen computing environments.

- In November 2024, Samsung developed the industry's first 24GB GDDR7 DRAM, designed for next-generation AI computing. This advanced memory solution offers significantly higher bandwidth and efficiency compared to previous generations, enabling faster data processing and enhanced performance for AI-driven applications. The 24GB GDDR7 DRAM is optimized for data-intensive tasks like machine learning, deep learning, and high-performance computing, paving the way for more powerful AI systems.

- In October 2024, Micron announced the launch of its ultra-fast clock driver for DDR5, designed to fuel the next generation of AI-powered PCs. The new product promises enhanced performance by delivering higher bandwidth and faster memory speeds, addressing the increasing needs of artificial intelligence and data-intensive applications. Micron's innovation aims to optimize memory systems for AI-driven workloads, providing a significant boost in computing efficiency.

- In October 2024, SKILL launched its Trident Z5 CK Series, a new range of overclocked DDR5 CU-DIMM memory modules. These modules feature a built-in clock driver, allowing them to achieve extreme speeds up to DDR5-9600. This innovation provides enhanced stability and higher performance, especially for gamers, overclockers, and PC enthusiasts seeking the best in memory performance. The Trident Z5 CK Series is designed to push the limits of DDR5, delivering superior bandwidth for demanding applications, gaming, and content creation tasks.

Partnerships & Collaborations:

- In April 2024, SK hynix partnered with TSMC to enhance its leadership in High Bandwidth Memory (HBM) technology. This collaboration aims to leverage TSMC’s advanced semiconductor fabrication capabilities, accelerating the development and production of next-gen HBM solutions. By combining SK hynix's expertise in memory technology with TSMC's cutting-edge manufacturing, the partnership is set to drive innovation in high-performance computing, AI, and data center applications.

Next Generation Memory Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 39.23 Billion |

| CAGR (2024-2031) | 22.3% |

| By Technology |

|

| By Interface |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Next Generation Memory Market? +

Next Generation Memory Market size is estimated to reach over USD 39.23 Billion by 2031 from a value of USD 7.85 Billion in 2023 and is projected to grow by USD 9.46 Billion in 2024, growing at a CAGR of 22.3% from 2024 to 2031.

What specific segmentation details are covered in the Next Generation Memory Market report? +

The Next Generation Memory Market report includes segmentation details by technology (Non-Volatile Memory: ReRAM, MRAM, PCRAM, 3D XPoint; Volatile Memory: DRAM, SRAM, Others), interface (NVMe, SATA, DDR, HBM, Others), end-user industry (IT & Telecom, Healthcare, Automotive, Aerospace & Defense, Consumer Electronics, Others), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which is the fastest-growing segment in the Next Generation Memory Market? +

The HBM (High Bandwidth Memory) segment is expected to grow rapidly during the forecast period. HBM technology provides ultra-high bandwidth and energy-efficient memory solutions, making it essential for AI, machine learning, and graphics-intensive applications.

Who are the major players in the Next Generation Memory Market? +

The major players in the Next Generation Memory Market include Samsung Electronics Co., Ltd. (South Korea), Micron Technology, Inc. (USA), SK hynix Inc. (South Korea), Intel Corporation (USA), Fujitsu Limited (Japan), Kioxia Holdings Corporation (Japan), Western Digital Corporation (USA), Seagate Technology Holdings PLC (USA), Toshiba Corporation (Japan), and NVIDIA Corporation (USA).