- Summary

- Table Of Content

- Methodology

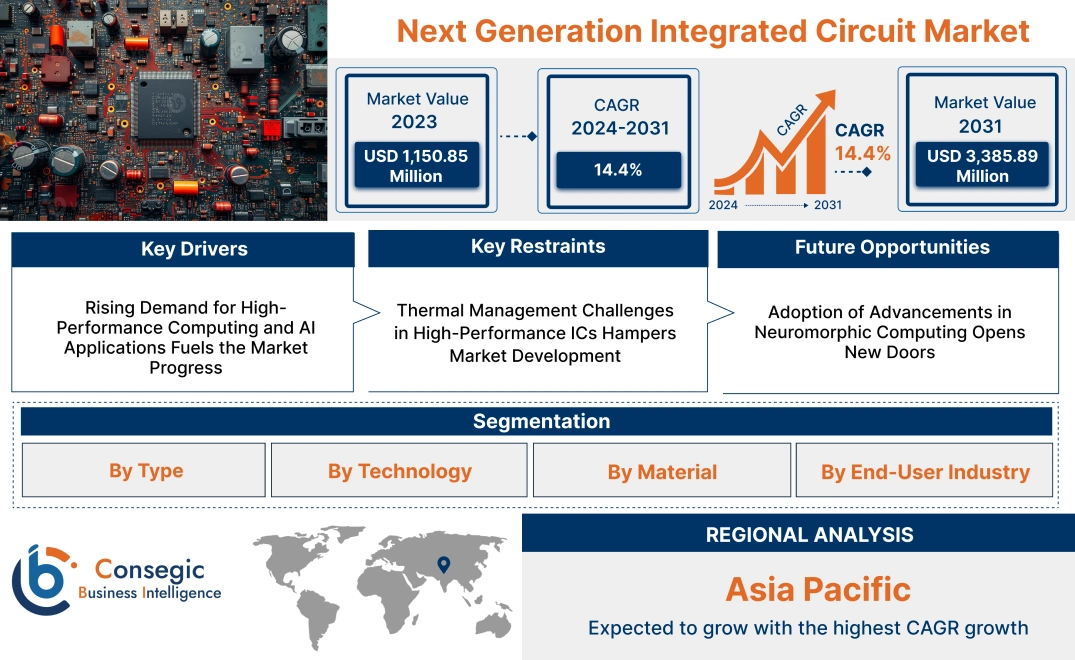

Next Generation Integrated Circuit Market Size:

Next Generation Integrated Circuit Market size is estimated to reach over USD 3,385.89 Million by 2031 from a value of USD 1,150.85 Million in 2023 and is projected to grow by USD 1,283.15 Million in 2024, growing at a CAGR of 14.4% from 2024 to 2031.

Next Generation Integrated Circuit Market Scope & Overview:

Next generation integrated circuits represent advanced semiconductor devices designed to deliver enhanced performance, efficiency, and functionality for modern electronic systems. These circuits are developed using cutting-edge technologies, enabling higher processing speeds, lower power consumption, and improved scalability. They are widely utilized in applications such as consumer electronics, telecommunications, automotive systems, and industrial automation, where high-performance computing and compact designs are essential.

These circuits incorporate advanced architectures and materials to support features such as miniaturization, multi-functionality, and compatibility with emerging technologies like artificial intelligence and IoT. They are produced using innovative fabrication techniques, ensuring reliability and durability under various operational conditions. These advancements make next generation circuits suitable for both high-demand commercial applications and critical industrial operations.

End-users of these circuits include electronic device manufacturers, telecommunication providers, and automotive system developers, who rely on them to enhance product capabilities, improve system performance, and meet evolving technological requirements.

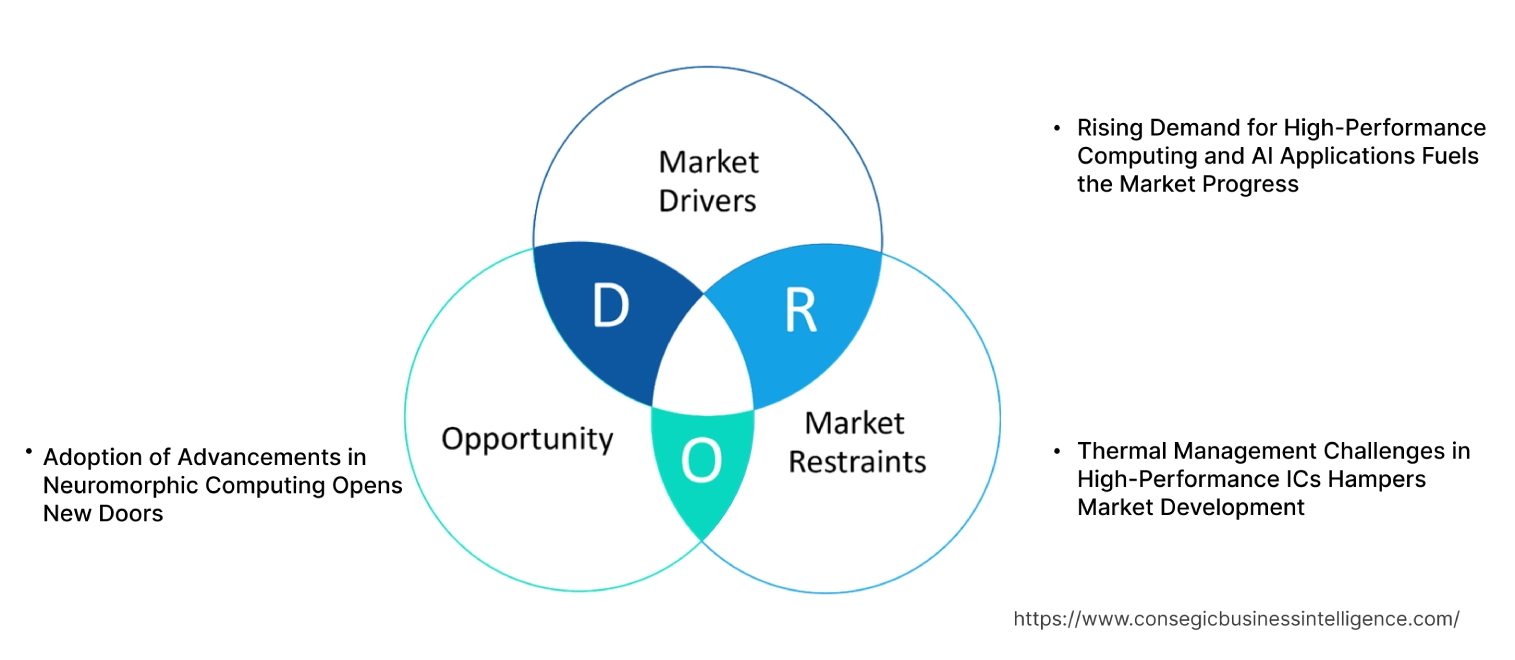

Next Generation Integrated Circuit Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for High-Performance Computing and AI Applications Fuels the Market Progress

The growing adoption of high-performance computing (HPC) and artificial intelligence (AI) applications is a key driver for the market, as industries increasingly rely on advanced computing systems to handle complex, data-intensive tasks. In healthcare, HPC-powered systems facilitate predictive analytics for disease modeling, drug discovery, and genome sequencing, requiring integrated circuits (ICs) that manage vast amounts of data with precision. Similarly, the automotive sector depends on AI-driven systems for autonomous driving, leveraging ICs to process real-time sensor data, navigation algorithms, and safety mechanisms.

Financial services also benefit from AI-enabled modeling and fraud detection, which demand ICs with high computational efficiency. Modern ICs, such as system-on-chip (SoC) and application-specific integrated circuits (ASICs), are engineered to meet these needs by delivering high-speed data processing and low latency. Specifically, AI workloads require specialized components like neural network accelerators and tensor processing units (TPUs) to optimize deep learning and machine learning operations. The growing need for such high-performance ICs is driving significant innovation, enabling industries to achieve breakthroughs in speed, accuracy, and scalability, fueling next generation integrated circuit market growth.

Key Restraints :

Thermal Management Challenges in High-Performance ICs Hampers Market Development

Next-generation integrated circuits, especially those used in high-performance computing (HPC), artificial intelligence (AI), and data-intensive applications, generate substantial heat during operation due to their compact designs and increased power densities. As ICs become smaller and more powerful, the dissipation of heat becomes increasingly difficult. Without effective thermal management, excessive heat leads to degraded performance, reduced efficiency, and even system failures, posing significant constraints for industries relying on these advanced circuits.

Traditional cooling methods, such as air or liquid cooling, are often inadequate for managing the thermal loads of modern ICs. Advanced cooling techniques, such as vapor chambers, thermoelectric coolers, and even immersion cooling, are being explored, but they significantly increase costs and complexity. The need for efficient, compact, and cost-effective thermal management solutions is particularly critical in industries like autonomous vehicles, data centers, and IoT, where space constraints and continuous operation exacerbate the issue. These restraints not only deter the adoption of high-performance ICs in cost-sensitive markets but also hinder their scalability for applications demanding reliability, precision, and long-term durability, hampering next generation integrated circuit market demand.

Future Opportunities :

Adoption of Advancements in Neuromorphic Computing Opens New Doors

Neuromorphic computing, a technology inspired by the functioning of the human brain, is revolutionizing how complex computing tasks are handled, particularly in scenarios requiring real-time decision-making and energy efficiency. Unlike traditional computing architectures, neuromorphic systems use specialized circuits to emulate neural networks, enabling faster processing with significantly lower power consumption. These systems are particularly well-suited for next-generation integrated circuits that are designed to handle dynamic and resource-intensive tasks.

Neuromorphic ICs are finding increasing applications in robotics, where real-time sensory processing and decision-making are essential for tasks such as navigation, object recognition, and autonomous operations. In autonomous vehicles, these ICs enhance systems like adaptive control and obstacle detection by processing complex data in milliseconds. Similarly, in edge computing, neuromorphic ICs allow localized data processing, reducing latency and dependency on cloud-based systems, which is crucial for IoT and smart devices. As the need for intelligent, energy-efficient computing grows across industries, advancements in neuromorphic ICs are driving innovation, offering next generation integrated circuit market opportunities.

Next Generation Integrated Circuit Market Segmental Analysis :

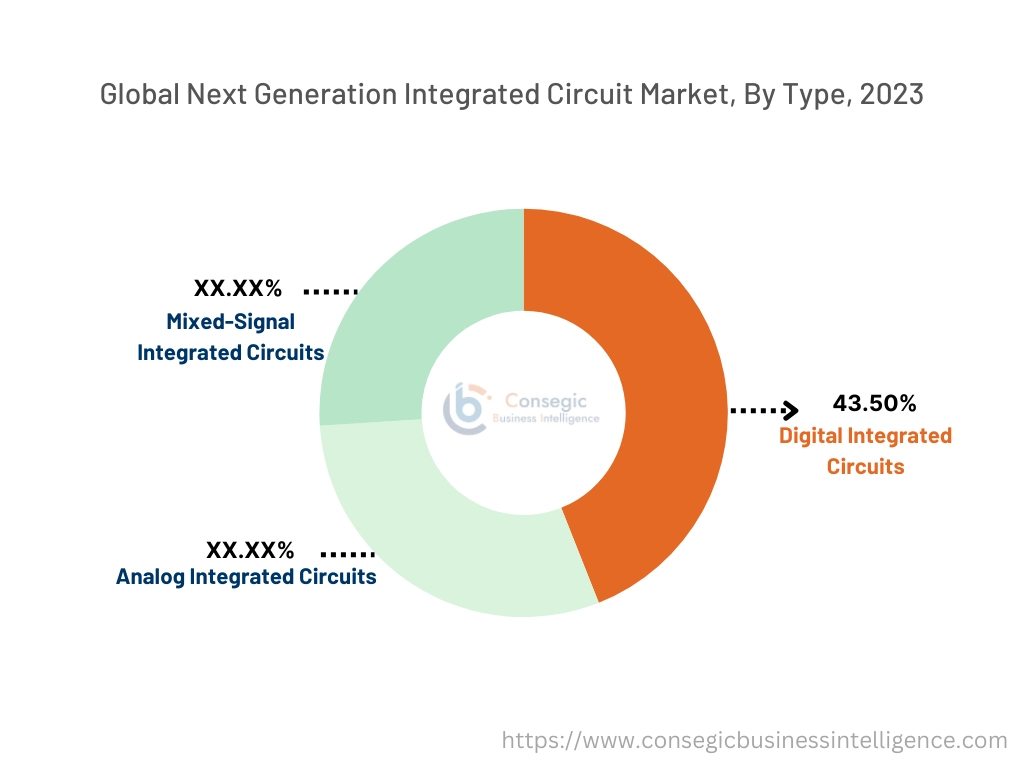

By Type:

Based on type, the market is segmented into Analog Integrated Circuits, Digital Integrated Circuits, and Mixed-Signal Integrated Circuits.

The Digital Integrated Circuits segment accounted for the largest revenue of 43.50% of the total next generation integrated circuit market share in 2023.

- Digital ICs are fundamental to modern computing and communication technologies, powering applications like microprocessors, memory chips, and logic circuits.

- Their widespread use in consumer electronics and IT & telecom drives the dominance of this segment, supported by innovations in semiconductor fabrication techniques.

- Digital ICs offer enhanced speed, energy efficiency, and scalability, making them indispensable for high-performance computing and data centers.

- As per market analysis, advancements in miniaturization technologies, such as 7nm and 5nm nodes, continue to strengthen the position of digital ICs in various industries, driving next generation integrated circuit market expansion.

The Mixed-Signal Integrated Circuits segment is expected to register the fastest CAGR during the forecast period.

- Mixed-signal ICs integrate analog and digital functions on a single chip, optimizing performance for applications like automotive systems and IoT devices.

- Their adoption is growing in the healthcare and automotive sectors, where precise analog-digital signal conversion is critical for medical devices and autonomous systems.

- Trends in connected devices and smart sensors are fueling the demand for mixed-signal ICs, ensuring their rapid growth across diverse applications.

- As per next generation integrated circuit market trends, the versatility of mixed-signal ICs positions them as a key component in next-generation technologies, particularly in emerging markets.

By Technology:

Based on technology, the market is segmented into System-on-Chip (SoC), Multi-Chip Module (MCM), 3D Integrated Circuits (3D ICs), and Application-Specific Integrated Circuits (ASICs).

The System-on-Chip (SoC) segment held the largest revenue next generation integrated circuit market share in 2023.

- SoCs integrate multiple components, including processors, memory, and peripherals, onto a single chip, offering compact and energy-efficient solutions.

- These ICs are widely used in smartphones, wearables, and consumer electronics, driving their dominance in the market.

- SoCs support high-speed communication and advanced computing, making them a preferred choice for AI and machine learning applications.

- As per industry trends, the increasing adoption of SoCs in automotive applications, including infotainment and advanced driver assistance systems (ADAS), is further boosting the segment, driving next generation integrated circuit market growth.

The 3D Integrated Circuits (3D ICs) is expected to register the fastest CAGR during the forecast period.

- 3D ICs use vertical stacking of components, enabling higher performance and reduced power consumption compared to traditional 2D designs.

- These ICs are essential for high-performance computing, big data analytics, and cloud infrastructure, where efficiency and processing power are critical.

- Advancements in Through-Silicon Via (TSV) technology are enhancing the reliability and scalability of 3D ICs for data-intensive applications.

- As per next generation integrated circuit market analysis, the rapid growth of this segment reflects its potential to address the challenges of miniaturization and heat dissipation in next-generation applications.

By Material:

Based on material, the market is segmented into Silicon, Silicon Carbide (SiC), Gallium Nitride (GaN), and Others.

The Silicon segment accounted for the largest revenue share in 2023.

- Silicon remains the most widely used material in integrated circuit fabrication due to its excellent semiconductor properties, cost-effectiveness, and scalability.

- Its dominance is supported by widespread adoption in consumer electronics, automotive systems, and telecommunications equipment.

- The integration of silicon in advanced technologies, such as FinFETs and SOI (Silicon-on-Insulator), enhances its relevance in high-performance ICs.

- Trends in semiconductor manufacturing highlight the continued innovations in silicon processing to meet the evolving needs of modern applications, fueling next generation integrated circuit market demand.

The Gallium Nitride (GaN) segment is expected to register the fastest CAGR during the forecast period.

- GaN materials offer superior electrical conductivity and heat resistance compared to traditional silicon, making them ideal for high-frequency and power applications.

- These materials are widely adopted in aerospace and defense for radar systems, satellite communication, and electronic warfare.

- The increasing use of GaN in power electronics and 5G infrastructure supports its growth trajectory in the market.

- Market analysis indicates the growing potential of GaN-based ICs to revolutionize high-power and high-frequency applications across industries, driving next generation integrated circuit market expansion.

By End-User Industry:

Based on end-user industry, the market is segmented into IT & Telecom, Automotive, Healthcare, Consumer Electronics, Aerospace & Defense, and Others.

The IT & Telecom segment held the largest revenue share in 2023.

- The IT & telecom sector relies heavily on integrated circuits for networking equipment, data centers, and 5G infrastructure, driving this segment's dominance.

- Advanced ICs support high-speed data transfer, signal processing, and real-time analytics, essential for modern telecom systems.

- Trends in cloud computing and edge infrastructure highlight the critical role of ICs in enabling efficient and scalable IT networks.

- This segment's dominance reflects its critical contribution to the global digital transformation and connected ecosystems, creating next generation integrated circuit market opportunities.

The Automotive segment is expected to register the fastest CAGR during the forecast period.

- Automotive manufacturers are adopting advanced ICs for autonomous driving, ADAS, and in-car connectivity systems.

- Innovations in EV powertrain technologies rely heavily on specialized ICs, such as power management and sensor integration circuits.

- The segment's rapid expansion is driven by trends emphasizing vehicle electrification and the adoption of advanced safety systems.

- The next generation integrated circuit market analysis underscores the importance of ICs in addressing the evolving requirements of modern vehicles, enhancing safety, efficiency, and performance.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

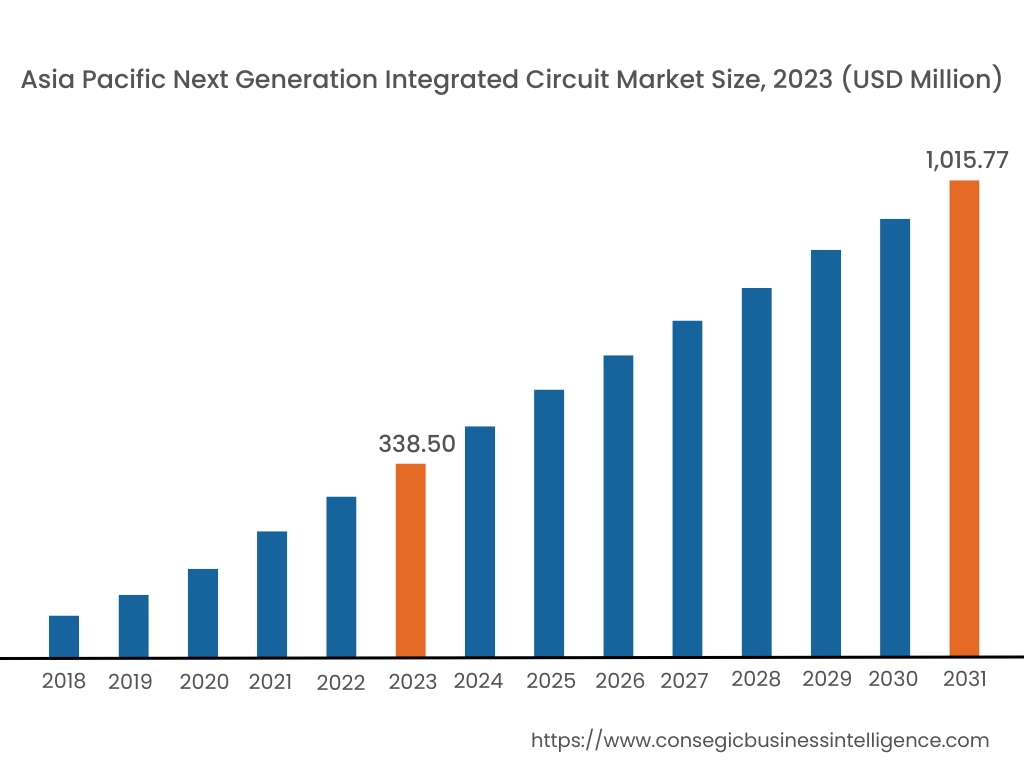

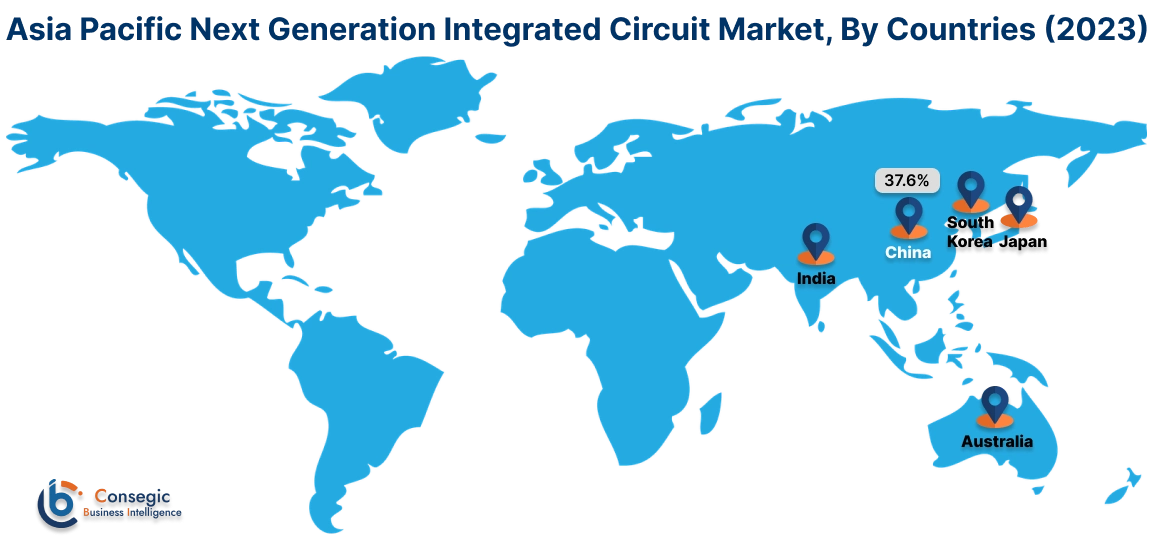

Asia Pacific region was valued at USD 338.50 Million in 2023. Moreover, it is projected to grow by USD 378.05 Million in 2024 and reach over USD 1,015.77 Million by 2031. Out of which, China accounted for the largest share of 37.6% in 2023. Asia-Pacific is witnessing rapid advancements in the next-generation IC market, driven by countries such as China, Japan, and South Korea. The region has become a global hub for semiconductor manufacturing, with a strong focus on consumer electronics, telecommunications, and automotive industries. As per next generation integrated circuit market trends, government initiatives promoting digitalization and technological self-reliance contribute to the market's momentum.

North America is estimated to reach over USD 1,113.96 Million by 2031 from a value of USD 382.53 Million in 2023 and is projected to grow by USD 426.15 Million in 2024. This region maintains a significant position in the next-generation IC market, primarily due to its robust technological infrastructure and the presence of leading semiconductor companies. The United States, in particular, is at the forefront, with substantial investments in research and development fostering innovation in integrated circuit technologies. As per market analysis, the emphasis on artificial intelligence, Internet of Things (IoT), and 5G technologies propels the adoption of advanced ICs.

Europe contributes notably to the global next-generation IC market, with countries like Germany, France, and the United Kingdom leading in terms of technological adoption and innovation. The region benefits from a strong emphasis on automotive electronics, industrial automation, and renewable energy sectors, which utilize advanced integrated circuits. Initiatives like the European Union's focus on digital transformation and sustainability further support the market.

The Middle East & Africa region shows emerging potential in the next-generation IC market, particularly in countries like the United Arab Emirates, Saudi Arabia, and South Africa. Investments in smart city projects, renewable energy, and technological innovation are fostering the adoption of advanced integrated circuits. The market analysis shows that the focus on diversifying economies and reducing dependence on oil revenues has led to growth in the technology sector.

Latin America is an emerging market for next-generation ICs, with Brazil and Mexico being the primary growth drivers. The rising adoption of consumer electronics, improving infrastructure, and increasing focus on digital transformation contribute to the market’s progression. Government initiatives aimed at modernizing technology infrastructure and promoting innovation are supporting market progress.

Top Key Players & Market Share Insights:

The Next Generation Integrated Circuit market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Next Generation Integrated Circuit market. Key players in the Next Generation Integrated Circuit industry include –

- NVIDIA Corporation (USA)

- Advanced Micro Devices, Inc. (AMD) (USA)

- Intel Corporation (USA)

- Qualcomm Incorporated (USA)

- Broadcom Inc. (USA)

- Samsung Electronics Co., Ltd. (South Korea)

- Taiwan Semiconductor Manufacturing Company Limited (TSMC) (Taiwan)

- Micron Technology, Inc. (USA)

- SK hynix Inc. (South Korea)

- Texas Instruments Incorporated (USA)

Recent Industry Developments :

- In January 2024, Siemens Digital Industries Software introduced the Solido™ Simulation Suite, a cutting-edge platform for analog, mixed-signal, and RF integrated circuit (IC) design. The suite integrates advanced simulation and machine learning technologies, enabling IC designers to achieve higher accuracy and efficiency in performance verification. Additionally, the suite supports a wide range of use cases, from low-power IC design to high-frequency RF applications, catering to the needs of next-generation semiconductors.

- In October 2024, Rambus introduced the industry's first complete chipsets for DDR5 MRDIMMs and RDIMMs, delivering enhanced performance for data centers and AI workloads. These chipsets optimize memory throughput and efficiency, supporting next-generation server and computing systems. By enabling higher bandwidth and lower latency, Rambus aims to address the growing needs of data-intensive applications. The solution underscores the company’s commitment to advancing memory technologies for critical AI and data center infrastructure.

- In October 2023, Macroblock debuts its next-gen LED driver ICs, MBI5762 and MBI5780, designed for high-end LED displays. The MBI5762 targets XR/VP applications with 240 FPS support, 16-bit grayscale, and enhanced visual performance. The MBI5780 supports super-fine-pitch mini-/micro-LEDs with a 90-scan design, reducing power consumption and thermal issues. Both ICs leverage proprietary DLL frequency-boosting technology for efficiency and performance, addressing industry demands for higher resolutions and lower costs in LED displays.

- In July 2023, Samsung introduced the industry's first GDDR7 DRAM, designed to enhance next-gen graphics performance. Boasting speeds of 32Gbps per pin and bandwidth exceeding 1.5TBps, it targets applications like AI, high-performance computing, and graphics cards. The DRAM utilizes PAM3 signaling for improved efficiency and features a low-operating voltage mode to reduce power consumption by 20%. Samsung plans to optimize the product for diverse customer needs, marking a leap in graphics and computing technologies.

Next Generation Integrated Circuit Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 3,385.89 Million |

| CAGR (2024-2031) | 14.4% |

| By Type |

|

| By Technology |

|

| By Material |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Next Generation Integrated Circuit Market? +

Next Generation Integrated Circuit Market size is estimated to reach over USD 3,385.89 Million by 2031 from a value of USD 1,150.85 Million in 2023 and is projected to grow by USD 1,283.15 Million in 2024, growing at a CAGR of 14.4% from 2024 to 2031.

What specific segmentation details are covered in the Next Generation Integrated Circuit Market report? +

The Next Generation Integrated Circuit Market report includes segmentation details by type (Analog Integrated Circuits, Digital Integrated Circuits, Mixed-Signal Integrated Circuits), technology (System-on-Chip (SoC), Multi-Chip Module (MCM), 3D Integrated Circuits (3D ICs), Application-Specific Integrated Circuits (ASICs)), material (Silicon, Silicon Carbide (SiC), Gallium Nitride (GaN), Others), end-user industry (IT & Telecom, Automotive, Healthcare, Consumer Electronics, Aerospace & Defense, Others), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which is the fastest-growing segment in the Next Generation Integrated Circuit Market? +

The 3D Integrated Circuits (3D ICs) segment is expected to grow rapidly during the forecast period. These ICs offer higher performance and reduced power consumption, which are crucial for high-performance computing, big data analytics, and cloud infrastructure.

Who are the major players in the Next Generation Integrated Circuit Market? +

The major players in the Next Generation Integrated Circuit Market include NVIDIA Corporation (USA), Advanced Micro Devices, Inc. (AMD) (USA), Intel Corporation (USA), Qualcomm Incorporated (USA), Broadcom Inc. (USA), Samsung Electronics Co., Ltd. (South Korea), Taiwan Semiconductor Manufacturing Company Limited (TSMC) (Taiwan), Micron Technology, Inc. (USA), SK hynix Inc. (South Korea), and Texas Instruments Incorporated (USA).