- Summary

- Table Of Content

- Methodology

Next Generation Data Storage Technologies Market Scope & Overview:

Next generation data storage technologies encompass advanced systems and methods designed to store, manage, and retrieve data with enhanced efficiency, scalability, and reliability. These technologies include solid-state drives (SSD), storage area networks (SAN), network-attached storage (NAS), and cloud-based storage solutions, offering superior performance compared to traditional storage systems. They are built to handle vast amounts of data generated across various industries, ensuring quick access and secure management.

These technologies integrate features such as high-speed data transfer, real-time data analysis, and compatibility with advanced IT infrastructures. They cater to applications in sectors like IT and telecommunications, healthcare, finance, and media, where seamless data storage and retrieval are essential. Advanced systems also incorporate artificial intelligence and machine learning algorithms to optimize storage utilization and improve operational efficiency.

End-users of these storage solutions include enterprises, data centers, and government organizations, which rely on cutting-edge storage technologies to support data-driven decision-making, enhance security, and ensure continuity in their operations.

Next Generation Data Storage Technologies Market Size:

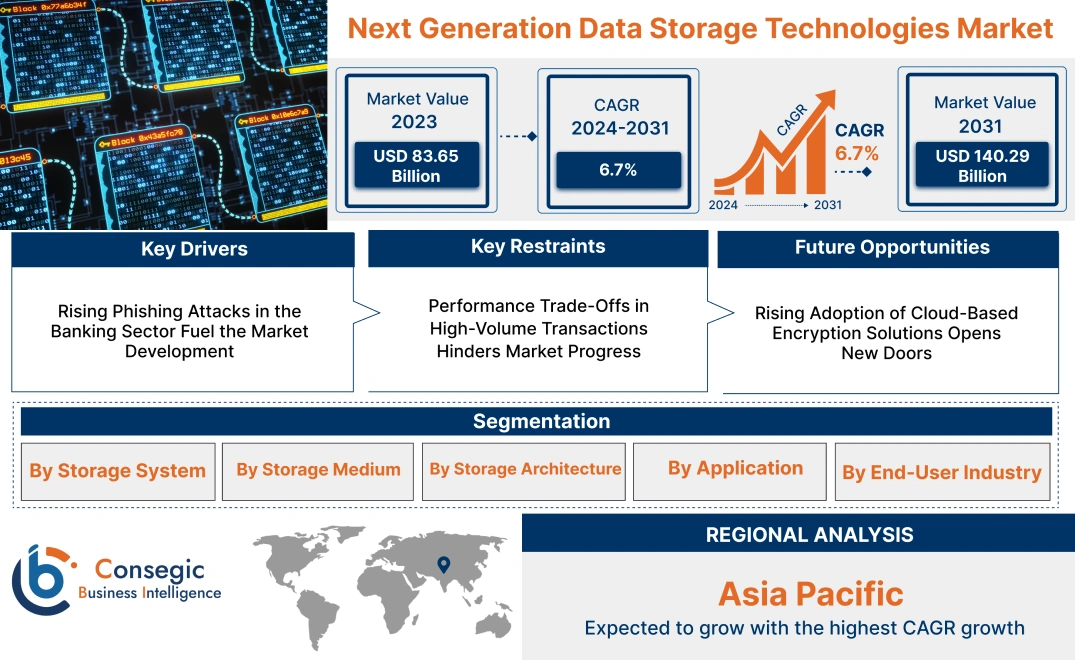

Next Generation Data Storage Technologies Market size is estimated to reach over USD 140.29 Billion by 2031 from a value of USD 83.65 Billion in 2023 and is projected to grow by USD 87.75 Billion in 2024, growing at a CAGR of 6.7% from 2024 to 2031.

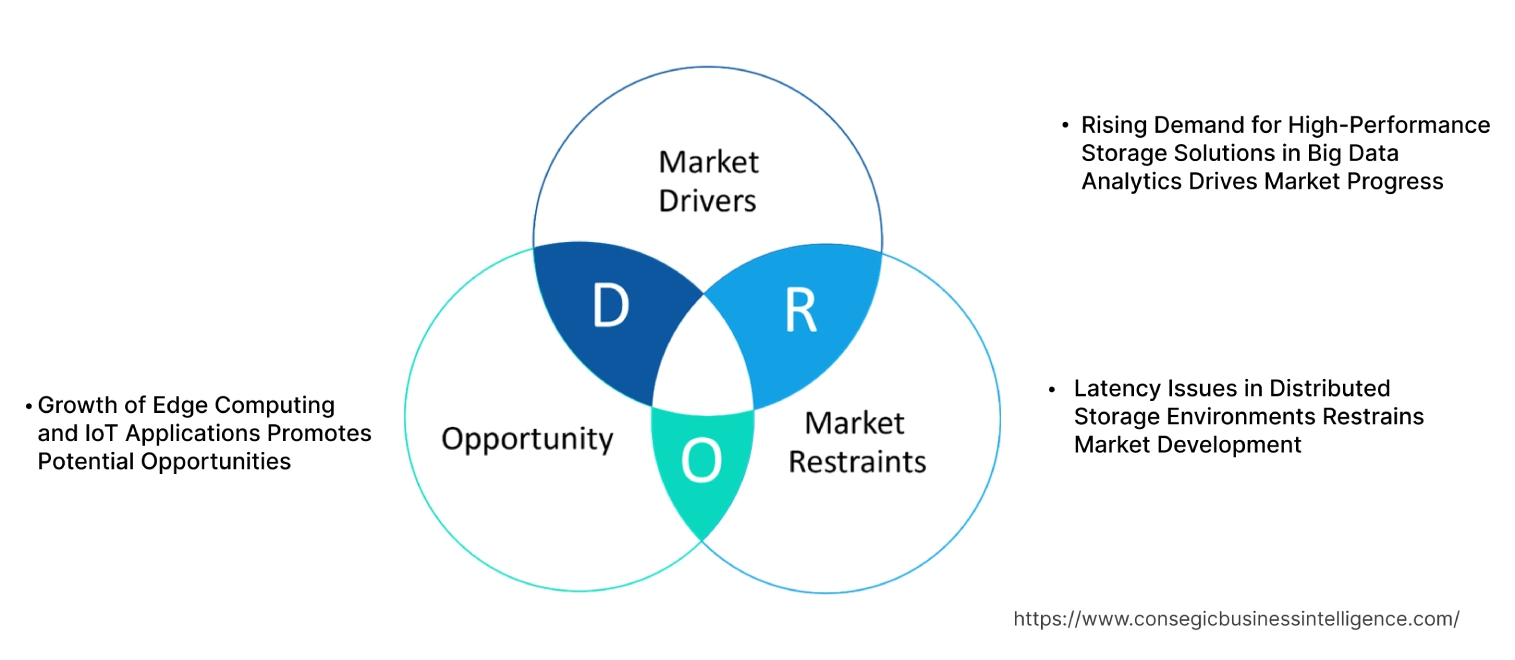

Next Generation Data Storage Technologies MarketDynamics - (DRO) :

Key Drivers:

Rising Demand for High-Performance Storage Solutions in Big Data Analytics Drives Market Progress

The rapid growth of big data analytics is driving demand for advanced storage technologies capable of handling massive data volumes with high speed and efficiency. Enterprises across industries, including finance, healthcare, and retail, are leveraging big data to derive actionable insights, requiring storage systems with high throughput and low latency.

Technologies such as NVMe-based storage and 3D NAND are gaining traction due to their ability to accelerate data processing and reduce operational bottlenecks. As per market trends, the need for scalable and performance-driven solutions in big data environments is a critical driver for next generation data storage technologies market growth.

Key Restraints :

Latency Issues in Distributed Storage Environments Restrains Market Development

Distributed storage environments, such as multi-cloud and hybrid cloud setups, often face latency issues due to the transfer of data across geographically dispersed locations. The distance between data centers, combined with network congestion and varying bandwidth capacities, results in delays that negatively impact system performance. These latency issues are particularly problematic for applications requiring real-time data processing, such as financial transactions, video streaming, and IoT analytics.

The complexity of managing data consistency and synchronization across multiple locations further compounds the problem, leading to potential inefficiencies and slower operations. Organizations are often required to invest in advanced optimization tools, such as content delivery networks (CDNs) and edge computing solutions, to reduce latency and enhance performance.

However, these additional costs are prohibitive for cost-sensitive businesses, especially small and medium enterprises, limiting the widespread adoption of distributed storage environments in latency-critical applications, thereby restraining next generation data storage technologies market demand.

Future Opportunities :

Growth of Edge Computing and IoT Applications Promotes Potential Opportunities

The rise of edge computing and IoT devices presents significant opportunities for advanced storage technologies. Edge computing generates vast amounts of decentralized data that require efficient storage and processing capabilities near the data source. Technologies like hyper-converged infrastructure (HCI) and distributed storage systems are ideal for addressing the latency and bandwidth challenges associated with edge data management.

As IoT adoption continues to grow, the need for localized, high-performance storage solutions is expected to surge, creating next generation data storage technologies market opportunities through increased innovation and adoption in this segment.

Top Key Players & Market Share Insights:

The Next Generation Data Storage Technologies market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Next Generation Data Storage Technologies market. Key players in the Next Generation Data Storage Technologies industry include -

- NetApp, Inc. (USA)

- Pure Storage, Inc. (USA)

- Western Digital Corporation (USA)

- Seagate Technology Holdings PLC (USA)

- IBM Corporation (USA)

- Dell Technologies Inc. (USA)

- Hewlett Packard Enterprise (HPE) (USA)

- Hitachi Vantara Corporation (USA)

- Quantum Corporation (USA)

- Toshiba Corporation (Japan)

Next Generation Data Storage Technologies Market Segmental Analysis :

By Storage System:

Based on the storage system, the market is segmented into Direct-Attached Storage (DAS), Network-Attached Storage (NAS), Storage Area Network (SAN), and Unified Storage.

The Network-Attached Storage (NAS) segment held the largest revenue of the total next generation data storage technologies market share in 2023.

- NAS systems are widely adopted for their scalability and ability to provide shared access to data across multiple users and devices, making them ideal for enterprises and small businesses.

- These systems are crucial for cloud-based environments, offering seamless integration and high-speed data transfer capabilities for enterprise workloads.

- NAS systems are increasingly preferred for data-intensive applications, including data archiving, media editing, and backup solutions.

- As per market trends, the dominance of NAS systems is supported by their cost-effectiveness and ease of deployment, catering to businesses of all sizes, driving next generation data storage technologies market expansion.

The Storage Area Network (SAN) segment is expected to register the fastest CAGR during the forecast period.

- SAN systems provide high-speed data transfer and centralized storage management, making them indispensable for mission-critical enterprise applications.

- These systems are widely used in industries such as healthcare and BFSI, where data integrity and accessibility are paramount.

- Innovations in fiber channel and Ethernet-based SAN technologies are enhancing system performance, supporting advanced data analytics and real-time processing.

- As per next generation data storage technologies market analysis, the increasing adoption of SAN systems reflects a shift toward high-performance, scalable storage solutions for enterprise environments.

By Storage Medium:

Based on a storage medium, the market is segmented into Solid State Drives (SSD), Hard Disk Drives (HDD), Tape Storage, and Blu-Ray Discs.

The Solid State Drives (SSD) segment accounted for the largest revenue of the total next generation data storage technologies market share in 2023.

- SSDs are widely adopted for their superior performance, faster read/write speeds, and higher energy efficiency compared to traditional HDDs.

- Enterprises rely on SSDs for applications requiring high-speed data access, such as big data analytics and high-performance computing.

- The increasing availability of cost-effective SSDs is driving their adoption in mid-range and consumer-grade data storage systems.

- As per next generation data storage technologies market trends, the segment's dominance is attributed to ongoing trends favoring faster and more reliable storage mediums for enterprise and consumer applications.

The Tape Storage segment is expected to register the fastest CAGR during the forecast period.

- Tape storage remains relevant for long-term data archiving due to its high reliability, low cost, and energy efficiency compared to disk-based solutions.

- This medium is widely used in industries requiring secure and scalable storage for compliance and regulatory purposes, such as government and BFSI.

- The adoption of advanced tape formats, such as LTO-9, ensures continued relevance in environments requiring massive data storage at minimal costs.

- Tape storage’s role in supporting hybrid cloud architectures further contributes to its rapid adoption across diverse industries, driving next generation data storage technologies market growth.

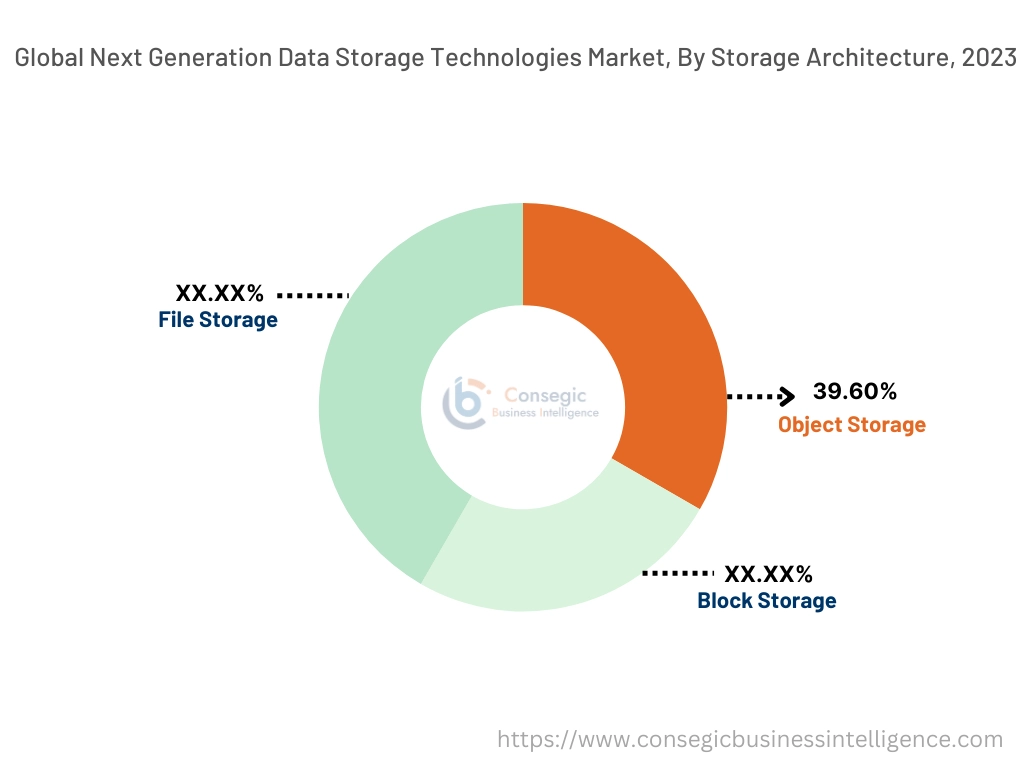

By Storage Architecture:

Based on storage architecture, the market is segmented into File Storage, Block Storage, and Object Storage.

The Object Storage segment held the largest revenue of 39.60% share in 2023.

- Object storage is widely used for managing unstructured data, making it a critical component in applications like media repositories, big data analytics, and cloud storage.

- Enterprises prefer object storage for its scalability and ability to handle large volumes of data efficiently, enabling seamless integration with modern cloud architectures.

- Advancements in object storage technologies are improving access speed and data retrieval, further driving adoption across industries.

- As per analysis, object storage dominates due to its flexibility and capability to address complex data storage needs across multiple sectors, fueling next generation data storage technologies market demand.

The File Storage segment is expected to register the fastest CAGR during the forecast period.

- File storage systems are essential for managing structured data, particularly in industries like healthcare and government where documentation and compliance are critical.

- These systems are widely used in shared environments, providing centralized access to files for collaboration and operational efficiency.

- The integration of file storage with hybrid cloud platforms supports real-time access and seamless data transfer across distributed networks.

- The segment's rapid growth reflects its continued relevance in traditional and emerging enterprise storage applications, driving next generation data storage technologies market expansion.

By Application:

Based on application, the market is segmented into Enterprise Data Management, Backup & Disaster Recovery, Data Archiving, Big Data Analytics, and High-Performance Computing (HPC).

The Backup & Disaster Recovery segment accounted for the largest revenue share in 2023.

- Backup and disaster recovery solutions are critical for ensuring business continuity and protecting data from accidental loss, cyberattacks, and hardware failures.

- Enterprises are increasingly investing in automated and cloud-integrated backup systems to minimize downtime and ensure rapid data recovery.

- As per market analysis, the rising frequency of ransomware attacks and data breaches is driving the adoption of robust backup solutions.

- The segment's dominance is attributed to its vital role in securing data integrity and supporting long-term operational resilience, creating next generation data storage technologies market opportunities.

The Big Data Analytics segment is expected to register the fastest CAGR during the forecast period.

- Big data analytics requires advanced storage solutions capable of handling massive datasets, ensuring real-time access and processing.

- Industries like healthcare, retail, and IT leverage data analytics to extract actionable insights, driving demand for scalable and high-performance storage systems.

- The integration of AI and machine learning into analytics workflows further emphasizes the need for optimized storage architectures.

- As per next generation data storage technologies market trends, the segment’s rapid growth is fueled by trends favoring data-driven decision-making across industries, enhancing competitive advantage.

By End-User Industry:

Based on the end-user industry, the market is segmented into IT & Telecom, BFSI, Healthcare, Retail, Government, Media & Entertainment, and Others.

The IT & Telecom segment held the largest revenue share in 2023.

- IT & telecom companies rely on advanced storage solutions to manage large volumes of customer data, application workloads, and cloud infrastructure.

- These industries adopt high-performance storage systems to ensure seamless connectivity and service delivery in a highly competitive environment.

- Innovations in network storage technologies, including NAS and SAN, are addressing the complex data management needs of the telecom sector.

- As per next generation data storage technologies market analysis, the segment’s dominance is driven by the critical role of storage systems in supporting modern IT ecosystems and telecom networks.

The Healthcare segment is expected to register the fastest CAGR during the forecast period.

- Healthcare providers require reliable storage solutions for managing sensitive patient data, medical imaging, and research information.

- Compliance with data protection regulations, such as HIPAA, is driving investments in secure and scalable storage architectures.

- The increasing adoption of AI and analytics in healthcare workflows highlights the need for high-performance storage systems.

- The analysis of segmental trends depicts that the healthcare segment’s rapid growth is attributed to its focus on improving patient outcomes through data-driven healthcare solutions.

Next Generation Data Storage Technologies Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 140.29 Billion |

| CAGR (2024-2031) | 6.7% |

| By Storage System |

|

| By Storage Medium |

|

| By Storage Architecture |

|

| By Application |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

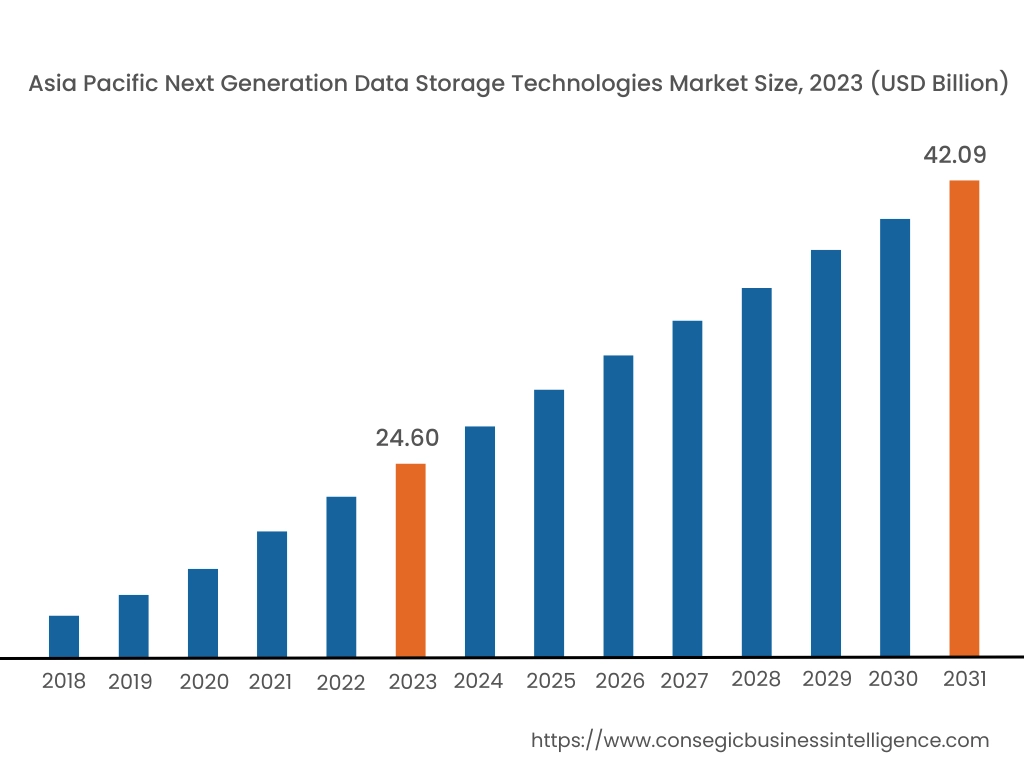

Asia Pacific region was valued at USD 24.60 Billion in 2023. Moreover, it is projected to grow by USD 25.85 Billion in 2024 and reach over USD 42.09 Billion by 2031. Out of these, China accounted for the largest share of 43.4% in 2023. Asia-Pacific is witnessing rapid adoption of next-generation data storage technologies, fueled by the exponential growth of e-commerce, digital services, and cloud computing in countries like China, India, and Japan. The region’s surging requirement for 5G connectivity and the rise of IoT devices are placing immense pressure on existing data storage systems, prompting investments in high-performance solutions such as flash storage and hybrid cloud platforms. Governments in China and India are implementing policies to localize data storage, which is further driving adoption.

North America is estimated to reach over USD 46.16 Billion by 2031 from a value of USD 27.80 Billion in 2023 and is projected to grow by USD 29.14 Billion in 2024. North America continues to lead the market due to the high concentration of data centers and advanced IT infrastructure. The United States, in particular, is a hub for cloud service providers and enterprises prioritizing data security and advanced storage capabilities. The increasing adoption of artificial intelligence (AI) and machine learning (ML) technologies is driving the need for scalable and high-speed data storage solutions. The region is also witnessing significant investments in NVMe (Non-Volatile Memory Express) and solid-state drives (SSDs) for faster data processing.

Europe is a critical market for next-generation data storage technologies, bolstered by the region's strong focus on data sovereignty and compliance with regulations like GDPR. Countries such as Germany and the UK are heavily investing in modernizing their data infrastructure to support growing needs in financial services, manufacturing, and healthcare. The push toward green data storage solutions and energy-efficient technologies is also gaining traction, particularly in Nordic countries.

The Middle East & Africa region is gradually emerging as a potential market for advanced data storage technologies. The UAE and Saudi Arabia are spearheading digital transformation initiatives, with increasing investments in data analytics, smart cities, and enterprise IT solutions. The demand for next-generation storage systems is rising, particularly in sectors like oil and gas, banking, and healthcare, which require secure and scalable storage solutions. South Africa is also focusing on strengthening its IT infrastructure.

Latin America is an evolving market for next-generation data storage technologies, with Brazil and Mexico driving adoption. The region's digital transformation across sectors such as retail, telecommunications, and finance is fueling the need for reliable data storage solutions. Brazil’s growing data center investments and Mexico’s emphasis on improving IT services are noteworthy. As per the market trends, the need for hybrid cloud storage solutions is increasing as companies look to balance cost efficiency and performance.

Recent Industry Developments :

Partnerships & Collaborations:

- In November 2024, Toshiba announced a collaboration with PROMISE Technology to enhance data storage for CERN’s Large Hadron Collider (LHC). The partnership focuses on providing robust and energy-efficient storage solutions, including the integration of Toshiba’s Enterprise Capacity HDDs with PROMISE’s new 60-bay JBOD storage system. The technology will support CERN's extensive data needs, which have grown to over one exabyte, helping facilitate groundbreaking research. This collaboration also emphasizes sustainability with energy-saving innovations.

Product Launches:

- In May 2024, NetApp unveiled its new AFF A-Series storage systems, designed to meet the demands of AI and other data-intensive workloads. These systems offer up to 2x better performance with 40 Billion IOPs and a 1 TB/s throughput, supporting unified data storage across various applications. New features include integrated real-time ransomware detection, enhanced VMware storage capabilities, and significant energy and space savings. This release marks a significant leap forward for businesses adopting AI technologies, providing high-speed, secure, and scalable data infrastructure for modern enterprises.

- In September 2024, Huawei launched the New-Gen OceanStor Dorado All-Flash Storage, designed to meet the needs of mission-critical applications in the AI era. Key features include extreme performance, extreme resilience with multi-layer fault tolerance, and AI-readiness. This storage solution supports databases, files, and containers, offering improved operational efficiency through its Data Management Engine (DME). It also includes ransomware protection and achieves high IOPS with ultra-low latency. The solution aims to accelerate digital transformation for industries like finance, healthcare, and manufacturing.

- In October 2023, IBM introduced the IBM Storage Scale System 6000, a high-performance cloud-scale storage platform designed to handle AI and data-intensive workloads. It boasts up to 7 Billion IOPS and 256GB/s throughput, optimizing storage for unstructured data. The system integrates NVMe FlashCore Modules, enhancing cost efficiency and energy savings. It accelerates AI workloads with improved data access speeds while providing scalability and flexibility across hybrid environments. The system is expected to drive AI research and digital transformations, offering faster access to data and a lower total cost of ownership.

Key Questions Answered in the Report

How big is the Next Generation Data Storage Technologies Market? +

Next Generation Data Storage Technologies Market size is estimated to reach over USD 140.29 Billion by 2031 from a value of USD 83.65 Billion in 2023 and is projected to grow by USD 87.75 Billion in 2024, growing at a CAGR of 6.7% from 2024 to 2031.

What specific segmentation details are covered in the Next Generation Data Storage Technologies Market report? +

The Next Generation Data Storage Technologies Market report includes segmentation details for a storage system (Direct-Attached Storage (DAS), Network-Attached Storage (NAS), Storage Area Network (SAN), Unified Storage), a storage medium (Solid State Drives (SSD), Hard Disk Drives (HDD), Tape Storage, Blu-Ray Discs), storage architecture (File Storage, Block Storage, Object Storage), application (Enterprise Data Management, Backup & Disaster Recovery, Data Archiving, Data Analytics, Performance Computing (HPC)), end-user industry (IT & Telecom, BFSI, Healthcare, Retail, Government, Media & Entertainment, Others), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which is the fastest-growing segment in the Next Generation Data Storage Technologies Market? +

The Big Data Analytics segment is expected to grow rapidly during the forecast period due to the increasing demand for scalable and high-performance storage solutions that can handle massive datasets and enable real-time data processing.

Who are the major players in the Next Generation Data Storage Technologies Market? +

The major players in the Next Generation Data Storage Technologies Market include NetApp, Inc. (USA), Pure Storage, Inc. (USA), Western Digital Corporation (USA), Seagate Technology Holdings PLC (USA), IBM Corporation (USA), Dell Technologies Inc. (USA), Hewlett Packard Enterprise (HPE) (USA), Hitachi Vantara Corporation (USA), Quantum Corporation (USA), and Toshiba Corporation (Japan).