- Summary

- Table Of Content

- Methodology

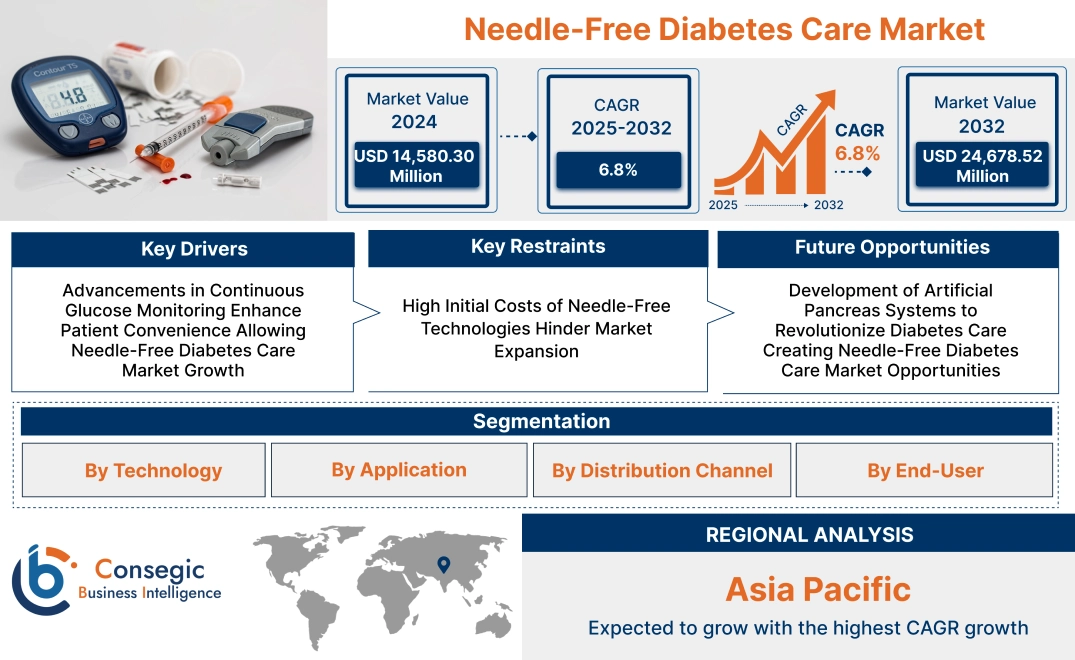

Needle-Free Diabetes Care Market Size:

Needle-Free Diabetes Care Market size is estimated to reach over USD 24,678.52 Million by 2032 from a value of USD 14,580.30 Million in 2024 and is projected to grow by USD 15,311.96 Million in 2025, growing at a CAGR of 6.8 % from 2025 to 2032.

Needle-Free Diabetes Care Market Scope & Overview:

Needle-free diabetes care includes advanced devices and solutions designed to manage blood glucose levels without the use of needles or invasive procedures. These systems utilize technologies such as laser-based sampling, microneedles, and transdermal patches for blood glucose monitoring and insulin delivery. The features of these solutions include reduced pain, enhanced patient comfort, and user-friendly designs. Many devices offer real-time monitoring, data storage, and seamless connectivity with mobile applications for improved diabetes management.

The benefits of needle-free diabetes care include minimizing patient anxiety, reducing the risk of infections, and improving adherence to treatment plans. Non-invasive systems also contribute to better long-term disease management and quality of life for individuals with diabetes. Applications span across glucose monitoring, insulin delivery, and overall diabetes management. End-use industries include hospitals, clinics, diagnostic centers, and home healthcare providers focusing on innovative diabetes care solutions.

Needle-Free Diabetes Care Market Dynamics - (DRO) :

Key Drivers:

Advancements in Continuous Glucose Monitoring Enhance Patient Convenience Allowing Needle-Free Diabetes Care Market Growth

Continuous glucose monitoring (CGM) systems offer real-time tracking of glucose levels, eliminating the need for traditional finger-prick methods. These systems improve patient compliance by reducing discomfort and providing valuable data for better diabetes management. For instance, wearable CGM devices with needle-free sensors allow seamless integration into patients' daily routines, facilitating timely insulin adjustments and preventing complications.

As the adoption of CGM systems grows due to their convenience and efficacy, the needle-free diabetes care market is expected to witness significant growth.

Key Restraints:

High Initial Costs of Needle-Free Technologies Hinder Market Expansion

The adoption of needle-free diabetes care devices is limited by their high upfront costs compared to traditional solutions. Advanced technologies, such as needle-free insulin delivery systems, involve significant research, development, and manufacturing expenses, which translate into higher prices for consumers. For example, insulin jet injectors often cost more than conventional insulin pens, making them less accessible to patients in low-income regions.

This financial barrier restricts the widespread use of needle-free devices, impeding the needle-free diabetes care market growth potential.

Future Opportunities :

Development of Artificial Pancreas Systems to Revolutionize Diabetes Care Creating Needle-Free Diabetes Care Market Opportunities

Artificial pancreas systems represent a groundbreaking advancement in diabetes management, integrating continuous glucose monitoring and automated insulin delivery without needles. These systems are in advanced development stages and aim to provide fully automated diabetes care with minimal patient intervention. For example, hybrid closed-loop systems are being enhanced with algorithm-driven features to deliver precise insulin doses based on real-time glucose readings.

The anticipated commercialization of artificial pancreas systems presents a transformative needle-free diabetes care market opportunit, promising to redefine diabetes treatment paradigms.

Needle-Free Diabetes Care Market Segmental Analysis :

By Technology:

Based on technology, the market is segmented into jet injectors, insulin patches, continuous glucose monitoring (CGM) systems, and artificial pancreas systems.

The continuous glucose monitoring (CGM) systems segment accounted for the largest revenue in needle-free diabetes care market share in 2024.

- CGM systems offer real-time monitoring of glucose levels, eliminating the need for frequent finger pricking.

- They provide actionable data for individuals to adjust their diabetes management strategies effectively.

- The growing preference for minimally invasive technologies and the increased prevalence of diabetes are driving demand.

- The integration of CGM systems with smartphone applications and wearable devices enhances user convenience and compliance.

- Continuous advancements in sensor accuracy and the expansion of CGM systems to non-diabetic patients for early detection further fuel trend.

- CGM systems also facilitate data sharing with healthcare professionals, enabling better decision-making in diabetes care.

- Therefore, according to needle-free diabetes care market analysis, CGM systems segment's dominance is attributed to its innovative approach to diabetes monitoring, aligning with user preferences for ease and effectiveness.

The artificial pancreas systems segment is anticipated to register the fastest CAGR during the forecast period.

- Artificial pancreas systems automate insulin delivery, combining CGM data with insulin pump technology for optimal glycemic control.

- This technology mimics the natural function of a healthy pancreas, improving the quality of life for individuals with diabetes.

- Increasing investment in research and development and the push for advanced treatment solutions contribute to its rapid adoption.

- The integration of artificial pancreas systems with mobile apps for real-time adjustments provides increased personalization and user control.

- As the systems become more affordable, they are expected to be adopted by a larger segment of the diabetes population.

- Thus, according to needle-free diabetes care market analysis, a rtificial pancreas systems are expected to witness substantial needle-free diabetes care market trend, driven by technological advancements and a shift toward automated diabetes care solutions.

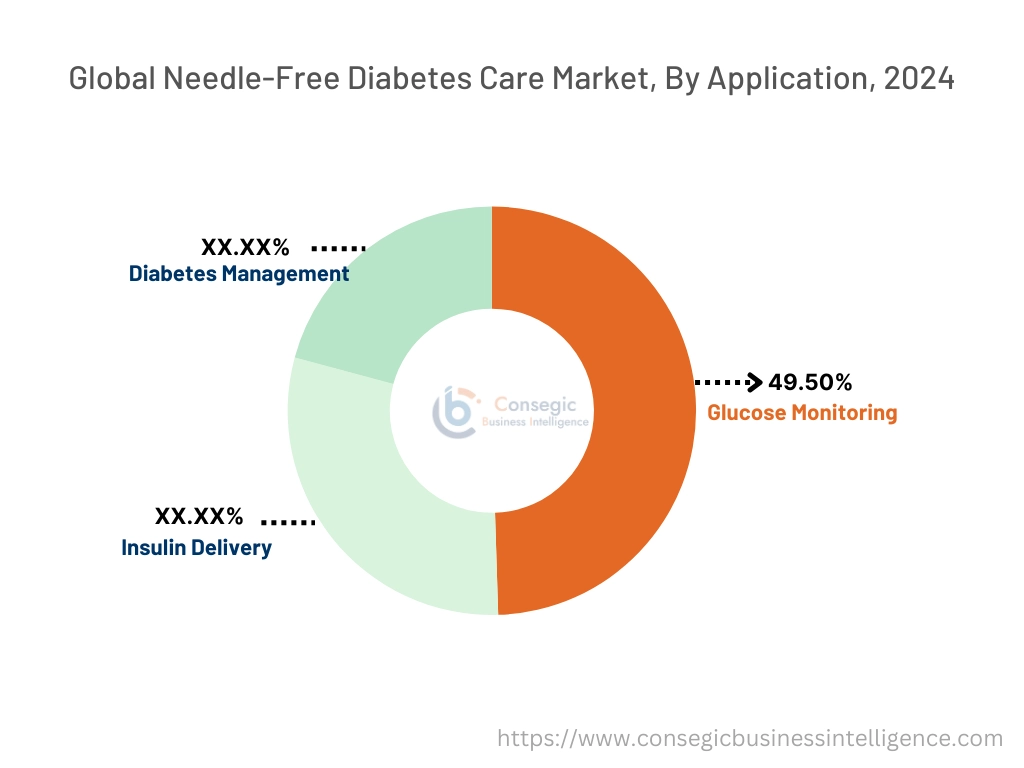

By Application:

Based on application, the market is segmented into insulin delivery, glucose monitoring, and diabetes management.

The glucose monitoring segment accounted for the largest revenue of 49.50% in needle-free diabetes care market share in 2024.

- Glucose monitoring systems are critical for maintaining optimal blood sugar levels, a cornerstone of diabetes care.

- These systems enable early detection of hypoglycemia or hyperglycemia, reducing complications.

- The availability of advanced glucose monitoring devices and growing patient awareness contribute to segment trend.

- The widespread adoption of glucose monitoring systems is further supported by their integration with digital health platforms.

- Ongoing innovations are focused on reducing the size of glucose sensors, enhancing user comfort and usability.

- Therefore, according to market analysis, the glucose monitoring segment remains crucial for diabetes management, with advancements ensuring its continued market leadership.

The diabetes management segment is anticipated to register the fastest CAGR during the forecast period.

- Diabetes management solutions integrate various technologies, including monitoring, data analysis, and personalized treatment plans.

- Increasing adoption of comprehensive care solutions by healthcare providers boosts demand in this segment.

- Focus on holistic patient care and reduction of long-term complications drives trend.

- Personalized care through digital health tools is enabling more tailored diabetes management strategies.

- The increasing prevalence of diabetes globally underscores the need for efficient and comprehensive diabetes management solutions.

- Thus, according to market analysis, the diabetes management segment's rapid trend highlights the shift towards integrated and personalized care in diabetes treatment.

By Distribution Channel:

Based on distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies.

The hospital pharmacies segment accounted for the largest revenue share in 2024.

- Hospital pharmacies are trusted providers for advanced diabetes care devices due to their association with healthcare professionals.

- They ensure access to the latest needle-free technologies and provide expert guidance for device usage.

- A centralized supply chain and reliable inventory management further enhance their prominence.

- Hospital pharmacies also play a critical role in educating patients on the proper usage of needle-free devices, which fosters trust in these technologies.

- The strong relationship between hospital pharmacies and healthcare providers facilitates improved patient outcomes.

- Therefore, according to market analysis, hospital pharmacies play a vital role in the accessibility and adoption of advanced needle-free diabetes care technologies.

The online pharmacies segment is anticipated to register the fastest CAGR during the forecast period.

- Online pharmacies offer convenience, competitive pricing, and home delivery services, appealing to tech-savvy consumers.

- Rising internet penetration and the preference for contactless shopping drive demand in this segment.

- Enhanced digital marketing and e-commerce platforms expand the reach of needle-free diabetes care products.

- The growing trend of self-managed healthcare and the increasing reliance on online platforms for health-related products further contribute to needle-free diabetes care market trend.

- Online pharmacies offer a wider variety of needle-free devices and related products, catering to diverse consumer needs.

- Thus, according to market analysis, online pharmacies represent a transformative shift in the distribution landscape, meeting modern consumer expectations for convenience and accessibility.

By End-User:

Based on end-user, the market is segmented into hospitals, clinics, homecare settings, and research institutions.

The homecare settings segment accounted for the largest revenue share in 2024.

- Homecare settings allow patients to manage their diabetes conveniently and efficiently using advanced needle-free devices.

- The rise in telehealth services and patient preference for at-home care solutions supports this segment.

- Cost-effectiveness and ease of use make homecare solutions attractive to patients and caregivers alike.

- Homecare settings offer enhanced comfort, as patients can manage their condition without frequent visits to healthcare facilities.

- The availability of remote patient monitoring and virtual consultations enhances the effectiveness of homecare settings for diabetes management.

- Therefore, according to market analysis, the homecare settings segment reflects the increasing trend towards decentralized healthcare and patient empowerment.

The research institutions segment is anticipated to register the fastest CAGR during the forecast period.

- Research institutions focus on the development of innovative diabetes care technologies and their applications.

- Collaborations between academic entities and industry players drive advancements in needle-free solutions.

- Government grants and funding initiatives further boost this segment's growth potential.

- Research institutions are also pivotal in clinical trials and studies that validate the efficacy and safety of new technologies.

- The demand for innovative solutions and breakthrough technologies in diabetes care is fueling investment in research-driven initiatives.

- Thus, according to market analysis, research institutions are pivotal in shaping the future of needle-free diabetes care through innovation and collaborative efforts.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

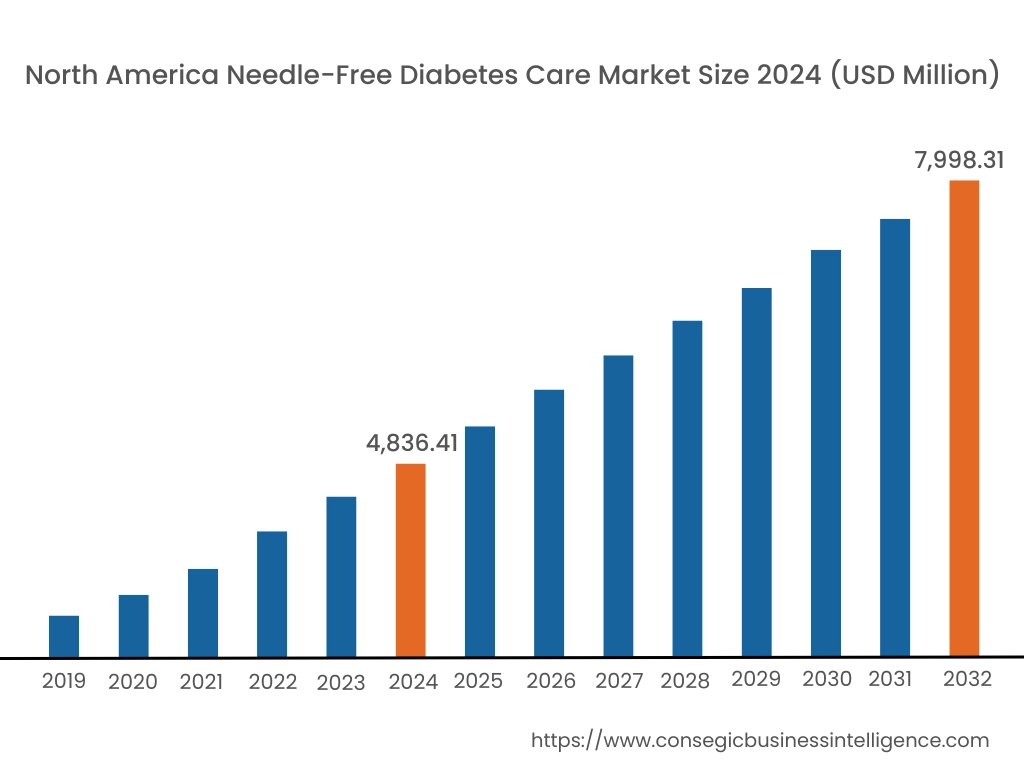

In 2024, North America was valued at USD 4,836.41 Million and is expected to reach USD 7,998.31 Million in 2032. In North America, the U.S. accounted for the highest share of 71.80% during the base year of 2024. North America holds a significant share of the needle-free diabetes care market, led by the United States and Canada. The increasing prevalence of diabetes, along with a high demand for innovative and less painful treatment options, boosts needle-free diabetes care market demand. Additionally, strong healthcare infrastructure and higher healthcare expenditure support the adoption of needle-free devices. Technological advancements in needle-free insulin delivery systems and increased awareness among patients regarding the benefits of needle-free solutions further contribute to needle-free diabetes care market expansion.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 7.2% over the forecast period. Asia-Pacific shows promising growth in the needle-free diabetes care market. The rising incidence of diabetes, particularly in countries like China, India, and Japan, along with increasing healthcare investments, enhances market potential. Urbanization and lifestyle changes, such as poor diet and lack of physical activity, lead to higher diabetes cases, thereby driving demand for needle-free solutions. However, market development faces challenges in rural areas due to limited access to advanced healthcare technologies and awareness gaps.

Europe is a key region for the needle-free diabetes care market. Countries like Germany, the UK, and France have strong healthcare systems that support the adoption of innovative diabetes care solutions. The increasing number of diabetes patients, combined with the need for pain-free and convenient treatment options, drives needle-free diabetes care market demand. In addition, stringent regulations and the presence of leading healthcare players in the region contribute to the market’s growth. Awareness of needle-free diabetes care solutions is high, further encouraging adoption among patients and healthcare providers.

In the Middle East and Africa, the needle-free diabetes care market is evolving. The region faces a rising prevalence of diabetes, particularly in countries like Saudi Arabia, the UAE, and South Africa, where lifestyle changes have led to increased health concerns. However, needle-free diabetes care market growth is hindered by limited access to advanced healthcare technologies and insufficient awareness about needle-free options in some areas. Despite this, rising healthcare investments and government initiatives in the GCC countries are likely to enhance market prospects in the coming years.

Latin America experiences moderate growth in the needle-free diabetes care market, with countries like Brazil and Mexico leading the demand. The increasing burden of diabetes, alongside a growing preference for pain-free treatment methods, supports market development. However, challenges related to the affordability and accessibility of advanced healthcare devices affect market penetration. Efforts to improve healthcare infrastructure and expand access to modern treatment options will play a crucial role in shaping the market’s future in the region.

Top Key Players and Market Share Insights:

The Global Needle-Free Diabetes Care Market is highly competitive with major players providing FWA to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global Needle-Free Diabetes Care Market. Key players in the Needle-Free Diabetes Care industry include-

- PharmaJet (United States)

- Insulet Corporation (United States)

- Mylan N.V. (United States)

- Tandem Diabetes Care, Inc. (United States)

- GlaxoSmithKline plc (United Kingdom)

- Valeritas, Inc. (United States)

- Medtronic PLC (Ireland)

- Novo Nordisk A/S (Denmark)

- BD (Becton, Dickinson and Company) (United States)

- IntraJet Technologies, Inc. (United States)

Recent Industry Developments :

Product Launches:

- According to a research in June 2024, by University of British Columbia, Oral insulin drops offer a needle-free alternative for diabetes management, potentially improving patient compliance and reducing the discomfort associated with traditional insulin injections.

Needle-Free Diabetes Care Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 24,678.52 Million |

| CAGR (2025-2032) | 6.8% |

| By Technology |

|

| By Application |

|

| By Distribution Channel |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Needle-Free Diabetes Care Market? +

In 2024, the Needle-Free Diabetes Care Market was USD 14,580.30 million.

What will be the potential market valuation for the Needle-Free Diabetes Care Market by 2032? +

In 2032, the market size of Needle-Free Diabetes Care Market is expected to reach USD 24,678.52 million.

What are the segments covered in the Needle-Free Diabetes Care Market report? +

The technology, application, distribution channel, and end-user are the segments covered in this report.

Who are the major players in the Needle-Free Diabetes Care Market? +

PharmaJet (United States), Insulet Corporation (United States), Mylan N.V. (United States), Valeritas, Inc. (United States), Medtronic PLC (Ireland), Novo Nordisk A/S (Denmark), BD (Becton, Dickinson and Company) (United States), IntraJet Technologies, Inc. (United States), Tandem Diabetes Care, Inc. (United States), GlaxoSmithKline plc (United Kingdom) are the major players in the Needle-Free Diabetes Care market.