- Summary

- Table Of Content

- Methodology

Narrowbody Aircraft MRO Market Size:

Narrowbody Aircraft MRO Market size is estimated to reach over USD 37,571.24 Million by 2032 from a value of USD 27,147.78 Million in 2024 and is projected to grow by USD 27,800.95 Million in 2025, growing at a CAGR of 4.4% from 2025 to 2032.

Narrowbody Aircraft MRO Market Scope & Overview:

Narrowbody aircraft MRO (Maintenance, Repair, and Overhaul) refers to services focused on the upkeep, repair, and optimization of single-aisle aircraft used for short to medium-haul routes. These services encompass routine maintenance, engine and component repairs, structural modifications, and avionics upgrades, ensuring the aircraft meets safety and operational standards. MRO activities are essential for maintaining the performance, reliability, and lifecycle of narrowbody fleets.

These services are carried out by specialized facilities equipped with advanced tools and skilled personnel capable of handling the specific requirements of narrowbody aircraft. Tasks include inspections, engine overhauls, cabin retrofitting, and landing gear maintenance. MRO providers also ensure compliance with regulatory standards while optimizing turnaround times to minimize downtime.

End-users of these services include commercial airlines, cargo operators, and leasing companies, where consistent and reliable maintenance is crucial to sustaining operations. Narrowbody aircraft MRO plays a vital role in supporting the efficiency and safety of global aviation networks.

Narrowbody Aircraft MRO Market Dynamics - (DRO) :

Key Drivers:

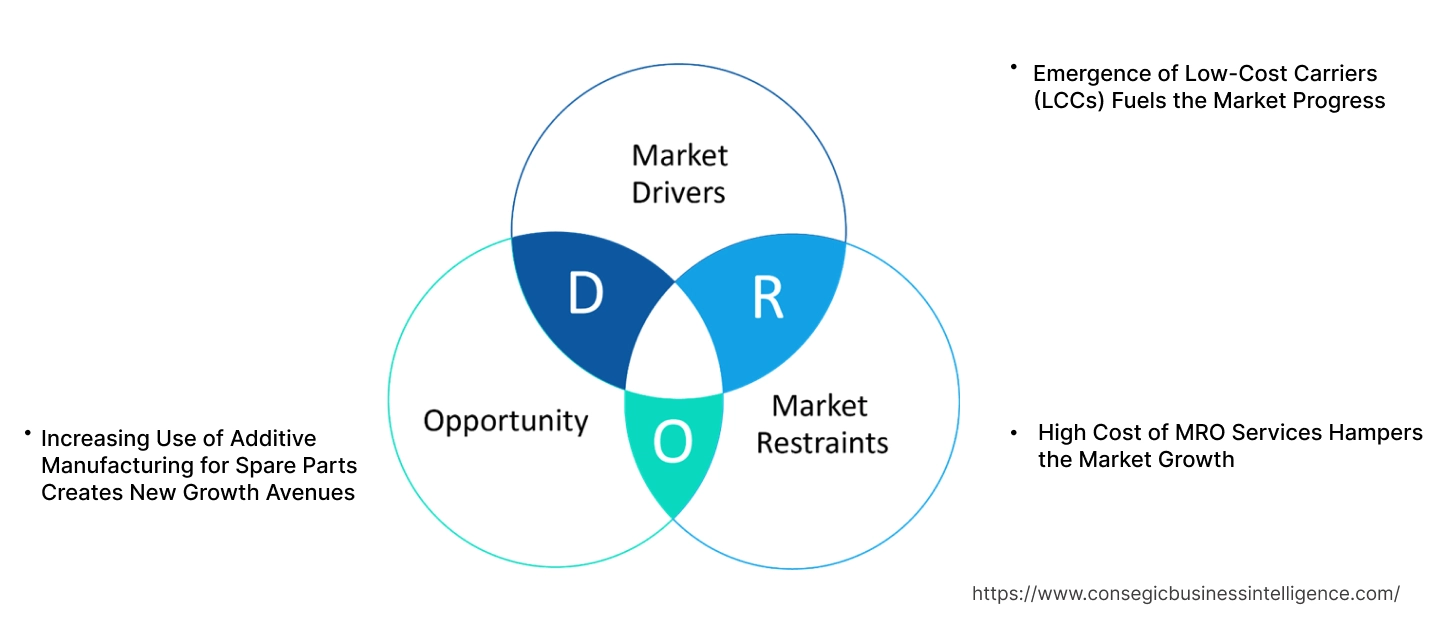

Emergence of Low-Cost Carriers (LCCs) Fuels the Market Progress

The rapid expansion of low-cost carriers (LCCs) has significantly driven the demand for cost-effective MRO services, as these airlines predominantly operate narrowbody aircraft to cater to short-haul and domestic routes. LCCs focus on maintaining lean operational models, prioritizing high aircraft utilization and minimal turnaround times. To achieve this, they rely heavily on outsourced MRO providers for maintenance, repair, and overhaul services. Outsourcing allows LCCs to access specialized expertise and advanced technologies without the need for in-house infrastructure, reducing costs while ensuring compliance with stringent aviation regulations. Additionally, outsourced MRO services provide flexibility in managing maintenance schedules and addressing unexpected repairs, minimizing aircraft downtime and enhancing fleet availability. With the continued growth of LCCs in emerging markets, the demand for efficient, scalable, and geographically accessible MRO solutions is expected to rise, further driving the narrowbody aircraft MRO market growth.

Key Restraints:

High Cost of MRO Services Hampers the Market Growth

The high cost of maintenance, repair, and overhaul (MRO) services is a significant restraint in the narrowbody aircraft MRO market, particularly for smaller airlines and low-cost carriers. Advanced technologies, such as predictive maintenance tools and specialized diagnostics, come with substantial upfront investment and operational expenses, making it difficult for budget-constrained operators to adopt them. Additionally, the increasing cost of labor and regulatory compliance further escalates the overall expense of MRO services. Airlines operating in regions with limited local MRO facilities face additional logistics and transportation costs, further burdening their budgets. This financial strain often forces airlines to delay non-critical maintenance activities, which impacts fleet availability and operational efficiency, thereby limiting the narrowbody aircraft MRO market demand.

Future Opportunities :

Increasing Use of Additive Manufacturing for Spare Parts Creates New Growth Avenues

The integration of additive manufacturing (3D printing) in MRO operations is transforming the production of spare parts by enabling on-demand manufacturing, reducing lead times, and lowering costs. Traditional spare parts production often involves long procurement cycles and extensive logistics, leading to delays and increased expenses. With 3D printing, MRO providers produce customized components locally, minimizing inventory requirements and avoiding supply chain disruptions. This technology is particularly beneficial for manufacturing low-volume, high-complexity parts that are difficult to source or expensive to store. Additionally, 3D printing allows for rapid prototyping and repair of parts, ensuring quick turnaround times and enhancing aircraft availability. The ability to use lightweight and durable materials in 3D printing also aligns with the aviation industry's focus on efficiency and sustainability. As additive manufacturing technologies advance, their application in MRO operations is expected to expand, offering significant cost and operational advantages to airlines and service providers. Thus, the aforementioned factors create significant narrowbody aircraft MRO market opportunities.

Narrowbody Aircraft MRO Market Segmental Analysis :

By Service Type:

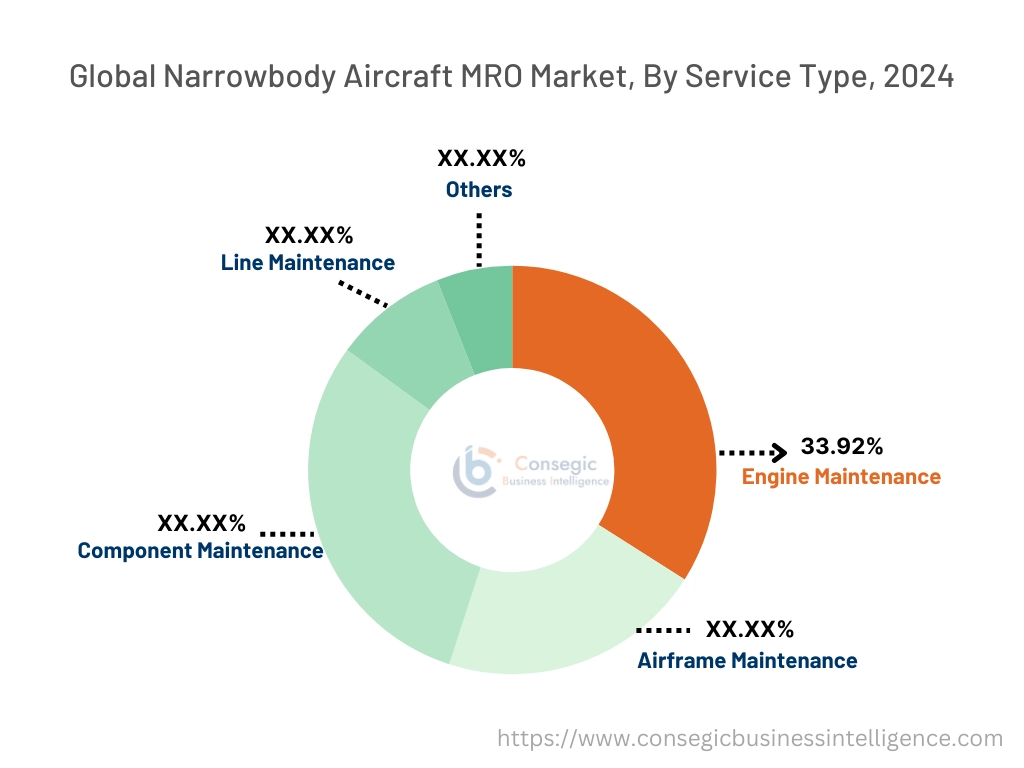

Based on service type, the market is segmented into engine maintenance, airframe maintenance, component maintenance, line maintenance, and others.

The engine maintenance segment held the largest revenue of 33.92% of the total narrowbody aircraft MRO market share in 2024.

- The high cost and complexity of engine maintenance drive its significant contribution to overall MRO expenditures.

- Engine maintenance services ensure optimal performance and fuel efficiency, reducing operational costs for aircraft operators.

- Increasing adoption of advanced engines with higher efficiency requires specialized MRO services, boosting this segment.

- As per market trends, the segment’s dominance is supported by the critical role engines play in aircraft performance and safety, contributing to the narrowbody aircraft MRO market expansion.

The component maintenance segment is expected to register the fastest CAGR during the forecast period.

- This segment benefits from technological advancements in modular components, enabling faster repair and replacement cycles.

- Increasing focus on predictive maintenance for components reduces downtime and enhances operational efficiency.

- Growth in requirement for digital tools like IoT and AI-driven analytics to monitor component performance supports market progression.

- As per the narrowbody aircraft MRO market analysis, the shift toward outsourcing component MRO to specialized providers boosts the adoption of such services.

By Aircraft Type:

Based on aircraft type, the market is categorized into fixed-wing and rotary-wing.

The fixed-wing aircraft segment accounted for the largest revenue of the total narrowbody aircraft MRO market share in 2024.

- Fixed-wing aircraft dominate commercial aviation, leading to substantial MRO service requirements.

- Extensive use in passenger transport and cargo operations drives need for periodic maintenance.

- Technological advancements in fixed-wing designs and materials require specialized MRO capabilities.

- As per the segmental trends analysis, the high volume of fixed-wing aircraft in service contributes significantly to this segment's prominence, further fueling the narrowbody aircraft MRO market growth.

The rotary-wing aircraft segment is anticipated to exhibit the fastest CAGR during the forecast period.

- Rotary-wing aircraft are extensively used in military, medical evacuation, and offshore operations, necessitating frequent MRO services.

- The increasing adoption of helicopters in urban air mobility (UAM) further fuels need for maintenance services.

- Specialized requirements for rotor blades, engines, and avionics boost growth in this segment.

- As per the narrowbody aircraft MRO market trends, expanding use of rotary-wing aircraft for defense applications supports the segment's rapid expansion.

By End-Use:

Based on end-use, the market is divided into military and civil.

The civil segment held the largest revenue share in 2024.

- The global extension of commercial airlines significantly drives demand for MRO services in the civil sector.

- Increasing air travel and cargo operations require frequent and reliable maintenance services.

- Civil aircraft operators prioritize MRO to ensure passenger safety, operational efficiency, and compliance with regulatory standards.

- As per narrowbody aircraft MRO market analysis, the dominance of this segment is due to the extensive fleet size of commercial narrowbody aircraft.

The military segment is projected to grow at the fastest CAGR during the forecast period.

- Military aircraft require advanced MRO services due to their specialized missions and operations.

- Governments are increasing defense budgets, leading to heightened requirement for military aircraft maintenance.

- Growing emphasis on modernizing existing fleets and ensuring mission readiness supports the enlargement of this segment.

- As per the narrowbody aircraft MRO market trends, advancements in defense technology and equipment necessitate highly specialized MRO capabilities.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

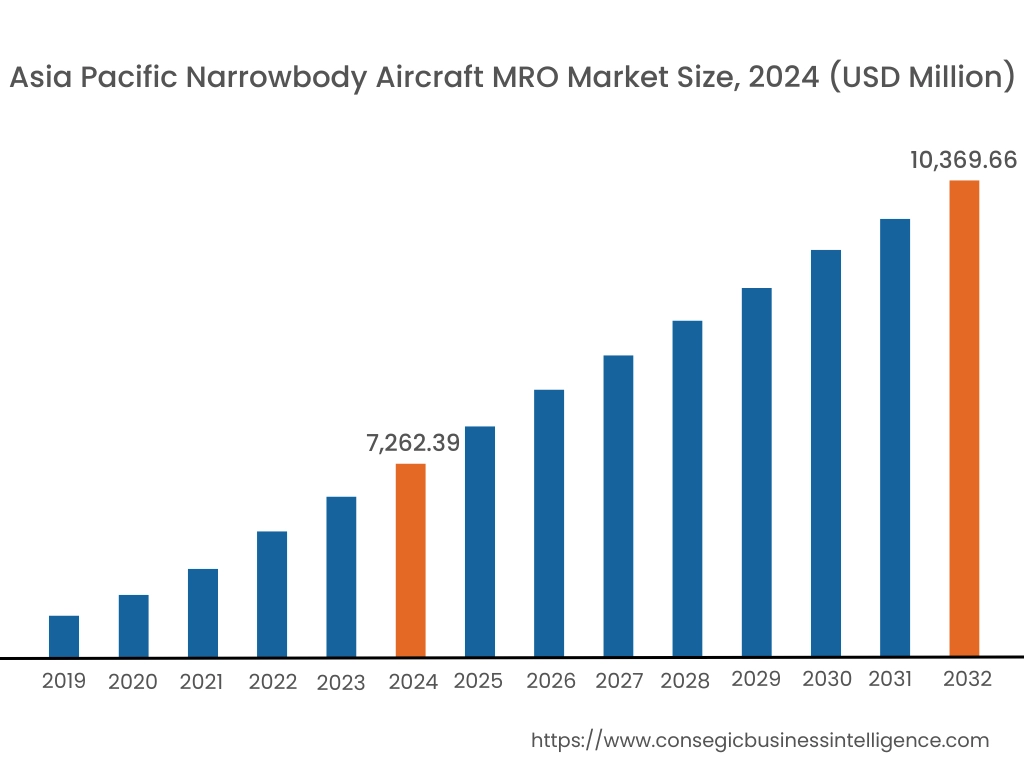

Asia Pacific region was valued at USD 7,262.39 Million in 2024. Moreover, it is projected to grow by USD 7,456.78 Million in 2025 and reach over USD 10,369.66 Million by 2032. Out of this, China accounted for the maximum revenue share of 29.7%. The Asia-Pacific region is experiencing a surge in air travel, leading to an increased deployment of narrowbody aircraft. This has resulted in a growing need for MRO services to ensure fleet readiness and safety. A prominent trend is the establishment of new MRO facilities and the extension of existing ones to cater to the rising demand. Analysis suggests that regional collaborations and government initiatives are playing a crucial role in enhancing narrowbody aircraft MRO market expansion across the continent.

North America is estimated to reach over USD 12,060.37 Million by 2032 from a value of USD 8,778.31 Million in 2024 and is projected to grow by USD 8,984.07 Million in 2025. This region commands a significant share of the narrowbody aircraft MRO market, largely due to the extensive fleet of narrowbody aircraft operated by major airlines. A notable trend is the substantial investments by key industry players to enhance MRO capabilities. Analysis suggests that such investments are pivotal in maintaining operational efficiency and meeting the rising need for MRO services in North America.

European carriers operate a substantial number of narrowbody aircraft, necessitating robust MRO services. The region is witnessing a trend towards the adoption of advanced technologies in MRO operations to enhance efficiency and reduce turnaround times. Analysis indicates that the presence of established MRO providers and a skilled workforce contributes to the region’s narrowbody aircraft MRO market demand.

In the Middle East, the strategic location as a global aviation hub has led to investments in MRO infrastructure to support narrowbody aircraft operations. The focus is on developing state-of-the-art facilities to attract international carriers for maintenance services. In Africa, the market is gradually evolving, with efforts to build local MRO capabilities to reduce dependence on foreign service providers. Analysis indicates that international collaborations and capacity-building initiatives are essential in enhancing MRO capabilities across the continent, which creates substantial narrowbody aircraft MRO market opportunities.

Latin American airlines are increasingly recognizing the importance of efficient MRO services to maintain operational reliability. A notable trend is the outsourcing of MRO activities to specialized providers to achieve cost-effectiveness and access to advanced technologies.

Top Key Players and Market Share Insights:

The Narrowbody Aircraft MRO market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Narrowbody Aircraft MRO market. Key players in the Narrowbody Aircraft MRO industry include -

- Aviation Technical Services (ATS) (USA)

- ST Aerospace (Singapore)

- SIA Engineering Company (Singapore)

- Delta TechOps (USA)

- KLM UK Engineering (UK)

- AAR Corp. (USA)

- Lufthansa Technik (Germany)

- HAECO Group (Hong Kong)

- Turkish Technic (Turkey)

- SR Technics (Switzerland)

Narrowbody Aircraft MRO Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 37,571.24 Million |

| CAGR (2025-2032) | 4.4% |

| By Service Type |

|

| By Aircraft Type |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Narrowbody Aircraft MRO Market? +

The Narrowbody Aircraft MRO Market size is estimated to reach over USD 37,571.24 Million by 2032 from a value of USD 27,147.78 Million in 2024 and is projected to grow by USD 27,800.95 Million in 2025, growing at a CAGR of 4.4% from 2025 to 2032.

What are the key segments in the Narrowbody Aircraft MRO Market? +

The market is segmented by service type (engine maintenance, airframe maintenance, component maintenance, line maintenance, etc.), aircraft type (fixed-wing, rotary-wing), and end-use (military, civil).

Which segment is expected to grow the fastest in the Narrowbody Aircraft MRO Market? +

The component maintenance segment is expected to register the fastest CAGR during the forecast period, driven by technological advancements and the increased focus on predictive maintenance.

Who are the major players in the Narrowbody Aircraft MRO Market? +

Key players in the Narrowbody Aircraft MRO market include Aviation Technical Services (ATS) (USA), ST Aerospace (Singapore), AAR Corp. (USA), Lufthansa Technik (Germany), HAECO Group (Hong Kong), Turkish Technic (Turkey), SR Technics (Switzerland), SIA Engineering Company (Singapore), Delta TechOps (USA), and KLM UK Engineering (UK).