- Summary

- Table Of Content

- Methodology

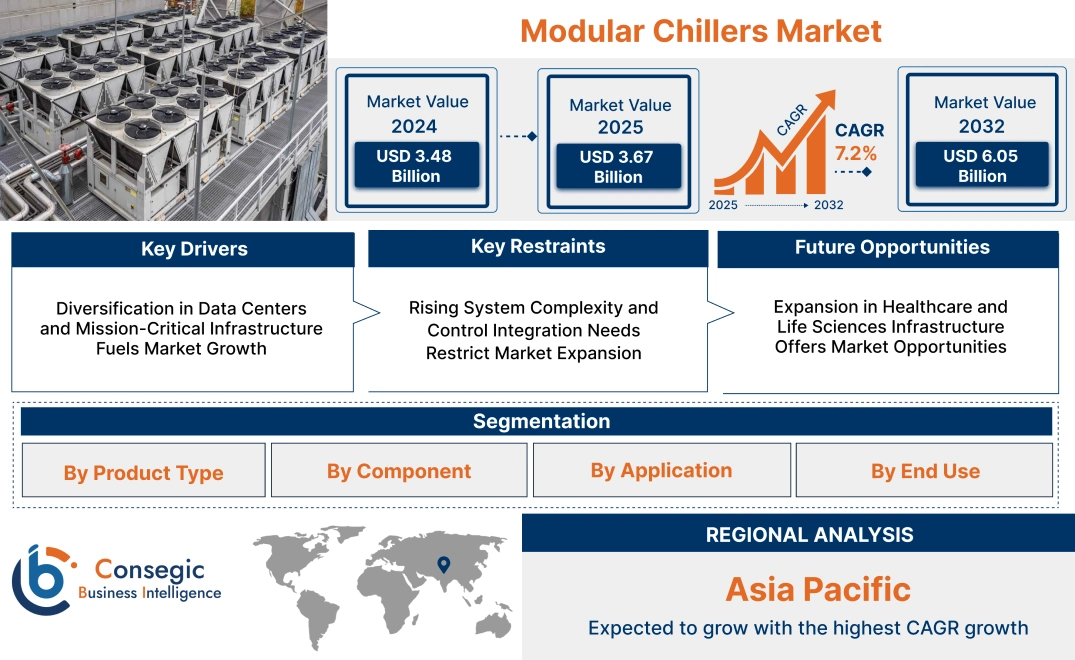

Modular Chillers Market Size:

Modular Chillers Market size is estimated to reach over USD 6.05 Billion by 2032 from a value of USD 3.48 Billion in 2024 and is projected to grow by USD 3.67 Billion in 2025, growing at a CAGR of 7.2% from 2025 to 2032.

Modular Chillers Market Scope & Overview:

Modular chillers are scalable cooling solutions made up of separate units, which operate individually or collectively, providing capacity flexibility for meeting different building requirements. They find application in commercial buildings, hospitals, industrial campuses, and educational institutions to provide accurate temperature control by circulating chilled water.

They come in air-cooled and water-cooled options and have compact footprints, smart controls, and simple service access. Modular construction provides phased installation, easy maintenance, and redundancy for uninterrupted operation in the event of servicing or load changes.

They enable energy optimization by varying output to correspond with real-time cooling load, increasing efficiency under variable load conditions. Their flexibility to work in retrofit and new construction applications makes them the choice for expansion projects as well as decentralized system configurations. Such a blend of operational flexibility, efficiency, and reliability makes them pertinent in today's HVAC planning and infrastructure development.

Modular Chillers Market Dynamics - (DRO):

Key Drivers:

Diversification in Data Centers and Mission-Critical Infrastructure Fuels Market Growth

The steady expansion of data centers, hyperscale computing centers, and mission-critical facilities is driving the installation of modular chillers. These facilities need to be cooled accurately, continuously, to provide thermal equilibrium and guarantee equipment lifespan. Modular chillers offer redundancy by distributed capacity, allowing for continuous operation even when a part of the system is under maintenance. Their adaptability allows scalable installation in phased IT infrastructure initiatives without interfering with operational systems. The small form factor is especially beneficial in edge data centers and co-lo facilities where space is at a premium. With growing worldwide data traffic and expansion of investments in cloud computing infrastructure, demand for highly efficient, fault-tolerant cooling is on the rise. As digital infrastructure extends into emerging markets and urban areas, it emerges as the go-to solution for operators who value resilience and operational responsiveness.

- For instance, in May 2024, Baidu received a patent for a modular cooling system for data centers. The proposed design comprised an airflow section forming a duct for air flow, a series of core units attached form a linear assembly, blower units attached to each core unit, motorized dampers placed between core units and the airflow section, fluid ports on each core unit, and at least one core unit loaded with various equipment. The equipment included combination of air filters, humidifiers, dehumidifiers, heat exchangers, evaporators, condensers, chillers, CRAC units, dry coolers, water spray systems, and cooling towers.

This convergence with the needs of critical infrastructure is one of the main drivers of the modular chillers market expansion.

Key Restraints:

Rising System Complexity and Control Integration Needs Restrict Market Expansion

Modular chillers use a network of interlinked units, and managing sequencing, load balancing, and energy optimization needs advanced control algorithms. Connecting these systems to legacy building management systems typically requires customized programming and sensor calibration. Sites without skilled HVAC engineers struggle to install and maintain these systems properly. Incorrect integration leads to less-than-optimal performance, higher cycling, and inefficiencies in energy consumption. Moreover, modular architecture troubleshooting becomes increasingly complicated as operational dependencies increase with system size. In smaller plants, the lack of experienced staff or proper digital infrastructure discourages adoption of sophisticated cooling solutions. This technical barrier retards adoption in markets that do not have strong engineering support, especially in developing economies or decentralized commercial buildings. Consequently, in spite of identified performance benefits, system complexity is a major limitation to modular chillers market growth.

Future Opportunities:

Expansion in Healthcare and Life Sciences Infrastructure Offers Market Opportunities

Healthcare and life sciences facilities require dependable and accurate thermal control to maintain indoor air quality, protect equipment, and facilitate critical processes like imaging, pharmaceutical storage, and lab research. Modular chillers achieve this through distributed redundancy and zone-cooling, which allows continuous operation even during maintenance cycles. Hospitals and research institutions increasingly choose modular systems for their capacity to grow with phased expansion of facilities, as well as their quick commissioning and smaller footprint. As global investments in healthcare infrastructure rise in the post-pandemic era, and pharmaceutical R&D facilities grow internationally, the need for advanced and robust HVAC systems is growing. Furthermore, regulatory focus on temperature stability and indoor environment control in healthcare facilities also contributes to the move towards modular systems. These industry-specific needs, coupled with modular scalability and reliability, are generating significant modular chillers market opportunities fueled by necessity and growth.

Modular Chillers Market Segmental Analysis :

By Product Type:

Based on product type, the modular chillers market is categorized into air-cooled and water-cooled modular chillers.

The air-cooled segment accounted for the largest revenue share in 2024.

- Air-cooled chillers are increasingly preferred due to their reduced installation complexity and lower maintenance costs compared to water-cooled variants.

- These chillers eliminate the need for cooling towers, making them more suitable for urban commercial installations and retrofitting projects.

- Technological advancements have enhanced energy efficiency and environmental compliance of air-cooled chillers, aligning with current market trends.

- For instance, in March 2025, Smardt launched the new AeroPure AF Series air-cooled chillers. This product line offers 36 models for data center cooling, with capacity range of 211 to 2500 kW and 36 models for comfort air conditioning, with capacities ranging from 211 to 1800 kW. The chillers contain oil-free, magnetically suspended compressors with the necessary certification to ensure reliable, safe, and code-compliant operation.

- With a rising need for decentralized cooling and fast deployment, the segment leads the modular chillers market demand across numerous industries.

The water-cooled segment is expected to witness the fastest CAGR over the forecast period.

- Water-cooled chillers are favored in large-scale projects where higher energy efficiency and cooling performance are critical.

- These systems are typically used in industrial or district cooling settings due to their ability to operate under high thermal loads.

- The segment is benefitting from market trends emphasizing energy conservation in high-demand infrastructure applications.

- As per modular chillers market analysis, the growing investments in green buildings and smart infrastructure support the rapid market growth for water-cooled solutions.

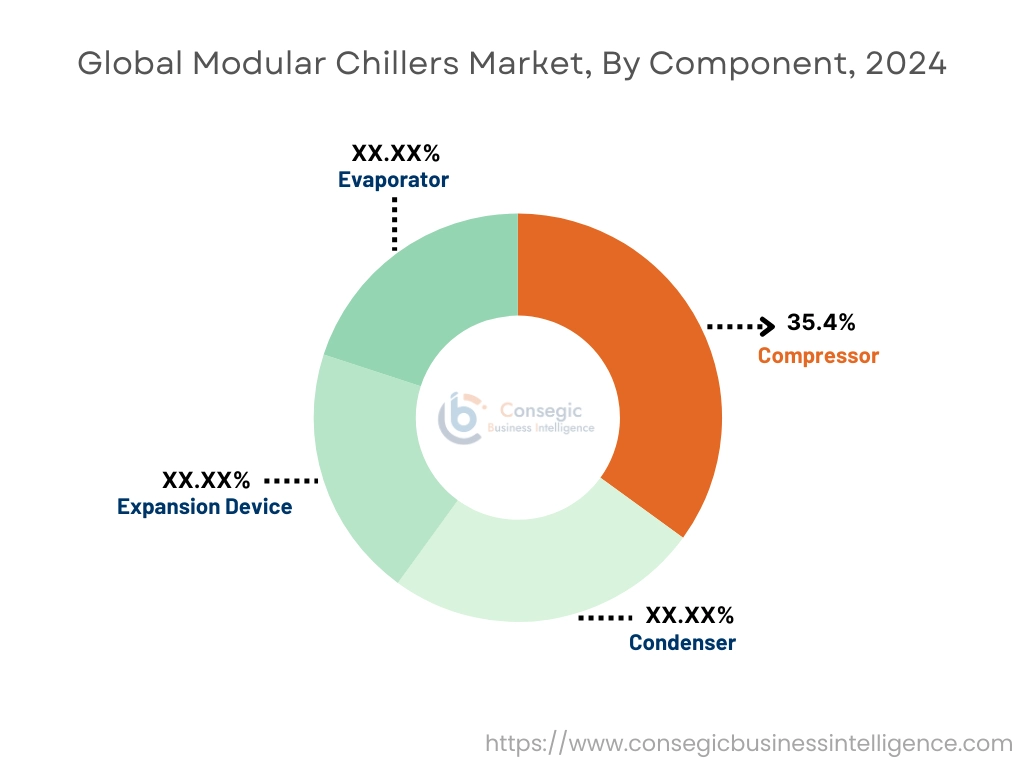

By Component:

Based on component, the market is segmented into compressor, condenser, expansion device, and evaporator.

The compressor segment accounted for the largest modular chillers market share of 35.4% in 2024.

- Compressors are central to chiller functionality and significantly influence system efficiency and lifecycle cost.

- In modular systems, high-efficiency variable-speed compressors enable adaptive cooling with precise load control.

- Technological integration, such as oil-free and magnetic bearing compressors, is enhancing component performance across markets.

- According to the modular chillers market analysis, compressors remain the key focus area for OEM innovation, driving both product differentiation and market expansion.

The evaporator segment is projected to exhibit the fastest CAGR over the forecast period.

- Rising need for modular systems with high heat exchange efficiency supports rapid adoption of next-gen evaporators.

- Plate-type and microchannel evaporators offer compact design, better thermal conductivity, and reduced refrigerant charge.

- These systems are suited for space-constrained environments, a critical factor amid the increasing modular chillers market demand.

- Market trends highlight growing applications in data centers and healthcare facilities, where space optimization is crucial.

By Application:

Based on application, the modular chillers market is segmented into space cooling, process cooling, and district cooling.

The space cooling segment held the largest revenue share in 2024.

- Space cooling dominates as they are widely deployed in commercial and institutional buildings for HVAC applications.

- Their modularity supports phased installations and reduces upfront capital investment for building owners.

- With rising urbanization and emphasis on energy-efficient buildings, the need is increasing for scalable cooling solutions.

- Modular chillers market trends show strong adoption in retrofitting older buildings to meet energy regulations.

The process cooling segment is expected to witness the fastest CAGR during the forecast period.

- Manufacturing and pharmaceutical sectors increasingly require precise thermal control for equipment and product safety.

- They provide redundancy and reliability in continuous operations, making them ideal for mission-critical cooling.

- Market analysis shows rising requirement from electronics manufacturing and food processing due to strict thermal standards.

- As the modular chillers market growth continues, process cooling emerges as a key area of equipment innovation and investment.

By End Use:

Based on end-use, the market is divided into commercial, industrial, institutional, and others.

The commercial segment accounted for the largest modular chillers market share in 2024.

- Commercial facilities such as office buildings, malls, and hospitality establishments rely heavily on HVAC systems for occupant comfort.

- They offer a cost-effective, space-saving, and energy-efficient solution, supporting broader market adoption.

- Demand is further driven by the need to meet green building certification and carbon emission goals.

- According to modular chillers market trends, the commercial sector remains the primary contributor to global revenues.

The industrial segment is expected to have the fastest CAGR during the forecast period.

- Industries like food & beverage, pharmaceuticals, and chemicals increasingly prefer these products for their reliability and scalability.

- Growth is supported by rising automation and process integration in production environments requiring consistent cooling.

- Market analysis indicates a shift toward decentralized cooling infrastructure in factory settings.

- The increase in capacity in industrial zones across Asia-Pacific and the Middle East is expected to propel the modular chillers market expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

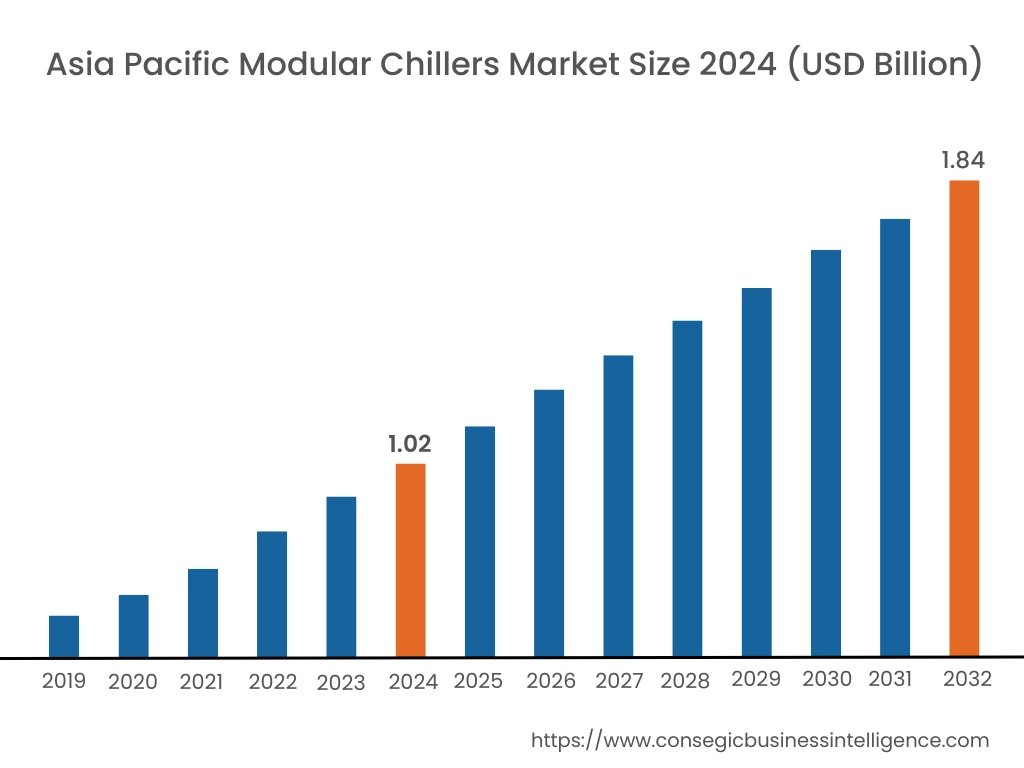

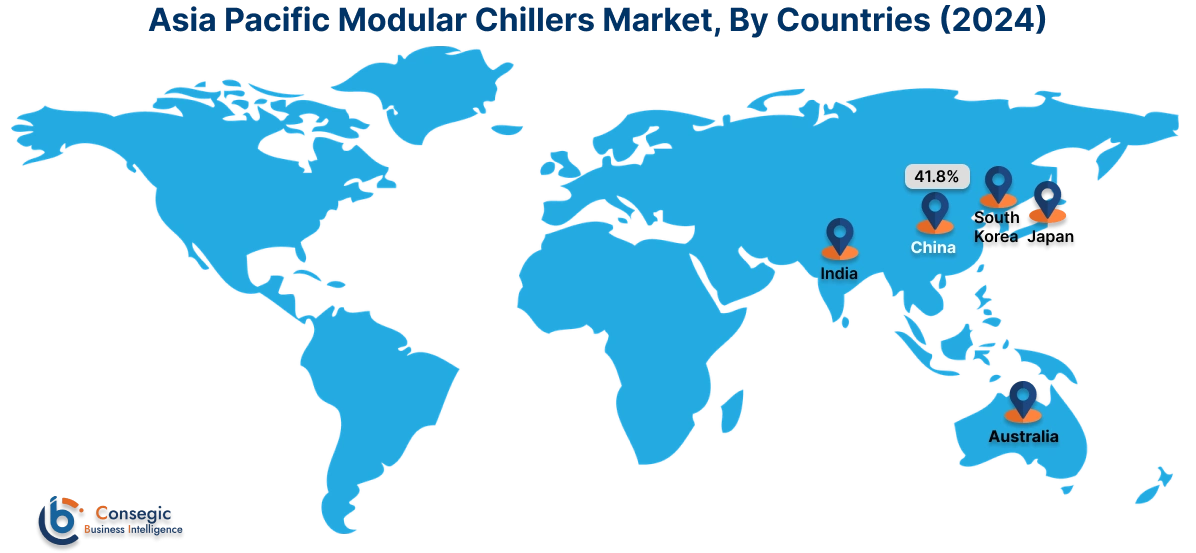

Asia Pacific region was valued at USD 1.02 Billion in 2024. Moreover, it is projected to grow by USD 1.08 Billion in 2025 and reach over USD 1.84 Billion by 2032. Out of this, China accounted for the maximum revenue share of 41.8%. Asia-Pacific is seeing the most rapid growth in the modular chillers market, led by increased urbanization, smart city initiatives, and growing demand for air conditioning in tropical and subtropical regions. China, India, Japan, and South Korea are seeing growing commercial building and increasing investments in high-rise buildings, airports, and technology parks. Regional trends indicate growing demand for modular systems due to their scalability and low maintenance, particularly in buildings with variable cooling loads. The modular chillers market opportunity is rapidly increasing in this region as governments focus on energy efficiency in buildings and localized climate control systems for expanding urban areas.

North America is estimated to reach over USD 1.96 Billion by 2032 from a value of USD 1.15 Billion in 2024 and is projected to grow by USD 1.21 Billion in 2025. North America holds a dominant position in the modular chillers industry due to robust commercial infrastructure, retrofit activities, and adoption of energy-efficient cooling technologies in healthcare, education, and data center applications. Modular systems are preferred in the United States and Canada for load flexibility and benefits of redundancy. Analysis indicates that policies favoring sustainability, HVAC operations decarbonization needs, and tax credits for green building technologies are propelling steady demand. Additionally, there is an increased need for hybrid chillers combining electric and clean sources to support continued expansion in both city and suburban building sectors.

- For instance, in February 2025, Clivet debuted Mits Airconditioning as the master distributor of their products in North America. This partnership enables the entry of Clivet, one of the leading European heat pump manufacturers, into the North American market with the introduction of a vast product line including heat pumps, chillers, fan coils, polyvalent heat recovery units, free cooling chillers and modular chillers/heat pumps.

Europe has a very technologically advanced but fast-changing market, with modular chillers utilized in response to energy performance regulation and urban intensification. Germany, France, and the UK are leading nations actively retrofitting HVAC systems within public buildings and commercial properties toward net-zero. There is a strong need from customers for all types of chiller products. Market analysis shows increasing adoption in district cooling schemes and renovated heritage buildings where decentralized, noiseless, and space-saving systems are priorities. Moreover, the shift towards combining chillers with heat recovery and thermal storage modules places the country at the forefront of technology integration and long-term efficiency planning.

In Latin America, the market is emerging with gradual improvement in urban and commercial development. Brazil, Mexico, and Chile lead the modernization drive in retail hubs, hotels, and government complexes. While traditional chillers remain predominant, trends show a trend toward modular systems as a result of enhanced transparency in energy consumption and system flexibility. Increased concern regarding energy-efficient cooling and global cooperation on green building codes are likely to fuel demand. Financial incentives and supply chain localization will be key to driving wider adoption in second-tier cities.

The Middle East and Africa region demonstrates increasing potential, especially in the Gulf countries and fast-developing areas of North and Sub-Saharan Africa. In the UAE and Saudi Arabia, requirement is driven by large-scale infrastructure, such as hotels, airports, and commercial towers, where modular chillers provide climate resilience and capacity optimization. Analysis highlights their increasing application in mixed-use developments where redundancy of the system and fast deployment are imperative. In Africa, public-private infrastructure projects are starting to include modular HVAC systems, although take-up remains in infancy. Increased investment in sustainable building and energy security is anticipated to underpin steady but promising development.

Top Key Players & Market Share Insights:

The modular chillers market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global modular chillers market. Key players in the modular chillers industry include -

- Trane Technologies plc (Ireland)

- Gree Electric Appliances, Inc. (China)

- Johnson Controls International plc (Ireland)

- Haier Group (China)

- Mitsubishi Electric Corporation (Japan)

- Carrier Corporation (USA)

- Frigel Firenze S.p.A. (Italy)

- Midea Group (China)

- Multistack LLC (USA)

- Daikin Industries Ltd. (Japan)

Recent Industry Developments :

Acquisitions:

- In December 2024, Vertiv, a global provider of critical digital infrastructure and continuity solutions, announced the acquisition by its Chinese subsidiary of certain assets and technologies of BiXin Energy Technology (Suzhou) Co., Ltd, a manufacturer of chillers, heat pumps, heat-recovery solutions and air-handling units. This move expands Vertiv’s global product offerings.

Partnerships:

- In February 2025, ACI Mechanical partnered with ChillMaster to expand the modular chiller options available to customers. This collaboration will allow ACI Mechanical to provide more adaptable heating and cooling solutions to their territories in Washington, Oregon and Northern Idaho.

Modular Chillers Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 6.05 Billion |

| CAGR (2025-2032) | 7.2% |

| By Product Type |

|

| By Component |

|

| By Application |

|

| By End Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Modular Chillers Market? +

Modular Chillers Market size is estimated to reach over USD 6.05 Billion by 2032 from a value of USD 3.48 Billion in 2024 and is projected to grow by USD 3.67 Billion in 2025, growing at a CAGR of 7.2% from 2025 to 2032.

What specific segmentation details are covered in the Modular Chillers Market report? +

The Modular Chillers market report includes specific segmentation details for product type, component, application and end-use.

What are the end-uses in the Modular Chillers Market? +

The end-uses of the Modular Chillers Market are commercial, institutional, industrial, data centres and others.

Who are the major players in the Modular Chillers Market? +

The key participants in the Modular Chillers market are Trane Technologies plc (Ireland), Gree Electric Appliances, Inc. (China), Carrier Corporation (USA), Frigel Firenze S.p.A. (Italy), Midea Group (China), Multistack LLC (USA), Daikin Industries Ltd. (Japan), Johnson Controls International plc (Ireland), Haier Group (China) and Mitsubishi Electric Corporation (Japan).