- Summary

- Table Of Content

- Methodology

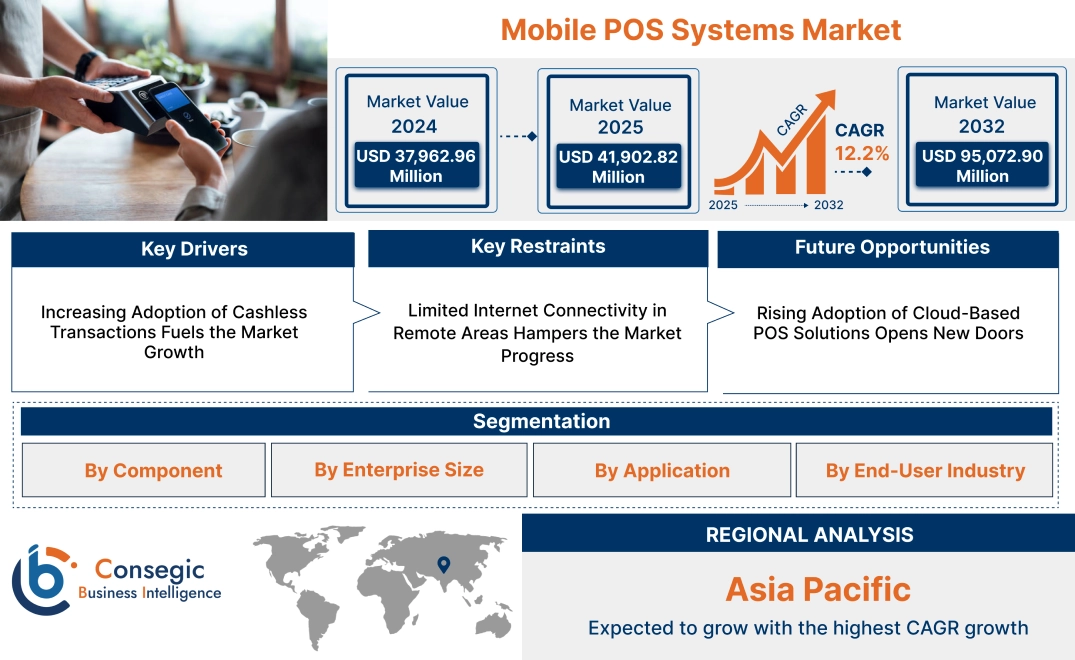

Mobile POS Systems Market Size:

Mobile POS Systems Market size is estimated to reach over USD 95,072.90 Million by 2032 from a value of USD 37,962.96 Million in 2024 and is projected to grow by USD 41,902.82 Million in 2025, growing at a CAGR of 12.2% from 2025 to 2032.

Mobile POS Systems Market Scope & Overview:

Mobile POS systems are portable point-of-sale solutions that enable businesses to process transactions using mobile devices such as smartphones, tablets, or dedicated handheld terminals. These systems are equipped with features such as card readers, receipt printers, and inventory management tools, allowing seamless payment processing and efficient management of sales operations. They are widely used across retail, hospitality, and other service-based industries.

These systems are designed for flexibility and ease of use, providing businesses with the ability to accept payments anywhere, enhance customer experiences, and streamline operations. These POS systems often integrate with existing payment gateways and software, offering compatibility with a variety of payment methods, including credit cards, digital wallets, and contactless payments. Advanced solutions also include features like real-time reporting, employee management, and customer relationship tools.

End-users include small businesses, restaurants, and retail chains seeking efficient and portable payment solutions to optimize their transaction processes. Mobile POS systems play a critical role in modernizing payment infrastructure and supporting on-the-go sales activities.

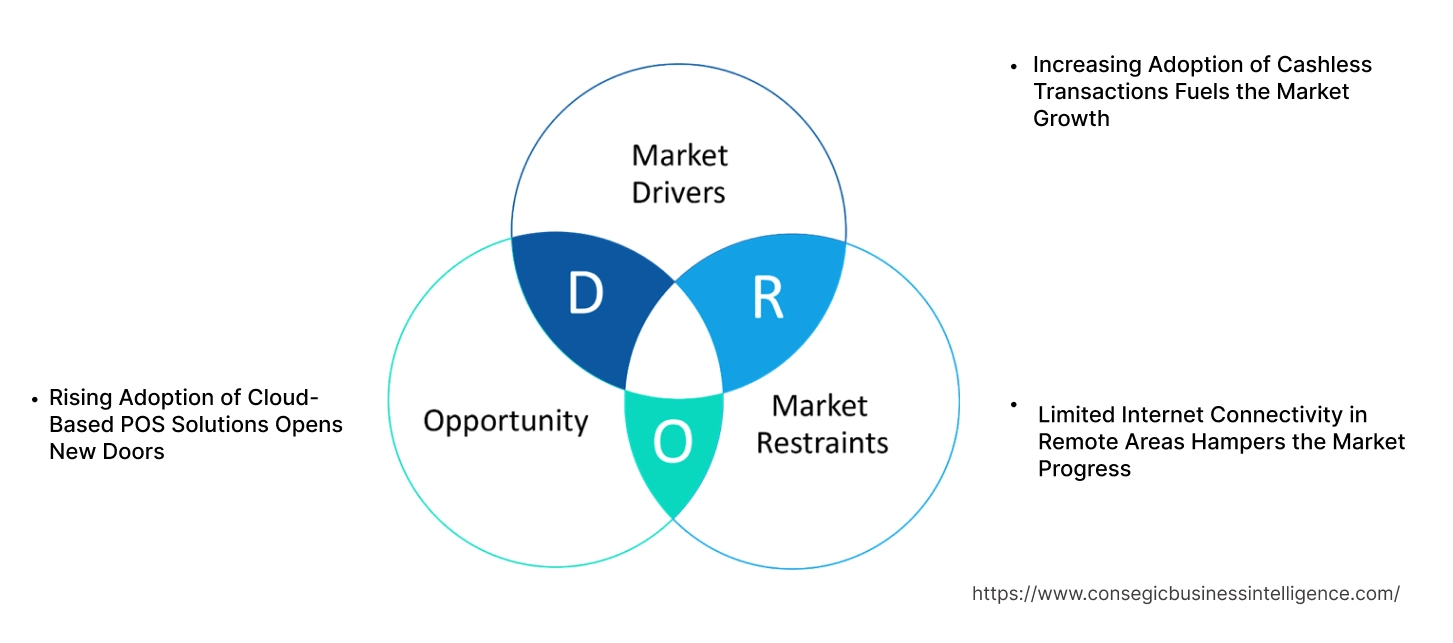

Mobile POS Systems Market Dynamics - (DRO) :

Key Drivers:

Increasing Adoption of Cashless Transactions Fuels the Market Growth

The increasing shift towards cashless and contactless transactions is significantly driving growth in the payment processing sector. As digital payments and mobile wallets become more mainstream, businesses across various industries, including retail, hospitality, and services, are adopting payment solutions that enable quick, secure, and efficient transactions. The convenience of tap-and-go payments and the security features offered by digital wallets are fueling consumer preference for cashless transactions. Additionally, the growing adoption of contactless payments is enhancing the customer experience by reducing wait times and minimizing physical contact, particularly in light of health and safety concerns. For businesses, this shift presents an opportunity to streamline operations, reduce the handling of physical currency, and improve transaction accuracy. As consumer behavior continues to evolve towards digital-first payments, the demand for seamless, efficient, and secure transaction solutions will continue to grow across industries. Thus, the aforementioned factors are driving the mobile POS systems market growth.

Key Restraints:

Limited Internet Connectivity in Remote Areas Hampers the Market Progress

Limited internet connectivity in remote areas poses a significant challenge for businesses relying on digital payment solutions. These systems require a stable internet connection to process transactions and sync data with central servers. In regions with unreliable or limited network coverage, businesses face delays or failures in transaction processing, leading to disruptions in operations and poor customer experience. For industries operating in rural or off-the-grid areas, this connectivity issue limits the effectiveness and reliability of digital payment solutions, making them less viable. Additionally, inconsistent internet access hinders real-time data updates, affecting inventory management, sales tracking, and reporting. As the demand for seamless, on-the-go payment solutions increases, addressing the issue of connectivity in remote areas will be crucial to expanding the use and reliability of digital payment systems across diverse geographical locations. Thus, the above factors limit the mobile POS systems market demand.

Future Opportunities :

Rising Adoption of Cloud-Based POS Solutions Opens New Doors

Cloud technology enables real-time data synchronization, ensuring that transaction information is instantly updated across multiple devices, which enhances operational efficiency. Businesses benefit from remote access to their POS systems, allowing managers to monitor sales, inventory, and performance from any location. Additionally, cloud-based solutions automatically update software, reducing the time and costs associated with manual updates and hardware maintenance. This streamlined approach ensures that businesses stay up-to-date with the latest features, security patches, and compliance requirements without the burden of managing complex infrastructure. The flexibility and scalability offered by cloud technology also allow businesses to easily expand their operations and integrate with other software applications, making cloud-based solutions increasingly attractive to retailers, restaurants, and service industries looking to improve efficiency, reduce costs, and enhance customer experiences. Therefore, the above mentioned factors create new mobile POS systems market opportunites.

Mobile POS Systems Market Segmental Analysis :

By Component:

Based on component, the market is segmented into hardware, software, and services.

The hardware segment accounted for the largest revenue of the total mobile POS systems market share in 2024.

- Hardware components, such as card readers, barcode scanners, and receipt printers, are essential for facilitating mobile POS transactions, particularly in retail and hospitality environments.

- Portable and compact devices, such as handheld terminals and tablets, are increasingly favored by businesses aiming to enhance flexibility and mobility in their payment processes.

- Advancements in hardware technology, including contactless payment compatibility and integration with biometric authentication, support the dominance of this segment.

- As per mobile POS systems market analysis, the continuous adoption of multi-functional devices tailored for specific industries ensures the widespread usage of hardware in mobile POS systems.

The software segment is anticipated to grow at the fastest CAGR during the forecast period.

- Mobile POS software enables businesses to streamline operations, including inventory tracking, sales reporting, and customer management, driving its rapid adoption.

- Cloud-based software solutions are particularly popular due to their scalability, affordability, and ability to provide real-time updates across multiple locations.

- Integration with advanced analytics tools allows businesses to gain actionable insights, enhancing decision-making and customer engagement.

- The growing preference for customizable and industry-specific software solutions propels this segment’s growth, fueling the mobile POS systems market expansion.

By Enterprise Size:

Based on enterprise size, the market is segmented into large enterprises and small & medium enterprises (SMEs).

The large enterprise segment accounted for the largest revenue of the total mobile POS systems market share in 2024.

- Large enterprises, particularly in retail and hospitality, adopt mobile POS systems to manage complex operations across multiple outlets and regions.

- These enterprises benefit from advanced features like real-time data synchronization, multi-location management, and robust reporting capabilities.

- Investments in comprehensive mobile POS solutions that integrate with enterprise resource planning (ERP) and customer relationship management (CRM) systems reinforce the dominance of this segment.

- As per mobile POS systems market trends, the need for enhanced operational efficiency and seamless customer experiences drives the adoption of these POS systems among large enterprises.

The SMEs segment is projected to grow at the fastest CAGR during the forecast period.

- Mobile POS systems offer cost-effective and easy-to-deploy solutions for small and medium-sized businesses, addressing their need for efficient and flexible payment processing.

- SMEs increasingly adopt mobile POS solutions to improve inventory management, streamline billing, and enhance customer engagement without significant infrastructure investment.

- Cloud-based platforms with subscription-based pricing models appeal to SMEs, providing access to advanced features without high upfront costs.

- As per mobile POS systems market analysis, the rising number of small businesses globally and their growing focus on digital transformation support the rapid adoption of these POS systems in this segment.

By Application:

Based on application, the market is segmented into inventory management, billing, customer engagement, reporting & analytics, and others.

The billing segment accounted for the largest revenue share in 2024.

- Mobile POS systems simplify billing processes by enabling businesses to accept payments from various methods, including credit/debit cards, mobile wallets, and contactless payments.

- The ability to generate invoices and receipts instantly enhances customer satisfaction and operational efficiency, particularly in fast-paced environments like retail and food service.

- Businesses leverage mobile POS billing features to reduce checkout times, eliminate long queues, and improve customer experiences.

- Thus, the increasing adoption of cashless payment methods and seamless integration of billing systems with accounting tools support the segment’s leadership, driving the mobile POS systems market growth.

The inventory management segment is anticipated to grow at the fastest CAGR during the forecast period.

- Mobile POS systems with integrated inventory management features allow businesses to monitor stock levels in real-time, minimizing overstocking and stockouts.

- These systems enable businesses to track sales patterns and optimize inventory replenishment, improving operational efficiency and profitability.

- The adoption of inventory-focused POS systems is particularly strong in retail and food service industries, where effective stock management is critical.

- Therefore, as per the market trends, the advancements in inventory tracking technologies, including barcode and RFID integration, enhance the capabilities of POS systems in inventory management, fueling the mobile POS systems market demand.

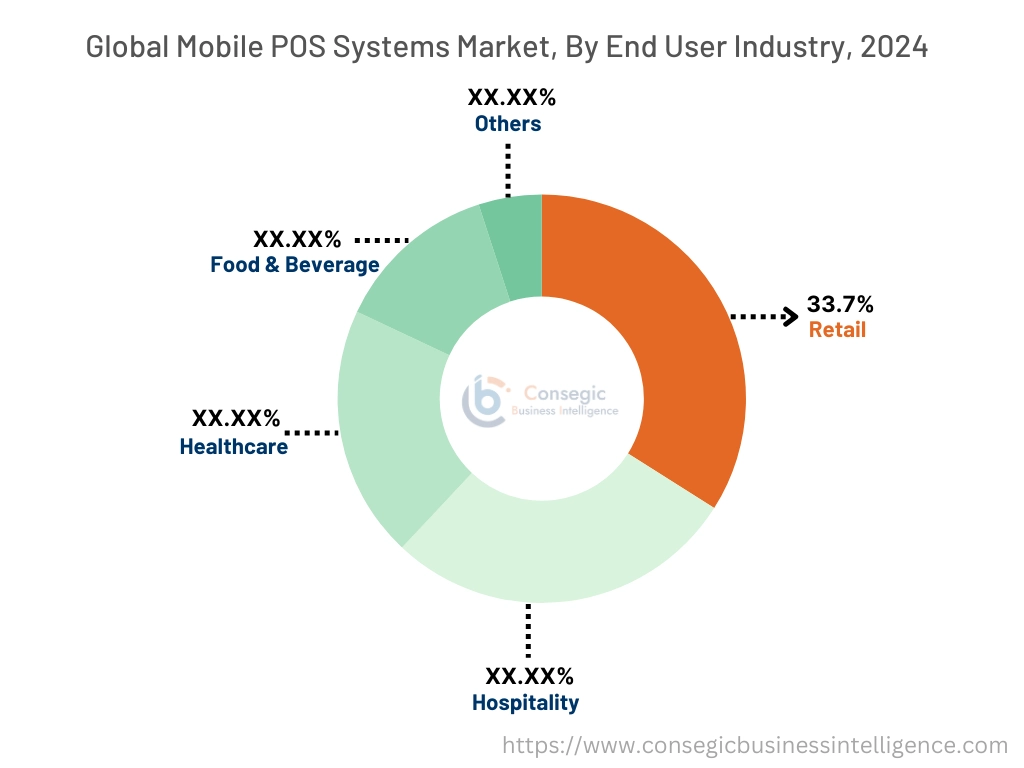

By End-User Industry:

Based on end-user industry, the market is segmented into retail, hospitality, healthcare, food & beverage, and others.

The retail segment accounted for the largest revenue of 33.7% share in 2024.

- Retail businesses extensively adopt mobile POS systems to improve checkout efficiency, enhance customer engagement, and manage inventory effectively.

- The growing trend of omnichannel retailing, where businesses aim to provide seamless shopping experiences across online and offline platforms, drives the adoption of POS systems.

- Features like customer data capture and targeted promotions make these POS systems integral to modern retail strategies.

- Thus, the continuous progress of retail chains and the increasing focus on improving in-store experiences support the segment’s dominance, contributing to the mobile POS systems market expansion.

The food & beverage segment is projected to grow at the fastest CAGR during the forecast period.

- Mobile POS systems are increasingly adopted in food trucks, quick-service restaurants (QSRs), and cafes to streamline billing and order management.

- Features like table-side ordering, split billing, and integration with kitchen display systems enhance operational efficiency in the food & beverage industry.

- The growing demand for contactless payment solutions and digital receipts further accelerates the adoption of POS systems in this sector.

- As per mobile POS systems market trends, the rise of delivery and takeaway services has prompted food & beverage businesses to invest in mobile POS solutions that support flexible and efficient operations.

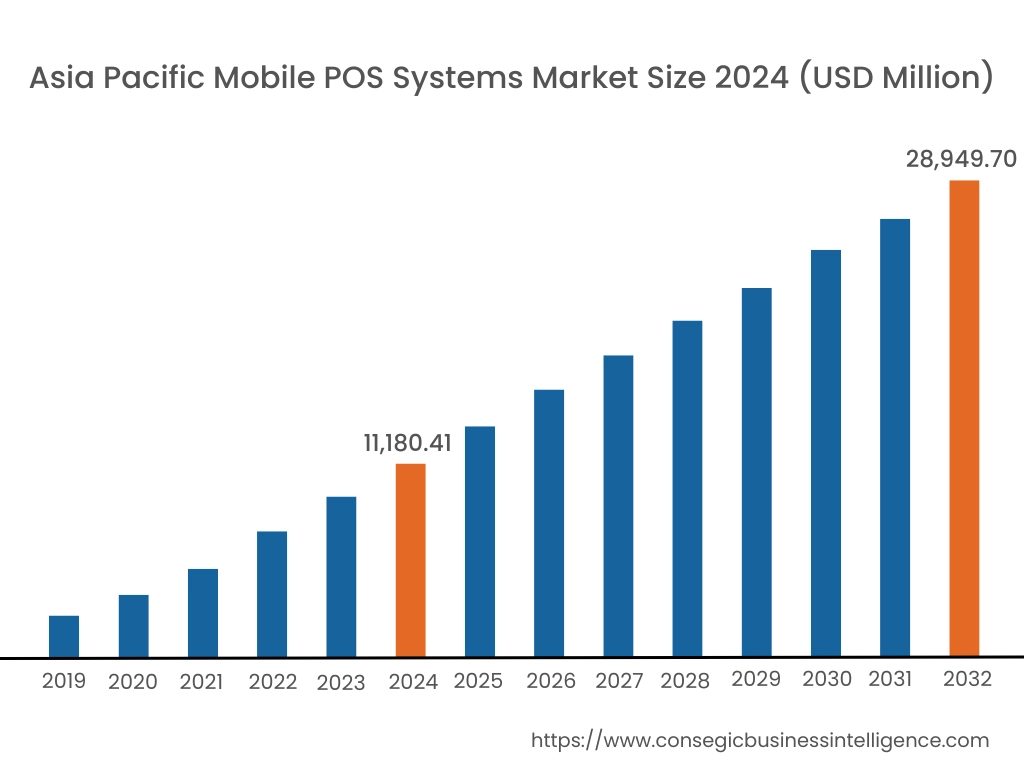

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

Asia Pacific region was valued at USD 11,180.41 Million in 2024. Moreover, it is projected to grow by USD 12,375.62 Million in 2025 and reach over USD 28,949.70 Million by 2032. Out of this, China accounted for the maximum revenue share of 32.6%. The Asia-Pacific region dominates the mPOS market, attributed to rapid urbanization and the proliferation of small and medium-sized enterprises (SMEs). A prominent trend is the utilization of mPOS systems in retail and hospitality sectors to streamline operations and enhance customer service. Analysis indicates that government initiatives supporting digital payments and the increasing affordability of smartphones are contributing to mobile POS systems market opportunities in this region.

North America is estimated to reach over USD 30,813.13 Million by 2032 from a value of USD 12,592.63 Million in 2024 and is projected to grow by USD 30,813.13 Million in 2025. This region maintains a substantial position in the mPOS market, driven by the increasing adoption of mobile payment technologies and high smartphone penetration. A notable trend is the shift towards cloud-based mPOS solutions, offering scalability and real-time data access for businesses. Analysis indicates that the emphasis on enhancing customer experience and operational efficiency is propelling the market in North America.

European countries are pivotal in the mPOS market, with a strong focus on secure and seamless payment solutions. A significant trend is the rise in contactless payments, supported by the widespread use of digital wallets and NFC-enabled devices. Analysis suggests that regulatory frameworks promoting cashless transactions and the integration of advanced technologies are influencing the adoption of mPOS systems in this region.

In the Middle East and Africa, the mPOS market is influenced by the adoption of innovative payment solutions to cater to a diverse and growing consumer base. The focus is on deploying mPOS systems in sectors like retail and transportation to facilitate convenient transactions. Analysis suggests that the enlargement of the e-commerce sector and the need for financial inclusion are pivotal in shaping the market landscape in these regions.

Latin American countries are increasingly recognizing the potential of mPOS systems in transforming traditional payment methods. A notable trend is the collaboration between financial institutions and technology providers to offer integrated mPOS solutions. Analysis indicates that the rising penetration of mobile devices and the push for cashless economies are key factors influencing the market in this region.

Top Key Players and Market Share Insights:

The Mobile POS Systems market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Mobile POS Systems market. Key players in the Mobile POS Systems industry include –

- Square, Inc. (USA)

- Ingenico Group (France)

- PAX Technology Limited (China)

- Newland Payment Technology (China)

- eMobilePOS (Puerto Rico)

- Intuit Inc. (USA)

- PayPal Holdings, Inc. (USA)

- Adyen N.V. (Netherlands)

- VeriFone Systems, Inc. (USA)

Recent Industry Developments :

Business Expansion:

- In January 2024, Unzer launched its mobile POS solutions in Austria and Luxembourg, extending its presence in Europe’s payment sector. The portfolio includes iPad cash registers, card terminals, and the POS Go mini checkout with an integrated card reader, printer, and scanner. Already serving 40,000+ merchants in Germany, Unzer aims to support SMEs in digitizing payments. With cloud-based software, real-time sales data, and "buy now, pay later" options, Unzer’s Unified Commerce strategy enhances seamless online and offline transactions.

Partnerships & Collaborations:

- In January 2025, Jumpmind partnered with Landmark Retail for POS and Promotions Expansion across eight Middle Eastern countries. This marks Jumpmind’s entry into the region, expanding its global presence. The deployment includes Jumpmind Commerce for fixed and mobile POS, RFID-enabled self-checkout, and Jumpmind Promote for unified promotions. With multi-language, multi-currency support, and cloud-native architecture, the technology enhances store operations and customer engagement, reinforcing Landmark’s innovation-driven retail growth.

- In January 2024, Jabil and fintech leader Revolut continue their collaboration to scale the Revolut Reader, a compact mPOS solution for secure, instant in-person transactions. Jabil's expertise in POS hardware, software integration, and manufacturing accelerates Revolut’s global expansion in merchant acquiring. The Revolut Reader supports contactless, chip, PIN, and mobile payments, ensuring fast, compliant, and seamless transactions. As demand grows, both companies are enhancing features and scaling production to meet evolving retail and digital commerce needs.

Mobile POS Systems Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 95,072.90 Million |

| CAGR (2025-2032) | 12.2% |

| By Component |

|

| By Enterprise Size |

|

| By Application |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Mobile POS Systems Market? +

The Mobile POS Systems Market size is estimated to reach over USD 95,072.90 Million by 2032 from a value of USD 37,962.96 Million in 2024 and is projected to grow by USD 41,902.82 Million in 2025, growing at a CAGR of 12.2% from 2025 to 2032.

What are the key segments in the Mobile POS Systems Market? +

The market is segmented by component (hardware, software, services), enterprise size (large enterprises, small & medium enterprises), application (inventory management, billing, customer engagement, reporting & analytics, others), and end-user industry (retail, hospitality, healthcare, food & beverage, others).

Which segment is expected to grow the fastest in the Mobile POS Systems Market? +

The software segment is anticipated to grow at the fastest CAGR during the forecast period, driven by the increasing adoption of cloud-based solutions that offer scalability, affordability, and real-time updates across multiple locations.

Who are the major players in the Mobile POS Systems Market? +

Key players in the Mobile POS Systems market include Square, Inc. (USA), Ingenico Group (France), Intuit Inc. (USA), PayPal Holdings, Inc. (USA), Adyen N.V. (Netherlands), VeriFone Systems, Inc. (USA), PAX Technology Limited (China), Newland Payment Technology (China), eMobilePOS (Puerto Rico).