- Summary

- Table Of Content

- Methodology

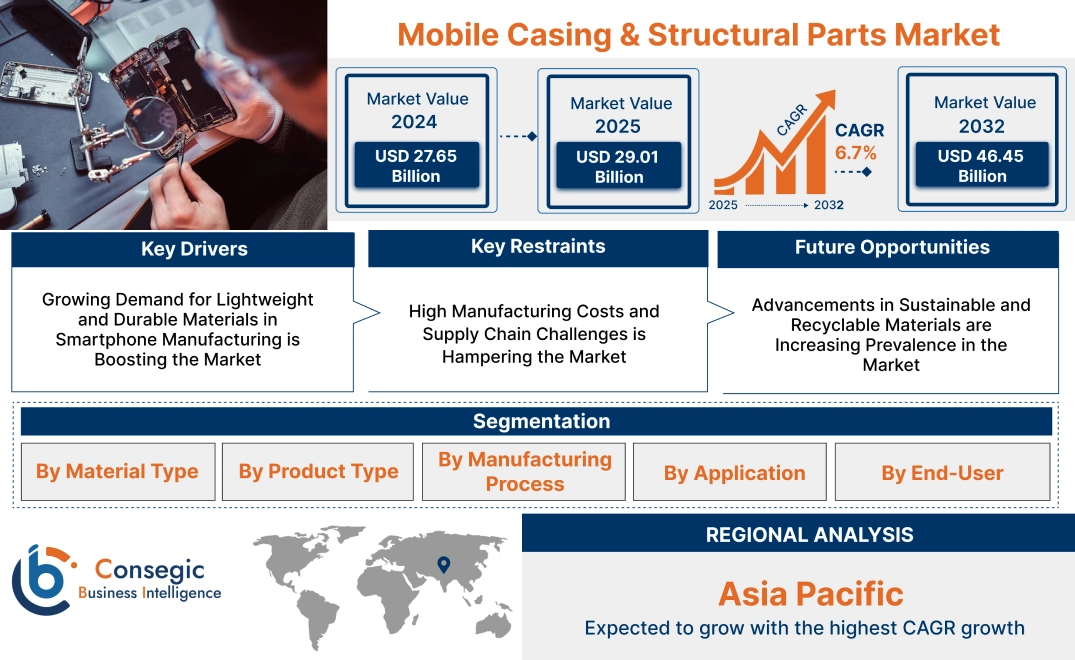

Mobile Casing & Structural Parts Market Size:

The Mobile Casing & Structural Parts Market size is estimated to reach over USD 46.45 Billion by 2032 from a value of USD 27.65 Billion in 2024 and is projected to grow by USD 29.01 Billion in 2025, growing at a CAGR of 6.7% from 2025 to 2032.

Mobile Casing & Structural Parts Market Scope & Overview:

The mobile casing and structural parts are external and internal components that form the body and framework of mobile devices, including smartphones, tablets, and wearable devices. These parts, such as casings, frames, and structural supports, are designed to provide durability, aesthetics, and protection for the internal components of mobile devices while maintaining a lightweight and compact design.

Key characteristics of mobile casings and structural parts include high precision, material versatility (such as aluminum, magnesium alloys, carbon fiber, and polycarbonate), and advanced surface finishes for aesthetics and user comfort. The benefits include enhanced device durability, improved thermal management, and the ability to support slim and ergonomic designs.

Applications span consumer electronics, including smartphones, tablets, laptops, and wearables. End-users include OEMs (original equipment manufacturers) and contract manufacturers in the electronics industry, driven by increasing consumer demand for lightweight, durable, and stylish devices, advancements in material science, and the growing adoption of sustainable and recyclable materials in device manufacturing.

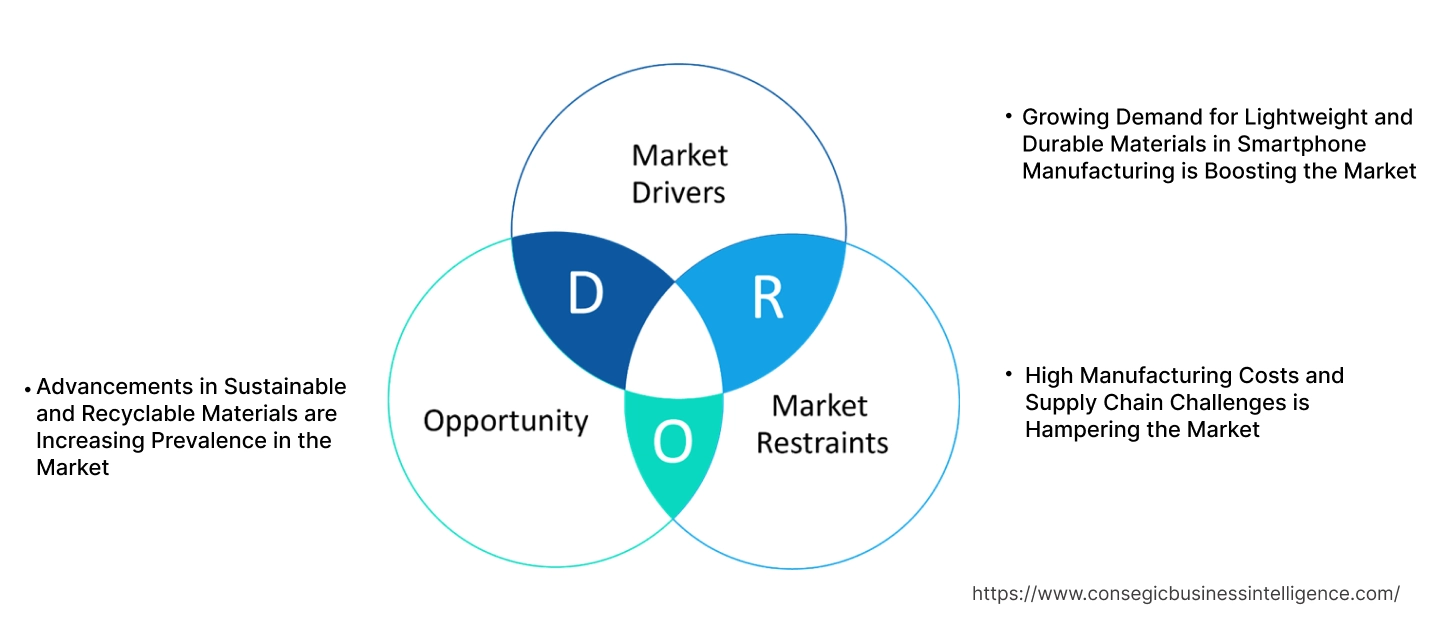

Mobile Casing & Structural Parts Market Dynamics - (DRO) :

Key Drivers:

Growing Demand for Lightweight and Durable Materials in Smartphone Manufacturing is Boosting the Market

The rising consumer demand for lightweight and durable smartphones is driving the mobile casing and structural parts market. With advancements in technology, manufacturers are focusing on using innovative materials such as aluminum alloys, magnesium alloys, carbon fiber, and polycarbonate to create robust yet lightweight casings and structural components. These materials not only enhance the device's durability and aesthetic appeal but also improve heat dissipation and impact resistance. Additionally, the increasing mobile casing & structural parts market trends toward premium smartphones with metallic or glass finishes have further fueled the requirement for high-quality casing and structural parts. The emphasis on slimmer, more compact designs in smartphones has also driven the development of advanced structural components that optimize space utilization without compromising strength.

Key Restraints:

High Manufacturing Costs and Supply Chain Challenges is Hampering the Market

The high cost of advanced materials and manufacturing processes poses a significant challenge for the mobile casing and structural parts market. Premium materials such as titanium and carbon fiber, while offering superior performance, significantly increase production costs, limiting their adoption in mid-range and budget smartphones. Additionally, the complexity of machining and processing these materials requires specialized equipment and expertise, further driving up costs. The market is also impacted by supply chain disruptions, particularly in sourcing raw materials, which can delay production and affect pricing. These challenges are particularly pronounced in cost-sensitive markets where affordability is a primary concern.

Future Opportunities:

Advancements in Sustainable and Recyclable Materials are Increasing Prevalence in the Market

The increasing focus on sustainability presents a significant growth opportunity for the mobile casing and structural parts market. Manufacturers are investing in eco-friendly materials, such as recycled aluminum and biodegradable polymers, to meet rising consumer demand for environmentally responsible products. These materials not only reduce the environmental footprint of smartphone production but also align with government regulations and corporate sustainability goals. Furthermore, advancements in material science, such as self-healing coatings and graphene-based composites, offer opportunities to enhance durability and performance while maintaining sustainability. Companies that innovate in sustainable materials and production processes are well-positioned to capitalize on the growing adoption for eco-friendly mobile devices.

These dynamics underscore the critical role of material innovation in shaping the mobile casing and structural parts market. While high manufacturing costs and supply chain challenges remain significant barriers, advancements in sustainable materials and designs offer promising pathways for mobile casing & structural parts market expansion and differentiation.

Mobile Casing & Structural Parts Market Segmental Analysis :

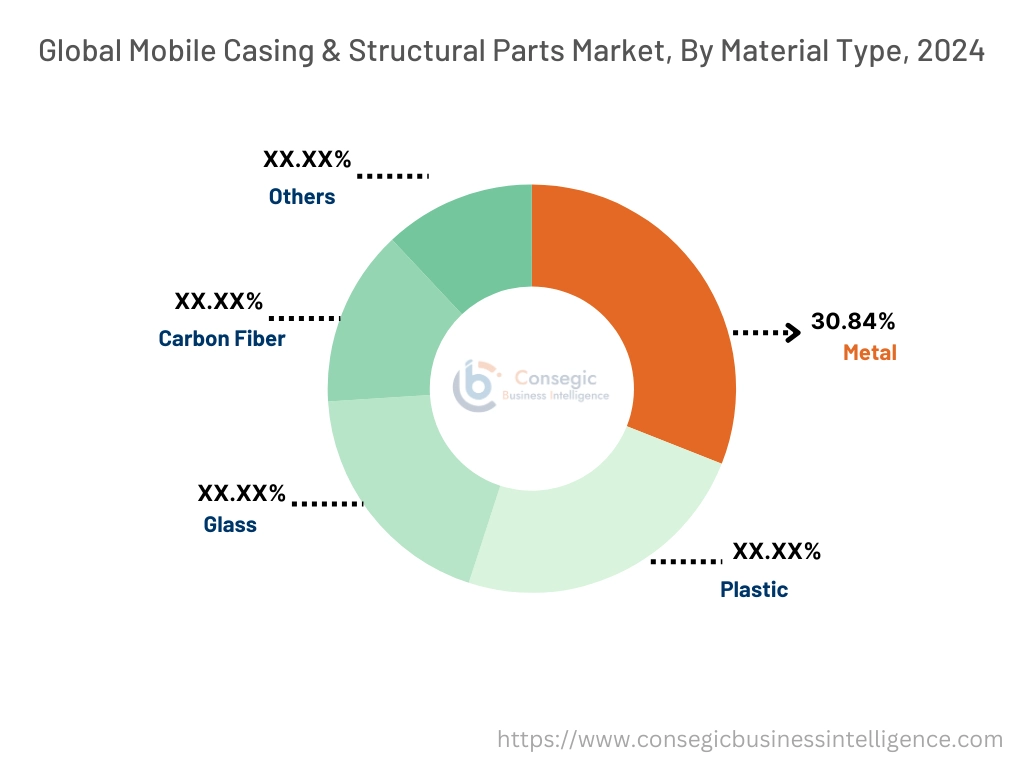

By Material Type:

Based on material type, the market is segmented into metal, plastic, glass, carbon fiber, and others.

The metal segment accounted for the largest revenue of mobile casing & structural parts market share of 30.84% in 2024.

- Metal casings are widely used in premium smartphones and devices due to their durability, heat dissipation, and premium look.

- Increasing adoption of aluminum and magnesium alloys for lightweight and robust structural parts drives this segment's dominance.

- Advancements in metal finishing technologies, such as anodization, enhance aesthetic appeal and scratch resistance.

- Growing consumer preference for sleek and sturdy device designs supports the widespread use of metal casings.

The carbon fiber segment is anticipated to register the fastest CAGR during the forecast period.

- Carbon fiber casings offer superior strength-to-weight ratios, making them ideal for high-end smartphones and wearable devices.

- Increasing adoption of advanced consumer electronics due to their premium and futuristic appeal supports growth.

- Rising focus on reducing device weight without compromising structural integrity drives the use of carbon fiber materials.

- Expanding production capabilities and cost reductions in carbon fiber manufacturing enhance market potential.

By Product Type:

Based on product type, the market is segmented into back covers, front frames, mid frames, battery covers, and side frames.

The back covers segment accounted for the largest revenue share in 2024.

- Back covers serve as a critical component for device aesthetics and protection, making them highly demanded in both premium and mid-range devices.

- Increasing adoption of gradient designs and textured finishes in back covers enhances their visual appeal.

- Advancements in material customization, such as glass and ceramic back covers, drive mobile casing & structural parts market demand in the premium segment.

- The rising production of smartphones globally contributes significantly to the trends of back covers in the market.

The mid-frames segment is anticipated to register the fastest CAGR during the forecast period.

- Mid frames provide structural integrity and house critical internal components, making them essential for modern mobile devices.

- Increasing mobile casing & structural parts market opportunities for thin and lightweight device designs drive innovation in mid-frame materials and manufacturing.

- Adoption of precision machining and die-casting processes for mid-frames enhances their structural reliability.

- Expanding metal and composite materials in mid-frames for high-end devices supports rapid surge.

By Manufacturing Process:

Based on the manufacturing process, the market is segmented into injection molding, die casting, extrusion, machining, and 3D printing.

The injection molding segment accounted for the largest revenue of mobile casing & structural parts market share in 2024.

- Injection molding is widely used for producing plastic casings and components due to its cost efficiency and scalability.

- High adoption in mass production of affordable and mid-range smartphones supports this segment’s dominance.

- Technological advancements in multi-material and over-molding techniques enhance product quality and durability.

- Increasing mobile casing & structural parts market opportunities for customizable and complex designs in casings further boost injection molding applications.

The 3D printing segment is anticipated to register the fastest CAGR during the forecast period.

- 3D printing allows rapid prototyping and manufacturing of custom casings, making it ideal for limited-edition and concept devices.

- Rising adoption in research and development for innovative structural designs supports mobile casing & structural parts market growth in this segmental analysis.

- Expanding use in the production of lightweight and intricate parts for wearable devices and premium smartphones enhances trends.

- Advancements in 3D printing materials and processes for mass production further propel market adoption.

By By Application:

Based on application, the market is segmented into smartphones, tablets, wearable devices, and feature phones.

The smartphone segment accounted for the largest revenue share in 2024.

- Smartphones dominate in the market trends due to their widespread use and high annual production volumes globally.

- Increasing consumer demand for premium designs and durable casings drives material and process innovations in smartphone manufacturing.

- Advancements in foldable and modular smartphone designs enhance mobile casing & structural parts market growth in this segment.

- Growing competition among manufacturers to differentiate products through casing aesthetics and features supports this segment’s dominance.

The wearable devices segment is anticipated to register the fastest CAGR during the forecast period.

- Wearable devices, such as smartwatches and fitness trackers, require lightweight and compact casings, driving innovation in this segment.

- Increasing consumer adoption of wearables for health monitoring and connectivity boosts advancement for specialized structural parts.

- Rising focus on premium materials, such as carbon fiber and titanium, in high-end wearables supports growth.

- Expanding applications of wearables in fitness, healthcare, and fashion drive mobile casing & structural parts market demand for advanced casing and structural solutions.

By End-User:

Based on end-user, the market is segmented into consumer electronics manufacturers, OEMs (original equipment manufacturers), and aftermarket.

The OEM segment accounted for the largest revenue share in 2024.

- OEMs are the primary consumers of casings and structural parts, integrating them directly into devices during production.

- Increasing partnerships between OEMs and material suppliers for innovative casing designs enhance mobile casing & structural parts market trends.

- Rising production of smartphones, tablets, and wearables globally drives the trends for OEM-specific components.

- Focus on vertical integration by major OEMs to streamline supply chains and improve quality supports this segment’s dominance.

The aftermarket segment is anticipated to register the fastest CAGR during the forecast period.

- The aftermarket offers replacement and custom casing solutions, catering to consumers seeking device personalization and upgrades.

- Increasing trends for protective and aesthetically appealing casing options in the aftermarket drives growth.

- Expanding availability of aftermarket products for a wide range of devices, including older models, supports this segment.

- Rising consumer interest in unique and limited-edition casing designs fuels applications in the aftermarket.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

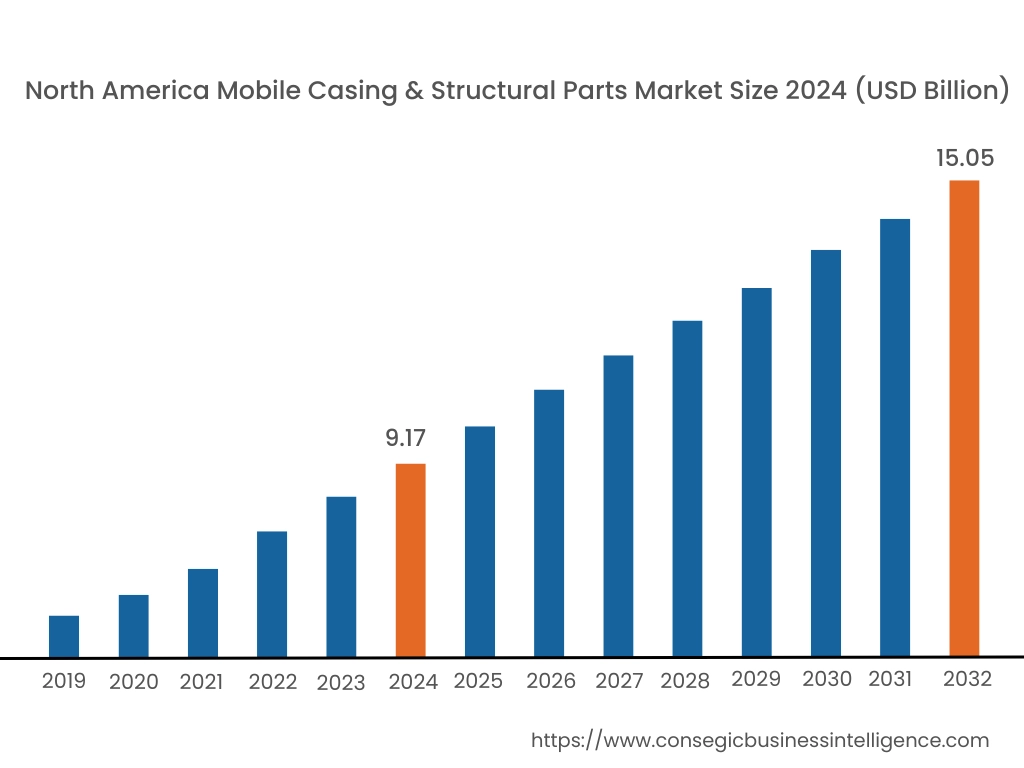

In 2024, North America was valued at USD 9.17 Billion and is expected to reach USD 15.05 Billion in 2032. In North America, the U.S. accounted for the highest share of 72.30% during the base year of 2024. North America holds a considerable share in the global mobile casing and structural parts market due to the increasing adoption of high-end smartphones and advancements in material technology. The U.S. leads the region, driven by a consistent rise in premium smartphones featuring durable and lightweight casings made of aluminum, titanium, and composite materials. Canada contributes with a growing inclination toward customized and protective casings, particularly in consumer and enterprise segments. The mobile casing & structural parts market analysis indicates that the market in North America benefits from strong investments in research and development to enhance durability and aesthetic appeal in mobile casings.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 7.1% over the forecast period. The mobile casing and structural parts market is fueled by the rapid expansion of smartphone manufacturing and rising disposable incomes in China, India, and South Korea. China dominates the region with a massive production base for smartphones and components, leveraging cost-effective manufacturing and advancements in material science. India’s growing smartphone penetration supports the trends for affordable and durable casings, especially in the mid-range and budget segments. South Korea emphasizes innovative casings with advanced functionalities, supported by its leading smartphone brands. Analysis highlights the increasing use of composite materials to enhance durability while maintaining affordability in this region.

Europe is a prominent market for mobile casing and structural parts, supported by a strong demand for eco-friendly and recyclable materials in smartphone manufacturing. Countries like Germany, the UK, and France are key contributors. Germany focuses on advanced material engineering to produce lightweight yet robust structural parts for premium smartphone brands. The UK emphasizes sustainable casing materials, aligning with its regulations on reducing environmental waste. France witnesses a rapid surge for stylish and premium casings in both luxury and mid-range smartphones. The mobile casing & structural parts market analysis of the region suggests that regulatory frameworks encouraging sustainability are driving innovation in material selection.

The Middle East & Africa region is witnessing steady growth in the mobile casing and structural parts market, driven by rising smartphone penetration and increasing appeals for durable products. Countries like Saudi Arabia and the UAE are adopting high-quality, premium smartphone casings due to rising consumer spending on luxury electronics. In Africa, South Africa is emerging as a key market, focusing on durable and affordable casings for budget-friendly smartphones. Regional analysis points out that limited local manufacturing capabilities often lead to reliance on imports, impacting availability and pricing in some areas.

Latin America is an emerging market for mobile casing and structural parts, with Brazil and Mexico leading the region. Brazil’s expanding smartphone user base and growing production of mid-range and budget smartphones drive trends for cost-effective casings. Mexico benefits from its proximity to North American manufacturers, contributing to the regional supply chain for smartphone structural components. The analysis highlights the increasing preference for lightweight and durable materials to improve smartphone usability and portability. However, economic fluctuations in some countries may pose challenges to consistent mobile casing & structural parts market expansion.

Top Key Players and Market Share Insights:

The mobile casing & structural parts market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global mobile casing & structural parts market. Key players in the mobile casing & structural parts industry include -

- Foxconn Technology Group (Taiwan)

- Catcher Technology Co., Ltd. (Taiwan)

- BYD Electronics (International) Co., Ltd. (China)

- Lite-On Technology Corporation (Taiwan)

- AAC Technologies Holdings Inc. (China)

- Jabil Inc. (United States)

- Samsung Electronics Co., Ltd. (South Korea)

- Nolato AB (Sweden)

- Lens Technology Co., Ltd. (China)

- Tongda Group Holdings Limited (China)

Recent Industry Developments :

Innovations:

- In May 2024, HUD's report on factory-built homes highlighted advanced manufacturing techniques using lightweight, durable materials. These innovations align with trends in the mobile casing and structural parts market, where similar techniques enhance durability and reduce costs.

- In 2024, Bole Intelligent Machinery Co., Ltd. introduced an advanced injection molding machine specifically designed for mobile phone covers. This machine features a central locking toggle mechanism, ensuring uniform clamping force distribution, which enhances product precision and reduces material waste. Additionally, the design minimizes the risk of flash, thereby decreasing the need for post-production trimming. These innovations aim to improve production efficiency and product quality in the mobile casing and structural parts market.

Mobile Casing & Structural Parts Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 46.45 Billion |

| CAGR (2025-2032) | 6.7% |

| By Material Type |

|

| By Product Type |

|

| By Manufacturing Process |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Mobile Casing & Structural Parts Market by 2032? +

The Mobile Casing & Structural Parts Market size is estimated to reach over USD 46.45 Billion by 2032 from a value of USD 27.65 Billion in 2024 and is projected to grow by USD 29.01 Billion in 2025, growing at a CAGR of 6.7% from 2025 to 2032.

What are the major materials used in mobile casings and structural parts? +

Key materials include Metal, Plastic, Glass, Carbon Fiber, and others. The Metal segment holds the largest revenue share due to its durability and premium aesthetics, while Carbon Fiber is projected to grow fastest due to its strength-to-weight ratio.

Which product type dominates the market? +

Back Covers dominate the market owing to their significant role in aesthetics and protection. Mid Frames are expected to grow at the fastest CAGR due to their critical function in structural integrity and innovation in materials.

What manufacturing processes are commonly used? +

The leading manufacturing processes include Injection Molding, Die Casting, Extrusion, Machining, and 3D Printing. Injection Molding accounts for the largest share due to its cost-efficiency, while 3D Printing is growing rapidly due to its use in prototyping and customized production.