- Summary

- Table Of Content

- Methodology

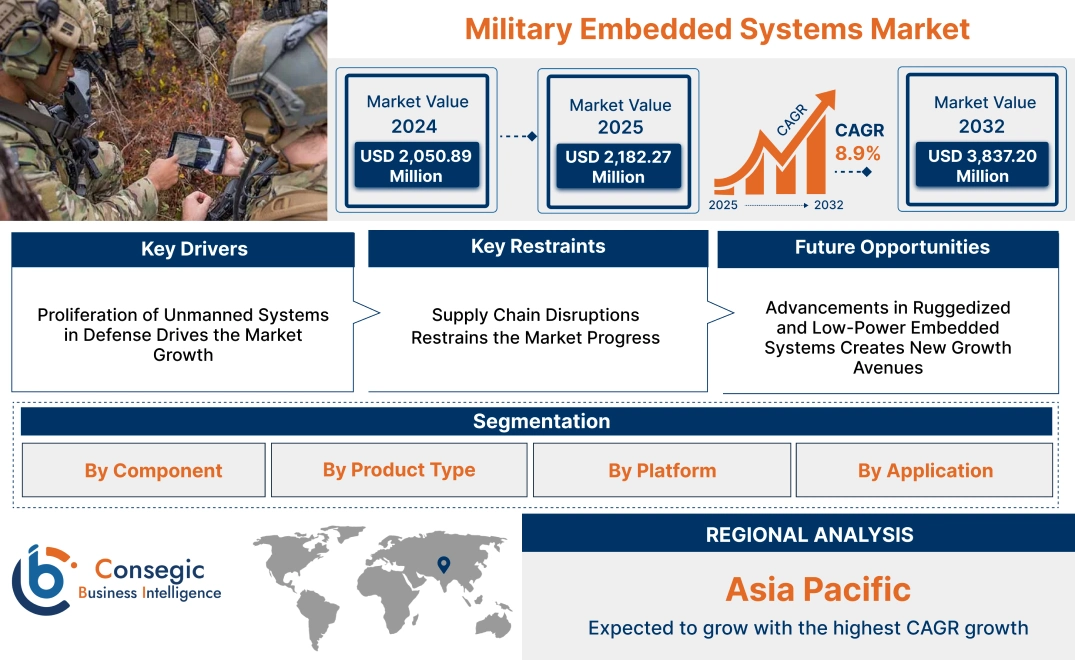

Military Embedded Systems Market Size:

Military Embedded Systems Market size is estimated to reach over USD 3,837.20 Million by 2032 from a value of USD 2,050.89 Million in 2024 and is projected to grow by USD 2,182.27 Million in 2025, growing at a CAGR of 8.9% from 2025 to 2032.

Military Embedded Systems Market Scope & Overview:

Military embedded systems are specialized computing platforms integrated into military equipment to perform critical functions such as data processing, communication, and control. These systems are designed for use in demanding environments, ensuring reliability and efficiency in applications such as surveillance, navigation, weapon control, and electronic warfare. They provide real-time performance and are tailored to meet the unique requirements of military operations.

These systems are equipped with advanced processors, sensors, and software to deliver high-performance computing capabilities. They are engineered to withstand harsh conditions, including extreme temperatures, vibration, and electromagnetic interference, ensuring consistent operation in field environments. Military embedded systems are adaptable to a variety of platforms, including aircraft, naval vessels, ground vehicles, and unmanned systems.

End-users include defense organizations, military contractors, and government agencies focused on enhancing operational efficiency and mission effectiveness. These systems play a critical role in modernizing defense infrastructure and enabling seamless integration of advanced technologies in military operations.

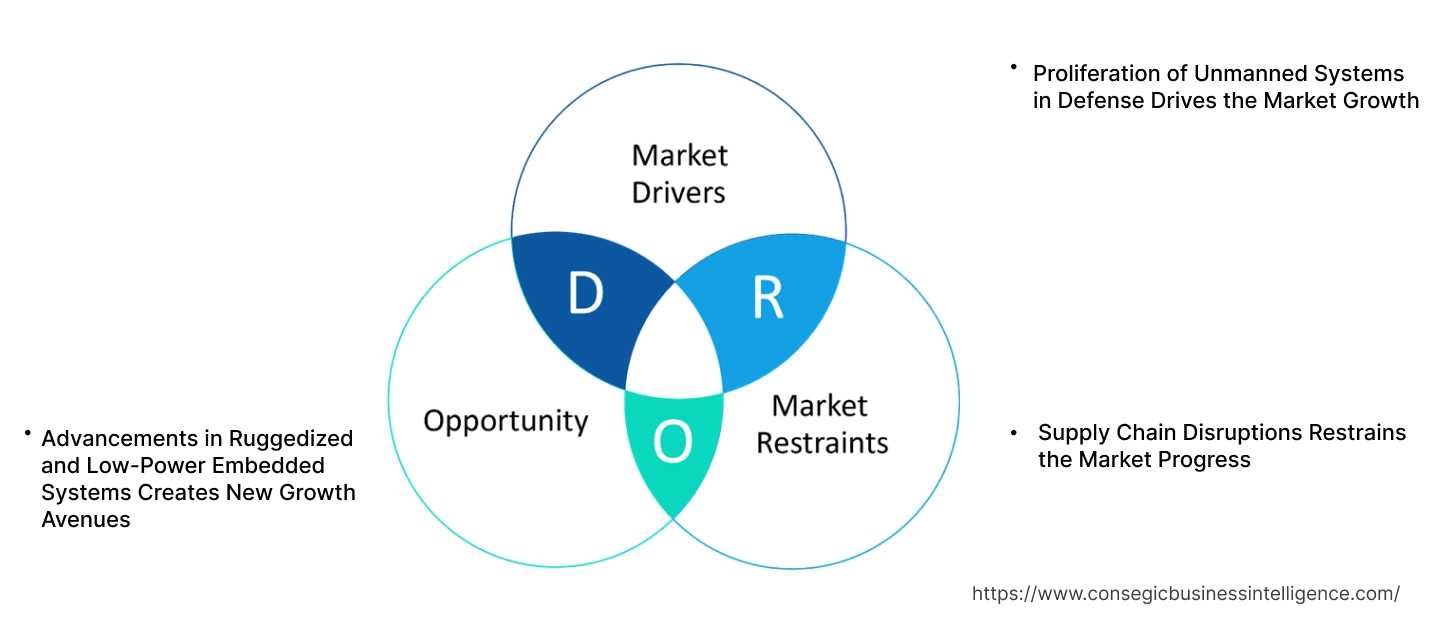

Military Embedded Systems Market Dynamics - (DRO) :

Key Drivers:

Proliferation of Unmanned Systems in Defense Drives the Market Growth

The increasing deployment of unmanned systems, including UAVs, unmanned ground vehicles (UGVs), and autonomous maritime systems, is significantly boosting the demand for advanced embedded systems. These systems are essential for enabling key functionalities such as autonomous navigation, real-time data analysis, and target acquisition, which are critical for modern warfare operations. In UAVs, embedded systems process vast amounts of sensor data, facilitate communication with command centers, and ensure precise mission execution, even in GPS-denied environments. For UGVs and maritime systems, embedded solutions enhance operational efficiency through capabilities like obstacle detection, route optimization, and environmental adaptation. The need for compact, rugged, and energy-efficient embedded systems is rising, as these platforms must operate in extreme conditions with minimal power consumption. As military strategies increasingly rely on unmanned systems for reconnaissance, surveillance, and combat operations, the role of embedded technologies becomes indispensable for mission success, further fueling the military embedded systems market growth.

Key Restraints:

Supply Chain Disruptions Restrains the Market Progress

Supply chain disruptions have become a significant issue for military embedded system manufacturers, driven by geopolitical tensions and dependence on critical semiconductor components. The global semiconductor shortage, exacerbated by trade restrictions and regional conflicts, has created bottlenecks in the production and delivery of key components required for embedded systems. This issue is further intensified by the complex and highly specialized nature of the defense industry supply chain, where sourcing reliable, high-quality components is paramount. Delays in procuring semiconductors and other essential parts result in extended production timelines, increased operational costs, and reduced responsiveness to defense procurement needs. Additionally, the reliance on specific regions for component manufacturing creates vulnerabilities, making the supply chain susceptible to disruptions from natural disasters, economic sanctions, or political instability. Thus, the aforementioned factors hinder the military embedded systems market demand.

Future Opportunities :

Advancements in Ruggedized and Low-Power Embedded Systems Creates New Growth Avenues

Advancements in ruggedized and low-power embedded systems are driving their adoption in portable military equipment, enhancing both mobility and operational efficiency. These systems are designed to withstand extreme environmental conditions, such as high temperatures, shock, vibration, and electromagnetic interference, making them ideal for use in harsh battlefield environments. Innovations in low-power technologies ensure extended operational capabilities for portable devices like handheld communication tools, wearable systems, and field radars without frequent recharging, a critical advantage in remote or high-intensity operations. Additionally, compact designs allow for integration into lightweight and portable devices, enabling soldiers to carry advanced technology without compromising mobility. Enhanced computational power and real-time data processing capabilities within these embedded systems support mission-critical tasks such as secure communication, surveillance, and target acquisition. These advancements are transforming modern military operations, allowing for greater situational awareness and seamless coordination in demanding operational scenarios. Thus, the above mentioned factors are creating new military embedded systems market opportunities

Military Embedded Systems Market Segmental Analysis :

By Component:

Based on component, the market is segmented into hardware and software.

The hardware segment accounted for the largest revenue of the total military embedded systems market share in 2024.

- Advanced processors and memory modules enable high-speed data processing and storage, essential for military operations.

- Power supplies and networking devices ensure seamless operation and communication between military systems.

- Sensors integrated into embedded systems support real-time monitoring and enhance mission-critical decision-making capabilities.

- As per the market trends, the dominance of this segment reflects its pivotal role in the development and deployment of cutting-edge military technologies, driving the military embedded systems market expansion.

The software segment is expected to register the fastest CAGR during the forecast period.

- Operating systems in embedded systems offer robust control over hardware components, ensuring high reliability and precision.

- Middleware solutions facilitate seamless integration of multiple military subsystems, improving operational efficiency.

- The growing focus on cybersecurity has led to increased adoption of advanced software solutions for data protection in military applications.

- As per the military embedded systems market analysis, increasing reliance on software-driven embedded systems across military platforms is driving the rapid extension of this segment.

By Product Type:

Based on product type, the market is segmented into advanced telecom computing architecture (TCA), compact-PCI (CPCI) boards, compact-PCI (CPCI) serial, VME BUS, OPEN VPX, and motherboard.

The advanced telecom computing architecture (TCA) segment held the largest revenue of the total military embedded systems market share in 2024.

- TCA platforms provide high performance and scalability, making them ideal for complex military applications.

- These systems are widely adopted for communication and command applications due to their modularity and durability.

- The ability to handle large volumes of data in real time further enhances the utility of TCA platforms in military environments.

- As per the military embedded systems market trends, the growing deployment of TCA platforms in modernizing military infrastructure supports its market dominance.

The OPEN VPX segment is projected to grow at the fastest CAGR during the forecast period.

- OPEN VPX systems offer flexibility and interoperability, addressing the diverse requirements of military systems.

- These systems are increasingly adopted for mission-critical operations due to their enhanced performance and rugged design.

- Rising investments in advanced embedded systems for defense applications are driving the adoption of OPEN VPX technology.

- The segment’s growth is supported by continuous innovation and standardization initiatives in embedded system platforms, fueling the military embedded systems market opportunities.

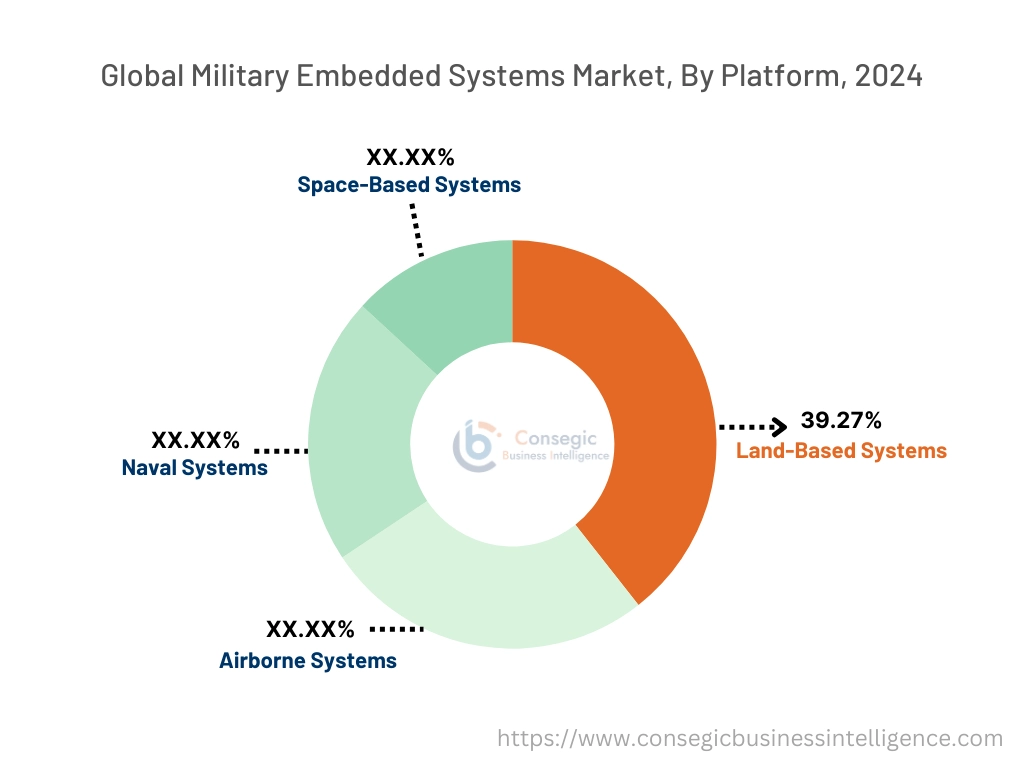

By Platform:

Based on platform, the market is segmented into land-based systems, airborne systems, naval systems, and space-based systems.

The land-based systems segment accounted for the largest revenue of 39.27% share in 2024.

- Land-based platforms rely on embedded systems for real-time situational awareness and decision-making.

- These systems enhance the efficiency and effectiveness of military operations, including surveillance, reconnaissance, and logistics.

- High demand for land-based embedded systems is driven by modernization programs in defense forces worldwide.

- The analysis of segmental trends depict that the dominance of this segment highlights the critical role of embedded systems in ground-based military applications, which further facilitates the military embedded systems market growth.

The space-based systems segment is expected to register the fastest CAGR during the forecast period.

- Embedded systems in space-based platforms support navigation, communication, and surveillance operations.

- Increasing investments in satellite-based defense infrastructure are driving the demand for space-based embedded systems.

- Technological advancements in miniaturized and high-performance components are boosting adoption in this segment.

- The segment’s growth is fueled by the rising focus on space-based military capabilities for strategic advantages, boosting the military embedded systems market demand.

By Application:

Based on application, the military embedded systems market is segmented into command & control systems, intelligence, surveillance & reconnaissance (ISR), electronic warfare, communication systems, and others.

The intelligence, surveillance & reconnaissance (ISR) segment held the largest revenue share in 2024.

- ISR systems rely on embedded systems for processing and analyzing data from multiple sources in real time.

- These systems enhance decision-making by providing actionable intelligence during missions.

- High adoption of ISR embedded systems in defense operations highlights their importance in modern warfare.

- The segment’s dominance reflects the critical role of embedded systems in achieving superior situational awareness, contributing to the military embedded systems market expansion.

The electronic warfare segment is projected to grow at the fastest CAGR during the forecast period.

- Embedded systems in electronic warfare applications enable efficient detection and countermeasures against threats.

- Increasing investments in advanced warfare technologies drive the adoption of embedded systems for electronic warfare.

- The ability to disrupt adversary communications and radar systems enhances the strategic importance of this segment.

- As per the military embedded systems market analysis, the segment’s growth is supported by the continuous evolution of electronic warfare tactics and technologies.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

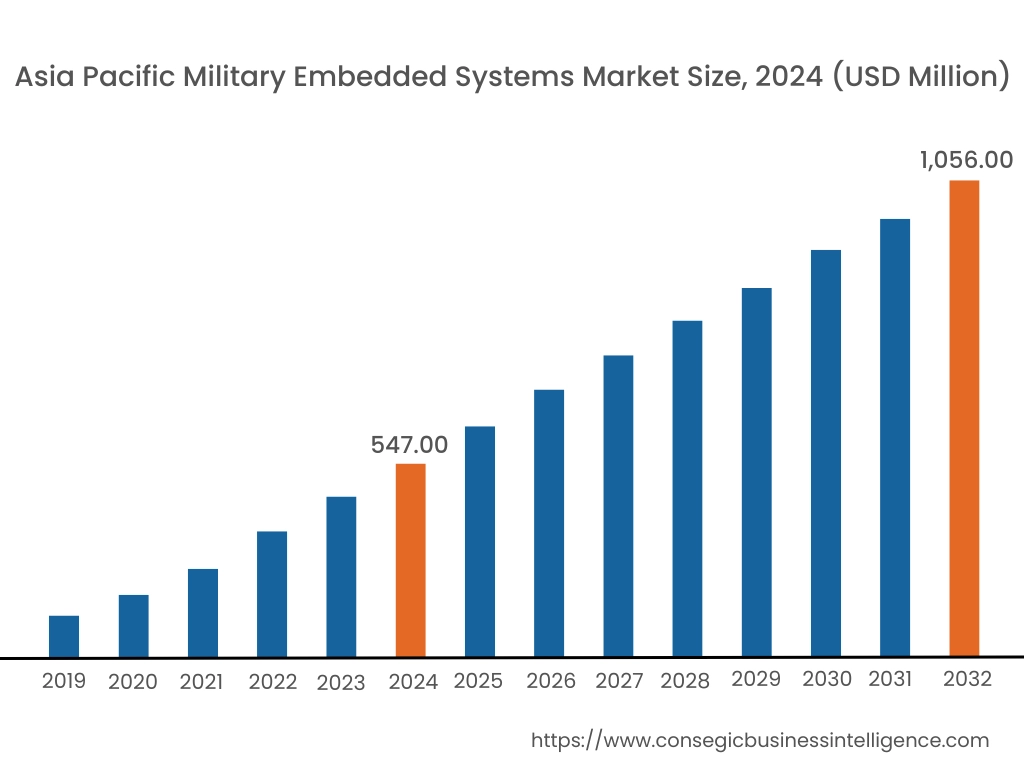

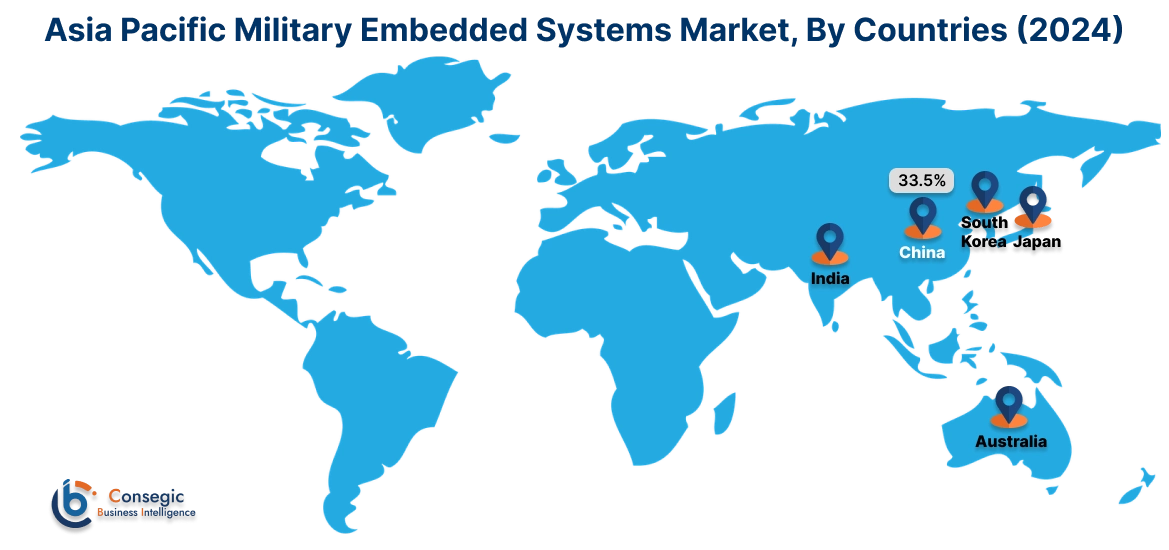

Asia Pacific region was valued at USD 547.00 Million in 2024. Moreover, it is projected to grow by USD 583.58 Million in 2025 and reach over USD 1,056.00 Million by 2032. Out of this, China accounted for the maximum revenue share of 33.5%. The Asia-Pacific region is witnessing a surge in requirement for military embedded systems, propelled by increasing defense expenditures and the induction of advanced military platforms. Countries such as China, India, and Japan are focusing on integrating embedded systems to enhance their defense capabilities. A prominent trend is the development of indigenous technologies to reduce reliance on foreign suppliers. Analysis suggests that regional security dynamics and technological advancements are key factors influencing the market in this area.

North America is estimated to reach over USD 1,228.67 Million by 2032 from a value of USD 661.52 Million in 2024 and is projected to grow by USD 703.47 Million in 2025. This region holds a substantial share of the military embedded systems market, driven by the United States' emphasis on enhancing defense capabilities through advanced technologies. The integration of sophisticated embedded systems into military platforms is a notable trend, aiming to provide real-time data processing and improved operational efficiency. Analysis indicates that ongoing investments in research and development, coupled with modernization programs, are pivotal in shaping the market landscape in North America.

European nations, including the United Kingdom, France, and Germany, are actively investing in military embedded systems to bolster their defense industry. A significant trend is the collaboration among European defense manufacturers to develop sophisticated embedded solutions tailored for various military applications.

In the Middle East, nations are prioritizing the enhancement of their military capabilities, leading to investments in advanced embedded systems. The focus is on equipping existing and new military platforms with state-of-the-art technologies to mitigate risks during operations. As per the military embedded systems market trends, political instability and economic diversification efforts in certain areas may impact market dynamics. In Africa, the market is gradually evolving, with a focus on addressing challenges related to defense modernization. Analysis indicates that international collaborations and capacity-building initiatives are playing a crucial role in enhancing military capabilities across the continent.

Latin American countries are increasingly recognizing the importance of military embedded systems in ensuring the effectiveness of their defense forces. Nations such as Brazil and Mexico are investing in embedded technologies to modernize their military capabilities. A notable trend is the emphasis on procuring cost-effective solutions that offer reliable performance.

Top Key Players and Market Share Insights:

The Military Embedded Systems market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Military Embedded Systems market. Key players in the Military Embedded Systems industry include -

- Curtiss-Wright Corporation (USA)

- Mercury Systems (USA)

- SMART Embedded Computing (USA)

- Thales Group (France)

- NXP Semiconductors (Netherlands)

- Kontron (S&T AG) (Austria)

- AMETEK (USA)

- General Dynamics Corporation (USA)

- BAE Systems (UK)

- Advantech Co., Ltd. (Taiwan)

Recent Industry Developments :

Partnerships & Collaborations:

- In October 2024, SAIC and Wind River expanded their partnership to accelerate the development of mission-critical systems for U.S. government entities, including the Army. The collaboration leverages Wind River's software portfolio, such as digital twin and DevSecOps, to modernize Army systems. Together, they aim to enhance lifecycle engineering, improve system integration, and drive AI-driven intelligent edge applications. This partnership supports Army modernization goals and advances secure, reliable mission-critical technologies across defense and civilian sectors.

Product Launches:

- In August 2024, United Electronic Industries (UEI) unveiled the DNR-MIL-4, a compact, military-grade I/O system designed for aerospace and defense application Built for durability under extreme conditions, it meets MIL-STD standards and supports versatile processors like PowerPC and Zynq UltraScale+. The system features dual Gigabit Ethernet, up to 200 I/O channels, and compatibility with over 90 boards, enabling precision in tasks like HUMS and jet engine testing. Its adaptability ensures reliable performance in harsh environments, reinforcing UEI's commitment to high-quality, mission-critical solutions.

- In June 2024, Kontron unveiled the VX6096, a 6U VPX computing board powered by Intel® Xeon® D2700/2800 processors. Designed for military radar and imaging applications, it features up to 128 GB DDR4 ECC memory, 100Gb Ethernet, and GPU expansion. It aligns with SOSA™ standards, offers advanced cooling, and supports operation in extreme temperatures. Security includes TPM2 and a secure PLD, enhancing PFR compliance. Available in multiple configurations, it ensures robust performance for compute-intensive, latency-sensitive environments.

- In April 2024, Curtiss-Wright introduced the V3-1222, the first safety-certifiable VPX single board computer featuring Intel’s 13th Gen Core™ processors. Designed for avionics, the 3U VPX board aligns with SOSA™ standards, supports DO-254 DAL A compliance, and offers robust performance with 64 GB DDR5 memory, PCIe connectivity, and Intel® Iris® Xe graphics. It provides COTS data artifacts for faster safety certification and reduced costs. Ideal for applications like flight control and mission systems, it combines high processing power with reliability and security features for critical avionics requirements.

Military Embedded Systems Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 3,837.20 Million |

| CAGR (2025-2032) | 8.9% |

| By Component |

|

| By Product Type |

|

| By Platform |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Military Embedded Systems Market? +

The Military Embedded Systems Market size is estimated to reach over USD 3,837.20 Million by 2032 from a value of USD 2,050.89 Million in 2024 and is projected to grow by USD 2,182.27 Million in 2025, growing at a CAGR of 8.9% from 2025 to 2032.

What are the key segments in the Military Embedded Systems Market? +

The market is segmented by component (hardware and software), product type (Advanced Telecom Computing Architecture, Compact-PCI, OPEN VPX, VME BUS, etc.), platform (land-based systems, airborne systems, naval systems, space-based systems), and application (Command & Control Systems, ISR, Electronic Warfare, Communication Systems, etc.).

Which segment is expected to grow the fastest in the Military Embedded Systems Market? +

The electronic warfare segment is expected to grow at the fastest CAGR during the forecast period, driven by increasing investments in advanced warfare technologies and the growing need for efficient detection and countermeasures against threats.

Who are the major players in the Military Embedded Systems Market? +

Key players in the Military Embedded Systems market include Curtiss-Wright Corporation (USA), Mercury Systems (USA), Kontron (S&T AG) (Austria), AMETEK (USA), General Dynamics Corporation (USA), BAE Systems (UK), Advantech Co., Ltd. (Taiwan), SMART Embedded Computing (USA), Thales Group (France), and NXP Semiconductors (Netherlands).