- Summary

- Table Of Content

- Methodology

Military Aircraft Avionics Market Size:

Military Aircraft Avionics Market size is estimated to reach over USD 48,434.00 Million by 2032 from a value of USD 36,937.01 Million in 2024 and is projected to grow by USD 37,567.16 Million in 2025, growing at a CAGR of 3.6% from 2025 to 2032.

Military Aircraft Avionics Market Scope & Overview:

Military aircraft avionics refers to the electronic systems used in military aircraft to enhance operational capabilities, safety, and mission effectiveness. These systems include navigation, communication, surveillance, flight control, and mission management technologies, enabling seamless coordination and precision during complex military operations. Avionics play a critical role in ensuring the reliability and functionality of aircraft in diverse combat and support scenarios.

These systems are integrated with advanced sensors, displays, and control modules, offering real-time data processing and situational awareness. Military avionics are designed to withstand extreme operational conditions, providing robust performance in adverse environments. They are adaptable to various types of aircraft, including fighter jets, transport planes, and unmanned aerial systems (UAS).

End-users include air forces and defense organizations seeking state-of-the-art solutions to enhance the efficiency and safety of military aircraft. These systems are essential for modernizing aviation capabilities and supporting diverse military missions.

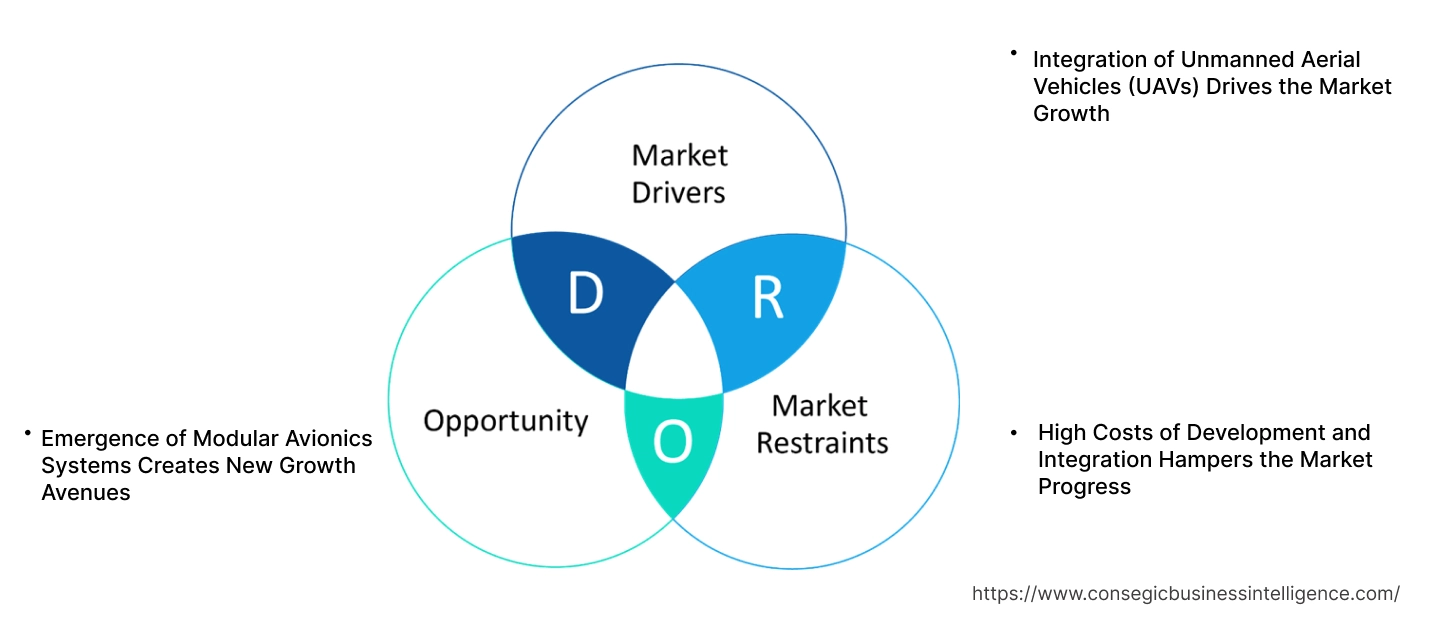

Military Aircraft Avionics Market Dynamics - (DRO) :

Key Drivers:

Integration of Unmanned Aerial Vehicles (UAVs) Drives the Market Growth

The increasing deployment of unmanned aerial vehicles (UAVs) in military operations is driving the demand for advanced avionics systems. These systems play a crucial role in enabling UAVs to navigate complex environments, maintain secure communication links, and execute mission-critical tasks with precision. Military UAVs often undertake high-stakes operations such as intelligence gathering, surveillance, reconnaissance, and target acquisition, requiring reliable avionics to ensure operational success. Features like automated flight control, real-time data processing, and obstacle avoidance enhance UAV efficiency and adaptability in challenging scenarios. Additionally, as UAV usage expands to include combat missions and logistics, the need for robust avionics capable of handling diverse applications is further accelerating. The integration of cutting-edge avionics technologies in UAVs ensures optimal performance, mission accuracy, and seamless coordination with broader defense networks, making them indispensable in modern warfare strategies. Thus, the aforementioned factors are driving the military aircraft avionics market growth.

Key Restraints:

High Costs of Development and Integration Hampers the Market Progress

The development and integration of advanced avionics systems require substantial investment, encompassing research and development, certification processes, and installation expenses. These costs are particularly burdensome for nations with smaller defense budgets, creating a significant financial barrier to adoption. The high cost not only impacts procurement but also influences the decision-making process for upgrading existing systems or acquiring new technologies. Furthermore, the stringent certification requirements and specialized workforce needed for seamless integration amplify the financial burden. This restraint disproportionately affects emerging economies and smaller defense forces, restricting their ability to modernize military fleets and adopt state-of-the-art avionics technologies. Consequently, the high costs of development and integration are a key factor limiting the military aircraft avionics market demand.

Future Opportunities :

Emergence of Modular Avionics Systems Creates New Growth Avenues

The transition to modular avionics systems is transforming military aircraft operations by offering flexibility and cost efficiency. Unlike traditional avionics setups, modular architectures allow components to be easily upgraded or replaced without overhauling the entire system. This adaptability enables military forces to customize avionics configurations to meet specific mission requirements, such as surveillance, combat, or logistics. Modular systems also simplify maintenance by isolating and addressing individual component issues, reducing downtime and operational expenses. Additionally, the ability to integrate emerging technologies, such as advanced sensors and AI-driven systems, enhances the long-term utility of military aircraft. With the growth in need for mission-specific adaptability and cost-effective modernization, modular avionics systems are becoming a key focus in the defense industry, providing military aircraft avionics market opportunities for manufacturers to deliver tailored and future-ready solutions.

Military Aircraft Avionics Market Segmental Analysis :

By System Type:

Based on system type, the market is segmented into flight management systems, navigation systems, communication systems, mission systems, and monitoring & control systems.

The flight management systems segment accounted for the largest revenue of the total military aircraft avionics market share in 2024.

- Flight management systems are critical for optimizing fuel efficiency, navigation, and route management, enhancing mission success rates.

- These systems ensure seamless coordination of onboard avionics components, improving operational reliability and reducing manual intervention.

- Their integration with cutting-edge GPS and automated navigation tools supports their widespread adoption across fixed-wing and rotary-wing platforms.

- The analysis of segmental trends shows that the dominance of this segment reflects the emphasis on real-time decision-making and efficiency in military operations, contributing to the military aircraft avionics market expansion.

The mission systems segment is projected to grow at the fastest CAGR during the forecast period.

- Mission systems offer advanced situational awareness, enabling efficient execution of combat and surveillance operations.

- Their ability to integrate multiple data sources, such as radar and communication systems, drives their adoption in complex missions.

- Increased focus on electronic warfare and network-centric operations further bolsters the demand for mission systems.

- As per the military aircraft avionics market analysis, the segment’s rapid growth is fueled by technological advancements in AI and data analytics for mission planning and execution.

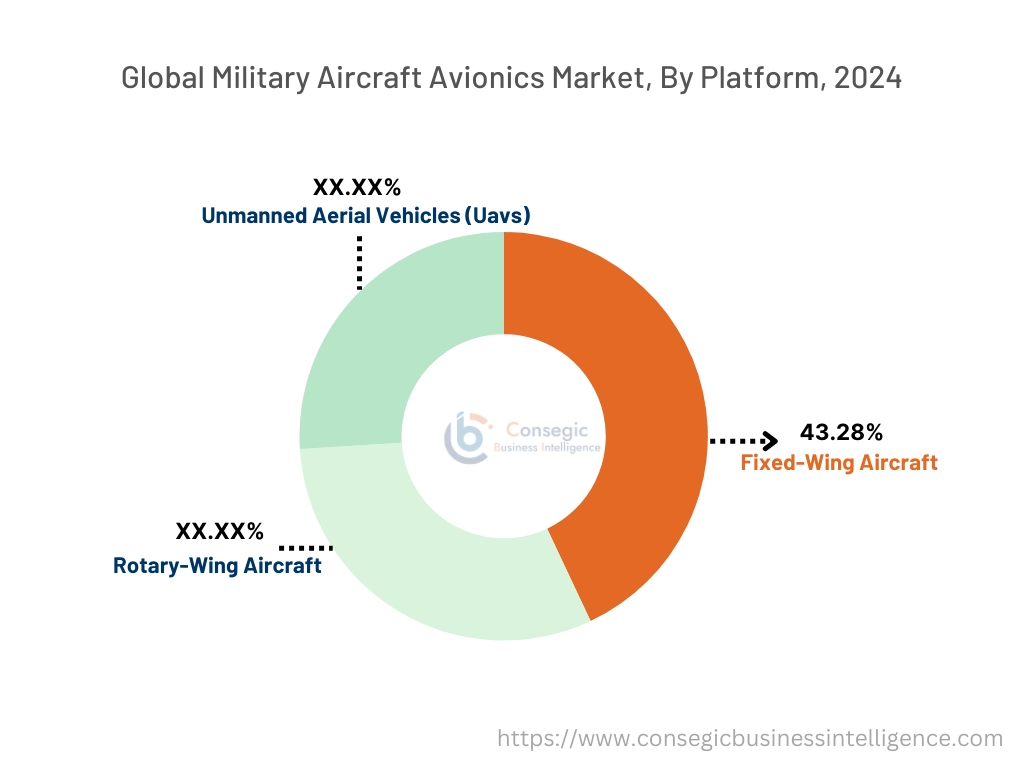

By Platform:

Based on platform, the market is segmented into fixed-wing aircraft, rotary-wing aircraft, and unmanned aerial vehicles (UAVs).

The fixed-wing aircraft segment held the largest revenue of 43.28% of the total military aircraft avionics market share in 2024.

- Fixed-wing aircraft are widely used for combat, surveillance, and transport operations, driving consistent demand for advanced avionics.

- These platforms rely heavily on navigation, communication, and flight management systems for mission-critical operations.

- Their extensive deployment in multi-role scenarios, including reconnaissance and strike missions, underscores their market dominance.

- As per the military aircraft avionics market trends, enhanced payload capacity and long operational ranges further solidify their significance in defense industry applications.

The UAV segment is expected to register the fastest CAGR during the forecast period.

- UAVs are increasingly adopted for intelligence, surveillance, and reconnaissance (ISR) missions due to their cost-effectiveness and operational versatility.

- Their reliance on advanced avionics systems, including autonomous navigation and sensor integration, supports their rapid market expansion.

- Advancements in drone technologies, such as AI-driven decision-making and real-time data transmission, further bolster their adoption.

- Thus, as per segmental trends analysis, governments and defense agencies worldwide are investing in UAV programs, driving demand for cutting-edge avionics systems tailored to UAV requirements, further fuels the military aircraft avionics market growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

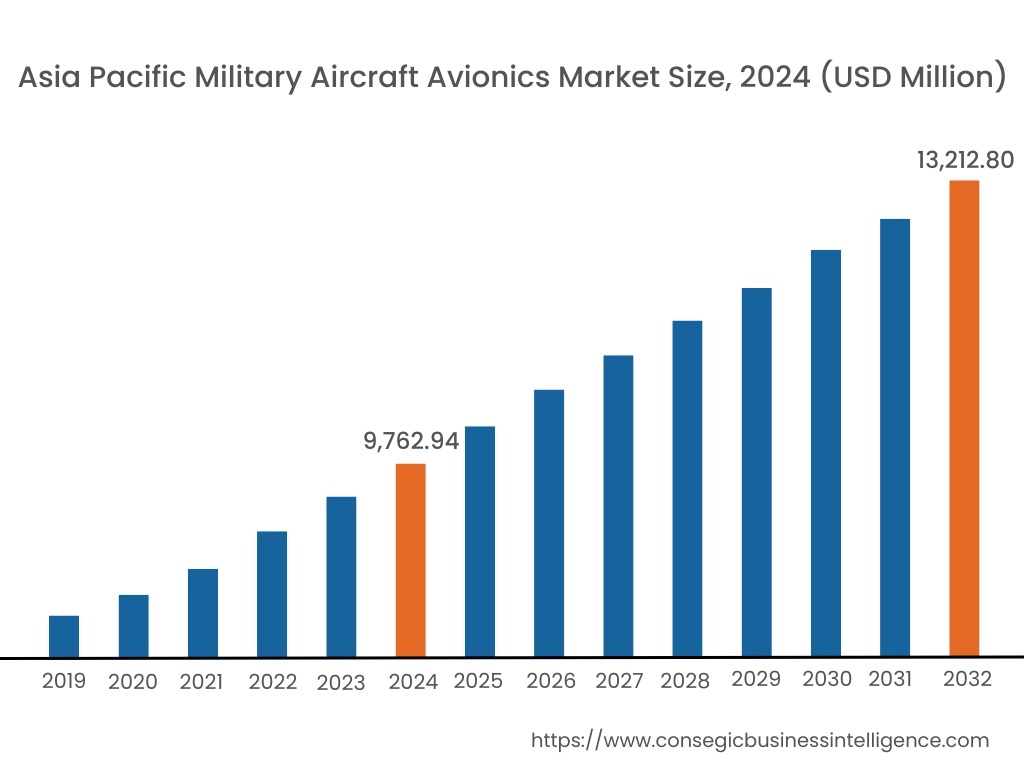

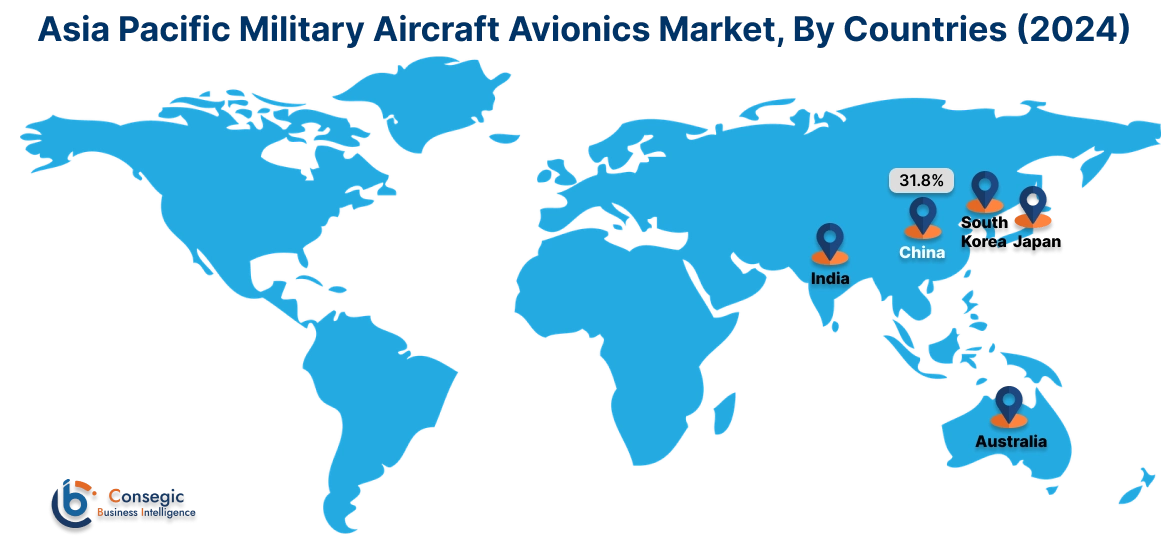

Asia Pacific region was valued at USD 9,762.94 Million in 2024. Moreover, it is projected to grow by USD 9,956.06 Million in 2025 and reach over USD 13,212.80 Million by 2032. Out of this, China accounted for the maximum revenue share of 31.8%. The Asia-Pacific region is witnessing growth in demand for military aircraft avionics, propelled by increasing defense expenditures and the induction of advanced military aircraft. Countries such as China, India, and Japan are focusing on integrating avionics systems to enhance their defense capabilities. A prominent trend is the development of indigenous avionics technologies to reduce reliance on foreign suppliers. Analysis suggests that regional security dynamics and technological advancements are key factors influencing the military aircraft avionics market expansion in this area.

North America is estimated to reach over USD 15,392.33 Million by 2032 from a value of USD 11,825.49 Million in 2024 and is projected to grow by USD 12,019.86 Million in 2025. This region holds a substantial share of the military aircraft avionics market, driven by the United States' emphasis on enhancing defense capabilities through advanced technologies. The integration of sophisticated avionics systems into military aircraft is a notable trend, aiming to provide precise targeting and improved operational efficiency. Analysis indicates that ongoing investments in research and development, coupled with modernization programs, are pivotal in shaping the military aircraft avionics market demand in North America.

European nations, including the United Kingdom, France, and Germany, are actively investing in military aircraft avionics to bolster their defense systems. A significant trend is the collaboration among European defense manufacturers to develop sophisticated avionics solutions tailored for various military applications, creating new military aircraft avionics market opportunities.

In the Middle East, nations are prioritizing the enhancement of their military capabilities, leading to investments in advanced avionics systems. The focus is on equipping existing and new military aircraft with state-of-the-art avionics to mitigate risks during operations. However, political instability and economic diversification efforts in certain areas may impact market dynamics. In Africa, the market is gradually evolving, with a focus on addressing challenges related to defense modernization. The military aircraft avionics market analysis indicates that international collaborations and capacity-building initiatives are playing a crucial role in enhancing military capabilities across the continent.

Latin American countries are increasingly recognizing the importance of military aircraft avionics in ensuring the effectiveness of their defense forces. As per the military aircraft avionics market trends, nations such as Brazil and Mexico are investing in avionics technologies to modernize their military aviation capabilities. A notable trend is the emphasis on procuring cost-effective solutions that offer reliable performance.

Top Key Players and Market Share Insights:

The military aircraft avionics market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global military aircraft avionics market. Key players in the military aircraft avionics industry include –

- Honeywell International Inc. (USA)

- Thales Group (France)

- Rockwell Collins (Collins Aerospace) (USA)

- Saab AB (Sweden)

- Leonardo S.p.A. (Italy)

- Raytheon Technologies Corporation (USA)

- BAE Systems (UK)

- General Dynamics Corporation (USA)

- Northrop Grumman Corporation (USA)

- Lockheed Martin Corporation (USA)

Recent Industry Developments :

Partnerships & Collaborations:

- In October 2024, Honeywell and Merlin signed an MOU to integrate Merlin Pilot, an autonomous flight system, with Honeywell Anthem avionics to reduce pilot workloads and enhance efficiency. Initially targeting military fixed-wing aircraft, the partnership aims to retrofit existing fleets for single-pilot and eventual uncrewed operations. This collaboration addresses pilot shortages, improves safety, and enhances scalability for military and commercial aviation. Honeywell and Merlin plan to advance autonomy with a focus on efficiency and safety in aviation operations.

Military Aircraft Avionics Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 48,434.00 Million |

| CAGR (2025-2032) | 3.6% |

| By System Type |

|

| By Platform |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Military Aircraft Avionics Market? +

The Military Aircraft Avionics Market size is estimated to reach over USD 48,434.00 Million by 2032 from a value of USD 36,937.01 Million in 2024 and is projected to grow by USD 37,567.16 Million in 2025, growing at a CAGR of 3.6% from 2025 to 2032.

What are the key segments in the Military Aircraft Avionics Market? +

The market is segmented by system type (Flight Management Systems, Navigation Systems, Communication Systems, Mission Systems, Monitoring & Control Systems), platform (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Unmanned Aerial Vehicles (UAVs)), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which segment is expected to grow the fastest in the Military Aircraft Avionics Market? +

The Mission Systems segment is projected to grow at the fastest CAGR due to increasing demand for advanced situational awareness and electronic warfare capabilities, driving the need for integrated avionics in combat and surveillance operations.

Who are the major players in the Military Aircraft Avionics Market? +

Key players in the Military Aircraft Avionics market include Honeywell International Inc. (USA), Thales Group (France), Raytheon Technologies Corporation (USA), BAE Systems (UK), General Dynamics Corporation (USA), Northrop Grumman Corporation (USA), Lockheed Martin Corporation (USA), Rockwell Collins (Collins Aerospace) (USA), Saab AB (Sweden), and Leonardo S.p.A. (Italy).