- Summary

- Table Of Content

- Methodology

Military Airborne Collision Avoidance Systems Market Size:

Military Airborne Collision Avoidance Systems Market size is estimated to reach over USD 1,982.32 Million by 2032 from a value of USD 1,141.25 Million in 2024 and is projected to grow by USD 1,202.94 Million in 2025, growing at a CAGR of 7.8% from 2025 to 2032.

Military Airborne Collision Avoidance Systems Market Scope & Overview:

Military airborne collision avoidance systems are specialized technologies designed to prevent mid-air collisions between military aircraft during operations. These systems utilize advanced sensors, radar, and communication networks to monitor the airspace and provide real-time alerts to pilots, ensuring safety during complex maneuvers and mission-critical activities. They are essential for maintaining operational efficiency and preventing accidents in high-risk environments.

These systems are integrated with avionics suites and feature technologies such as traffic advisory systems, resolution advisories, and automated avoidance maneuvers. They are capable of detecting and responding to potential threats in dynamic airspaces, offering reliable performance even in challenging operational conditions. The systems are adaptable to various aircraft types, including fighter jets, transport planes, and unmanned aerial vehicles (UAVs).

End-users include air forces and defense organizations seeking advanced solutions to enhance flight safety and operational readiness. These systems play a crucial role in modernizing military aviation safety standards and reducing the risk of airborne collisions during tactical operations.

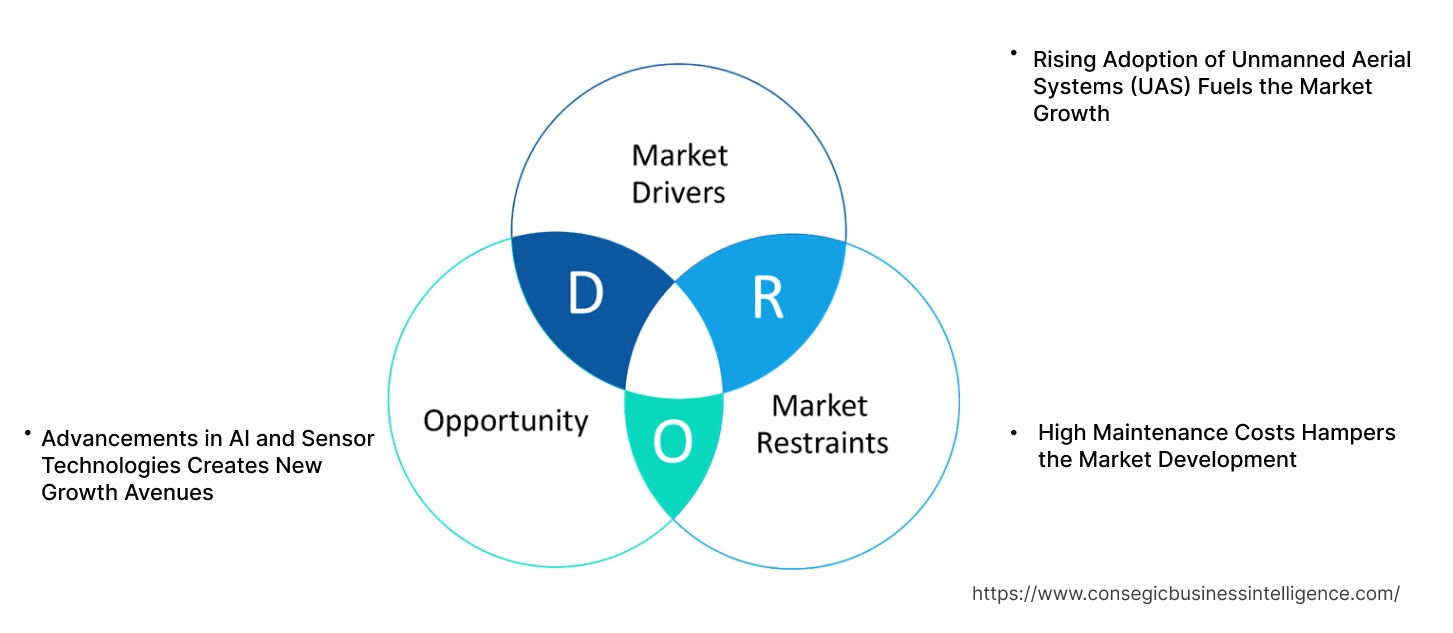

Military Airborne Collision Avoidance Systems Market Dynamics - (DRO) :

Key Drivers:

Rising Adoption of Unmanned Aerial Systems (UAS) Fuels the Market Growth

The growing deployment of unmanned aerial systems (UAS) in military operations is significantly boosting the demand for advanced collision avoidance systems. UAS are increasingly used for intelligence, surveillance, reconnaissance, and combat missions, often operating in congested airspaces or challenging environments. To ensure operational safety and mission success, these systems require precise navigation and obstacle detection technologies. Collision avoidance solutions equipped with advanced sensors, real-time data processing, and automated decision-making capabilities enhance the reliability of UAS by preventing mid-air collisions.

Moreover, the complexity of modern battlefields, with multiple aircraft and dynamic scenarios, further necessitates robust collision avoidance systems. As military forces expand the scope of UAS applications, including swarm operations and cross-border missions, the integration of these technologies has become critical to ensuring the safe and efficient execution of unmanned operations. This trend is driving significant innovation and investment in the development of advanced collision prevention systems for UAS, which further boosts the military airborne collision avoidance systems market growth.

Key Restraints:

High Maintenance Costs Hampers the Market Development

The advanced technologies used in military airborne collision avoidance systems, such as AI-powered algorithms and sophisticated sensors, require regular maintenance to ensure optimal performance. These systems involve intricate hardware and software components that demand specialized expertise for troubleshooting, repairs, and upgrades. The cost of spare parts, skilled labor, and system recalibration significantly adds to the operational expenses. For countries with constrained defense budgets, these high maintenance costs act as a barrier to adopting or expanding the use of such systems across their fleets. Thus, the aforementioned factors are hindering the military airborne collision avoidance systems market demand.

Future Opportunities :

Advancements in AI and Sensor Technologies Creates New Growth Avenues

The integration of artificial intelligence (AI) and advanced sensor technologies is revolutionizing collision avoidance systems in military aviation. AI-powered algorithms enable real-time decision-making, predictive analytics, and adaptive responses to dynamic airspace conditions. These systems process vast amounts of data from radar, LiDAR, and infrared sensors to detect and classify potential threats with high precision.

Additionally, AI enhances situational awareness by predicting potential collision scenarios, allowing proactive maneuvering to avoid accidents. Advanced sensors improve detection capabilities in complex environments, including adverse weather and high-speed operations, ensuring reliability and accuracy. This integration supports the increasing demand for sophisticated collision avoidance solutions to ensure operational safety during high-stakes missions. As the military industry embraces autonomous and semi-autonomous platforms, these advancements create significant military airborne collision avoidance systems market opportunities by addressing the challenges of congested airspaces and enhancing mission success rates.

Military Airborne Collision Avoidance Systems Market Segmental Analysis :

By System Type:

Based on system type, the market is segmented into Traffic Alert and Collision Avoidance System (TCAS), Ground Proximity Warning System (GPWS), Airborne Collision Avoidance Radar, and others.

The Traffic Alert and Collision Avoidance System (TCAS) segment accounted for the largest revenue of the total military airborne collision avoidance systems market share in 2024.

- TCAS systems prevent mid-air collisions by providing timely alerts to pilots, ensuring safety during military operations.

- The widespread adoption of TCAS in both manned and unmanned aerial platforms is a key factor driving its dominance.

- These systems are increasingly integrated with advanced avionics, enhancing their operational efficiency and reliability.

- As per market analysis, the high reliability of TCAS in identifying and mitigating collision risks underpins its extensive use across military applications, contributing to the military airborne collision avoidance systems market expansion.

The Airborne Collision Avoidance Radar segment is expected to grow at the fastest CAGR during the forecast period.

- These radars offer advanced real-time threat detection capabilities, which are essential for modern military operations.

- Growing investments in advanced radar technologies by defense organizations are propelling their adoption.

- These systems are highly effective in diverse operational scenarios, including adverse weather conditions.

- As per the military airborne collision avoidance systems market trends, the rising demand for precision-driven collision avoidance technologies contributes to the segment's robust growth trajectory.

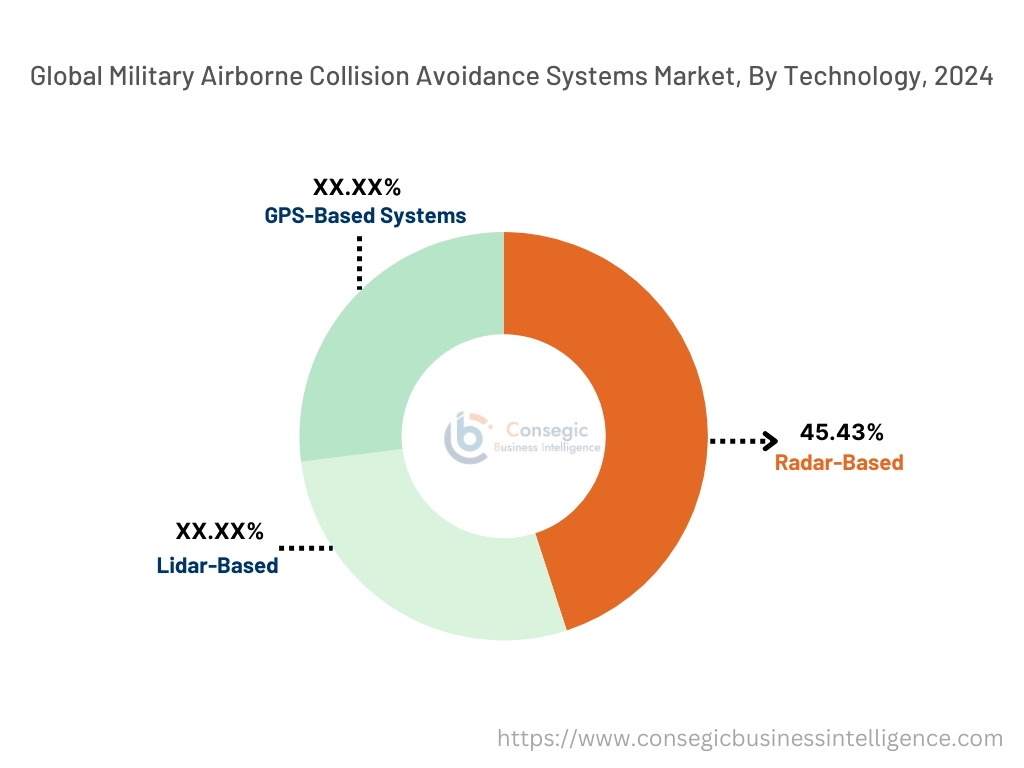

By Technology:

Based on technology, the market is categorized into radar-based, lidar-based, and GPS-based systems.

The Radar-Based segment accounted for the largest revenue of 45.43% of the total military airborne collision avoidance systems market share in 2024.

- Radar systems provide superior reliability in threat detection under complex and diverse environmental conditions.

- Military operators prefer radar-based technologies for their ability to perform effectively in harsh weather and combat zones.

- Continuous advancements in radar capabilities, such as real-time data processing and extended range detection, fuel their dominance.

- As per market trends, the integration of radar-based systems in modern military aircraft significantly enhances situational awareness, thereby driving the military airborne collision avoidance systems market growth.

The Lidar-Based segment is projected to grow at the fastest CAGR during the forecast period.

- Lidar systems offer high precision and suitability for autonomous aerial systems, driving their adoption.

- The increasing demand for lightweight and compact solutions in military UAVs contributes to the segment's rapid growth.

- Lidar technology ensures accurate detection and measurement, making it a vital component in advanced collision avoidance systems.

- As per military airborne collision avoidance systems market analysis, the segment benefits from growing investments in autonomous military applications and next-generation sensor technologies.

By Component:

Based on components, the market includes sensors, transponders, processors, display units, and others.

The Sensors segment accounted for the largest revenue share in 2024.

- Sensors form the backbone of collision avoidance systems by providing accurate data for threat detection and mitigation.

- Advancements in multi-sensor fusion technologies enhance their effectiveness in modern military aircraft.

- Their integration with AI-driven systems improves situational awareness and decision-making in high-risk scenarios.

- As per the segmental trends analysis, the pivotal role of sensors in ensuring operational safety and effectiveness underscores their market dominance, fueling the military airborne collision avoidance systems market demand.

The Processors segment is expected to grow at the fastest CAGR during the forecast period.

- High-speed processors enable advanced analytics and real-time threat assessment, essential for military collision avoidance.

- The segment's growth is fueled by the increasing need for sophisticated computing power in autonomous aerial platforms.

- These processors support seamless integration with avionics systems, enhancing overall system performance.

- The analysis of segmental trends depicts that the need for high-performance processors in next-generation military technologies accelerates the segment's adoption, creating new military airborne collision avoidance systems market opportunities.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

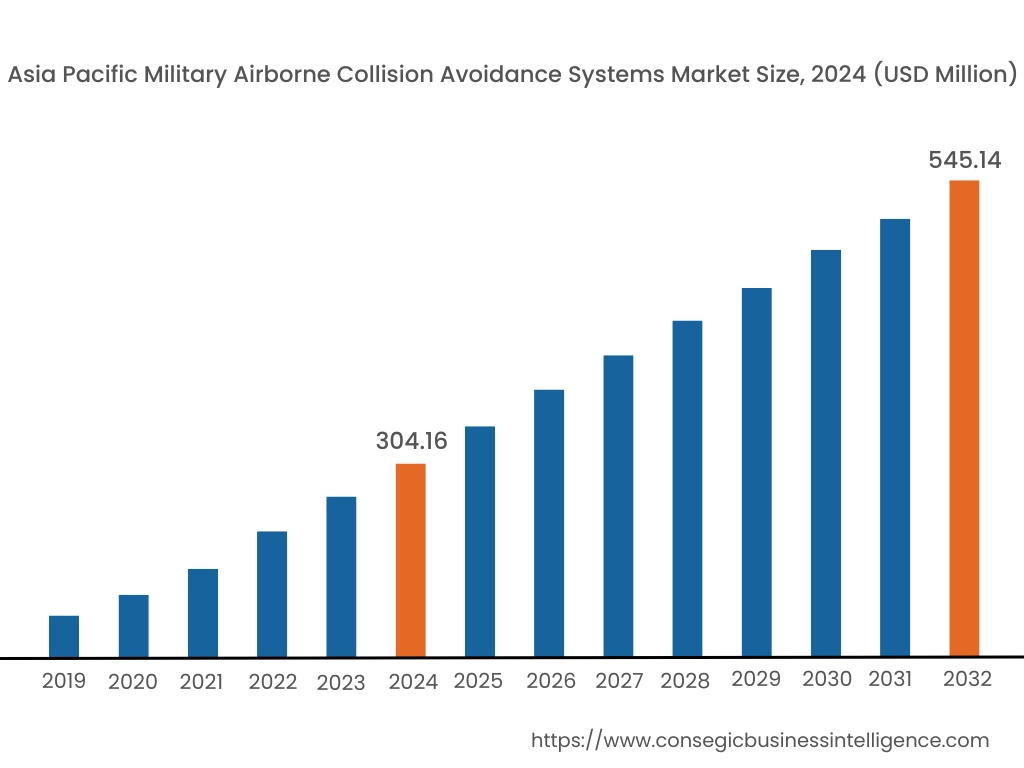

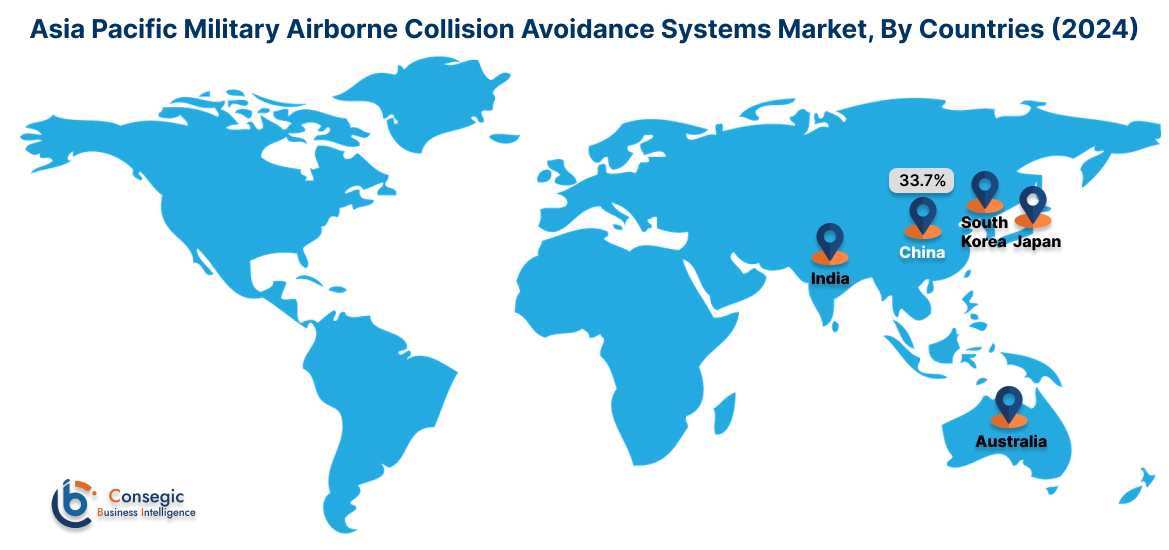

Asia Pacific region was valued at USD 304.16 Million in 2024. Moreover, it is projected to grow by USD 321.45 Million in 2025 and reach over USD 545.14 Million by 2032. Out of this, China accounted for the maximum revenue share of 33.7%. The Asia-Pacific region is witnessing a surge in requirement for military ACAS, propelled by increasing defense expenditures and the induction of advanced military aircraft. Countries such as China, India, and Japan are focusing on integrating collision avoidance systems to enhance flight safety. A prominent trend is the development of indigenous ACAS technologies to reduce reliance on foreign suppliers. Analysis suggests that regional security dynamics and technological advancements are key factors influencing the military airborne collision avoidance systems market expansion in this area.

North America is estimated to reach over USD 634.34 Million by 2032 from a value of USD 367.88 Million in 2024 and is projected to grow by USD 387.54 Million in 2025. This region holds a substantial share of the military ACAS market, driven by the United States' emphasis on enhancing flight safety and operational efficiency. The integration of advanced collision avoidance systems in military aircraft is a notable trend, aiming to reduce mid-air collision risks during complex missions. The military airborne collision avoidance systems market analysis indicates that ongoing modernization programs and investments in next-generation technologies are pivotal in shaping the market landscape in North America.

European nations, including the United Kingdom, France, and Germany, are actively investing in military ACAS to bolster air safety and comply with stringent aviation regulations. A significant trend is the collaboration among European defense manufacturers to develop sophisticated collision avoidance solutions tailored for various military aircraft.

In the Middle East, nations are prioritizing the enhancement of their military aviation safety measures, leading to investments in ACAS. The focus is on equipping existing and new military aircraft with advanced collision avoidance systems to mitigate risks during operations. However, the military airborne collision avoidance systems market trends shows that political instability and economic diversification efforts in certain areas may impact industry dynamics. In Africa, the market is gradually evolving, with a focus on addressing challenges related to airspace safety. Analysis indicates that international collaborations and capacity-building initiatives are playing a crucial role in enhancing military aviation safety capabilities across the continent.

Latin American countries are increasingly recognizing the importance of military ACAS in ensuring the safety of their air forces. Nations such as Brazil and Mexico are investing in collision avoidance technologies to modernize their military aviation capabilities. A notable trend is the emphasis on procuring cost-effective solutions that offer reliable performance.

Top Key Players and Market Share Insights:

The Military Airborne Collision Avoidance Systems market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Military Airborne Collision Avoidance Systems market. Key players in the Military Airborne Collision Avoidance Systems industry include -

- Honeywell International Inc. (USA)

- BAE Systems plc (UK)

- Raytheon Technologies Corporation (USA)

- Indra Sistemas S.A. (Spain)

- Collins Aerospace (USA)

- Thales Group (France)

- Saab AB (Sweden)

- Northrop Grumman Corporation (USA)

- Lockheed Martin Corporation (USA)

- L3Harris Technologies, Inc. (USA)

Military Airborne Collision Avoidance Systems Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 1,982.32 Million |

| CAGR (2025-2032) | 7.8% |

| By System Type |

|

| By Technology |

|

| By Component |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Military Airborne Collision Avoidance Systems Market? +

The Military Airborne Collision Avoidance Systems Market size is estimated to reach over USD 1,982.32 Million by 2032 from a value of USD 1,141.25 Million in 2024 and is projected to grow by USD 1,202.94 Million in 2025, growing at a CAGR of 7.8% from 2025 to 2032.

What are the key segments in the Military Airborne Collision Avoidance Systems Market? +

The market is segmented by system type (Traffic Alert and Collision Avoidance System (TCAS), Ground Proximity Warning System (GPWS), Airborne Collision Avoidance Radar, and others), technology (Radar-Based, Lidar-Based, GPS-Based), and component (Sensors, Transponders, Processors, Display Units, and others).

Which segment is expected to grow the fastest in the Military Airborne Collision Avoidance Systems Market? +

The Airborne Collision Avoidance Radar segment is expected to grow at the fastest CAGR during the forecast period due to its advanced real-time threat detection capabilities and increasing investments by defense organizations in radar technologies.

Who are the major players in the Military Airborne Collision Avoidance Systems Market? +

Key players in the Military Airborne Collision Avoidance Systems market include Honeywell International Inc. (USA), BAE Systems plc (UK), Thales Group (France), Saab AB (Sweden), Northrop Grumman Corporation (USA), Lockheed Martin Corporation (USA), L3Harris Technologies, Inc. (USA), Raytheon Technologies Corporation (USA), Indra Sistemas S.A. (Spain), and Collins Aerospace (USA).