- Summary

- Table Of Content

- Methodology

Microdisplay Market Scope & Overview:

Microdisplay, known for their small size and high pixel density, are essential elements in immersive technologies, delivering users a high-resolution viewing experience in a compact design. Advances in technology have resulted in microdisplay with improved brightness, contrast, and energy efficiency, serving a wide range of applications from military and defense to automotive and healthcare.

These displays provide excellent image quality and facilitate immersive viewing experiences, rendering them vital in cutting-edge digital imaging solutions. The market is also experiencing substantial development in the automotive industry, where these displays are utilized in heads-up displays (HUDs) to offer real-time information to drivers without distracting them from the road, thus improving safety and the overall driving experience.

Microdisplay Market Size:

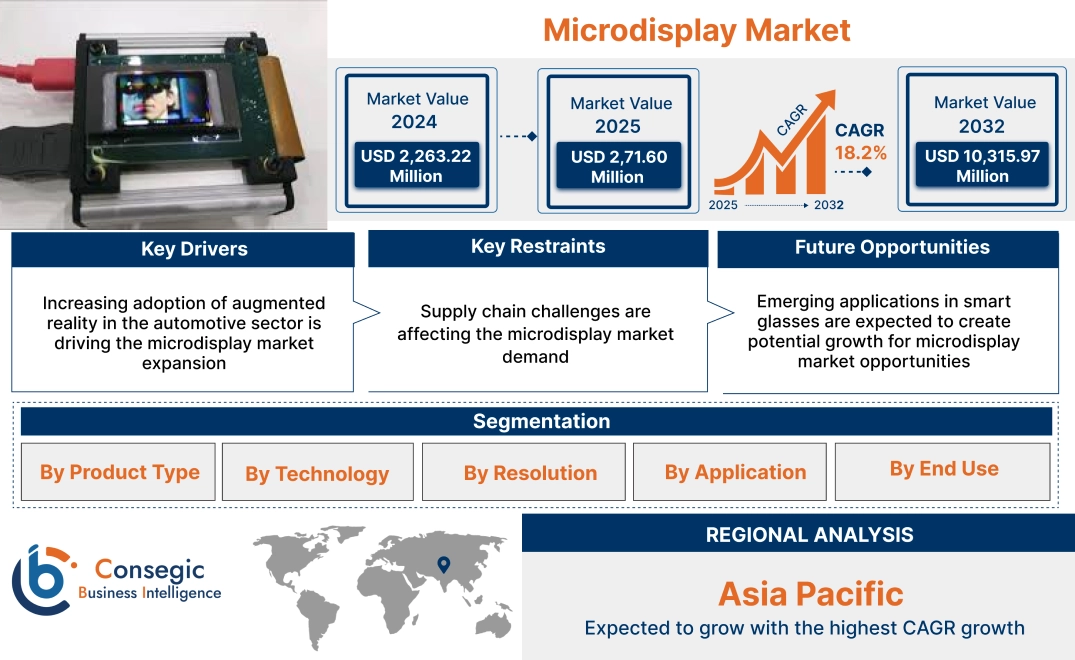

Microdisplay Market Size is estimated to reach over USD 10,315.97 Million by 2032 from a value of USD 2,263.22 Million in 2024 and is projected to grow by USD 2,71.60 Million in 2025, growing at a CAGR of 18.2% from 2025 to 2032.

Microdisplay Market Dynamics - (DRO) :

Key Drivers:

Increasing adoption of augmented reality in the automotive sector is driving the microdisplay market expansion

The incorporation of augmented reality (AR) within the automotive industry is a major catalyst for the worldwide market. As AR technologies improve driver hypervigilance and safety, the need for sophisticated microdisplay solutions, especially in Head-Up Displays (HUDs) and Advanced Driver Assistance Systems (ADAS), is escalating. For instance, Volkswagen leads the way by utilizing high-resolution data glasses and plans to integrate 3D HUDs that blend essential information with actual surroundings.

Further, DHL has noted a 15% boost in productivity from using AR Vision Picking smart glasses in its international warehouses, showcasing AR's game-changing capabilities. As businesses increasingly acknowledge the benefits of AR for real-time data representation and better training, the market is set for significant expansion.

- For instance, in May 2024, VueReal launched the ColorFusion microdisplay, an augmented reality display for multiple industries spanning automotive, consumer electronics, medical, and industrial.

- The ColourFusion display combines advanced full color microLED technology, an image quality improvement algorithm, and LCOS (Liquid Crystal on Silicon) systems to provide high resolution, increased grayscale and color depth, enhanced contrast, and remarkable low power usage through an energy-saving algorithm and adjustable frame rates.

Thus, according to the microdisplay market analysis, the growing augmented reality in the automotive sector is driving the microdisplay market size and trends.

Key Restraints:

Supply chain challenges are affecting the microdisplay market demand

Effectively tackling the significant challenges within the supply chain of the global market is crucial, as these issues can interfere with production timelines and prolong lead times. A major concern is the scarcity of essential components, especially specialized materials like semiconductors, OLED films, and MicroLED chips.

The rising demand for these components, together with restricted manufacturing capability, has led to considerable production setbacks in multiple sectors. Additionally, the production process for cutting-edge microdisplay heavily relies on scarce materials such as indium and gallium. Moreover, fluctuations in the availability of these raw materials can drastically impact production abilities, particularly as the market for high-performance displays continues to expand.

In addition to this, logistical challenges further heighten the supply chain difficulties, with disruptions in transportation caused by geopolitical conflicts and natural calamities leading to delays in the shipment of crucial components. These delays not only raise costs but also prolong lead times for manufacturers. These factors would further impact on the microdisplay market share during the forecast period.

Future Opportunities :

Emerging applications in smart glasses are expected to create potential growth for microdisplay market opportunities

The emerging uses for smart glasses are broadening the possibilities of microdisplay technology, changing how individuals engage with digital content and improving daily experiences. Another exciting application is found in mixed reality (MR), where smart glasses featuring advanced displays facilitate immersive interactions that merge virtual and physical environments. MR applications enrich training simulations, design prototyping, and educational experiences by allowing users to engage with 3D models and digital overlays in real time, promoting creativity and collaboration across different fields.

- For instance, in December 2024, Foxconn announced the partnership with Porotech, to enter in the AR glasses market. The partnership seeks to expedite Foxconn’s strategic progress in AR and MicroLED technologies, all while providing efficient and lightweight AR display solutions.

- This collaboration will utilize Porotech’s cutting-edge Gallium Nitride (GaN) technology in conjunction with Foxconn’s fully integrated services that include wafer processing, packaging, and optical module expertise, with the goal of fulfilling the manufacturing needs for microdisplay chips and AR eyewear.

Thus, based on the above analysis, the growing adoption of displays in smart glasses applications is driving the microdisplay market opportunities and trends.

Top Key Players and Market Share Insights:

The global microdisplay market is highly competitive with major players providing display solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the microdisplay industry include-

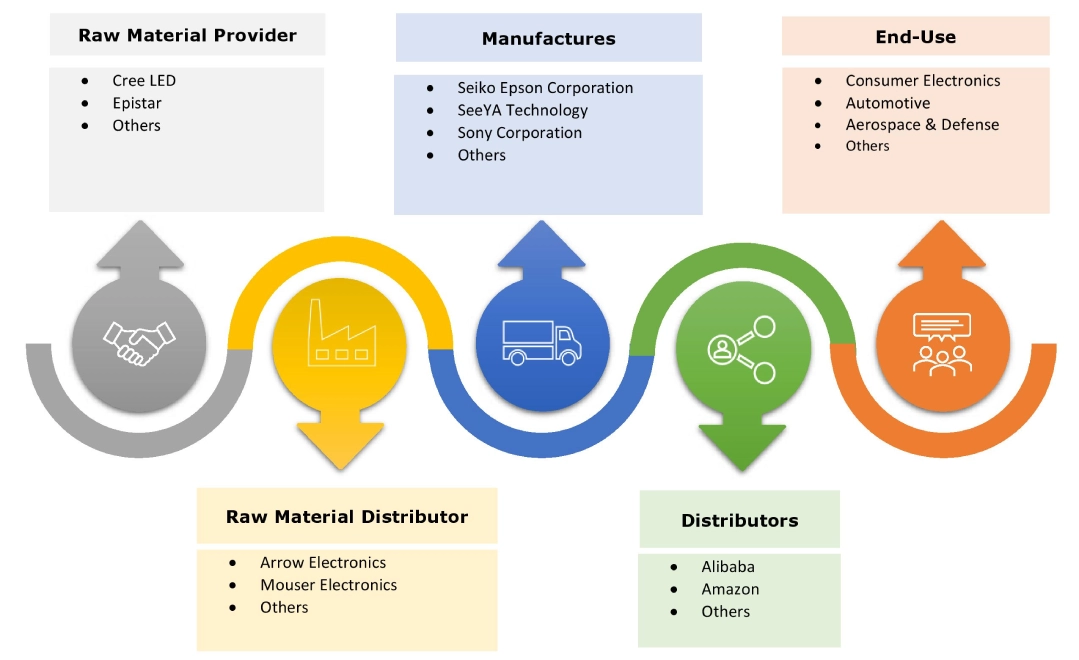

- Seiko Epson Corporation (Japan)

- SeeYA Technology (China)

- WiseChip Semiconductor Inc. (Taiwan)

- WINSTAR Display Co., Ltd. (Taiwan)

- Syndiant (U.S.)

- Sony Corporation (Japan)

- Kopin Corporation (U.S.)

- Himax Technologies, Inc. (Taiwan)

- HOLOEYE Photonics AG (Germany)

- eMagin Corporation (U.S.)

Microdisplay Market Segmental Analysis :

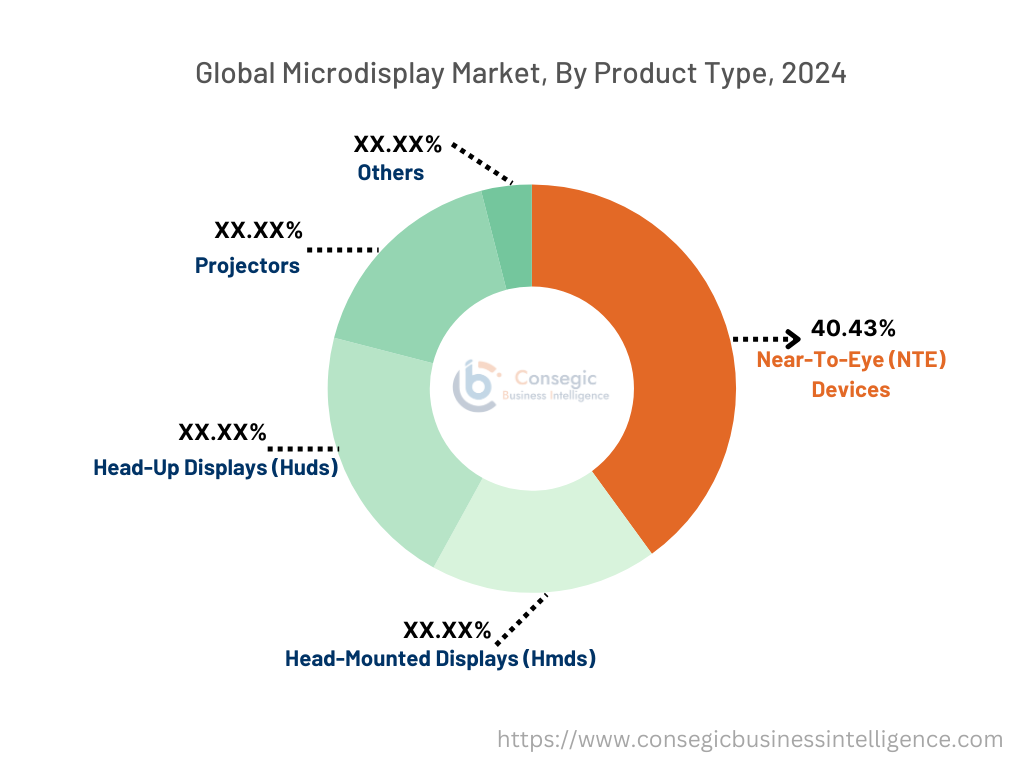

By Product Type:

Based on product type, the microdisplay market is segmented into Near-to-eye (NTE) Devices, Head-Mounted displays (HMDs), Head-up Displays (HUDs), Projectors, and others.

Trends in the product type:

- The increasing acceptance of augmented and virtual reality technologies is boosting the need for superior displays intended for use in HMDs.

- Manufacturers are persistently innovating and enhancing display technologies, such as MicroLED and OLED, which provide improved performance, greater resolution, and reduced energy usage.

- These factors, and analysis in display technologies in various end use industries would further create the microdisplay market demand and opportunities during the forecast period.

The near-to-eye devices segment accounted for the largest revenue share of 40.43% in the year 2024 and it is expected to register the highest CAGR during the forecast period.

- The segment growth can be attributed to the remarkable innovations and product introductions by major players in the fields of augmented reality (AR) and virtual reality (VR).

- Companies such as Meta and Sony have played a crucial role in this development. Meta's Meta Quest 3, equipped with cutting-edge NTE display technology, improves resolution and offers a more engaging experience for both gaming and social activities.

- Near-to-eye displays can produce a large image from a small, lightweight source display unit, facilitating their incorporation into compact devices like wearables. With high pixel density, they yield outstanding resolution and clarity, making them increasingly sought after in the medical and military sectors.

- For instance, in January 2025, Kopin Corporation showcased its advanced near-to-eye displays and application-specific optical solutions at SPIE AR/VR/MR 2025 in California. The demonstrations in the Kopin booth included FLCos, microLED displays, OLED, and integrated head-mounted displays, among others.

- These advancements in near-to-eye devices segment would further drive the microdisplay market size during the forecast period.

By Technology:

Based on technology, the market is segmented into Liquid Crystal Display (LCD), Organic Light-emitting Diode (OLED), Digital Light Processing (DLP), Liquid Crystal on Silicon (LCoS), and others.

Trends in technology:

- OLED displays provide outstanding image clarity with elevated contrast ratios, rich blacks, and swift response times. Additionally, they consume less energy compared to LCDs.

- LCoS displays merge the benefits of LCD and reflective technologies. They deliver high resolution alongside impressive image quality. LCOS displays are commonly utilized in projection settings.

- These displays are progressively adopted in automotive contexts, like HUDs and AR dashboards, to relay essential information to drivers while minimizing distractions from driving.

- The microdisplay market is set for considerable development in the near future, fuelled by technological progress, rising interest in AR/VR devices, and a wider acceptance across multiple applications.

The Liquid Crystal Display (LCD) segment accounted for the largest revenue share in the year 2024.

- LCDs are preferred for their capability to deliver high-quality visuals with outstanding color accuracy and energy efficiency, rendering them perfect for various uses. Companies like Samsung, LG Display, and Sharp have been leaders in LCD innovation, constantly improving display clarity and energy effectiveness.

- LG Display's breakthroughs in LCD technology have allowed for the creation of ultra-slim screens that are lightweight and ideal for portable gadgets, thereby increasing demand in industries like smartphones and tablets. Beyond conventional LCDs, progress in specialized LCD types, such as IPS (In-Plane Switching) and VA (Vertical Alignment), has further improved viewing angles and contrast ratios, making these displays highly desired in gaming and professional fields.

- For instance, in January 2023, Seiko Epson Corporation announced the lajunched of its PowerLite and BrightLink laser projector series. The latest models feature 12 new lamp-free laser displays driven by Epson's exclusive 3-chip 3LCD technology, along with appropriate collaboration tools, straightforward installation, and ultra-wide options to ensure that every participant can see, engage, and be visible.

- The factors and developments are shaping the future of microdisplay market growth.

The Liquid Crystal on Silicon (LCoS) segment is anticipated to register the fastest CAGR during the forecast period.

- LCoS technology is ideal for projection uses, and the rising need for high-definition projectors in different environments (home theaters, classrooms, conference rooms) is fuelling the progression of LCoS displays.

- Consumers and companies are progressively seeking high-calibre displays with clear images, excellent contrast, and precise colors. LCoS technology satisfies these needs, promoting its use in a range of applications.

- Ongoing progress in LCoS technology, including enhanced brightness and contrast, is enhancing its appeal for multiple applications.

- These factors and analysis in the display technologies would further drive the global market during the forecast period.

By Resolution:

Based on the resolution, the market is segmented into standard display resolution, ultra-high resolution, 4K resolution.

Trends in the resolution:

- Emerging technologies such as MicroLED and enhanced OLED are facilitating the development of displays with notably greater resolutions.

- Manufacturers are concentrating on lowering pixel pitch (the space separating pixels) to obtain higher resolution without enlarging the overall dimensions of the displays.

- These developments and analysis would further supplement the microdisplay market trends during the forecast period.

The ultra-high resolution segment accounted for the largest revenue share in the year 2024 and it is expected to register the highest CAGR during the forecast period.

- New innovations such as MicroLED and OLED on Silicon (OLEDoS) are leading the advancement of ultra-high-resolution displays. These advancements provide the capability for very tiny pixel dimensions and substantial brightness, which are crucial for realizing ultra-high resolution.

- To fully leverage the advantages of ultra-high resolution, displays are being combined with eye-tracking and foveated rendering technologies.

This enables the display to prioritize the highest resolution on the region the user is focusing on, while lowering the resolution in the peripheral vision, thus enhancing processing efficiency and reducing power usage.

- These factors and analysis in the resolution segment would further drive the microdisplay market growth during the forecast period.

By Application:

Based on application, the market is segmented into night vision/thermal imaging devices, medical equipment and scientific imaging, simulation training, mobile computing systems, field maintenance and repair, AR/VR, instrumentation and test equipment, 3D HD gaming, drones and FPV, and others.

Trends in application:

- Microdisplay serve an essential function in AR/VR headsets, delivering the visuals that foster immersive experiences.

- In the automotive and aviation sectors, HUDs display information on the windshield or a clear screen, enabling users to access vital data without diverting their attention from their main task. Micro displays are crucial for developing compact and efficient HUDs.

- In cameras and camcorders, EVFs utilize displays to offer a high-resolution preview of the scene being recorded. This is particularly beneficial in professional settings where precise framing and focus are of utmost importance.

- These analysis and factors, such as growing demand for immersive experience and advancements in display technologies would further drive the microdisplay market share during the forecast period.

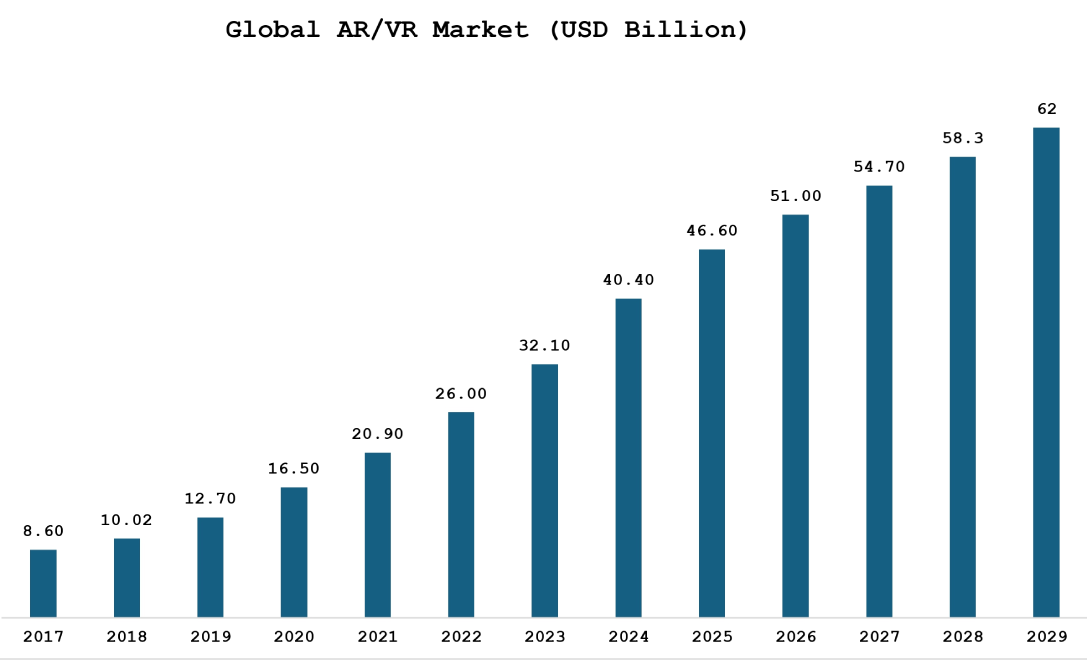

The AR/VR segment accounted for the largest revenue in the year 2024 and it is expected to register the highest CAGR during the forecast period.

- MicroLED and OLED displays are becoming more popular in AR/VR because of their exceptional performance features, including high brightness, excellent contrast, and quick response times.

- The growing enthusiasm for augmented and virtual reality is the main catalyst for the global market within this field. As AR/VR technology evolves and becomes more widely available, the need for top-quality displays will keep increasing.

- The ongoing progress in display technologies, such as enhanced resolution, better image clarity, and reduced energy usage, is making them increasingly appropriate for AR/VR applications.

- Leading companies are making significant investments in the development of AR/VR hardware and software, which is boosting the need for advanced displays.

- For instance, in April 2024, Researchers at the Fraunhofer Institute for Photonic Microsystems (IPMS) have achieved noteworthy progress in creating semi-transparent OLED displays, managing to enhance the transparency of their OLED displays to 45%. This groundbreaking technology has led to a high-resolution display that is considerably lighter than conventional optical see-through systems utilized in augmented reality applications.

- Thus, factors and trends, such as growing popularity of AR/VR and expanding applications of AR/VR are driving the microdisplay market trends during the forecast period.

By End Use:

Based on the end use, the market is segmented into consumer electronics, automotive, aerospace & defense, healthcare, sports & entertainment, industrial, manufacturing, education, retail, and others.

Trends in the end use:

- Consumers are progressively looking for tailored experiences with their devices. The screens facilitate this by offering personalized information and visuals.

- The rise of smart gadgets, such as wearables and interconnected devices, is fuelling the need for display solutions during the forecast period.

- Both consumers and enterprises are requesting superior displays featuring crisp images, excellent contrast, and true-to-life colors, leading to a greater demand for enhanced displays.

- Thus, growing advancements in consumer electronics and automotive industries would further supplement the market demand during the forecast period.

The consumer electronics segment accounted for the largest revenue share in the year 2024.

- Microdisplay play a crucial role in the performance of products like VR headsets, wearable technology, and AR glasses in the consumer electronics sector. These displays provide immersive visual experiences for digital content viewing, gaming, and entertainment, featuring high pixel density and low latency.

- Additionally, the increasing need for portable and user-friendly devices, along with the expanding use of smartphones, smart glasses, and smartwatches, is driving market throughout the projected period.

- These advantages are anticipated to further drive the global market during the forecast period.

The automotive segment is anticipated to register the fastest CAGR during the forecast period.

- These displays are employed in automotive applications like heads-up displays (HUDs), augmented reality dashboards, and entertainment systems for backseat passengers.

- They enable drivers to see crucial information such as navigation instructions and vehicle diagnostics without taking their focus off the road, improving safety and the overall driving experience.

- Additionally, the emerging advancements in displays and the incorporation of cutting-edge features by major companies permit drivers to manage music and reply to calls and messages without losing focus.

- For instance, Harman’s augmented reality platform merges the physical and digital world to create intelligent overlays in the real-time onto the road surface without blocking the driver’s view.

- These trends are anticipated to further drive the global market during the forecast period.

Microdisplay Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 10,315.97 Million |

| CAGR (2025-2032) | 18.2% |

| By Product Type |

|

| By Technology |

|

| By Resolution |

|

| By Application |

|

| By End Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Regional Analysis:

The global market has been classified by region into North America, Europe, Asia-Pacific, MEA, and Latin America.

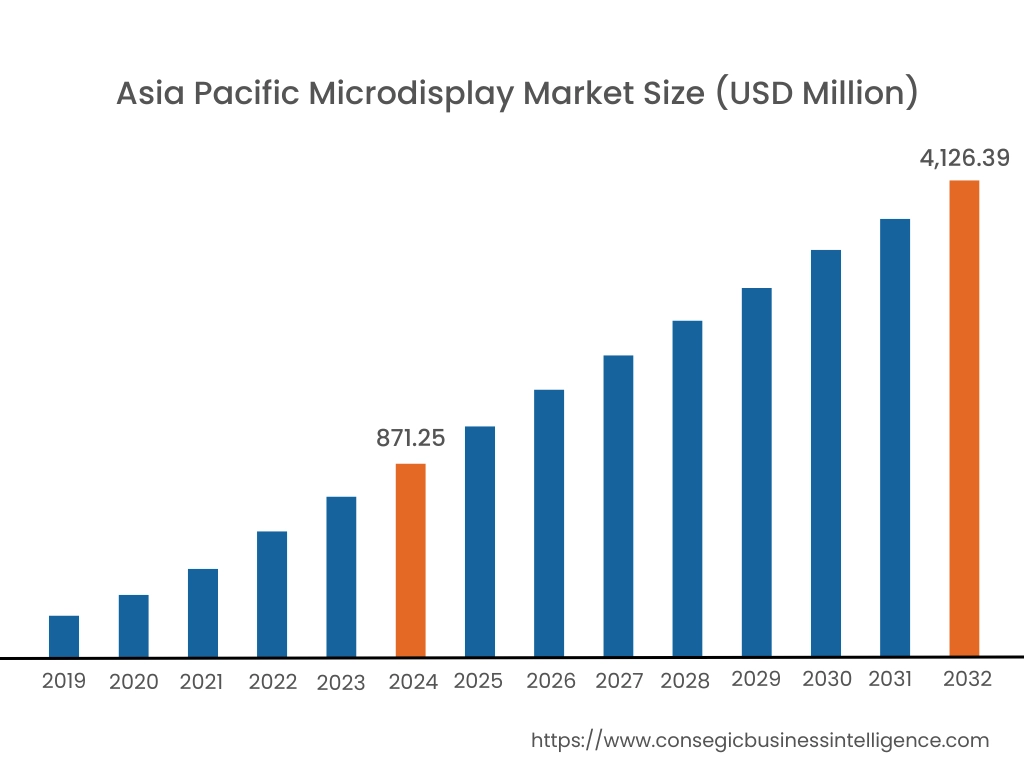

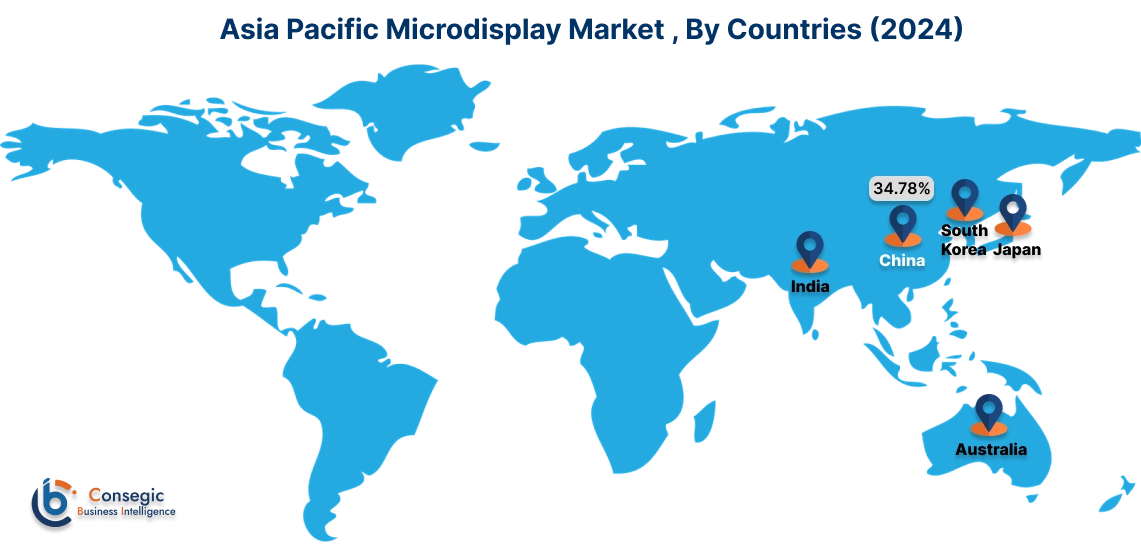

Asia Pacific microdisplay market expansion is estimated to reach over USD 4,126.39 million by 2032 from a value of USD 871.25 million in 2024 and is projected to grow by USD 1,048.03 million in 2025. Out of this, the China market accounted for the maximum revenue split of 34.78%. Countries such as China, Japan, and India are experiencing significant development in their consumer electronics sectors, leading producers to implement cutting-edge display technologies. Further, the significant funding in augmented reality (AR) and virtual reality (VR) is apparent in Japan, as firms like Panasonic are creating AR eyewear equipped with high-performance displays. Moreover, the automotive industry in South Korea and Japan is swiftly incorporating display solutions into advanced driver-assistance systems (ADAS) and head-up displays (HUDs). This regional emphasis on innovation and investment establishes the Asia-Pacific area as a crucial participant in the worldwide microdisplay market, ready for continuous development. These factors would further drive the market trends during the forecast period.

- For instance, in June 2024, LG Display has revealed the commencement of large-scale manufacturing for the globe's pioneering 13-inch Tandem OLED display intended for laptops. The firm is focusing on the OLED sector by utilizing the improved efficiency and reduced energy usage provided by Tandem OLED technology.

North America market is estimated to reach over USD 2,523.29 million by 2032 from a value of USD 557.58 million in 2024 and is projected to grow by USD 668.14 million in 2025. North America has positioned itself as the quickest expanding region in the microdisplay market, fueled by the increasing need for sophisticated display technologies across various industries. This growth can be attributed to the surging interest in augmented reality (AR) and virtual reality (VR) uses, especially in head-mounted displays (HMDs) and head-up displays (HUDs) in the automotive sector. These advancements have markedly boosted the necessity for compact, high-resolution, and energy-effective displays. Further, The United States and Canada are spearheading this progress with significant investments in the consumer electronics arena. Additionally, the rising popularity of wearable devices and smart glasses further accelerates market growth, as these technologies increasingly integrate display solutions to enhance user experiences. These factors and developments would further drive the regional microdisplay market during the forecast period.

- For instance, in January 2022, Sony Group Corporation launched OLED displays designed for mirrorless cameras, electronic viewfinders (EVF), head-mounted displays (HMD), and various other uses. Boasting outstanding quality and clarity, these displays appear to hold significant promise for incorporation in wearable devices featuring AR (augmented reality) and VR (virtual reality) functionalities.

According to the microdisplay industry, the European market has seen robust progression in recent years. European automotive manufacturers are progressively incorporating display technology into their vehicles for use such as HUDs and augmented reality dashboards, which is fostering market development. Additionally, due to rising concerns regarding sustainability, there is considerable emphasis on creating energy-efficient display solutions in Europe. Additionally, the use of cutting-edge technology, the accessibility of consumer electronic goods in the region, the growth of several large companies in various sectors of Latin America, and the rise of many tech-focused industries are anticipated to foster greater growth in the years ahead. Additionally, Governments in the MEA area are promoting the advancement of technology and innovation, which can indirectly aid the microdisplay market. Additionally, the growing interest in augmented and virtual reality is boosting the need for high-quality displays for AR/VR devices in the MEA region. Thus, on the above microdisplay market analysis and trends, these factors would further drive the regional market during the forecast period.

Recent Industry Developments :

Agreement:

- In February 2024, Kopin Corporation, a firm providing optical solutions tailored for distinct applications and high-performance micro-displays for defense, business, consumer, and medical sectors, has received a new contract from the Naval Air Warfare Center for Small Business Innovation Research (SBIR). This agreement entails Kopin leveraging its more than 30 years of experience in display development in the United States to produce sophisticated displays specifically crafted for lens less computational imaging.

Key Questions Answered in the Report

How big is the Microdisplay market? +

Microdisplay Market Size is estimated to reach over USD 10,315.97 Million by 2032 from a value of USD 2,263.22 Million in 2024 and is projected to grow by USD 2,713.60 Million in 2025, growing at a CAGR of 18.2% from 2025 to 2032.

Which is the fastest-growing region in the Microdisplay market? +

Asia-Pacific is the region experiencing the most rapid growth in the market.The regional growth can be attributed to the growing demand for consumer electronics in countries such as China and India, the high volume of companies engaged in the electronics and automotive production sector, technological improvements embraced by various firms, and the accessibility of products.

What specific segmentation details are covered in the Microdisplay report? +

The microdisplay report includes specific segmentation details for product type, technology, resolution, application, and end use, and region.

Who are the major players in the Microdisplay market? +

The key participants in the market are Seiko Epson Corporation (Japan), SeeYA Technology (China), Sony Corporation (Japan), Kopin Corporation (U.S.), Himax Technologies, Inc. (Taiwan), HOLOEYE Photonics AG (Germany), eMagin Corporation (U.S.), WiseChip Semiconductor Inc. (Taiwan), WINSTAR Display Co., Ltd. (Taiwan), Syndiant (U.S.), and others.