- Summary

- Table Of Content

- Methodology

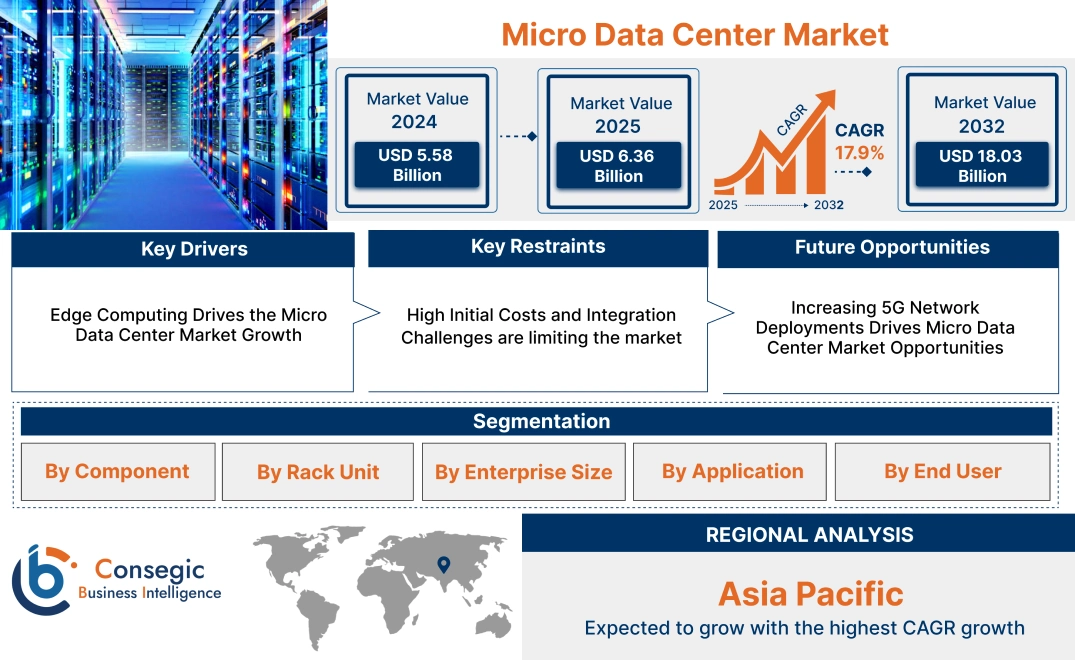

Micro Data Center Market Size:

Micro Data Center Market Size is estimated to reach over USD 18.03 Billion by 2032 from a value of USD 5.58 Billion in 2024 and is projected to grow by USD 6.36 Billion in 2025, growing at a CAGR of 17.9% from 2025 to 2032.

Micro Data Center Market Scope & Overview:

Micro data centers are compact data center solutions designed for deployment in close proximity to data sources, enabling localized data processing and storage. They typically include essential infrastructure components such as servers, storage, networking, and cooling systems. The benefits of using data centers include reduced latency, enhanced reliability, improved security, increased scalability and flexibility, and reduced bandwidth costs. Further key factors driving the market include the increasing demand for localized data processing due to the proliferation of IoT and 5G applications, and growing need for modular and scalable infrastructure solutions to support edge computing deployments.

Micro Data Center Market Dynamics - (DRO) :

Key Drivers:

Edge Computing Drives the Micro Data Center Market Growth

The surge in edge computing is a primary catalyst for the data center market's expansion. Edge computing brings computational resources closer to data sources, enabling faster response times crucial for IoT, 5G, and AI-driven applications. Further, data centers provide localized infrastructure for data processing and storage which reduces reliance on distant data centers in turn improving efficiency and reliability. Furthermore, the increasing need for immediate data analysis in sectors like manufacturing, healthcare, and autonomous vehicles further accelerates the adoption of data centers.

- For instance, Dell Technologies Inc. offers Micro 815 which is a self-contained, single 48RU IT rack solution designed for edge deployments, offering integrated power and cooling options of 10, 20, or 30kW. The system is UL Listed and CE Marked, making it suitable for standard IT deployments in telecommunications environments.

Thus, increasing adoption of IoT, 5G, and AI is driving the edge computing which in turn drives the micro data center market size.

Key Restraints:

High Initial Costs and Integration Challenges are limiting the market

The data center market faces significant hurdles due to high initial costs and integration challenges. The deployment of facilities involves substantial upfront investments in hardware, cooling systems, power infrastructure, and security measures. This financial barrier particularly affects small and medium enterprises, hindering their ability to adopt edge computing solutions. Furthermore, integrating data centers into existing IT architecture presents considerable complexity. Compatibility issues with legacy systems, network configurations, and data management protocols can lead to prolonged deployment times and increased operational costs. Thus, high initial costs and the need for specialized expertise to manage integrations limit the micro data center market growth.

Future Opportunities :

Increasing 5G Network Deployments Drives Micro Data Center Market Opportunities

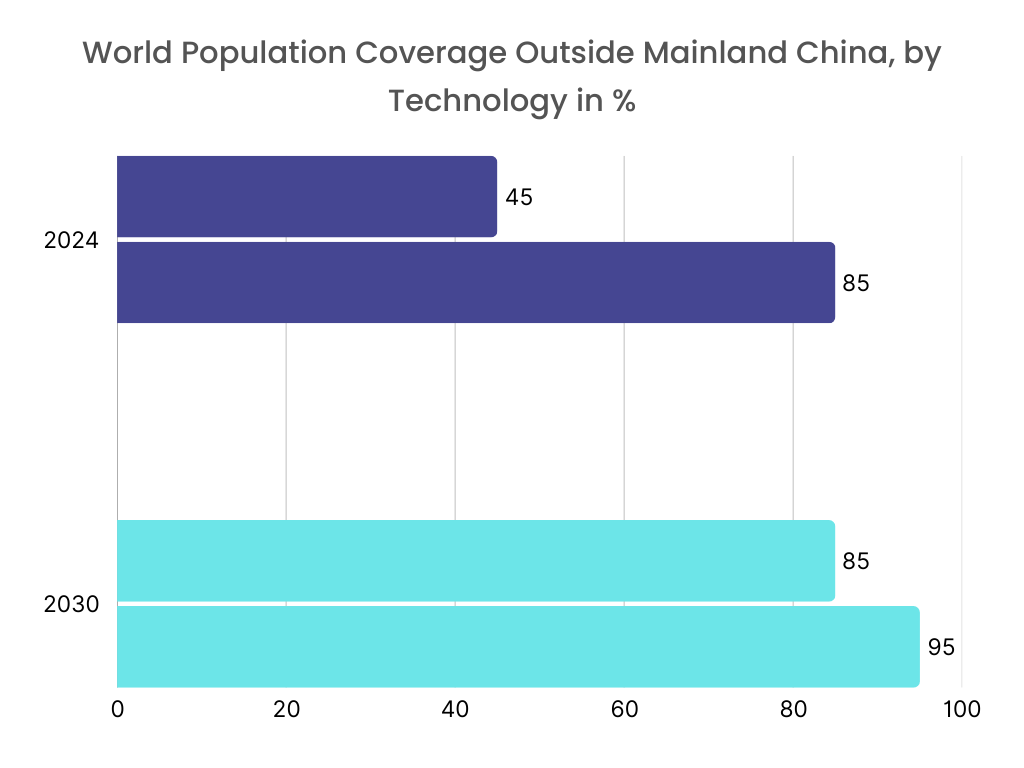

The rapid deployment of 5G networks is significantly expanding opportunities within the micro data center market. Edge computing infrastructure is crucial for unlocking the full capabilities of 5G's ultra-low latency and high bandwidth. Further micro data centers are crucial in this context, providing the localized processing power needed to support 5G applications. Furthermore, as 5G networks proliferate, the demand for edge data centers to handle data-intensive tasks like augmented reality, autonomous driving, and industrial automation is escalating.

- For instance, according to Ericsson Mobility Report, by 2030, 5G technology will cover approximately 85% of the population outside of mainland China. Moreover, in Europe, 5G mid-band coverage is expanding, rising from about 30% in late 2023 to an anticipated 45% by the end of 2024.

Thus, telecommunication providers are investing in these technologies to ensure seamless 5G performance, thereby driving micro data center market opportunities.

Micro Data Center Market Segmental Analysis :

By Component:

Based on the component, the market is segmented into solution and services.

Trends in the Component:

- The proliferation of IoT devices, 5G networks, and AI applications is driving the need for localized data processing which in turn drives micro data center market trends.

- Increasing adoption in applications including telecommunication, healthcare, BFSI, and others is expected to drive micro data center market size.

Solution accounted for the largest revenue share in the year 2024.

- There's a strong trend towards energy-efficient data center solutions which include advanced cooling systems, efficient power management, and the use of renewable energy in turn driving the micro data center market share.

- Further, modular designs are gaining popularity due to their flexibility, scalability, and ease of deployment.

- Moreover, advancement in cooling technologies further drives the micro data center market trends.

- Thus, as per micro data center market analysis, energy efficiency, modular designs, and cooling technologies are driving the market.

Services is anticipated to register the fastest CAGR during the forecast period.

- There’s a rising demand for specialized services that cater to the unique requirements of edge data centers which in turn drives the micro data center market share.

- Further, remote monitoring and management services are essential for ensuring up time and performance in turn drives the market.

- Therefore, based on analysis, aforementioned factors are anticipated to boost the market during the forecast period.

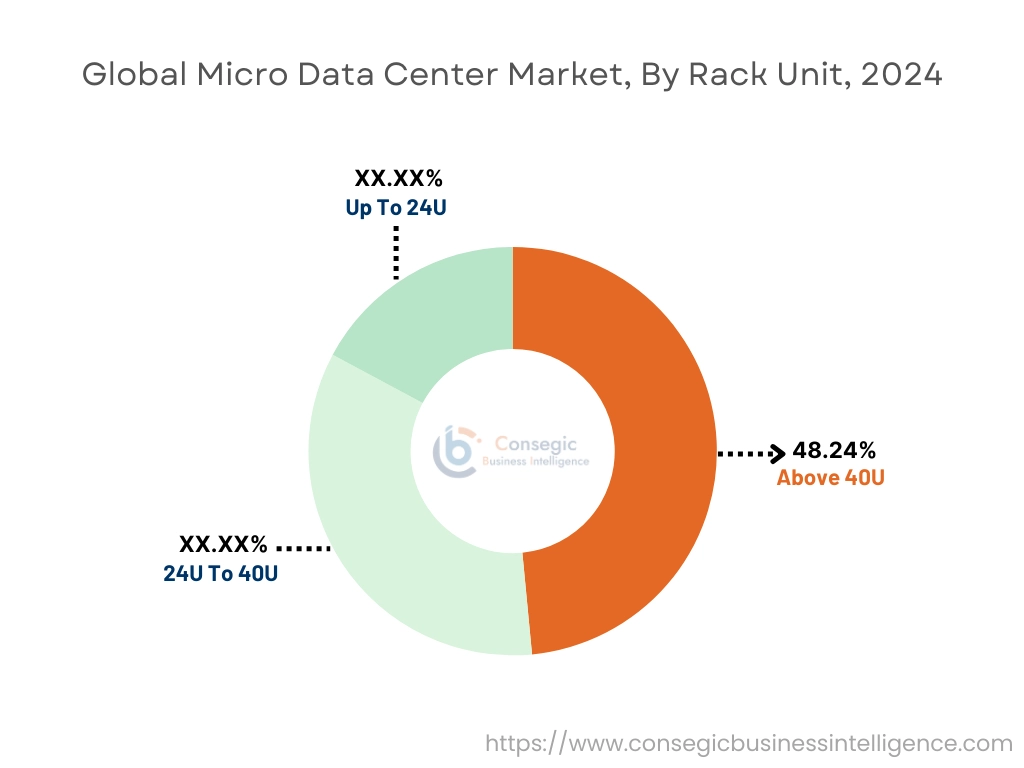

By Rack Unit:

Based on the rack unit, the market is segmented into Up to 24U, 24U to 40U, and Above 40U.

Trends in the Rack Unit:

- Up to 24U rack units are ideal for edge computing deployments, supporting IoT devices and localized data processing.

- Increased use of up to 24U rack units in retail and branch offices further drives the market growth.

Above 40U accounted for the largest revenue share of 48.24% in the year 2024.

- There is a growing emphasis on automation, and centralized management software which drives the demand for above 40U rack units.

- Further, above 40U rack units require robust cooling and power infrastructure to handle the high heat loads and power consumption in turn driving the micro data center industry.

- Furthermore, these larger rack units are designed for high-density computing and storage applications.

- Thus, as per micro data center market analysis, high-density computing, advanced cooling, and emphasis on automation are driving the market.

24U to 40U is anticipated to register the fastest CAGR during the forecast period.

- 24U to 40U rack unit offers a balance between computing and storage capacity, making it suitable for a wider range of applications, including data storage, and localized cloud applications.

- Further, these units provide scalability, allowing organizations to expand their infrastructure as their needs grow, by adding additional racks which subsequently propels the micro data center market expansion.

- Furthermore, these rack dimensions are very common in edge data center deployments that requires a balance between dimension and processing power.

- Therefore, based on analysis, balanced computing & storage and use in small to medium edge data centers is anticipated to boost the growth of the market during the forecast period.

By Enterprise Size:

Based on the enterprise size, the market is segmented into large enterprises and small and medium-sized enterprises.

Trends in the Enterprise Size:

- SMEs are increasingly recognizing the importance of business continuity and disaster recovery and are using modular data centers to provide localized backups, and redundancy which in turn drives the micro data center market expansion.

Large enterprises accounted for the largest revenue share in the year 2024

- Large enterprises are increasingly utilizing modular data centers to bridge the gap between their on-premises infrastructure and cloud resources.

- Further, large enterprises are prioritizing security and compliance in modular data center deployments which in turn drives the market.

- Thus, based on analysis, hybrid cloud strategy and emphasis on security and compliance are driving the market.

Small and medium-sized enterprises is anticipated to register the fastest CAGR during the forecast period.

- SMEs are seeking cost-effective and scalable data center solutions that can adapt to their changing business needs.

- Further, as edge computing becomes more accessible, SMEs are increasingly adopting compact data centers to support applications like localized data storage, remote monitoring, and point-of-sale systems which subsequently propel the market.

- Therefore, cost-effective & scalable solutions and increased adoption of edge applications are anticipated to boost the growth of the market during the forecast period.

By Application:

Based on the application, the market is segmented into disaster recovery, edge computing, data storage, cloud computing, and high-performance computing.

Trends in the Application:

- There's a focus towards processing and storing data closer to the source which in turn drives the micro data center market demand.

- Modular data centers are enabling distributed disaster recovery strategies, providing redundant infrastructure at multiple locations.

Edge computing accounted for the largest revenue share in the year 2024 and is anticipated to register the fastest CAGR during the forecast period.

- The rollout of 5G networks is a major catalyst for edge computing which in turn drives the market.

- Further, proliferation of Internet of Things (IoT) devices is generating massive amounts of data which is driving the need for edge computing.

- Furthermore, as edge deployments increase, there's a growing focus on securing data and devices at the edge in turn driving the market.

- Thus, 5G deployment, edge security, and proliferation of internet of things are driving the market.

By End User:

Based on the end user, the market is segmented into BFSI, IT & telecommunication, energy, government, healthcare, industrial, and others.

Trends in the End User:

- The BFSI industry is increasingly deploying modular data centers to ensure data security and meet stringent regulatory requirements which in turn drives the micro data center market demand.

- Modular data centers are essential for supporting IIoT applications, enabling real-time data analysis and automation in manufacturing and other industrial settings.

IT & telecommunication accounted for the largest revenue share in the year 2024 and is anticipated to register the fastest CAGR during the forecast period.

- Telecommunications companies are heavily investing in data centers to support the rollout of 5G networks, driving the market.

- Further, data centers are facilitating the virtualization of network functions, allowing for greater flexibility and scalability in network management.

- Furthermore, telecom companies utilize data centers to bridge the gap between centralized cloud resources and edge devices, enabling hybrid and multi-cloud deployments.

- For instance, in November 2022, Rittal introduced RiMatrix Micro Data Centers that provide a compact, efficient, and rapidly deployable solution for edge computing and distributed IT infrastructure by integrating all necessary OT components into a standardized package.

- Thus, rise of 5G technology, network function virtualization, and hybrid and multi-cloud deployments are driving the market.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

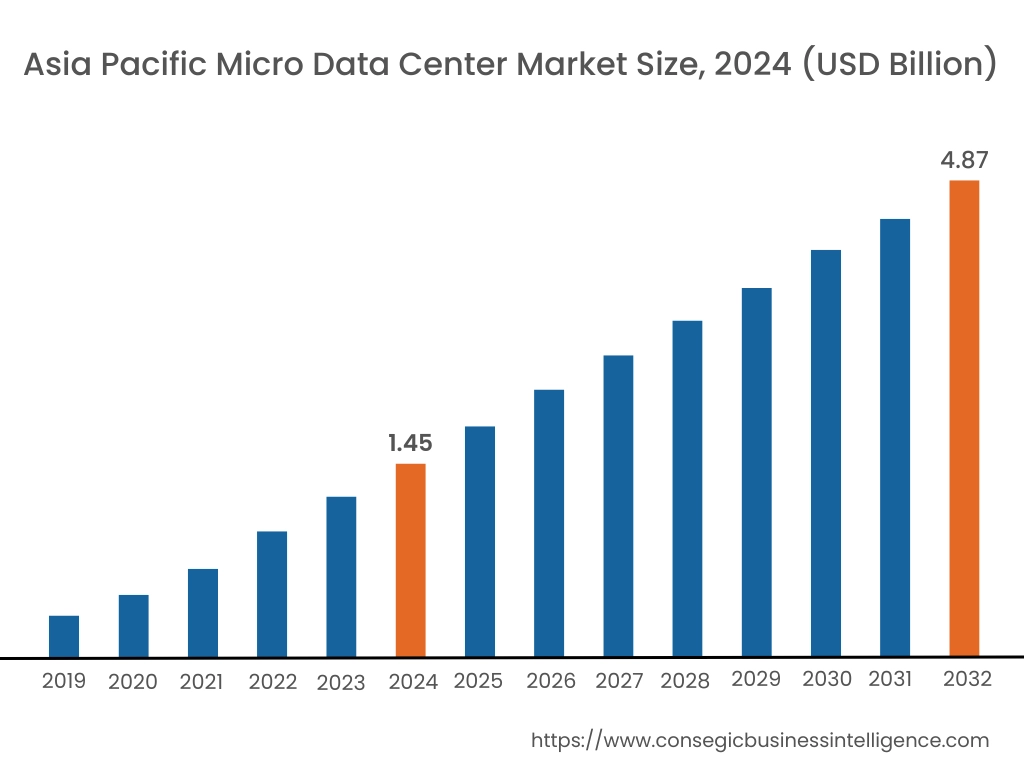

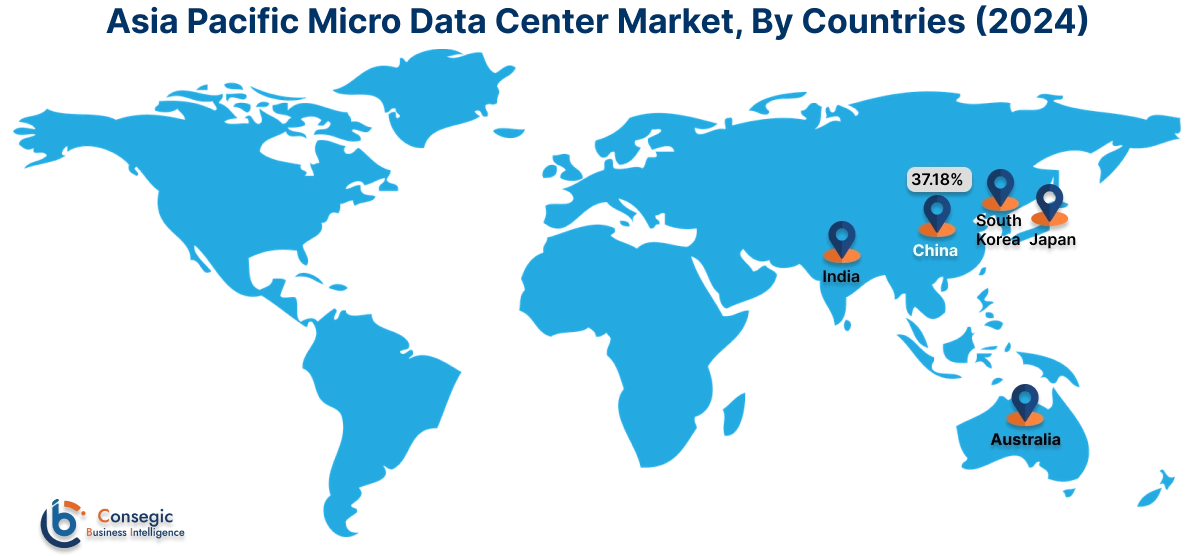

Asia Pacific region was valued at USD 1.45 Billion in 2024. Moreover, it is projected to grow by USD 1.66 Billion in 2025 and reach over USD 4.87 Billion by 2032. Out of this, China accounted for the maximum revenue share of 37.18%. The market growth for data center is mainly driven by rapid adoption of 5G networks and the increasing adoption of IoT devices. Additionally, the region's accelerated digital transformation across various sectors, including telecommunications, healthcare, and manufacturing, is fueling the market.

- For instance, in October 2021, Schneider Electric launched the Easy Micro Data Center Series, aimed at standard IT and commercial environments. These pre-integrated solutions combine compute, storage, and infrastructure for edge computing, emphasizing speed, reliability, and affordability.

North America is estimated to reach over USD 6.59 Billion by 2032 from a value of USD 2.04 Billion in 2024 and is projected to grow by USD 2.32 Billion in 2025. The North American market is primarily driven by rapid adoption of edge computing, due to the high demand for low-latency applications across various industries. Furthermore, the established and expanding presence of major technology companies significantly contributes to the market's growth.

- In October 2024, MARA, in collaboration with NGON, is deploying 25-megawatt micro data centers at oil wellheads in Texas and North Dakota. These data centers will be powered by excess natural gas, converting it to electricity.

The regional trends analysis depicts that stringent data sovereignty regulations and increasing adoption of edge computing to support 5G deployment in Europe is driving the market. Additionally, the factors driving the market in the Middle East and African region are increasing investments in digital infrastructure and the rapid adoption of cloud. Further, accelerating digital transformation and increasing investments in telecommunications infrastructure is paving the way for the progress of market trends in Latin America region.

Top Key Players and Market Share Insights:

The global micro data center market is highly competitive with major players providing solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the micro data center industry. Key players in the global micro data center market include-

- Schneider Electric (France)

- Hewlett Packard Enterprise (US)

- Zella DC (Australia)

- Enconnex (US)

- Dataracks (UK)

- Dell Technologies (US)

- Rittal GmbH & Co. KG (Germany)

- Vertiv (US)

- Panduit (US)

- Stulz (US)

- Huawei (China)

- Eaton (Ireland)

Recent Industry Developments :

Product Launch

- In October 2024, Zella DC launched Zella Outback, an advanced outdoor micro data center, building upon their previous Zella Hut design. It's available in three dimensions and is part of Zella DC's broader edge data center range, all powered by their Zella Sense automation platform.

Micro Data Center Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 18.03 Billion |

| CAGR (2025-2032) | 17.9% |

| By Component |

|

| By Rack Unit |

|

| By Enterprise Size |

|

| By Application |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Micro Data Center market? +

The Micro Data Center market is estimated to reach over USD 18.03 Billion by 2032 from a value of USD 5.58 Billion in 2024 and is projected to grow by USD 6.36 Billion in 2025, growing at a CAGR of 17.9% from 2025 to 2032.

What specific segmentation details are covered in the Micro Data Center report? +

The micro data center report includes specific segmentation details for component, rack unit, enterprise size, application, end user, and regions.

Which is the fastest segment anticipated to impact the market growth? +

In the micro data center market, edge computing is the fastest-growing segment during the forecast period.

Who are the major players in the micro data center market? +

The key participants in the micro data center market are Schneider Electric (France), Hewlett Packard Enterprise (US), Rittal GmbH & Co. KG (Germany), Vertiv (US), Panduit (US), Stulz (US), Eaton (Ireland), Zella DC (Australia), Enconnex (US), Dataracks (UK), Dell Technologies (US), Huawei (China) and others.

What are the key trends in the micro data center market? +

The micro data center market is being shaped by several key trends including increasing demand for edge computing, the proliferation of IoT devices, the need for low-latency applications, and the growing focus on modular, scalable, and energy-efficient infrastructure solutions.