- Summary

- Table Of Content

- Methodology

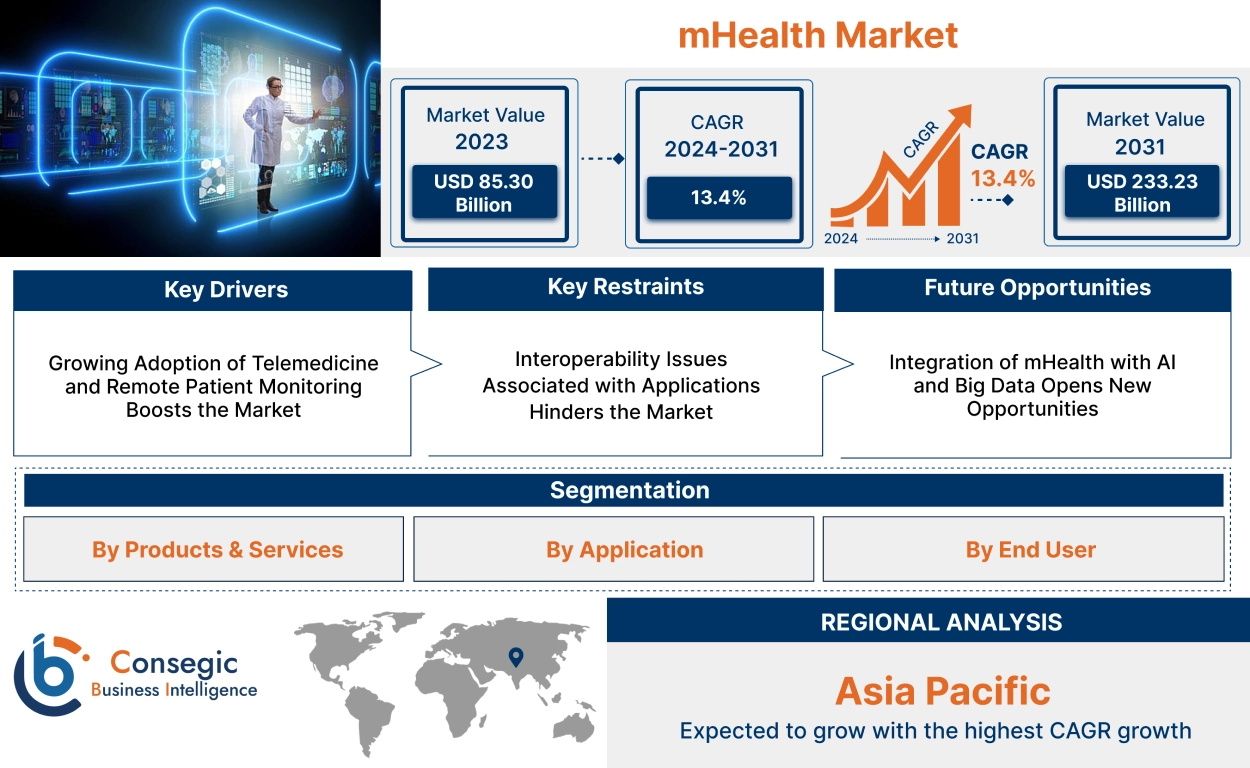

mHealth Market Size:

mHealth Market size is estimated to reach over USD 233.23 Billion by 2031 from a value of USD 85.30 Billion in 2023 and is projected to grow by USD 95.21 Billion in 2024, growing at a CAGR of 13.4% from 2024 to 2031.

mHealth Market Scope & Overview:

Mobile Health, commonly referred to as mHealth, encompasses the use of mobile and wireless technologies to support healthcare practices. This includes health-related mobile applications (apps) and wearable devices that monitor health indicators. mHealth applications are vast and varied, addressing needs such as remote monitoring, health information access, telemedicine, chronic disease management, public health & education, etc. They often have user-friendly interfaces, and data security, collect data in real-time, are interoperable, and can be personalized. They are commonly used in industries like healthcare, pharmaceutical, insurance companies, public health organizations, corporate wellness programs, etc.

mHealth Market Insights:

mHealth Market Dynamics - (DRO) :

Key Drivers:

Growing Adoption of Telemedicine and Remote Patient Monitoring Boosts the Market

Telemedicine is the application of electronic communication technologies, like video conferences and apps, for remote clinical services. On the other hand, Remote Patient Monitoring uses devices and apps to control the condition of patients using their vital signs at a distance. Both of these methods belong to the mHealth trend, which uses mobile and wireless technologies to offer health services away from the healthcare provider.

This combination of technologies has made it easier and more convenient to deliver healthcare, particularly when it comes to chronic illnesses, routine check-ups, and visiting the doctor for follow-up consultations. The easy access to medical professionals and the health monitoring done through mobile health tools are the primary reasons why they are so popular, the latter especially during the COVID-19 pandemic when physical visits were not possible.

- For instance, mySugr apps enable users to track their glucose levels, receive medication reminders, and communicate with healthcare providers remotely.

Thus, Remote Patient Monitoring (RPM) and the adoption of telemedicine drive the growth of the market.

Rising Focus on Preventive Healthcare Spurs the Market

Preventive healthcare is the care that focuses on doing things to prevent diseases and maintain good health, rather than just curing an illness if one occurs. Mobile health technologies are the ways that give individuals the power to be in charge of their health and the tools they need to participate.

mHealth innovation makes available functions such as health monitoring, personalized health assessments, reminders for check-ups and vaccinations, and information for medical purposes. The preventive approach is a perfect match for the aspirants of preventive health care, and mHealth has thereby been irreplaceable to the broader healthcare sector.

- For instance Fitbit helps users track their diet, exercise, and overall wellness. These apps provide users with insights into their daily habits, set health goals, and offer personalized recommendations to improve their lifestyles.

Since these devices aid in preventing chronic diseases by providing preventing healthcare they drive the global mHealth market growth.

Key Restraints :

Interoperability Issues Associated with Applications Hinders the Market

Interoperability is the ability of various healthcare systems, applications, and devices to communicate, share, and use data most efficiently. Such problems come up when mobile health applications or devices/ gadgets or even the already-existing healthcare systems are not able to integrate electronic health records and health information systems properly. These bumps in the road cause the interruption of the fast communication of data between patients, healthcare providers, and various healthcare facilities, resulting in data isolation and possible breakdowns in patient care.

Therefore, it can be concluded that issues related to interoperability within applications can restrict market growth.

Future Opportunities :

Integration of mHealth with AI and Big Data Opens New Opportunities

AI, big data, and mobile health(ABMM) are the current buzzwords in the tech world with the large chunks of data fetched by the mHealth gadgets and applications processed through AI algorithms, resulting in predictive analytics, health tracking, and more individualized care, making life the most calm. Big data analytics algorithms can identify the patients' conditions from different sources of health data and offer them life-saving lessons on patient behavior, sickness progression, and treatment efficacy.

Owing to the largest amount of data processing and rapid technological development, AI systems have a chance to learn and develop targeted medicines and treatment plans. AI and big data intercepting mobile health applications can be used to an extent resembling personalized health recommendations, early identification of potential health problems, and the treatment of cognitive diseases and disorders.

- For instance, IBM Watson Health is an AI-powered app that analyzes a user's health data to predict the likelihood of developing chronic conditions like diabetes or heart disease, allowing for early intervention.

Thus, big data analytics can help healthcare providers understand population health trends and tailor public health initiatives accordingly.

mHealth Market Segmental Analysis :

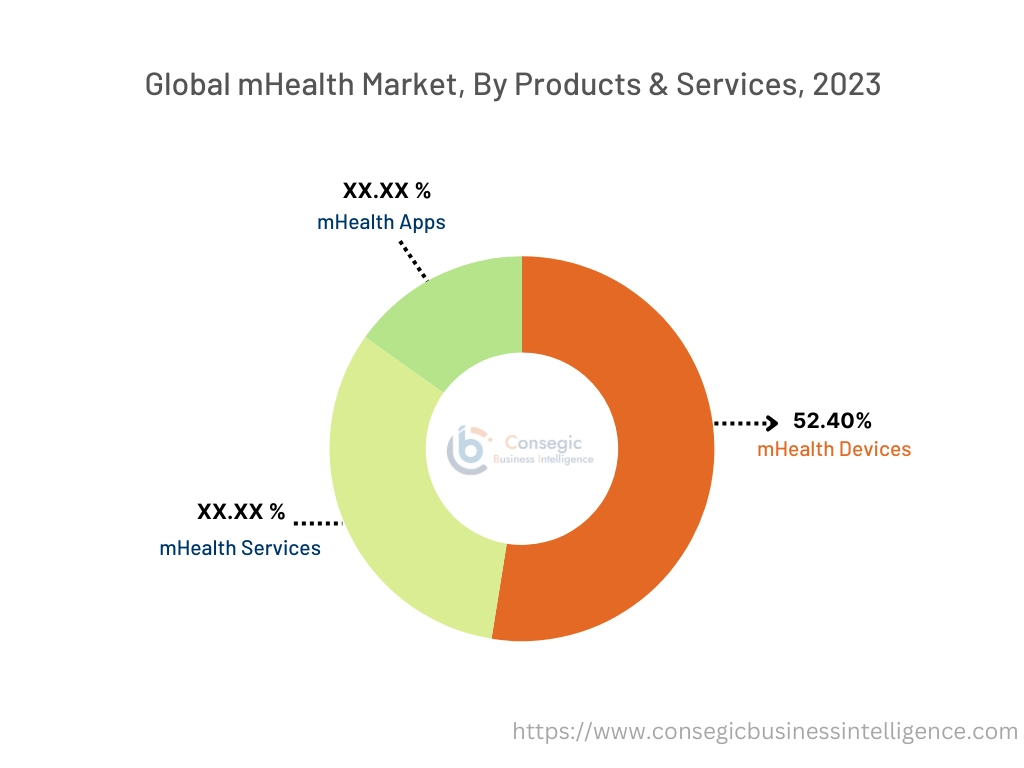

By Products & Services:

Based on Products & Services, the mHealth Market has been trifurcated into mHealth Devices (Wearable Fitness Sensor Devices, Blood Pressure Monitors, Blood Glucose Monitors, Apnea and Sleep Monitors, Neurological Monitors, Cardiac Monitors, Heart Rate Meters, Pulse Oximetry, and Others), mHealth Services (Treatment Services, Diagnostic Services, Prevention Services, Monitoring Services, Others), and mHealth Apps (Remote Monitoring Apps, Medical Apps, Fitness Apps, and Diagnostic Apps).

Trends in the Products & Services:

- Platforms that facilitate the integration of data from various mHealth apps and wearable devices with EHR systems are becoming essential. They help to improve data accuracy and accessibility for healthcare providers.

- Digital therapeutics for chronic diseases, such as apps providing structured therapeutic programs for diabetes or cardiovascular health, are emerging. These programs often use data analytics to personalize treatment.

The mHealth Devices segment accounted for the largest revenue of 52.40% in the year 2023 of the overall mHealth market share.

- This is driven by the increasing adoption of mobile health technologies and applications across various sectors of the healthcare industry.

- Key factors contributing include the widespread use of smartphones and mobile devices, advancements in mobile technology, and the rising demand for remote healthcare services.

- The COVID-19 pandemic further accelerated the adoption of mHealth devices, as healthcare providers and patients sought safe and convenient alternatives to in-person consultations.

- The prominence underscores the sector's potential to revolutionize healthcare delivery by making it more accessible, efficient, and patient-centered.

- For instance, EOFlow by Medtronic is a wearable insulin patch maker that utilizes specialized microfluidic technology intended for administering insulin accurately and dependably while reducing the chance of insulin blockage. It is accompanied by a corresponding smartphone app that enables users to oversee and manage the patch from their phone.

- Thus, the market analysis concludes that the devices segment is driving the mHealth market trends.

The mHealth Apps segment is anticipated to register the fastest CAGR during the forecast period.

- The app's rapid expansion is driven by several key factors such as increasing smartphone penetration, advancements in mobile technology, growing awareness of preventive healthcare, integration with AI and Big Data, and support from healthcare providers.

- This trend is expected to continue as technology evolves and consumer demand for accessible and personalized healthcare solutions increases.

- For instance, MyFitnessPal allows users to track their diet and exercise, providing personalized feedback and insights based on their health goals. The app's extensive database of foods and exercises, combined with features like goal tracking and community support, has made it a popular choice for individuals looking to manage their health proactively.

- Therefore, the apps segment is anticipated to boost mHealth market opportunities during the forecast period.

By Application:

Based on application, the mHealth market has been segmented into Remote Monitoring, Diagnostics and Treatment, Disease and Epidemic Outbreak Tracking, Communication and Training, Education and Awareness, and Others.

Trends in the application:

- Modern telemedicine apps now offer features like AI-driven triage, integration with Electronic Health Records (EHR), and tools for managing patient flow and care coordination.

The remote monitoring segment accounted for the largest revenue share in 2023.

- Remote monitoring involves using technology to track patients' health metrics and vital signs from a distance, allowing healthcare providers to observe, assess, and manage patients' conditions without requiring physical visits.

- This method often employs wearable devices, mobile apps, and connected sensors to collect real-time data on parameters such as heart rate, glucose levels, and blood pressure.

- Remote monitoring plays a crucial role by leveraging mobile devices and applications to deliver continuous health monitoring and management. Mobile health solutions enable patients to share their health data instantly with healthcare professionals, facilitating timely interventions and personalized care based on real-time insights.

- Factors for the growth of remote monitoring include increased demand for chronic disease management, advancements in technology, healthcare cost reduction, increased adoption of telehealth, regulatory and reimbursement support, etc.

- For instance, in 2023 Dexcom, a leading provider of continuous glucose monitoring (CGM) systems. Dexcom's CGM systems, include devices and mobile apps for monitoring blood glucose levels.

- Thus, the market analysis concludes that the remote monitoring segment is driving the mHealth market demand.

The diagnostics and treatment segment is anticipated to register the fastest CAGR during the forecast period.

- Mobile health apps and devices can facilitate remote diagnostic tests, analyze health data, and deliver tailored treatment plans.

- This integration allows for more accessible, timely, and personalized healthcare, improving patient outcomes and enabling continuous monitoring.

- The key trends and developments in this sector such as advancements in diagnostic technology, increased demand for personalized medicine, integration with AI and Machine Learning, expansion of digital therapeutics, growing adoption of remote diagnostics, and more promote the segment.

- For instance, Abbott's FreeStyle Libre system is a continuous glucose monitoring (CGM) technology. The FreeStyle Libre system provides real-time glucose monitoring and diagnostic data for diabetes management. Its innovative approach to diagnostics and treatment has positioned it as a leader in the market, reflecting the segment's rapid growth.

- Therefore, the diagnostics and treatment segment is anticipated to boost mHealth market opportunities during the forecast period.

By End User:

Based on end users, mHealth Market has been segmented into Patients, Providers, Payers, and others.

Trends in the End User:

- Insurance providers are recognizing the value of mobile health solutions in improving patient outcomes and reducing costs. Many insurers are now covering remote monitoring and telemedicine services, and offering incentives for the use of health apps and wearables.

The provider's segment accounted for the largest revenue share in 2023.

- Several key factors influencing the growing adoption of technologies among healthcare providers include integration with electronic health records (EHRs), utilization of remote monitoring tools, enhanced data analytics and AI, support for population health management, and more.

- For instance, Samsung made significant investments, particularly through partnerships and research initiatives with leading institutions. The company launched the, Open Innovation Initiative, collaborating with the Massachusetts Institute of Technology (MIT) Media Lab, Brigham & Women's Hospital, Tulane University School of Medicine, and Samsung Medical Center. It focuses on sleep monitoring and improvement, resilience and frailty research, cardiovascular disease monitoring, and multi-domain healthcare approaches.

- Therefore, the providers segment is driving the mHealth market demand.

The patient segment is anticipated to register the fastest CAGR during the forecast period

- Factors driving the growth of the patient segment include increased use of health and wellness apps, remote diagnostics and monitoring, interest in preventive health, enhanced access to telehealth services, integration with wearable devices, and more.

- For instance, Fitbit's devices, including the Fitbit Charge and Fitbit Versa, provide users with a range of health monitoring features such as heart rate tracking, sleep analysis, and activity monitoring.

- Thus, the market analysis concludes that the patient segment is driving the mHealth market trends.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

North America is estimated to reach over USD 99.82 Billion by 2031 from a value of USD 36.26 Billion in 2023. The mobile health industry is mainly driven by its deployment in healthcare providers, the pharmaceutical industry, insurance companies, and other industries.

The region's dominance is attributed to several factors, including advanced healthcare infrastructure, high smartphone penetration, and a growing focus on digital health innovations. The strong presence of key market players and supportive government initiatives further bolster the mHealth market in North America.

The mHealth market in North America is substantial, with significant investments in digital health startups and innovations. The market is expected to grow at a robust pace, driven by continuous advancements in mobile health technologies and increasing consumer interest in convenient healthcare solutions.

- Teladoc Health is a leading telemedicine provider in the United States, offering a range of services, including virtual consultations, remote patient monitoring, and mental health services.

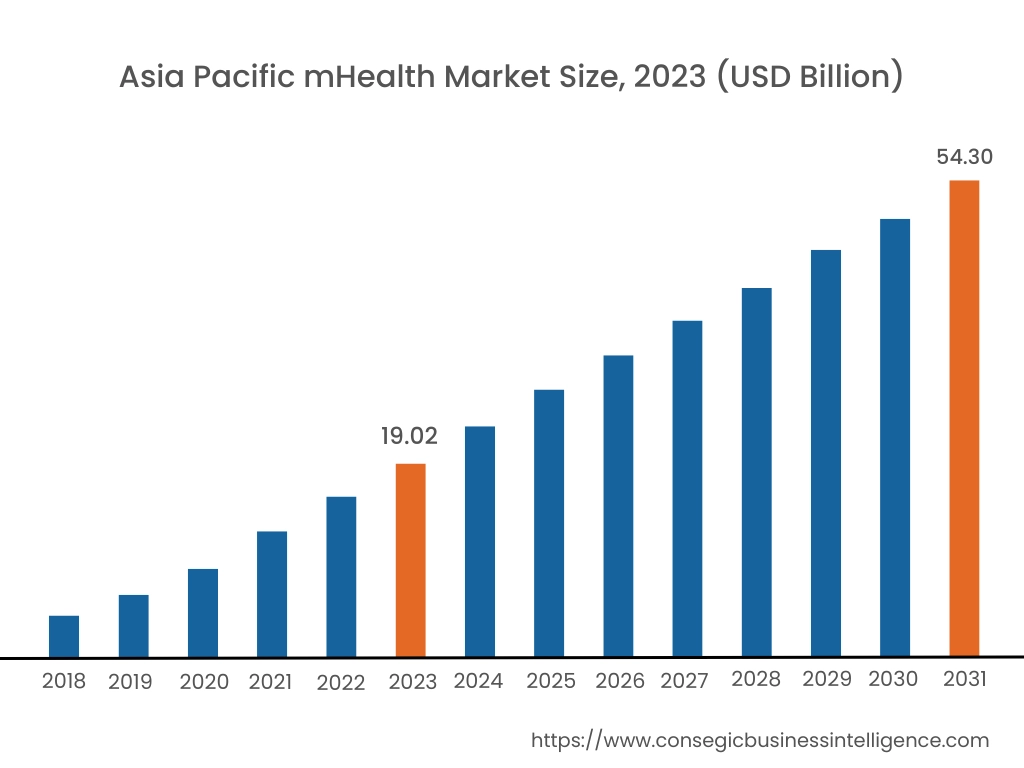

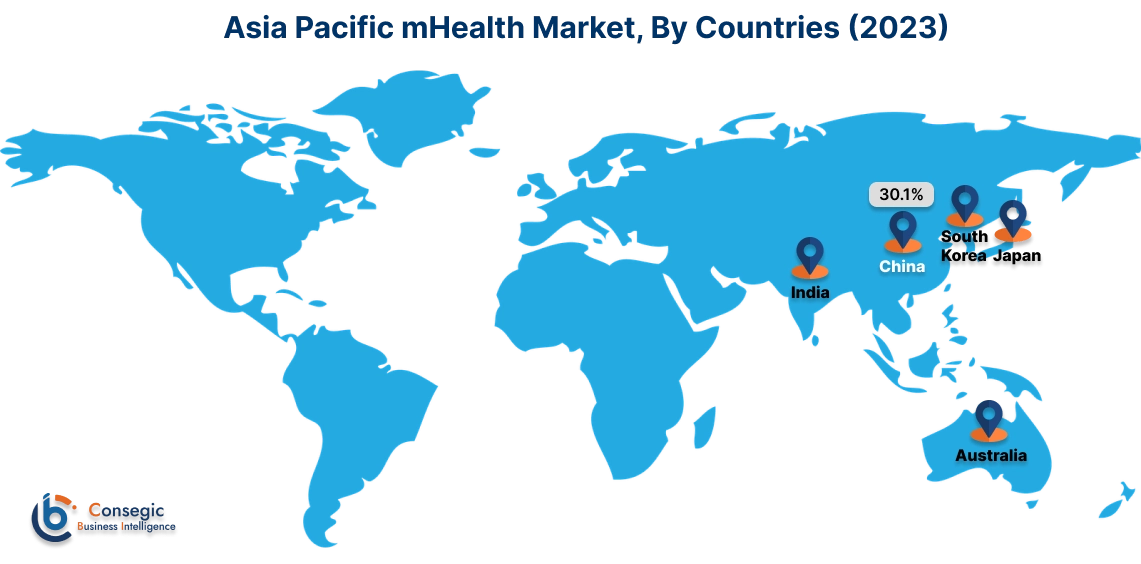

Asia Pacific region was valued at USD 19.02 Billion in 2023. Moreover, it is projected to reach over USD 54.30 Billion by 2031. Out of this, China accounted for the maximum revenue share of 30.1%.

The Asia Pacific region is experiencing rapid growth in the mHealth industry, driven by factors such as increasing smartphone penetration, rising healthcare awareness, and significant investments in digital health infrastructure. Countries like China, India, Japan, and South Korea are at the forefront of this growth, leveraging technological advancements to enhance healthcare delivery and accessibility.

- Practo offers a wide range of services, including online doctor consultations, appointment scheduling, and health record management. The app has gained significant traction due to the increasing demand for convenient and accessible healthcare services in India. Practo's success is supported by the Indian government's push towards digital health initiatives, such as the National Digital Health Mission, which aims to digitize healthcare services across the country.

As per the mHealth market analysis, Europe is anticipated to witness a substantial rise, driven by the increasing adoption of mHealth technologies across various sectors, particularly the healthcare sector. The region's mature healthcare infrastructure, combined with supportive regulatory frameworks, is fostering the integration of mHealth solutions to enhance patient care and streamline clinical processes.

The Middle East, Africa, and Latin America are expected to grow at a considerable rate in the mHealth market, driven by increasing investments in digital infrastructure and healthcare services across countries like Brazil and the UAE.

Top Key Players & Market Share Insights:

The mHealth market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the mHealth industry include-

- Koninklijke Philips N.V. (Netherlands)

- International Business Machines Corporation (USA)

- Apple Inc. (USA)

- Google LLC (USA)

- Samsung Electronics Co., Ltd. (South Korea)

- Medtronic (USA)

- Qualcomm Life (USA)

- FitBit, Inc.

- Withings S.A. (France)

- Cerner Corporation (USA)

Recent Industry Developments :

Product Launches:

- In September 2023, Apple, which was initially announced in late 2019, to bolster its health and wellness technology offerings with wearable health-tracking solutions.

- In August 2023, Fitbit introduced the Charge 6, featuring improved GPS capabilities and expanded health monitoring functions, including more detailed sleep tracking and stress management tools.

Partnerships & Collaborations:

- In April 2024, Samsung and Google Health, announced a strategic partnership to integrate Google's health services with Samsung's wearable devices, enhancing the health and fitness tracking capabilities of their products.

mHealth Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 233.23 Billion |

| CAGR (2024-2031) | 13.4% |

| By Products & Services |

|

| By Application |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the mHealth Market? +

The mHealth market size is estimated to reach over USD 233.23 Billion by 2031 from a value of USD 85.30 Billion in 2023 and is projected to grow by USD 95.21 Billion in 2024, growing at a CAGR of 13.4% from 2024 to 2031.

Which is the fastest-growing region in the mHealth Market? +

Asia-Pacific is the region experiencing the most rapid growth in mHealth Market.

What specific segmentation details are covered in the mHealth report? +

The mHealth report includes specific segmentation details for products and services, application, end-user, and region.

Who are the major players in the mHealth market? +

The key players in the mHealth market are Koninklijke Philips N.V. (Netherlands), International Business Machines Corporation (USA), Medtronic (USA), Qualcomm Life (USA), Apple Inc. (USA), Google LLC (USA), Samsung Electronics Co., Ltd. (South Korea), FitBit, Inc., Withings S.A. (France), and Cerner Corporation (USA).