- Summary

- Table Of Content

- Methodology

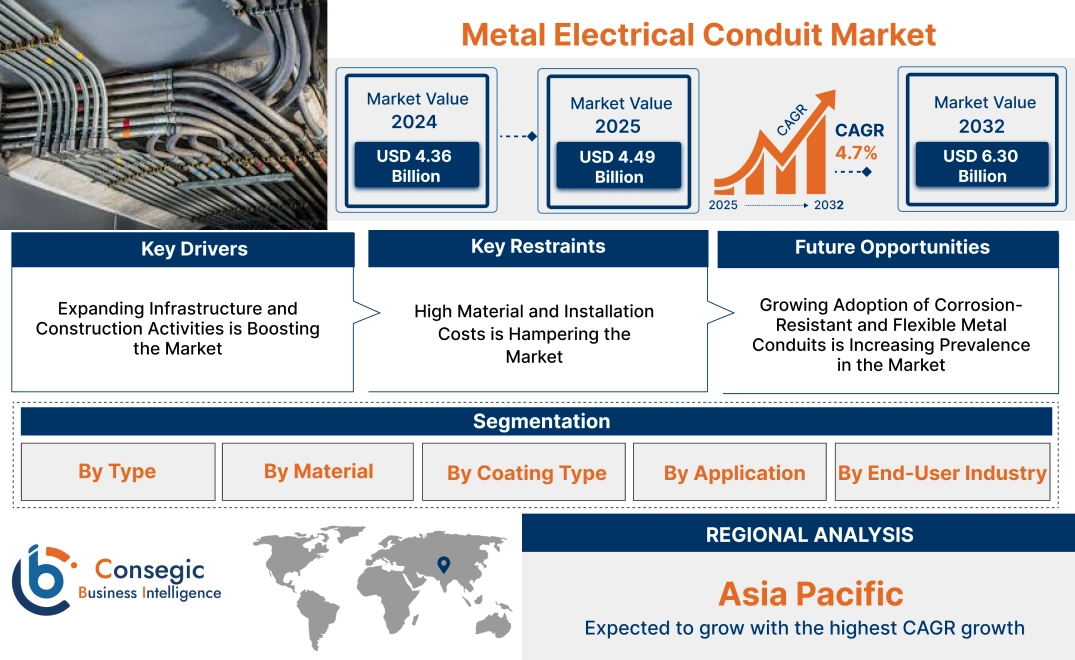

Metal Electrical Conduit Market Size:

Metal Electrical Conduit Market size is estimated to reach over USD 6.30 Billion by 2032 from a value of USD 4.36 Billion in 2024 and is projected to grow by USD 4.49 Billion in 2025, growing at a CAGR of 4.7% from 2025 to 2032.

Metal Electrical Conduit Market Scope & Overview:

The metal electrical conduit industry focuses on protective tubing systems designed to house and safeguard electrical wiring in residential, commercial, and industrial applications. These conduits, typically made from galvanized steel, aluminum, or stainless steel, provide mechanical protection, durability, and fire resistance while facilitating efficient wiring management. Key types of metal electrical conduits include rigid metal conduit (RMC), electrical metallic tubing (EMT), and flexible metal conduit (FMC), each suited for specific installation needs.

Key characteristics of metal electrical conduits include high strength, corrosion resistance, and compliance with electrical safety standards. The benefits include enhanced protection against physical damage, improved fire safety, and long-term reliability in electrical installations.

Applications span power distribution, telecommunications infrastructure, industrial automation, and commercial building wiring systems. End-users include electrical contractors, construction firms, utility providers, and manufacturing industries, driven by increasing urbanization, rising investments in infrastructure projects, and growing emphasis on electrical safety and regulatory compliance.

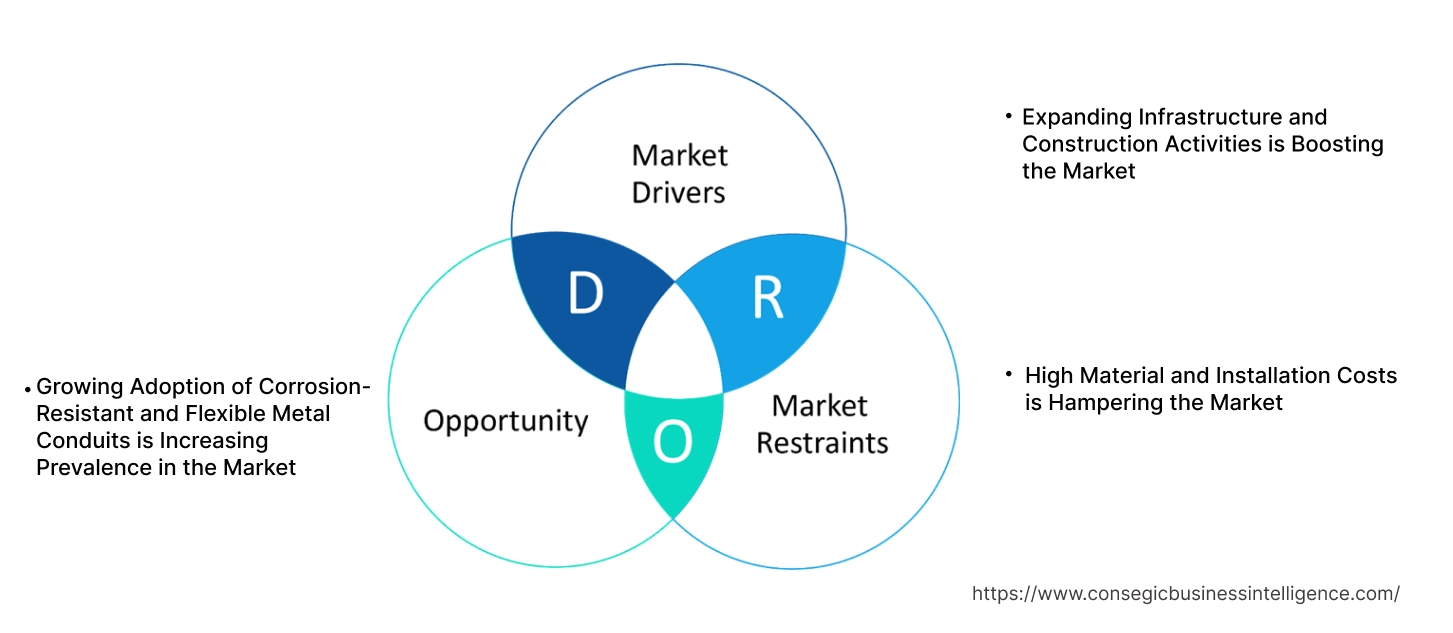

Metal Electrical Conduit Market Dynamics - (DRO) :

Key Drivers:

Expanding Infrastructure and Construction Activities is Boosting the Market

The growth of infrastructure development and construction activities is a major driver of the market. Increasing urbanization and the expansion of commercial, residential, and industrial projects have fueled the demand for reliable electrical systems, where metal conduits play a critical role in protecting electrical wiring from physical damage, moisture, and fire hazards. The rising adoption of metal conduits in high-risk environments such as data centers, healthcare facilities, and manufacturing plants further drives metal electrical conduit market demand. Additionally, stringent building codes and electrical safety regulations are pushing contractors and engineers toward durable and fire-resistant conduit solutions, favoring metal over plastic alternatives.

Key Restraints:

High Material and Installation Costs is Hampering the Market

One of the primary challenges in the metal electrical conduit market is the high cost of raw materials, particularly steel and aluminum, which are commonly used in conduit manufacturing. Fluctuations in metal prices due to supply chain disruptions and global economic conditions can significantly impact production costs. Additionally, metal conduits require specialized tools and labor for installation, increasing overall project expenses compared to non-metallic alternatives like PVC conduits. These cost-related barriers may limit market adoption, particularly in cost-sensitive construction projects and emerging markets where budget constraints are a concern.

Future Opportunities:

Growing Adoption of Corrosion-Resistant and Flexible Metal Conduits is Increasing Prevalence in the Market

The development of corrosion-resistant and flexible metal conduits presents significant growth opportunities for the market. With the rising need for electrical systems in harsh and hazardous environments, such as offshore platforms, chemical processing plants, and underground installations, manufacturers are investing in galvanized steel, stainless steel, and aluminum-coated conduits that offer enhanced durability and longevity. Additionally, the trends for flexible metal conduits (FMC) is increasing in modern construction projects where adaptability and ease of installation are critical. These advanced conduit solutions are particularly valuable in retrofitting older buildings and smart city infrastructure, where electrical upgrades require flexible and resilient conduit systems.

These dynamics highlight the increasing reliance on metal electrical conduits for safe and durable electrical wiring protection, particularly in industrial and commercial applications. While cost challenges persist, innovations in corrosion-resistant materials and flexible conduit solutions are creating new growth in metal electrical conduit market opportunities for manufacturers and contractors in the evolving construction landscape.

Metal Electrical Conduit Market Segmental Analysis:

By Type:

Based on type, the market is segmented into Rigid Metal Conduit (RMC), Intermediate Metal Conduit (IMC), Electrical Metallic Tubing (EMT), Flexible Metal Conduit (FMC), and Liquid-Tight Flexible Metal Conduit (LFMC).

The Rigid Metal Conduit (RMC) segment accounted for the largest revenue of metal electrical conduit market share in 2024.

- RMC offers superior protection against mechanical damage and environmental hazards, making it ideal for heavy-duty industrial and commercial applications.

- Its high durability and corrosion resistance support widespread adoption in harsh environments, such as energy & utility infrastructure.

- Increasing safety regulations in electrical installations drive trends for RMC in underground and exposed wiring.

- Expanding use in large-scale infrastructure projects, including smart cities and power grids, strengthens market dominance.

The Liquid-Tight Flexible Metal Conduit (LFMC) segment is anticipated to register the fastest CAGR during the forecast period.

- LFMC provides enhanced moisture resistance, making it ideal for wet locations, outdoor installations, and industrial machinery wiring.

- Increasing adoption in data centers and IT infrastructure for secure and flexible cabling solutions fuels metal electrical conduit market trends.

- Rising focus on efficient electrical installations in renewable energy projects, such as solar and wind farms, supports segment expansion.

- Advancements in flexible conduit materials improve strength, longevity, and ease of installation, enhancing market potential as per the analysis.

By Material:

Based on material, the market is segmented into steel and aluminum.

The steel segment accounted for the largest revenue share in 2024.

- Steel conduits provide high mechanical strength, fire resistance, and durability, making them suitable for heavy-duty applications.

- Increasing use in commercial and industrial buildings for secure electrical wiring enhances segment metal electrical conduit market growth.

- Expanding trends for steel conduits in underground wiring due to their superior corrosion resistance strengthens market presence.

- Advancements in galvanized and coated steel conduits improve performance and longevity, further driving adoption.

The aluminum segment is anticipated to register the fastest CAGR during the forecast period.

- Aluminum conduits are lightweight, corrosion-resistant, and cost-effective, making them ideal for applications in energy & utilities and infrastructure sectors.

- Growing adoption in coastal and high-moisture environments where corrosion resistance is critical supports this segment.

- Rising investments in lightweight electrical wiring solutions for modern commercial buildings boost metal electrical conduit market demand for aluminum conduits.

- Advancements in aluminum alloy manufacturing improve mechanical strength and flexibility, enhancing adoption across various industries.

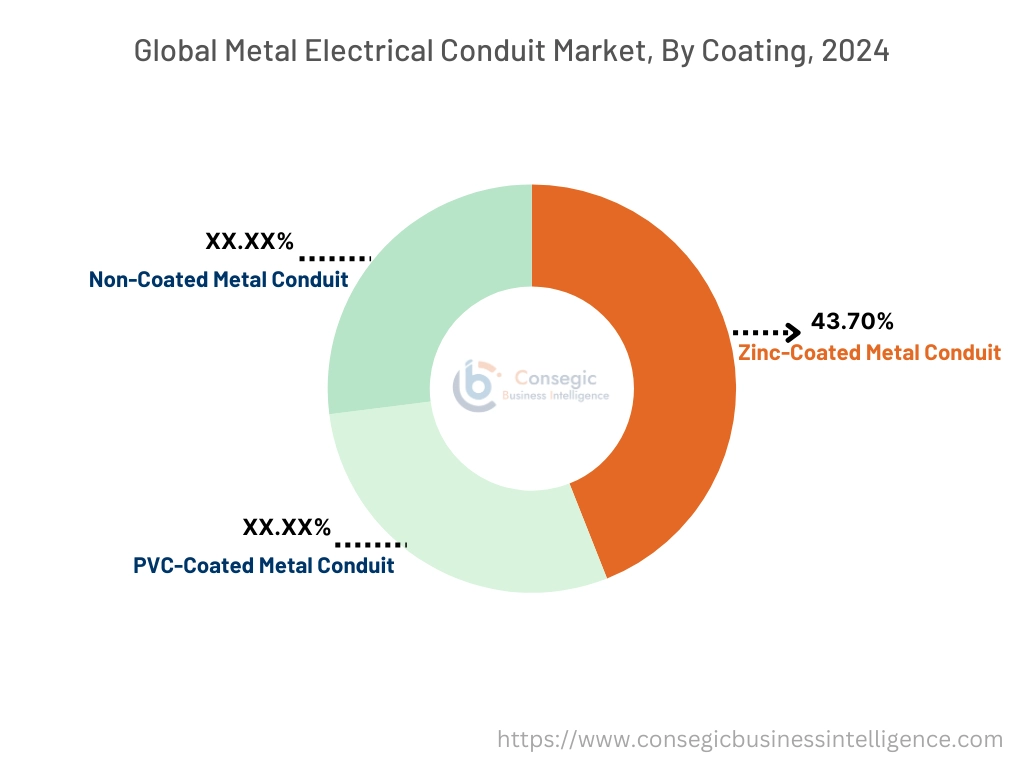

By Coating Type:

Based on coating type, the market is segmented into PVC-coated metal conduit, zinc-coated metal conduit, and non-coated metal conduit.

The zinc-coated metal conduit segment accounted for the largest revenue of metal electrical conduit market share of 43.70% in 2024.

- Zinc-coated conduits provide excellent corrosion resistance, making them suitable for outdoor and industrial applications.

- Increasing metal electrical conduit market trends in underground and exposed wiring installations support segment dominance.

- Growing adoption in critical infrastructure projects, such as transportation networks and smart grids, fuels demand.

- Advancements in hot-dip and electro-galvanized coating technologies enhance the durability of zinc-coated conduits.

The PVC-coated metal conduit segment is anticipated to register the fastest CAGR during the forecast period.

- PVC coatings enhance moisture and chemical resistance, making them ideal for extreme weather conditions and hazardous environments.

- Rising adoption in energy & utility infrastructure, including oil & gas and power plants, boosts demand.

- Expanding use in commercial buildings and data centers for improved cable insulation and protection supports segment metal electrical conduit market growth.

- Technological advancements in PVC formulations improve heat resistance and environmental sustainability, driving further adoption.

By Application:

Based on application, the market is segmented into building wiring, underground wiring, industrial machinery, data centers & IT infrastructure, and others.

The building wiring segment accounted for the largest revenue share in 2024.

- Increasing urbanization and construction activities drive surge for safe and reliable electrical wiring solutions.

- Rising adoption of metal conduits in commercial and residential buildings for fire-resistant wiring installations enhances market presence.

- Expanding government regulations promoting high-quality electrical infrastructure supports segment dominance.

- Growing use of smart building systems requiring advanced wiring protection further propels demand.

The data centers & IT infrastructure segment is anticipated to register the fastest CAGR during the forecast period.

- Rising global investments in data centers for cloud computing, AI, and IoT applications increase trends for secure wiring solutions.

- Metal conduits provide enhanced protection against electromagnetic interference (EMI), ensuring stable data transmission.

- Increasing need for flexible and liquid-tight conduits to protect critical IT cabling systems fuels adoption.

- Technological advancements in conduit materials and coatings improve efficiency and longevity in data center environments.

By End-User Industry:

Based on end-user industry, the market is segmented intoresidential, commercial, industrial, energy & utilities, and infrastructure.

The industrial segment accounted for the largest revenue share in 2024.

- Industries such as manufacturing, chemicals, and oil & gas require robust electrical conduit systems for high-power machinery and hazardous environments.

- Growing focus on workplace safety and compliance with electrical wiring standards supports segment growth.

- Expanding automation in industrial facilities increases the need for reliable and durable conduit solutions.

- Investments in energy-efficient and high-performance electrical infrastructure further drive trends.

The energy & utilities segment is anticipated to register the fastest CAGR during the forecast period.

- Rising investments in renewable energy projects, including solar and wind power plants, drive advancement for corrosion-resistant conduits.

- Metal conduits provide superior protection against environmental conditions in high-voltage transmission lines and substations.

- Increasing electrification projects in emerging markets boost adoption of metal conduits for safe power distribution.

- Expanding use of smart grid technology and power management systems enhances market potential.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

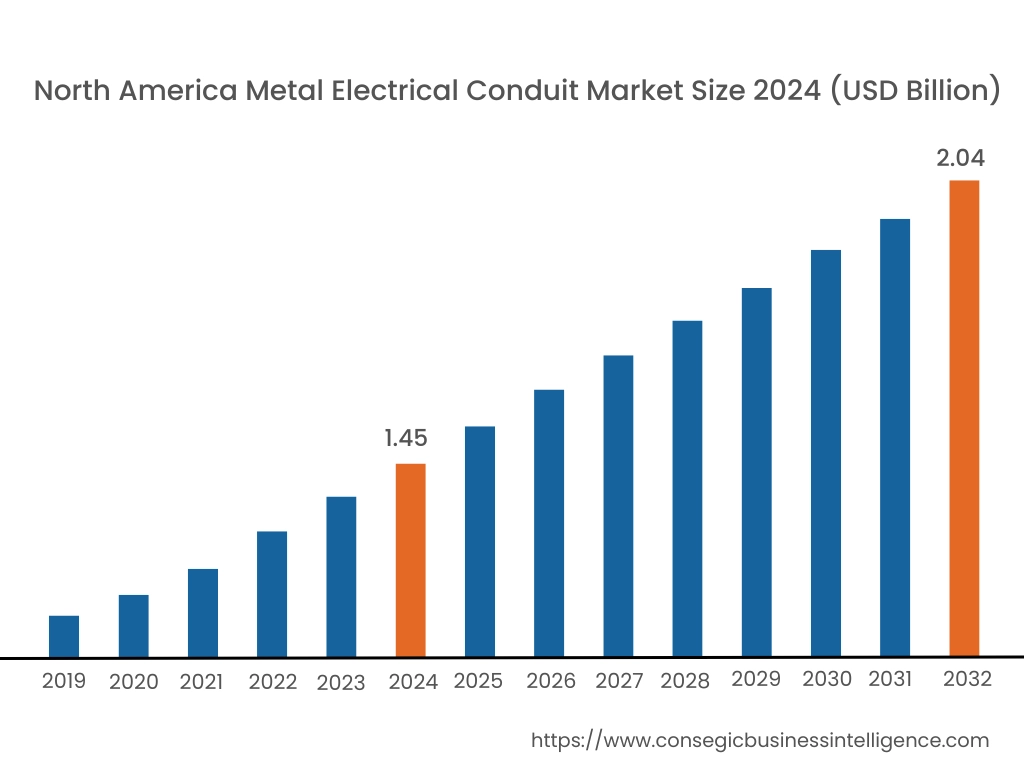

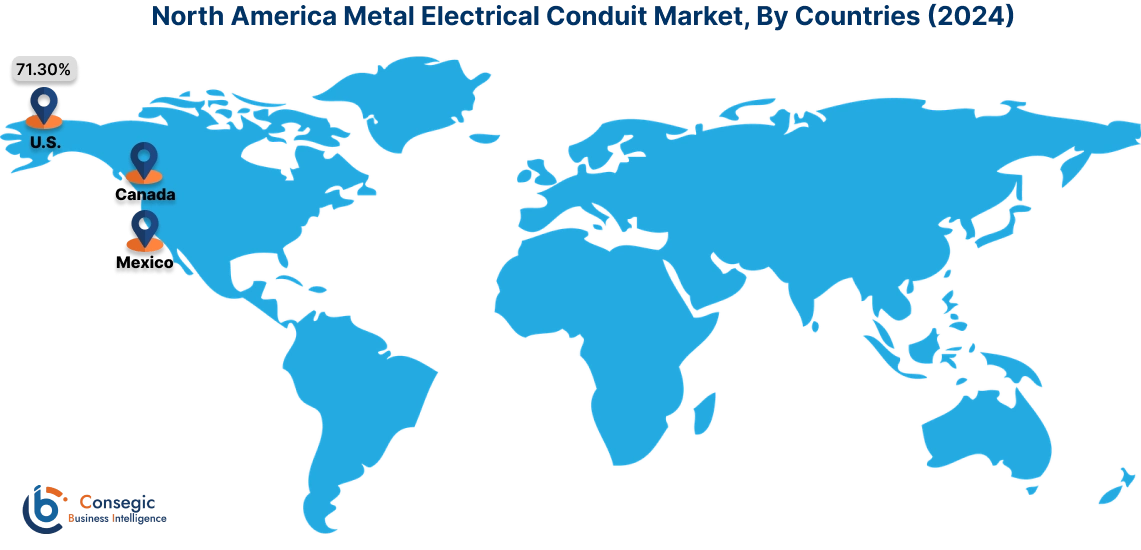

In 2024, North America was valued at USD 1.45 Billion and is expected to reach USD 2.04 Billion in 2032. In North America, the U.S. accounted for the highest share of 71.30% during the base year of 2024. North America holds a substantial share of the global metal electrical conduit market, driven by increasing investments in infrastructure development, stringent safety regulations, and rising trends for durable electrical wiring solutions. The U.S. leads the region with strong adoption of rigid and flexible metal conduits in commercial and industrial construction. The enlargement of data centers and smart buildings further contributes to market expansion. Canada follows with a growing demand for corrosion-resistant conduits in the energy and transportation sectors. Analysis highlights the region’s focus on fire-resistant and high-performance conduit systems to enhance electrical safety.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 5.1% over the forecast period. The metal electrical conduit market is fueled by rapid urbanization, increasing industrialization, and expanding construction activities in China, India, and Japan. China dominates the region with extensive infrastructure projects and a rising trends for robust electrical conduit solutions in commercial and residential construction. India’s focus on smart cities and industrial development supports the adoption of metal conduits in power distribution and high-rise buildings. Japan emphasizes precision-engineered conduit solutions for industrial automation and high-tech manufacturing. Regional metal electrical conduit market analysis suggests that increasing foreign investments in infrastructure are driving significant growth for metal electrical conduit market opportunities.

Europe is a significant market for metal electrical conduits, supported by stringent regulations on electrical safety, energy efficiency, and sustainable construction practices. Countries like Germany, the UK, and France are key contributors. Germany drives demand through its strong manufacturing sector and increasing deployment of metal conduits in renewable energy projects. The UK focuses on the integration of high-quality electrical wiring solutions in commercial and residential buildings, while France emphasizes industrial safety and underground cabling projects. The metal electrical conduit market analysis of the region points to an increasing shift toward galvanized and stainless steel conduits for enhanced durability in harsh environments.

The Middle East & Africa region is experiencing steady market expansion, driven by rising investments in energy infrastructure, commercial real estate, and industrial projects. Countries like Saudi Arabia and the UAE are adopting metal electrical conduits in large-scale construction projects, including airports, metro systems, and high-rise buildings. In Africa, South Africa is emerging as a key market, focusing on improving electrical safety in industrial and residential developments. Regional analysis points to challenges related to high material costs and limited local manufacturing capabilities, which impact overall market accessibility.

Latin America is an emerging market, with Brazil and Mexico leading the region. Brazil’s growing construction sector and increasing investments in power distribution systems drive metal electrical conduit market trends for durable conduit solutions. Mexico focuses on expanding industrial manufacturing and commercial infrastructure, boosting the need for rigid and flexible metal conduits. Analysis highlights that regional governments are prioritizing electrical safety standards, which is expected to enhance the adoption of high-performance conduit materials. However, economic uncertainties and inconsistent regulatory enforcement in some countries may slow metal electrical conduit market expansion.

Top Key Players and Market Share Insights:

The metal electrical conduit market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global metal electrical conduit market. Key players in the metal electrical conduit industry include -

- Atkore International (USA)

- Ocal, LLC (Nucor) (USA)

- General Electric Company (GE) (USA)

- Southwire Company, LLC (USA)

- Robroy Industries, Inc. (USA)

- Shanghai LINA Industrial Co., Ltd. (China)

- Thomas & Betts Corporation (USA)

- Penn Union (USA)

- Unitech Metal Industries (India)

- Western Tube and Conduit Corporation (USA)

Recent Industry Developments :

Innovations:

- In April 2024, BEP Surface Technologies launched BEP Solutions, an innovation arm designed to accelerate R&D in metal surface technology. This initiative focuses on using cutting-edge digital techniques and partnerships with governments, academic institutions, and businesses to tackle global challenges. This development signifies BEP's commitment to advancing the capabilities of metal surface technologies, potentially impacting industries such as water treatment, where ultrafiltration systems benefit from innovations in material science. BEP Solutions aims to provide enhanced metal surface solutions that could lead to more efficient and sustainable filtration technologies.

Metal Electrical Conduit Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 6.30 Billion |

| CAGR (2025-2032) | 4.7% |

| By Type |

|

| By Material |

|

| By Coating Type |

|

| By Application |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the current and projected size of the Metal Electrical Conduit Market? +

Metal Electrical Conduit Market size is estimated to reach over USD 6.30 Billion by 2032 from a value of USD 4.36 Billion in 2024 and is projected to grow by USD 4.49 Billion in 2025, growing at a CAGR of 4.7% from 2025 to 2032.

What are the key types of metal electrical conduits used in the market? +

The market is segmented into Rigid Metal Conduit (RMC), Intermediate Metal Conduit (IMC), Electrical Metallic Tubing (EMT), Flexible Metal Conduit (FMC), and Liquid-Tight Flexible Metal Conduit (LFMC). RMC held the largest market share in 2024 due to its superior mechanical protection and durability.

Which material dominates the Metal Electrical Conduit Market? +

Steel conduits accounted for the largest revenue share in 2024, driven by their high strength, fire resistance, and suitability for heavy-duty applications, while aluminum conduits are experiencing rapid growth due to their lightweight properties and corrosion resistance.

What factors are driving the growth of the Metal Electrical Conduit Market? +

Growth is driven by increasing urbanization, rising infrastructure development, stringent electrical safety regulations, and expanding industrial and commercial construction projects globally.