- Summary

- Table Of Content

- Methodology

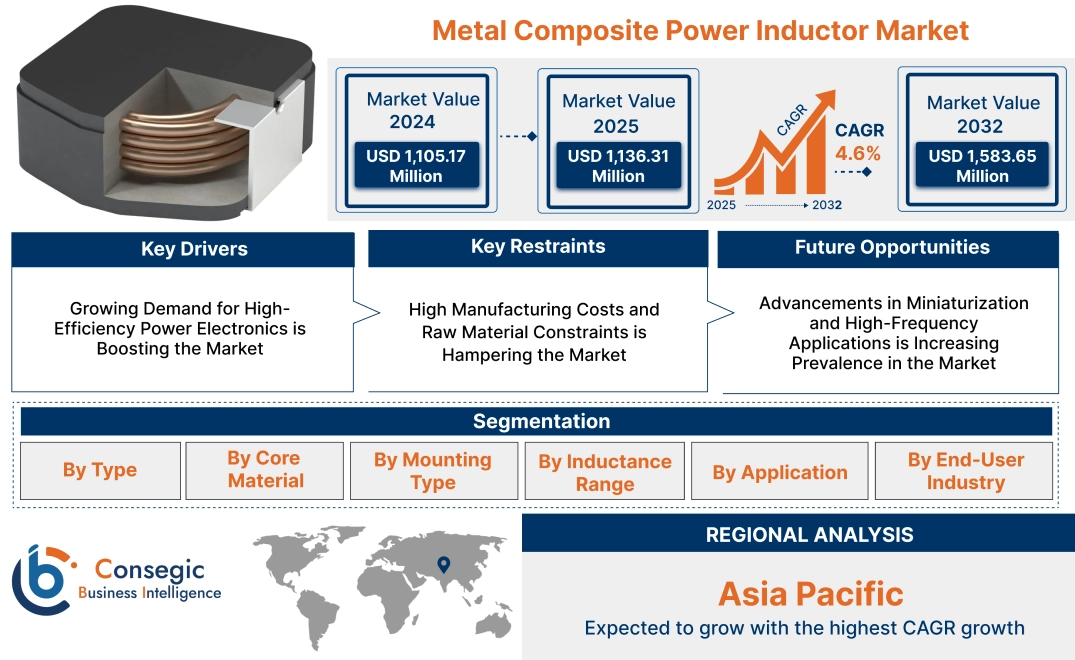

Metal Composite Power Inductor Market Size:

Metal Composite Power Inductor Market size is estimated to reach over USD 1,583.65 Million by 2032 from a value of USD 1,105.17 Million in 2024 and is projected to grow by USD 1,136.31 Million in 2025, growing at a CAGR of 4.6% from 2025 to 2032.

Metal Composite Power Inductor Market Scope & Overview:

The metal composite power inductor industry focuses on the production and application of inductors made from metal composite materials, offering superior efficiency and performance in power conversion and energy storage applications. These inductors are widely used in high-frequency power electronics, automotive powertrains, telecommunications, and industrial automation systems, where stable inductance, low core loss, and high current handling are essential.

Key characteristics of metal composite power inductors include high saturation current capability, excellent thermal stability, and compact form factors, making them ideal for miniaturized electronic devices. The benefits include enhanced energy efficiency, improved electromagnetic interference (EMI) suppression, and prolonged operational lifespan in demanding environments.

Applications span power management in consumer electronics, electric vehicles, renewable energy systems, and industrial power supplies. End-users include automotive manufacturers, consumer electronics companies, and industrial equipment producers, driven by increasing adoption of electric and hybrid vehicles, advancements in power electronics, and rising demand for energy-efficient components in next-generation electronic devices.

Metal Composite Power Inductor Market Dynamics - (DRO) :

Key Drivers:

Growing Demand for High-Efficiency Power Electronics is Boosting the Market

The increasing opportunities for high-efficiency power electronics in industries such as automotive, telecommunications, and consumer electronics is a major driver of the market. These inductors offer superior performance in terms of high current handling, low core loss, and thermal stability, making them essential in modern power circuits. The rising adoption of electric vehicles (EVs), 5G infrastructure, and energy-efficient power supplies has further fueled the market as manufacturers seek compact, reliable, and high-performance power management solutions. Additionally, advancements in semiconductor technologies and the increasing need for miniaturized components are driving the integration of metal composite power inductors in next-generation electronic devices.

Key Restraints:

High Manufacturing Costs and Raw Material Constraints is Hampering the Market

A significant challenge in the market is the high manufacturing cost of metal composite power inductors due to the complexity of material processing and precision engineering required. The production involves advanced magnetic materials, specialized coatings, and stringent quality control measures, increasing overall costs. Additionally, the fluctuating prices of raw materials such as iron-based alloys, ferrites, and rare earth metals impact production expenses. These cost-related factors limit the adoption of high-performance inductors in cost-sensitive applications, posing a challenge for metal composite power inductor market expansion, especially in emerging economies.

Future Opportunities :

Advancements in Miniaturization and High-Frequency Applications is Increasing Prevalence in the Market

The trends toward miniaturization and high-frequency applications present a significant opportunity for the market. With the growing applications for compact and energy-efficient electronic components, manufacturers are focusing on developing smaller, high-power-density inductors that maintain high performance even at elevated frequencies. Innovations in nanocrystalline materials and multilayer inductor designs are enabling power electronics to achieve improved efficiency and reduced electromagnetic interference (EMI). The expansion of IoT, wearable devices, and next-generation computing systems also creates new avenues for advanced power inductors, positioning manufacturers to capitalize on the evolving needs of high-speed and miniaturized electronics.

These market dynamics highlight the increasing demand for high-performance inductors in power electronics applications. While cost challenges remain a restraint, advancements in miniaturization, material science, and high-frequency power management technologies present significant opportunities for trends in innovation and metal composite power inductor market growth.

Metal Composite Power Inductor Market Segmental Analysis :

By Type:

Based on type, the market is segmented into shielded metal composite power inductors and unshielded metal composite power inductors.

The shielded metal composite power inductors segment accounted for the largest revenue of metal composite power inductor market share in 2024.

- Shielded inductors offer superior electromagnetic interference (EMI) suppression, making them ideal for high-frequency applications.

- Increasing adoption in compact electronic circuits, including DC-DC converters and automotive electronics, enhances market penetration.

- Advancements in shielding materials improve efficiency, durability, and thermal stability, strengthening their dominance.

- Growing trends for EMI-resistant components in industrial automation and telecommunications supports metal composite power inductor market trends.

The unshielded metal composite power inductors segment is anticipated to register the fastest CAGR during the forecast period.

- Unshielded inductors are preferred for cost-sensitive applications where EMI suppression is not a primary requirement.

- Increasing use in consumer electronics, such as smartphones and tablets, supports advancement for compact, lightweight solutions.

- Advancements in material engineering improve the performance and reliability of unshielded inductors.

- Expanding use in high-density power circuits drives adoption in emerging applications.

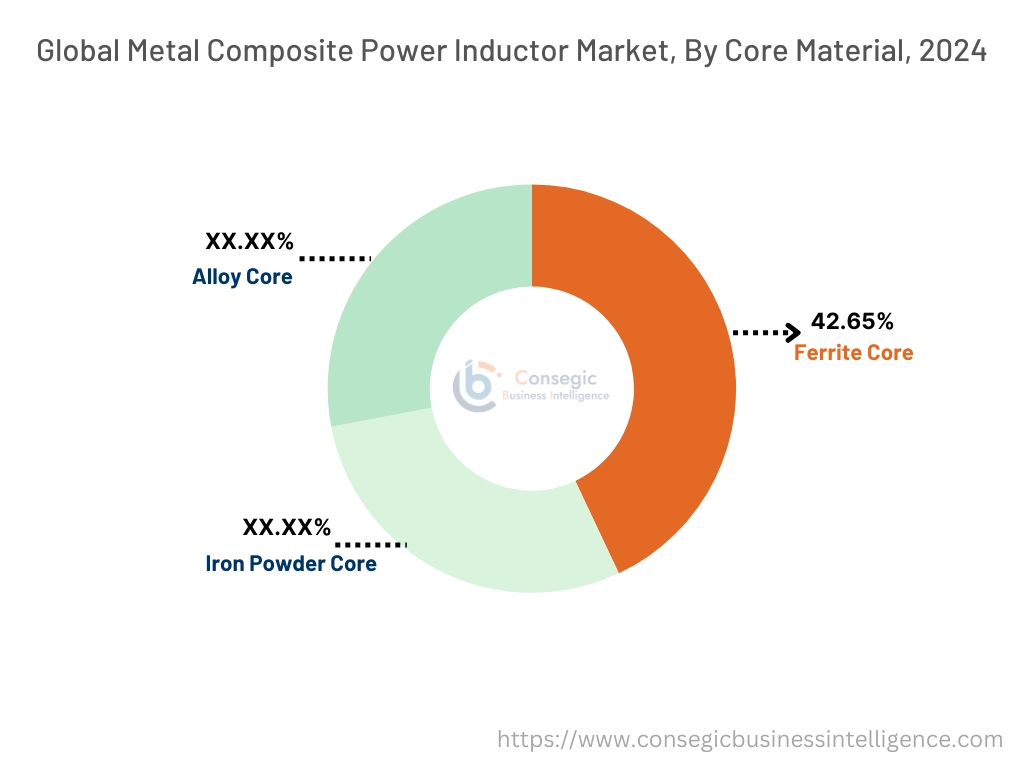

By Core Material:

Based on core material, the market is segmented into iron powder core, ferrite core, and alloy core.

The ferrite core segment accounted for the largest revenue share of 42.65% in 2024.

- Ferrite core inductors provide excellent high-frequency performance, making them widely used in telecommunications and power electronics.

- Increasing adoption in industrial automation and medical devices supports their market dominance.

- Advancements in ferrite materials improve energy efficiency and reduce core losses in high-frequency applications.

- Expanding use of electric vehicles (EVs) and renewable energy systems further strengthens its surge in the market place.

The alloy core segment is anticipated to register the fastest CAGR during the forecast period.

- Alloy core inductors offer high current handling capabilities and low core losses, making them ideal for automotive and industrial applications.

- Rising trends for energy-efficient power conversion solutions in high-power circuits supports adoption.

- Technological innovations in alloy compositions enhance thermal stability and overall performance.

- Expanding implementation of alloy core inductors in 5G infrastructure and next-generation power electronics fuels market growth.

By Mounting Type:

Based on mounting type, the market is segmented into surface mount technology (SMT) inductors and through-hole technology (THT) inductors.

The surface mount technology (SMT) inductors segment accounted for the largest revenue of metal composite power inductor market share in 2024.

- SMT inductors are widely adopted in compact electronic devices due to their small footprint and high integration capability.

- Increasing automation in PCB assembly processes enhances demand for SMT components.

- Rising use in power supply circuits, portable electronics, and automotive applications supports segment dominance.

- Continuous improvements in SMT inductor performance, including higher efficiency and better thermal management, drive metal composite power inductor market expansion.

The through-hole technology (THT) inductors segment is anticipated to register steady growth.

- THT inductors are preferred for high-power applications where durability and mechanical strength are crucial.

- Increasing use in industrial power supplies and high-reliability applications supports their continued progress.

- Expanding deployment in power transmission and heavy-duty electronic circuits enhances market presence.

- Ongoing developments in hybrid mounting solutions improve the usability of THT inductors in complex electronic assemblies.

By Inductance Range:

Based on inductance range, the market is segmented into low inductance (up to 1µH), medium inductance (1µH – 10µH), and high inductance (above 10µH).

The medium inductance segment accounted for the largest revenue share in 2024.

- Inductors in the 1µH – 10µH range are widely used in DC-DC converters, power management systems, and industrial electronics.

- Increasing deployment in automotive power systems and telecommunications equipment supports their dominance.

- Advancements in material technology enhance efficiency and reliability in medium-inductance applications.

- Growing adoption in energy storage and renewable energy applications contributes to segment growth.

The high inductance segment is anticipated to register the fastest CAGR during the forecast period.

- High inductance inductors are increasingly used in industrial automation, medical devices, and aerospace applications requiring robust power management.

- Rising investments in next-generation power distribution systems fuel advancement for high-inductance solutions.

- Technological advancements in core materials and winding techniques enhance performance in critical applications.

- Expanding research into ultra-high inductance applications in power electronics strengthens metal composite power inductor market growth.

By Application:

Based on application, the market is segmented into DC-DC converters, power supplies, automotive electronics, smartphones & tablets, industrial automation, medical devices, and others.

The DC-DC converters segment accounted for the largest revenue share in 2024.

- Metal composite power inductors play a vital role in voltage regulation and power conversion in DC-DC converters.

- Increasing adoption of high-efficiency power conversion solutions in automotive and industrial electronics drives metal composite power inductor market trends.

- Advancements in power semiconductor technology improve the performance and reliability of inductors in converters.

- Expanding deployment of renewable energy systems and EV charging infrastructure enhances demand.

The automotive electronics segment is anticipated to register the fastest CAGR during the forecast period.

- Increasing electrification of vehicles and rising adoption of hybrid and electric powertrains boost applications for high-performance inductors.

- Expanding use of ADAS (Advanced Driver-Assistance Systems) and infotainment systems increases the need for reliable power inductors.

- Growth in EV charging infrastructure and battery management systems supports the adoption of advanced inductors.

- Regulatory mandates promoting energy-efficient automotive solutions further strengthen market extention.

By End-User Industry:

Based on end-user industry, the market is segmented into consumer electronics, automotive, telecommunications, industrial manufacturing, healthcare, and aerospace & defense.

The consumer electronics segment accounted for the largest revenue share in 2024.

- Rising production of smartphones, tablets, and wearable devices increases metal composite power inductor market opportunities for compact, high-efficiency power inductors.

- Expanding adoption of fast-changing technologies and wireless power solutions supports metal composite power inductor market progress.

- Advancements in IoT devices and smart home appliances drive continuous innovation in power inductor applications.

- Increased integration of inductors in battery management and power regulation circuits enhances development.

The automotive segment is anticipated to register the fastest CAGR during the forecast period.

- Growing adoption of electric and hybrid vehicles significantly increases the need for high-performance inductors in power management.

- The rising trends in in-vehicle electronics, including infotainment and safety systems, enhance the development of inductors.

- Development of next-generation powertrains and autonomous driving technologies drives market rise.

- Increasing investments in vehicle electrification and smart charging solutions strengthen the market for automotive power inductors.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

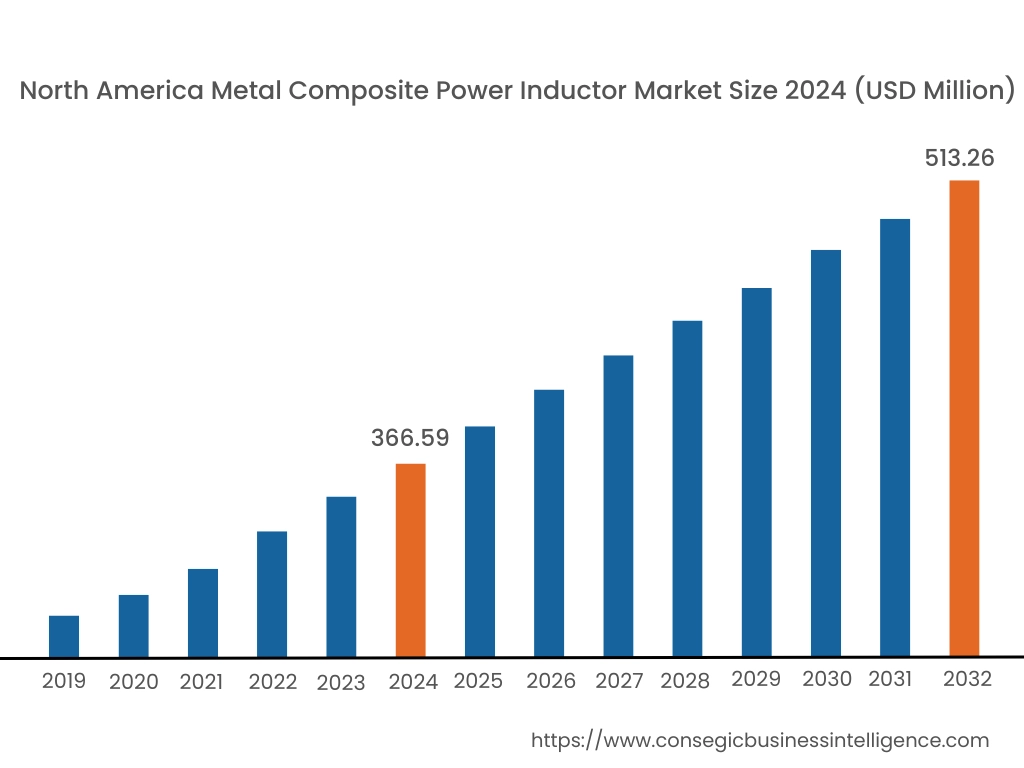

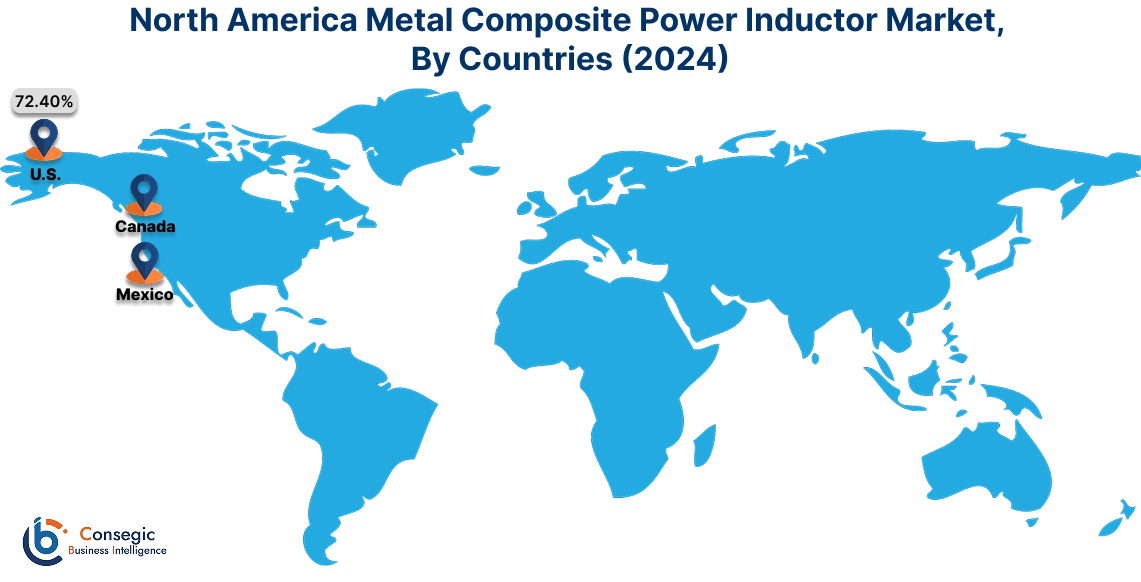

In 2024, North America was valued at USD 366.59 Million and is expected to reach USD 513.26 Million in 2032. In North America, the U.S. accounted for the highest share of 72.40% during the base year of 2024. North America holds a significant share in the global metal composite power inductor market, driven by the strong presence of the consumer electronics, automotive, and industrial automation sectors. The U.S. leads the region with increasing adoption of power inductors in electric vehicles (EVs), 5G infrastructure, and advanced computing systems. Canada contributes to market enlargement with rising investments in renewable energy and power management applications that require high-efficiency inductors. Analysis highlights that ongoing advancements in miniaturized and high-frequency power inductors are shaping the region’s competitive landscape.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 5.0% over the forecast period. The metal composite power inductor market is fueled by rapid industrialization, expanding consumer electronics manufacturing, and increasing adoption of electric vehicles in China, Japan, and South Korea. China dominates the market with extensive production of high-performance inductors for smartphones, data centers, and automotive applications. India’s growing semiconductor industry and investments in local manufacturing support metal composite power inductor market expansion. Japan focuses on precision-engineered power inductors for advanced robotics and IoT devices. Analysis suggests that the rising implementation of 5G networks and automation technologies is driving substantial market advancement.

Europe is a key market for metal composite power inductors, supported by increasing demand from the automotive, aerospace, and telecommunication industries. Countries like Germany, the UK, and France are major contributors. Germany drives trends through its leadership in automotive electrification, with power inductors being crucial in EV powertrains and battery management systems. The UK focuses on integrating efficient power components in smart grid applications, while France emphasizes advanced semiconductor technologies in the defense and aerospace sectors. Analysis indicates that the push toward energy-efficient electronic components is accelerating innovation in this region.

The Middle East & Africa region is witnessing steady growth in the metal composite power inductor market, driven by increasing investments in telecommunications infrastructure, renewable energy, and industrial automation. Countries like Saudi Arabia and the UAE are focusing on expanding smart city projects and integrating high-efficiency inductors in power distribution networks. In Africa, South Africa is emerging as a key market, supporting the adoption of power inductors in energy management systems and consumer electronics. Regional metal composite power inductor market analysis points to challenges such as limited local production and dependence on imported components, affecting supply chain dynamics.

Latin America is an emerging market for metal composite power inductors, with Brazil and Mexico leading the region. Brazil’s expanding automotive and industrial automation sectors are driving advancement for efficient power management solutions. Mexico focuses on enhancing its electronics manufacturing base, leading to increased adoption of high-performance inductors in circuit protection and voltage regulation applications. The metal composite power inductor market analysis highlights that increasing foreign direct investment (FDI) in semiconductor and automotive manufacturing is supporting regional market rise, despite economic uncertainties in smaller economies.

Top Key Players & Market Share Insights:

The metal composite power inductor market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global metal composite power inductor market. Key players in the metal composite power inductor industry include -

- Murata Manufacturing Co., Ltd. (Japan)

- TDK Corporation (Japan)

- Samsung Electro-Mechanics (South Korea)

- Würth Elektronik GmbH & Co. KG (Germany)

- Yageo Corporation (Taiwan)

- Taiyo Yuden Co., Ltd. (Japan)

- Vishay Intertechnology, Inc. (USA)

- Coilcraft, Inc. (USA)

- Chilisin Electronics Corp. (Taiwan)

- Sumida Corporation (Japan)

Recent Industry Developments :

Innovations:

- In November 2021, KEMET introduced its METCOM MPEV series metal composite power inductors, designed specifically for automotive applications. These inductors offer significant advantages such as higher tolerance for current transients, stable performance over a wide temperature range, and low acoustic noise. The METCOM series is ideal for DC-DC switching power supplies used in automotive systems like LED headlights, electric water pumps, and power steering systems. With a maximum operating temperature of 180°C and an AEC-Q200 qualification, these inductors ensure reliability and durability in high-performance automotive electronics. This development highlights the growing importance of advanced power inductors in the automotive industry, particularly for electric vehicles and other high-demand applications.

Metal Composite Power Inductor Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 1,583.65 Million |

| CAGR (2025-2032) | 4.6% |

| By Type |

|

| By Core Material |

|

| By Mounting Type |

|

| By Inductance Range |

|

| By Application |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Metal Composite Power Inductor Market by 2032? +

The market is expected to reach USD 1,583.65 million by 2032.

Which product type dominates the market? +

The shielded metal composite power inductors segment holds the largest market share due to their superior electromagnetic interference (EMI) suppression, making them ideal for high-frequency applications.

Which segment is expected to register the fastest growth? +

The unshielded metal composite power inductors segment is anticipated to grow at the fastest CAGR, driven by their increasing use in consumer electronics like smartphones and tablets.

What is the fastest-growing application for metal composite power inductors? +

Automotive electronics are expected to see the fastest growth due to increasing adoption in electric and hybrid vehicles, as well as advanced driver-assistance systems (ADAS).

Which core material dominates the market? +

The ferrite core segment holds the largest share due to its excellent high-frequency performance, making it widely used in telecommunications and power electronics.