- Summary

- Table Of Content

- Methodology

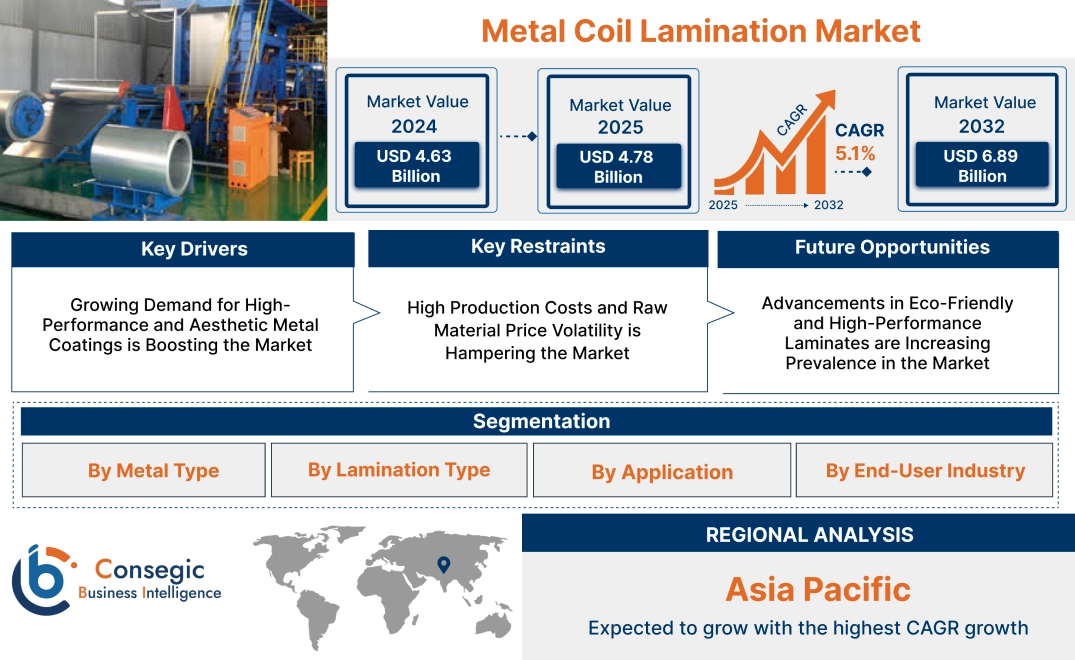

Metal Coil Lamination Market Size:

Metal Coil Lamination Market size is estimated to reach over USD 6.89 Billion by 2032 from a value of USD 4.63 Billion in 2024 and is projected to grow by USD 4.78 Billion in 2025, growing at a CAGR of 5.1% from 2025 to 2032.

Metal Coil Lamination Market Scope & Overview:

The metal coil lamination industry focuses on the process of bonding protective or decorative films, adhesives, and coatings onto metal coils, enhancing their durability, aesthetics, and functional properties. This process is widely used in industries such as automotive, construction, packaging, and appliances, where coated metal sheets offer improved resistance to corrosion, abrasion, and environmental factors. Key materials used for lamination include PVC, PET, polyester, and epoxy-based coatings.

Key characteristics of metal coil lamination include superior surface protection, high adhesion strength, and customization options for color, texture, and finish. The benefits include extended material lifespan, enhanced aesthetic appeal, improved resistance to chemicals and moisture, and better forming capabilities for downstream processing.

Applications span automotive panels, roofing materials, appliance exteriors, and food and beverage packaging, where laminated metal provides added protection and aesthetic value. End-users include automotive manufacturers, construction firms, appliance producers, and packaging companies, driven by increasing metal coil lamination market demand for lightweight, corrosion-resistant materials, advancements in lamination technologies, and rising adoption of pre-coated metal sheets for industrial applications.

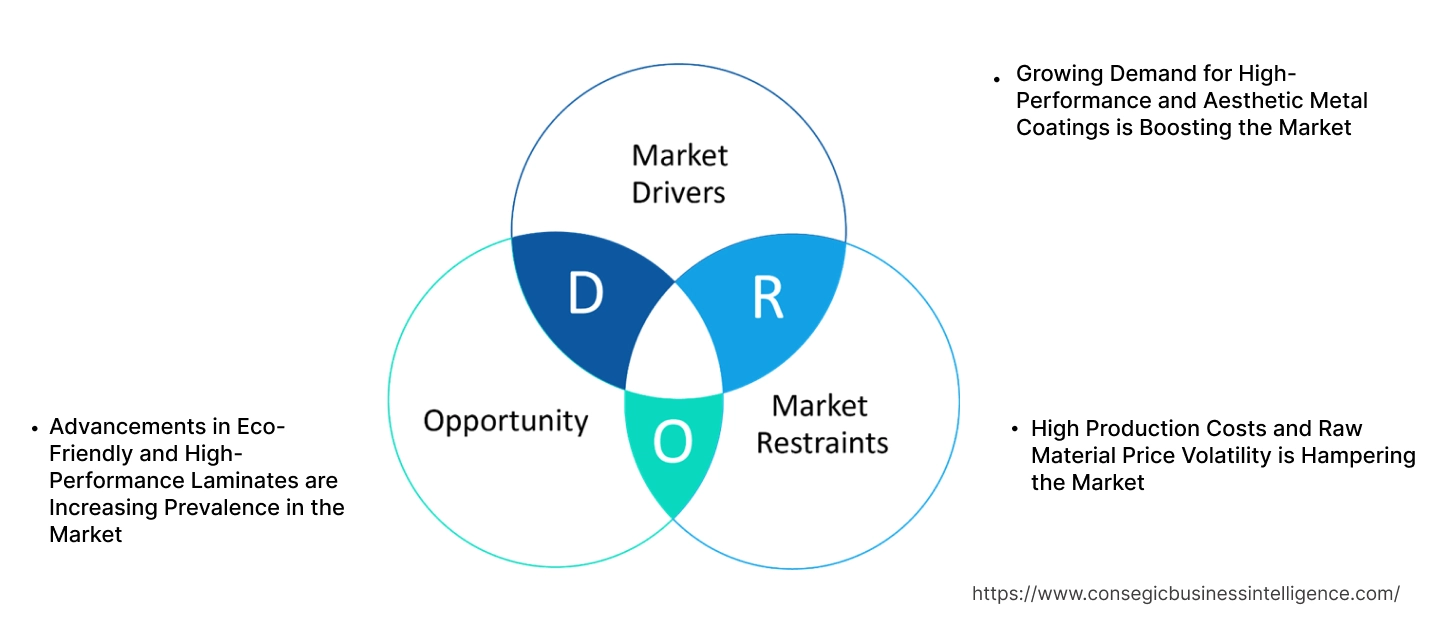

Metal Coil Lamination Market Dynamics - (DRO) :

Key Drivers:

Growing Demand for High-Performance and Aesthetic Metal Coatings is Boosting the Market

The increasing metal coil lamination market opportunities for high-performance, corrosion-resistant, and aesthetically appealing metal surfaces is a significant driver for the metal coil lamination market. Industries such as automotive, construction, appliances, and aerospace rely on laminated metal coils for enhanced durability, improved surface finish, and added functionality. Laminated metal coils provide superior protection against environmental factors, reducing maintenance costs and extending product lifespan. Additionally, trends in lightweight materials for fuel-efficient vehicles and energy-efficient buildings have further increased the adoption of laminated metal solutions in various industrial applications.

Key Restraints:

High Production Costs and Raw Material Price Volatility is Hampering the Market

The high cost associated with advanced lamination processes and fluctuations in raw material prices pose challenges to metal coil lamination market growth. High-performance coatings and adhesive lamination technologies require precision manufacturing, increasing production expenses. Additionally, volatile prices of steel, aluminum, and specialty coatings directly impact the overall cost structure, making it difficult for manufacturers to maintain stable pricing. These cost-related concerns, along with the requirement for specialized machinery and skilled labor, create barriers for small and mid-sized players looking to enter the market.

Future Opportunities :

Advancements in Eco-Friendly and High-Performance Laminates are Increasing Prevalence in the Market

The growing development of sustainable and eco-friendly laminated metal solutions presents a significant opportunity for the market. Manufacturers are investing in low-VOC (volatile organic compound) adhesives, recyclable coatings, and energy-efficient lamination processes to align with stringent environmental regulations and growing corporate sustainability initiatives. Additionally, trends in high-performance laminates, such as anti-microbial, fingerprint-resistant, and UV-resistant coatings, are expanding the application scope of metal coil lamination in industries requiring enhanced material performance. The integration of smart coating technologies, including self-healing and temperature-sensitive laminates, is also driving innovation and creating new growth prospects.

These market dynamics underscore the increasing demand for durable, aesthetically enhanced, and high-performance laminated metal solutions across various industries. While cost and raw material challenges persist, advancements in sustainable lamination technologies and specialized coatings are creating new metal coil lamination market opportunities for growing expansion in both traditional and emerging applications.

Metal Coil Lamination Market Segmental Analysis :

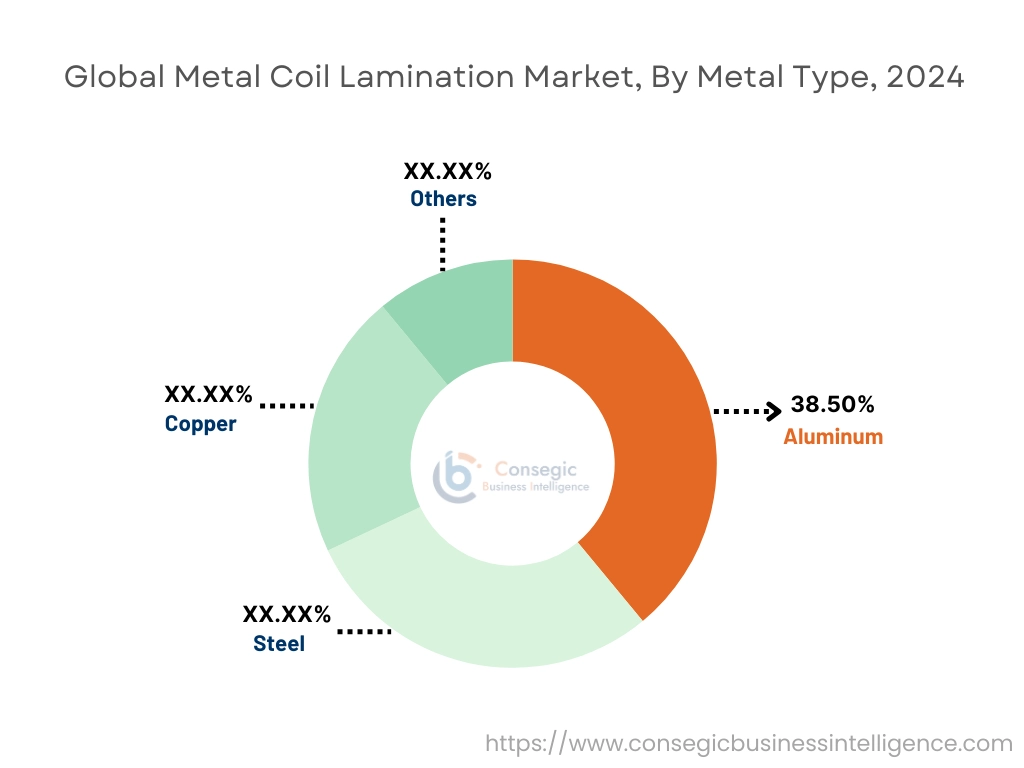

By Metal Type:

Based on metal type, the metal coil lamination market is segmented into aluminum, steel, copper, and others.

The aluminum segment accounted for the largest revenue of the metal coil lamination market share of 38.50% in 2024.

- Aluminum is widely used in coil lamination due to its lightweight nature, corrosion resistance, and high durability.

- Increasing adoption in automotive and aerospace applications supports metal coil lamination market trends.

- Advancements in aluminum coatings and lamination technologies enhance product longevity and performance.

- Expanding use in building facades and construction materials strengthens market dominance.

The copper segment is anticipated to register the fastest CAGR during the forecast period.

- Copper-laminated coils are highly valued for their superior conductivity, making them ideal for electrical and electronic applications.

- Growing investments in renewable energy infrastructure, including power grids and battery technology, drive adoption.

- Rising growth for high-performance materials in industrial machinery and advanced electronics boosts metal coil lamination market expansion.

- Technological innovations in protective lamination processes enhance copper coil durability and efficiency.

By Lamination Type:

Based on lamination type, the market is segmented into film lamination, powder coating lamination, hot melt lamination, and adhesive lamination.

The film lamination segment accounted for the largest revenue of the metal coil lamination market share in 2024.

- Film lamination provides superior protection against corrosion, UV radiation, and chemical exposure, making it widely used in construction and automotive industries.

- Increasing preference for aesthetic and functional surface finishes in architectural applications supports metal coil lamination market expansion.

- Advancements in high-performance films, including self-healing and anti-microbial coatings, enhance adoption.

- Expanding use in decorative applications, including interior design and furniture, further drives trends.

The powder coating lamination segment is anticipated to register the fastest CAGR during the forecast period.

- Powder coating lamination offers high durability, impact resistance, and eco-friendly benefits compared to traditional coatings.

- Rising adoption in industrial manufacturing and transportation sectors for superior corrosion resistance propels growth.

- Stringent environmental regulations promoting low-VOC (volatile organic compound) solutions boost metal coil lamination market demand for powder-coated laminated coils.

- Increasing technological advancements in heat-resistant and anti-fingerprint coatings expand application potential.

By Application:

Based on application, the market is segmented into building & construction, automotive, aerospace, electronics, industrial machinery, packaging, and others.

The building & construction segment accounted for the largest revenue share in 2024.

- Laminated metal coils are widely used in roofing, cladding, and decorative panels due to their strength and weather resistance.

- Increasing urbanization and infrastructure projects drive the adoption of metal coil laminates in modern architecture.

- Advancements in fire-resistant and energy-efficient coatings enhance the use of laminated metals in green building initiatives.

- Growing trends for aesthetic and sustainable construction materials support market advancement.

The electronics segment is anticipated to register the fastest CAGR during the forecast period.

- Laminated metal coils play a critical role in heat dissipation and electromagnetic shielding in electronic devices.

- Rising metal coil lamination market trends for high-performance electronic components, including printed circuit boards (PCBs), support metal coil lamination market growth.

- Expansion of 5G networks and IoT (Internet of Things) applications increases demand for high-conductivity laminated metals.

- Technological advancements in ultra-thin laminated coatings improve performance in miniaturized electronic devices.

By End-Use Industry:

Based on the end-user industry, the market is segmented into construction, automotive & transportation, aerospace & defense, electronics & electrical, industrial manufacturing, and packaging industry.

The construction segment accounted for the largest revenue share in 2024.

- The increasing use of pre-laminated metal coils in exterior cladding, wall panels, and structural components drives trends.

- Growing investments in smart cities and sustainable construction materials enhance market potential.

- Advancements in anti-corrosion and self-cleaning laminated coatings boost adoption in infrastructure projects.

- A rising focus on lightweight, durable, and aesthetic materials in commercial and residential buildings supports this segment analysis.

The automotive & transportation segment is anticipated to register the fastest CAGR during the forecast period.

- Laminated metal coils are used in automotive body panels, chassis components, and decorative trims to improve durability and design.

- Increasing production of electric vehicles (EVs) accelerates advancement for lightweight laminated materials to enhance energy efficiency.

- Advancements in high-strength and scratch-resistant coatings support their adoption in high-performance vehicles.

- Stringent emissions and fuel efficiency regulations drive the use of laminated aluminum and steel in next-generation vehicles.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

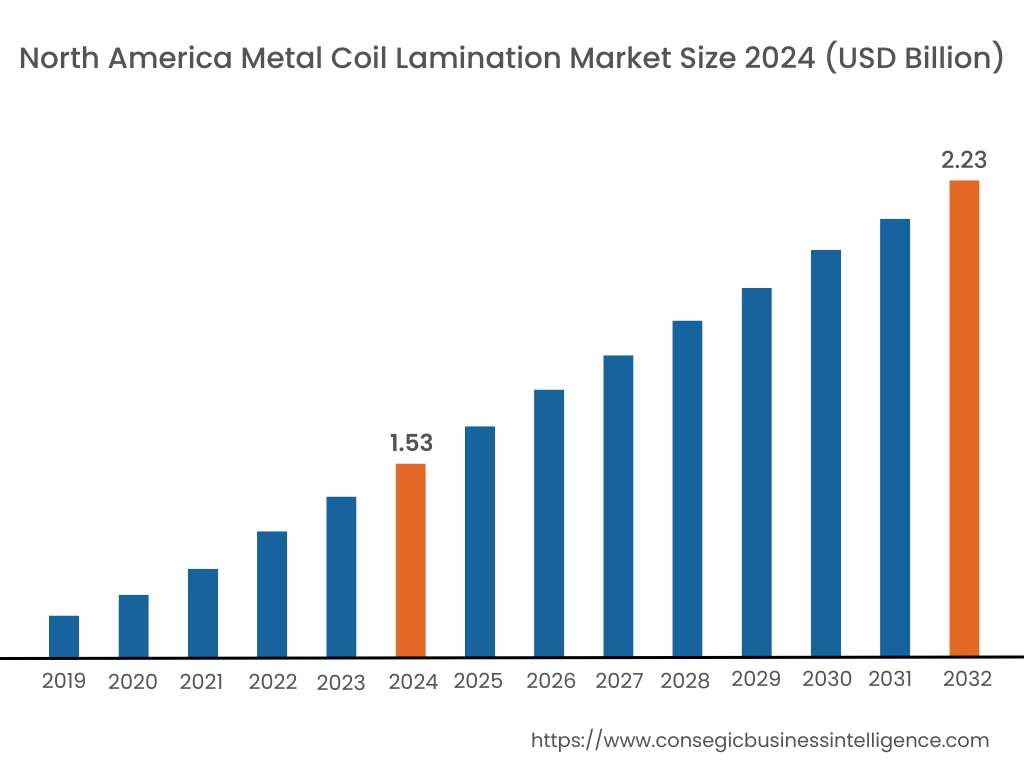

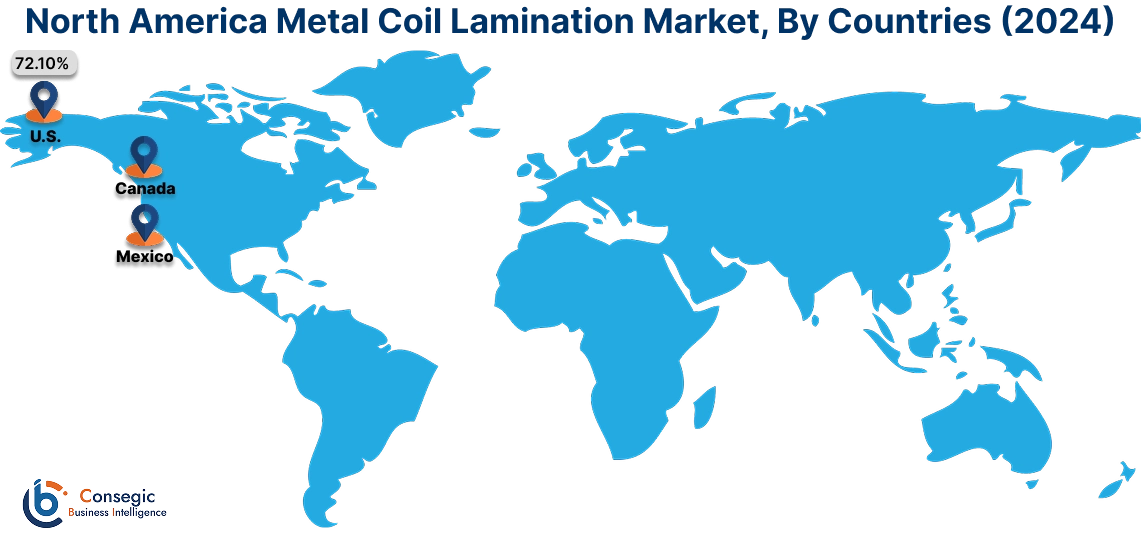

In 2024, North America was valued at USD 1.53 Billion and is expected to reach USD 2.23 Billion in 2032. In North America, the U.S. accounted for the highest share of 72.10% during the base year of 2024. North America holds a significant share of the global metal coil lamination market, driven by increasing demand from the automotive, construction, and industrial sectors. The U.S. leads the region due to the extensive use of laminated metal coils in appliance manufacturing, roofing, and architectural applications. Canada supports the market surge with the rising adoption of energy-efficient building materials, particularly in commercial infrastructure projects. Analysis highlights that the region’s focus on sustainable coatings and corrosion-resistant laminates is driving innovations in metal coil processing technologies.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 5.5% over the forecast period. The metal coil lamination market is fueled by rapid industrialization, expanding infrastructure projects, and increasing manufacturing activities in China, India, and Japan. China dominates the market with large-scale production of laminated metal sheets for consumer electronics, automotive components, and building materials. India’s growing construction sector and government initiatives supporting domestic manufacturing drive the adoption of laminated coils in roofing and paneling applications. Japan focuses on advanced laminated metal technologies with high resistance to wear and corrosion, benefiting the electronics and precision engineering sectors. The analysis highlights that increasing foreign investments in the region’s manufacturing capabilities are accelerating the adoption of high-quality laminated metal coils.

Europe is a key market for metal coil lamination, supported by stringent regulations on energy efficiency, increasing trends for lightweight materials in automotive production, and the presence of advanced manufacturing industries. Countries like Germany, the UK, and France are major contributors. Germany drives metal coil lamination market trends through its automotive and machinery sectors, focusing on high-performance laminated metal sheets for enhanced durability. The UK emphasizes the integration of laminated metal solutions in modern architectural designs, while France sees increased adoption in appliance and industrial equipment manufacturing. Analysis suggests that eco-friendly laminating processes and strict emission norms are shaping technological advancements in the region.

The Middle East & Africa region is witnessing steady growth in the metal coil lamination market, driven by rising investments in infrastructure, commercial construction, and industrial enlargement. Countries like Saudi Arabia and the UAE are focusing on high-performance laminated metals for energy-efficient building materials and architectural applications. In Africa, South Africa is emerging as a key market, with increasing demand for durable metal laminates in residential and commercial roofing. Regional metal coil lamination market analysis indicates that limited local production of high-quality laminated coils results in reliance on imports, affecting pricing and supply chain dynamics.

Latin America is an emerging market for metal coil lamination, with Brazil and Mexico leading the region. Brazil’s growing industrial and automotive sectors drive trends for laminated metal sheets in manufacturing and construction. Mexico focuses on increasing production of laminated coils for export, benefiting from its proximity to North American markets. The metal coil lamination market analysis reveals that infrastructure modernization projects and rising growth for corrosion-resistant materials are supporting market progress, despite economic uncertainties in some countries.

Top Key Players & Market Share Insights:

The metal coil lamination market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global metal coil lamination market. Key players in the metal coil lamination industry include -

- ArcelorMittal (Luxembourg)

- Nippon Steel Corporation (Japan)

- Jindal Steel & Power Ltd. (India)

- S. Steel Košice (Slovakia)

- Hindalco Industries Ltd. (India)

- United States Steel Corporation (U.S. Steel) (USA)

- BASF SE (Germany)

- JFE Steel Corporation (Japan)

- Reliance Steel & Aluminum Co. (USA)

- Swastik Industrial Works Pvt. Ltd. (India)

Metal Coil Lamination Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 6.89 Billion |

| CAGR (2025-2032) | 5.1% |

| By Metal Type |

|

| By Lamination Type |

|

| By Application |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the current and projected size of the Metal Coil Lamination Market? +

Metal Coil Lamination Market size is estimated to reach over USD 6.89 Billion by 2032 from a value of USD 4.63 Billion in 2024 and is projected to grow by USD 4.78 Billion in 2025, growing at a CAGR of 5.1% from 2025 to 2032.

What are the key types of metals used in coil lamination? +

The market is segmented into aluminum, steel, copper, and others. Aluminum held the largest market share in 2024 due to its lightweight nature, corrosion resistance, and durability, while the copper segment is expected to register the fastest CAGR, driven by its high conductivity and increasing application in electronics and renewable energy.

Which lamination type dominates the Metal Coil Lamination Market? +

Film lamination accounted for the largest revenue share in 2024, primarily due to its superior protection against corrosion, UV radiation, and chemical exposure. Powder coating lamination is anticipated to grow at the fastest CAGR, as it offers high durability, impact resistance, and eco-friendly advantages over traditional coatings.

What factors are driving the growth of the Metal Coil Lamination Market? +

Growth is driven by rising demand for high-performance, corrosion-resistant, and aesthetically enhanced laminated metals across industries such as automotive, construction, and electronics. The increasing focus on lightweight and durable materials for fuel-efficient vehicles and energy-efficient buildings further supports market expansion.

Which region holds the largest share in the Metal Coil Lamination Market? +

North America leads the market, with the U.S. dominating due to its extensive use of laminated metal coils in appliances, roofing, and architectural applications. The region also benefits from strong investments in sustainable coatings and corrosion-resistant laminates.