- Summary

- Table Of Content

- Methodology

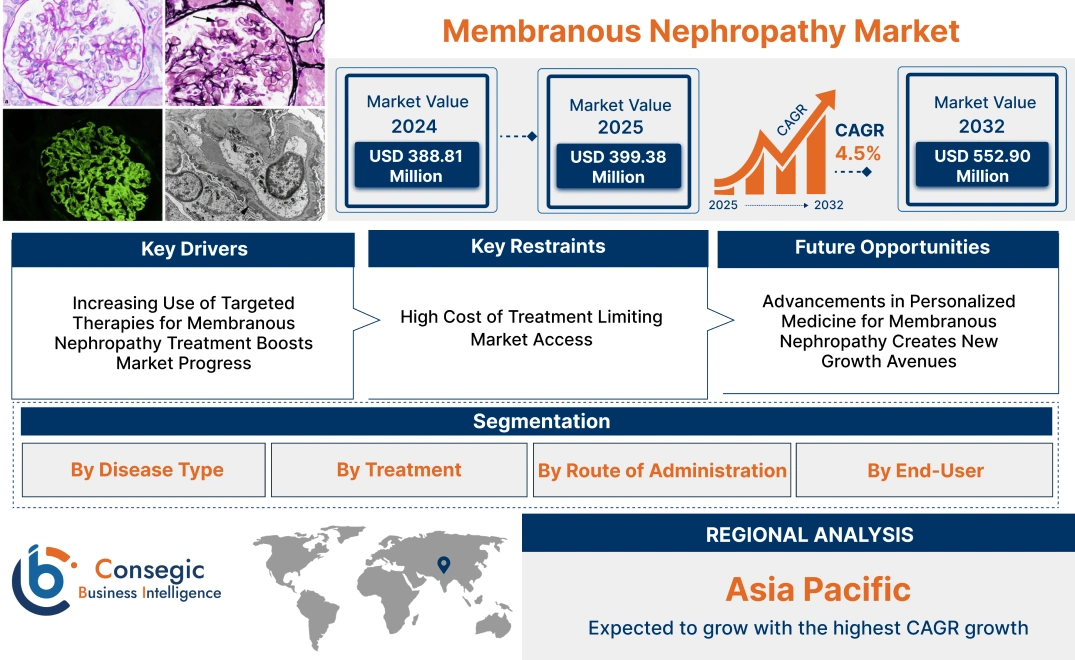

Membranous Nephropathy Market Size:

Membranous Nephropathy Market size is estimated to reach over USD 552.90 Million by 2032 from a value of USD 388.81 Million in 2024 and is projected to grow by USD 399.38 Million in 2025, growing at a CAGR of 4.5% from 2025 to 2032.

Membranous Nephropathy Market Scope & Overview:

Membranous nephropathy is a kidney disorder characterized by the thickening of the glomerular basement membrane, often leading to nephrotic syndrome. The disease primarily affects adults and is a leading cause of nephrotic syndrome in the elderly.

Treatments for membranous nephropathy include immunosuppressive therapy, angiotensin-converting enzyme (ACE) inhibitors, and corticosteroids. These treatments help reduce proteinuria, manage symptoms, and slow disease progression.

The market serves healthcare providers, offering a range of therapeutic options to improve patient outcomes and prevent kidney failure. It caters to hospitals, nephrology clinics, and research institutions focused on kidney diseases.

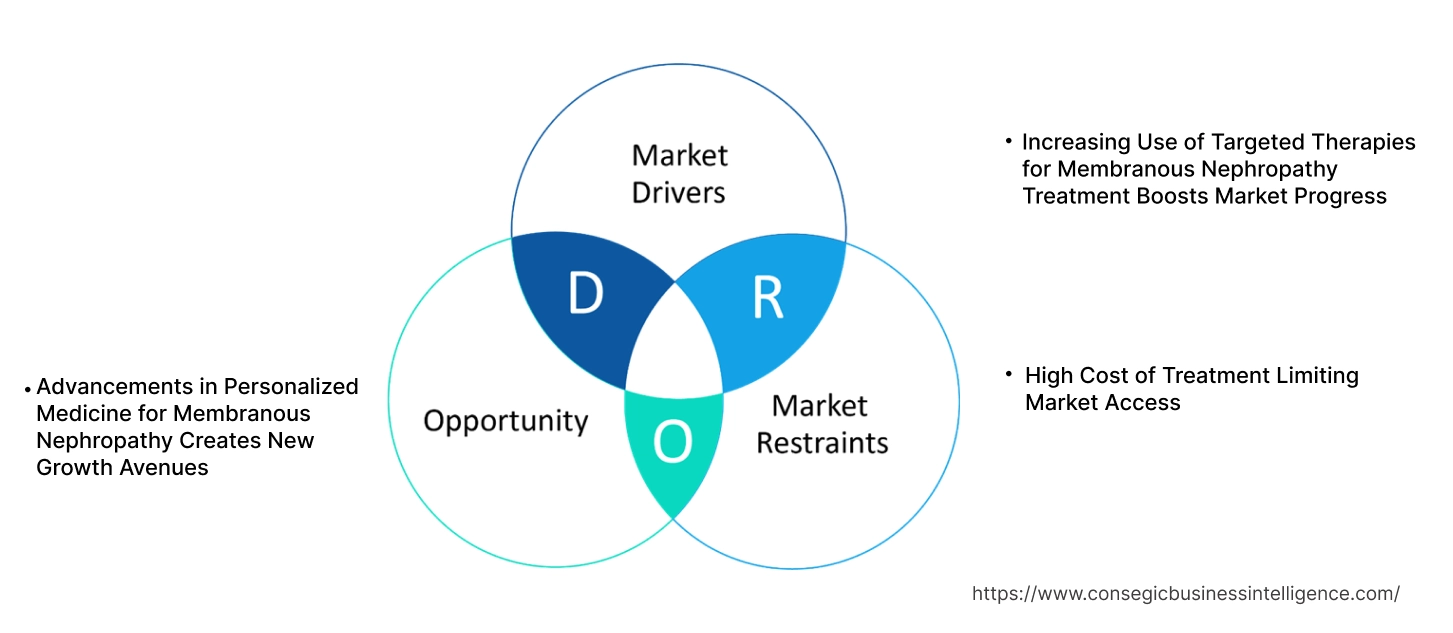

Membranous Nephropathy Market Dynamics - (DRO) :

Key Drivers:

Increasing Use of Targeted Therapies for Membranous Nephropathy Treatment Boosts Market Progress

The application of targeted therapies in the treatment of membranous nephropathy has significantly enhanced treatment outcomes. These therapies focus on specific immune system pathways that are involved in the disease’s progression, offering more effective control of the disease compared to traditional treatment options. For example, monoclonal antibodies, such as rituximab, have shown promising results in reducing proteinuria and improving kidney function in patients with membranous nephropathy. By targeting specific pathways involved in immune response, targeted therapies have reduced adverse effects and improved the long-term prognosis for patients.

Thus, the growing use of targeted therapies is fueling the membranous nephropathy market trend for treatments.

Key Restraints:

High Cost of Treatment Limiting Market Access

The cost of novel treatments for membranous nephropathy, particularly biologic therapies, remains a significant barrier to membranous nephropathy market growth. While medications such as rituximab and cyclophosphamide have demonstrated positive outcomes, their high cost makes them less accessible, especially in lower-income regions or to patients without comprehensive health insurance. Additionally, the prolonged duration of treatment and the need for frequent medical supervision add to the financial burden. These high treatment costs limit the adoption of advanced therapies and create disparities in patient access to effective care.

This financial constraint remains a key factor obstructing the widespread membranous nephropathy market demand.

Future Opportunities :

Advancements in Personalized Medicine for Membranous Nephropathy Creates New Growth Avenues

Personalized medicine represents a significant opportunity in the treatment of membranous nephropathy. By tailoring treatments based on genetic profiles and the specific immune mechanisms of individual patients, personalized approaches have the potential to increase the effectiveness of therapies while reducing side effects. Future advancements in genetic testing and biomarker identification are expected to facilitate more precise treatment plans for patients with membranous nephropathy. For example, research into genetic predispositions and immune system markers specific to membranous nephropathy may enable more individualized care, optimizing outcomes.

The continued development of personalized medicine offers a major membranous nephropathy market opportunity, enhancing treatment efficacy and improving patient care in the near future.

Membranous Nephropathy Market Segmental Analysis :

By Disease Type:

Based on disease type, the market is segmented into Primary Membranous Nephropathy (PMN) and Secondary Membranous Nephropathy (SMN).

The Primary Membranous Nephropathy (PMN) sector accounted for the largest revenue in membranous nephropathy market share in 2024.

- Primary Membranous Nephropathy (PMN) is an autoimmune disorder characterized by damage to the glomerular basement membrane in the kidneys, leading to proteinuria, edema, and potential kidney failure.

- It is one of the most common causes of nephrotic syndrome in adults and is often idiopathic, though genetic predisposition and environmental factors may contribute to its development.

- Treatment options for PMN include immunosuppressive medications like corticosteroids and cyclophosphamide, which aim to reduce immune system activity and minimize kidney damage.

- The high prevalence of PMN and the ongoing development of advanced treatments have made it the largest revenue-generating segment within the market.

- Consequently, PMN will continue to dominate the market in the coming years.

- Therefore, according to membranous nephropathy market analysis, the PMN sector is the largest revenue share holder and remains pivotal in shaping the membranous nephropathy market growth dynamics.

The Secondary Membranous Nephropathy (SMN) sector is anticipated to register the fastest CAGR during the forecast period.

- Secondary Membranous Nephropathy (SMN) occurs due to other underlying conditions such as infections, cancer, or autoimmune diseases like lupus.

- Treatment for SMN typically targets the underlying condition alongside the use of supportive therapies for kidney protection.

- As awareness of the links between systemic diseases and kidney conditions grows, the trend for SMN-specific treatments is expected to rise.

- This segment is projected to grow rapidly, driven by advancements in diagnostic technologies and the increasing focus on addressing secondary causes of kidney diseases.

- Thus, according to membranous nephropathy market analysis, SMN, with its growing recognition and targeted treatment options, is likely to experience the highest membranous nephropathy market trend rate.

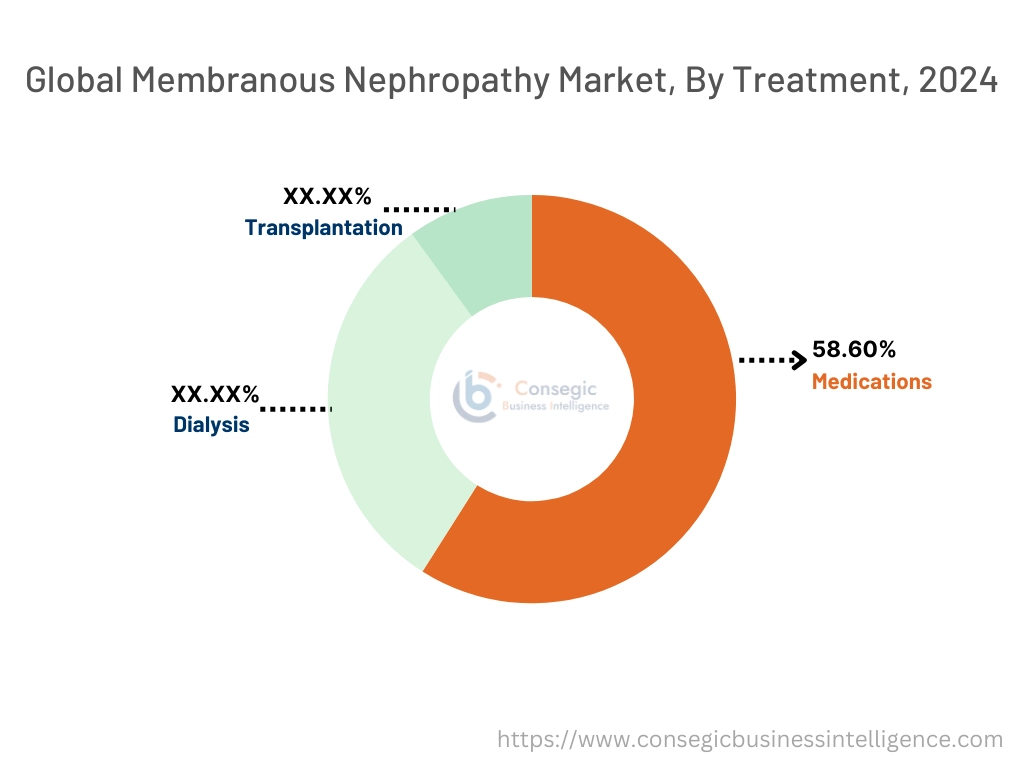

By Treatment:

Based on treatment, the market is segmented into Medications (immunosuppressive drugs, ACE inhibitors, PDE5 inhibitors, and other immunosuppressants), Dialysis, and Transplantation.

The medications segment accounted for the largest revenue in membranous nephropathy market share by 58.60% in 2024.

- Immunosuppressive drugs, including corticosteroids and cyclophosphamide, play a crucial role in the treatment of membranous nephropathy by reducing inflammation and preventing further kidney damage.

- ACE inhibitors help in reducing blood pressure and proteinuria, while PDE5 inhibitors can improve renal function by enhancing kidney blood flow.

- The ongoing development of new drugs and treatment regimens has bolstered the medications segment’s dominance.

- As the first-line therapy for most patients, medications are likely to continue driving the largest share of the market revenue.

- Therefore, according to market analysis, medications, particularly immunosuppressive drugs, are the dominant treatment approach and will continue to generate significant revenue in the market.

The dialysis segment is anticipated to register the fastest CAGR during the forecast period.

- Dialysis is employed in cases where kidney function is severely impaired, and options include hemodialysis and peritoneal dialysis.

- Hemodialysis involves the use of a machine to filter waste products from the blood, while peritoneal dialysis uses the abdominal lining as a filter.

- As the incidence of kidney failure increases, there is a growing trend for dialysis treatments, particularly in regions with aging populations.

- Technological advancements in dialysis equipment and techniques are expected to accelerate the trend of this segment.

- Thus, according to market analysis, dialysis, especially hemodialysis, is poised for rapid growth as an essential treatment for patients with advanced kidney damage.

By Route of Administration:

Based on the route of administration, the market is segmented into Oral, Intravenous (IV), and Subcutaneous.

The oral segment accounted for the largest revenue share in 2024.

- Oral administration of medications, such as corticosteroids and ACE inhibitors, is widely preferred due to its convenience, ease of use, and patient compliance.

- Most immunosuppressive drugs and other nephropathy treatments are available in oral forms, which contributes to the large revenue share of this segment.

- As oral therapies for membranous nephropathy continue to expand, this segment will maintain its leading position in terms of revenue generation.

- Therefore, according to market analysis, oral administration remains the preferred and largest segment due to the patient-friendly nature of oral treatments.

The intravenous (IV) segment is anticipated to register the fastest CAGR during the forecast period.

- Intravenous administration is often used for delivering immunosuppressive treatments, particularly in hospitalized patients with severe membranous nephropathy.

- IV treatments offer the advantage of rapid absorption and effectiveness in critical cases, which makes them essential for acute care.

- As the trend for more aggressive and immediate treatments increases, IV therapies are expected to experience a sharp rise in market share.

- Thus, according to market analysis, IV administration is set to grow rapidly due to its effectiveness in treating severe cases of membranous nephropathy.

By End-User:

Based on end-user, the market is segmented into Hospitals, Specialty Clinics, Homecare Settings, and Research Institutes.

The hospital segment accounted for the largest revenue share in 2024.

- Hospitals are the primary treatment centers for patients with membranous nephropathy, providing advanced medical care, diagnostic services, and treatment options like immunosuppressive drugs, dialysis, and transplantation.

- Due to the complexity of nephropathy treatments, hospitals are better equipped to handle severe cases and provide specialized care, contributing to their dominant market share.

- Furthermore, the increasing number of hospital admissions for nephropathy-related complications supports this segment's revenue trend.

- Therefore, according to market analysis, hospitals remain the dominant end-user segment, largely due to their advanced treatment facilities and comprehensive patient care services.

The homecare settings segment is anticipated to register the fastest CAGR during the forecast period.

- Homecare settings provide patients with an option for receiving care in the comfort of their homes, particularly for those undergoing dialysis or requiring long-term management for membranous nephropathy.

- The growing demand of personalized and patient-centric healthcare, combined with advancements in home dialysis technologies, is expected to drive the rapid growth of this segment.

- With the increasing adoption of remote monitoring tools and patient education programs, homecare settings will likely experience a significant rise in demand.

- Thus, according to market analysis, homecare settings, supported by technological advancements and patient preferences for at-home treatments, are set to witness the fastest growth in the membranous nephropathy market.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

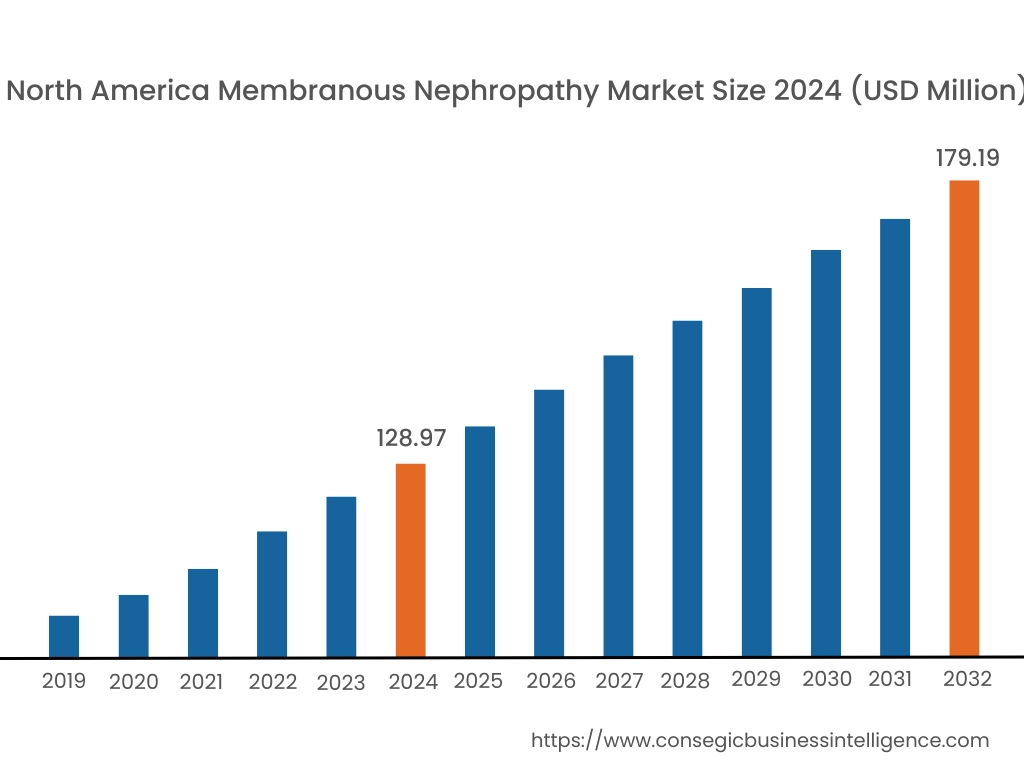

In 2024, North America was valued at USD 128.97 Million and is expected to reach USD 179.19 Million in 2032. In North America, the U.S. accounted for the highest share of 71.55% during the base year of 2024. North America holds a significant share in the membranous nephropathy market. The United States leads in market performance due to advanced healthcare infrastructure, high diagnosis rates, and access to specialized treatments. The presence of leading pharmaceutical companies conducting clinical trials for new therapies also strengthens the market. Additionally, increased awareness about rare kidney diseases and improved healthcare policies support the demand for membranous nephropathy treatments. However, the high cost of therapies and treatment accessibility in underserved regions remain challenges for broader market access.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 4.9% over the forecast period. The Asia-Pacific region is witnessing expanding opportunities in the membranous nephropathy market. Countries like Japan, China, and India have seen advancements in medical technologies and an increase in healthcare investments. Improved diagnosis and the rising prevalence of kidney diseases contribute to market demand. However, the region also faces challenges, such as limited awareness in rural areas and varying healthcare standards across countries. Access to innovative therapies remains uneven, with high treatment costs being a barrier in certain markets. The development of healthcare infrastructure and government support for rare diseases will likely enhance market conditions in the long term.

Europe shows strong growth in the membranous nephropathy market, led by countries like Germany, France, and the UK. The region benefits from comprehensive healthcare systems and a high focus on kidney disease treatment. The European Medicines Agency (EMA) facilitates the approval of new therapies, accelerating access to innovative treatment options. Moreover, increasing research activities and growing awareness of membranous nephropathy contribute to the market's development. However, economic disparities between Western and Eastern Europe may result in uneven access to advanced treatments. The ongoing shift towards personalized medicine and specialized care further supports membranous nephropathy market expansion.

The Middle East and Africa (MEA) region faces challenges in the membranous nephropathy market due to limited healthcare infrastructure and lower awareness of rare kidney diseases. However, countries like the UAE and Saudi Arabia are investing in improving healthcare systems and expanding access to specialized care. The rising incidence of kidney diseases and government initiatives aimed at enhancing healthcare services are likely to contribute to market development. In sub-Saharan Africa, limited access to healthcare services, particularly for rare diseases, presents a significant challenge. The market's growth in MEA depends largely on continued improvements in healthcare infrastructure.

Latin America is witnessing gradual growth in the membranous nephropathy market, with countries like Brazil, Mexico, and Argentina improving their healthcare systems. The increasing prevalence of kidney diseases and the expansion of diagnostic facilities support market demand. However, high treatment costs and limited insurance coverage in certain regions pose barriers to access. Despite these challenges, growing investments in healthcare infrastructure and the introduction of new therapies help enhance market prospects. Awareness programs and partnerships with international organizations will play a crucial role in boosting market growth in the coming years.

Top Key Players and Market Share Insights:

The Global Membranous Nephropathy Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global Membranous Nephropathy Market. Key players in the Membranous Nephropathy industry include-

- Novartis International AG (Switzerland)

- Pfizer Inc. (United States)

- Johnson & Johnson (United States)

- Bristol-Myers Squibb Company (United States)

- Roche Holding AG (Switzerland)

- AbbVie Inc. (United States)

- Amgen Inc. (United States)

- Bayer AG (Germany)

- Sanofi S.A. (France)

- Merck & Co., Inc. (United States)

Recent Industry Developments :

Mergers and Acquisitions:

- In July 2024, Biogen completed its acquisition of HI-Bio, which had previously entered into an agreement with MorphoSys AG in June 2022. This partnership focuses on developing and commercializing MorphoSys’ anti-CD38 antibody, felzartamab, for treating membranous nephropathy.

Membranous Nephropathy Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 552.90 Million |

| CAGR (2025-2032) | 4.5% |

| By Disease Type |

|

| By Treatment |

|

| By Route of Administration |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected market size and growth rate of the Biomaterial Wound Dressing Market by 2032? +

Biomaterial Wound Dressing Market size is estimated to reach over USD 9,838.14 Million by 2032 from a value of USD 6,080.45 Million in 2024 and is projected to grow by USD 6,349.09 Million in 2025, growing at a CAGR of 6.2% from 2025 to 2032.

What are the primary factors driving the growth of the market? +

The market is primarily driven by the rising incidence of chronic wounds, such as diabetic foot ulcers and pressure ulcers, a growing elderly population, and the increasing demand for advanced wound care solutions with enhanced healing properties.

What challenges are restraining market growth? +

High costs of advanced biomaterial-based dressings and inconsistent reimbursement policies across regions are significant challenges limiting market adoption, particularly in low- and middle-income countries.

Which product segment holds the largest share in the market? +

Natural biomaterial dressings, especially collagen and alginate dressings, hold the largest market share due to their superior biocompatibility and effectiveness in promoting faster wound healing.

Which region leads the global biomaterial wound dressing market? +

North America leads the global market due to its advanced healthcare infrastructure, rising prevalence of chronic wounds, and the presence of major market players. However, the Asia Pacific region is expected to grow at the fastest rate, driven by expanding healthcare access and increasing diabetes cases.