- Summary

- Table Of Content

- Methodology

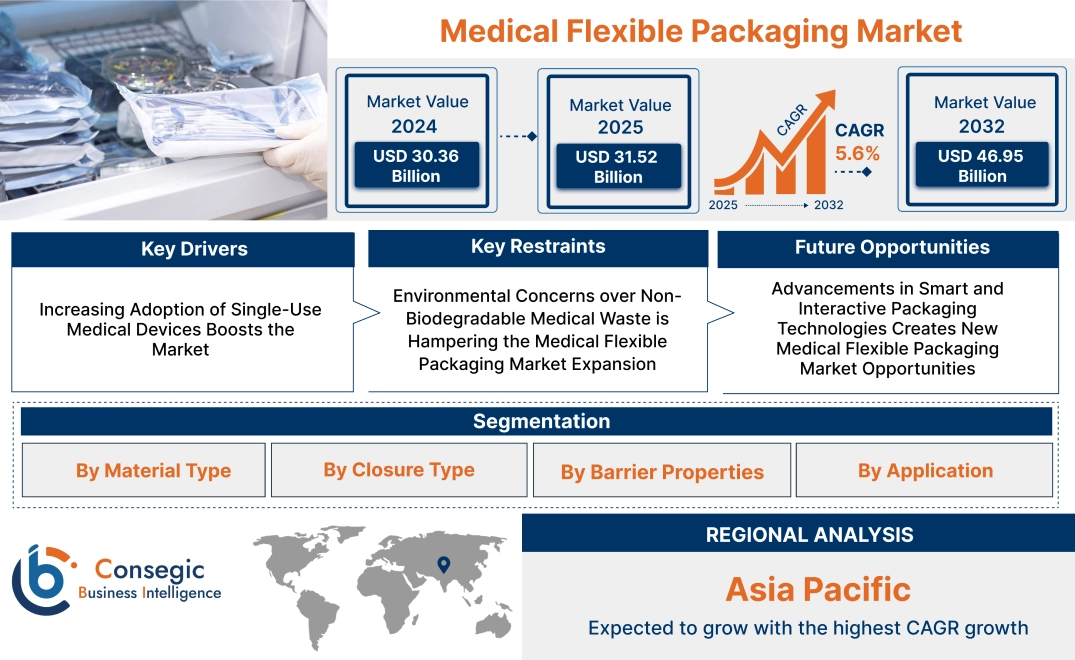

Medical Flexible Packaging Market Size:

Medical Flexible Packaging Market size is estimated to reach over USD 46.95 Billion by 2032 from a value of USD 30.36 Billion in 2024 and is projected to grow by USD 31.52 Billion in 2025, growing at a CAGR of 5.6% from 2025 to 2032.

Medical Flexible Packaging Market Scope & Overview:

The medical flexible packaging focuses on the development and application of lightweight, durable, and sterilizable packaging solutions for medical devices, pharmaceuticals, and healthcare products. This market encompasses materials such as films, pouches, bags, and wraps that are designed to ensure product safety, maintain sterility, and extend shelf life. Key characteristics of medical flexible packaging include high barrier properties, tamper resistance, and compatibility with sterilization techniques like autoclaving and ethylene oxide treatment. The benefits include enhanced product protection, reduced packaging waste, and improved convenience for medical professionals and patients. Applications span the packaging of surgical instruments, IV bags, diagnostic kits, and pharmaceutical products. End-users include hospitals, clinics, pharmaceutical manufacturers, and diagnostic laboratories, driven by the increasing demand for sterilized and safe medical packaging, advancements in material science, and the growing focus on sustainability in the healthcare sector.

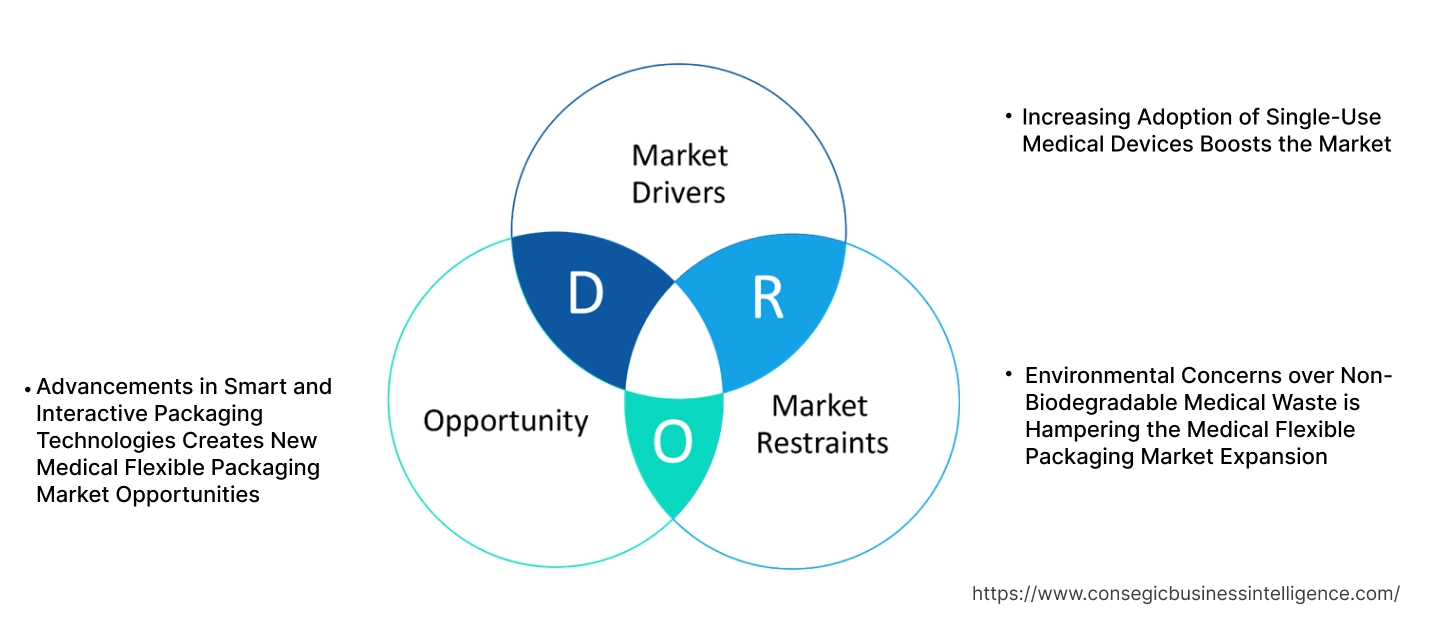

Medical Flexible Packaging Market Dynamics - (DRO) :

Key Drivers:

Increasing Adoption of Single-Use Medical Devices Boosts the Market

The rising reliance on single-use medical devices is driving significant surge in the medical flexible packaging market trends. Products such as syringes, catheters, IV bags, and diagnostic kits are increasingly preferred due to their role in preventing cross-contamination and ensuring patient safety. These devices require high-quality flexible packaging solutions that maintain sterility and integrity during storage, transportation, and usage. Flexible materials, including pouches, wraps, and barrier films, are particularly suited to the demands of single-use applications, offering lightweight, cost-effective, and tamper-resistant solutions.

Trends in infection control, especially within hospitals and clinics, further underscore the importance of single-use devices and their associated packaging. Additionally, advancements in healthcare delivery, such as home-based treatments and point-of-care diagnostics, emphasize the need for portable and secure packaging for single-use medical products. As healthcare systems prioritize safety and operational efficiency, the analysis indicates that single-use medical devices and their packaging are becoming increasingly central to modern healthcare practices.

Key Restraints:

Environmental Concerns over Non-Biodegradable Medical Waste is Hampering the Medical Flexible Packaging Market Expansion

The extensive use of plastic-based flexible packaging in the medical sectors has raised significant environmental concerns due to the accumulation of non-biodegradable waste. Medical flexible packaging often involves complex multilayer materials that are challenging to recycle, exacerbating the issue of waste management. Additionally, the disposal of used medical packaging is often subject to strict regulatory and safety guidelines, which limit recycling opportunities and increase landfill contributions.

Governments and regulatory bodies worldwide are implementing stricter waste management policies to address this issue, encouraging the development of sustainable alternatives. However, the lack of established recycling infrastructure and the high costs of eco-friendly materials pose challenges for manufacturers. Trends in circular economy practices and innovations in biodegradable materials offer potential pathways to mitigate these concerns, but achieving widespread adoption remains a key hurdle for the sector.

Future Opportunities :

Advancements in Smart and Interactive Packaging Technologies Creates New Medical Flexible Packaging Market Opportunities

Innovations in smart and interactive packaging are transforming the medical flexible packaging landscape. Features such as temperature monitoring, RFID tags, and QR codes integrated into flexible packaging enhance functionality and improve safety and traceability. These technologies allow real-time monitoring of critical parameters like temperature, humidity, and product integrity, ensuring optimal storage and transportation conditions for sensitive medical products.

Interactive packaging also supports better patient engagement by providing digital information, such as dosage instructions or expiration alerts, accessible through smartphone apps or embedded codes. Trends in digital health and IoT-enabled devices are further driving the adoption of these advanced solutions. As the healthcare sectors focuses on enhancing efficiency and personalization, the integration of smart technologies into packaging is poised to create significant medical flexible packaging market opportunities for manufacturers, aligning with the broader push toward innovation and improved patients outcome.

Medical Flexible Packaging Market Segmental Analysis :

By Material Type:

Based on material type, the market is segmented into polyethylene (PE), polypropylene (PP), polyvinyl chloride (PVC), ethylene vinyl alcohol (EVOH), aluminum foils, and others.

The polyethylene (PE) segment accounted for the largest revenue in medical flexible packaging market share in 2024.

- Polyethylene is extensively used for its excellent flexibility, durability, and moisture resistance, making it ideal for pharmaceutical and diagnostic packaging.

- The adaptability of PE for various forms, such as films, pouches, and bags, supports its medical flexible packaging market trends across multiple medical applications.

- Manufacturers are increasingly adopting recyclable PE materials, aligning with sustainability goals and reducing environmental impact.

- Polyethylene's ability to maintain product integrity during transportation and storage drives its widespread usage in global healthcare industries.

- Polyethylene leads the market due to its versatility, durability, and compatibility with sustainability initiatives in medical packaging.

The aluminum foils segment is anticipated to register the fastest CAGR during the forecast period.

- Aluminum foils offer exceptional barrier properties, including protection against moisture, oxygen, and UV light, ensuring the safety of sensitive medical products.

- Their lightweight yet robust nature makes them suitable for high-value pharmaceutical products and temperature-sensitive applications.

- Increasing adoption of aluminum foils in sterile and single-use packaging solutions highlights their role in infection control practices.

- Advancements in coating technologies for aluminum foils enhance their functionality, further driving their medical flexible packaging market demand in specialized medical applications.

- Aluminum foils are expected to grow rapidly, driven by their superior barrier properties and suitability for advanced medical and pharmaceutical packaging.

By Closure Type:

Based on closure type, the market is segmented into heat-sealable, cold-formable, zip-top, and twist-off.

The heat-sealable segment accounted for the largest revenue in medical flexible packaging market share in 2024.

- Heat-sealable closures ensure tamper-evident and airtight packaging, critical for preserving product sterility in healthcare settings.

- These closures are compatible with various materials and packaging formats, making them a versatile solution across multiple applications.

- The increasing use of heat-sealable packaging in combination with high-speed automated packaging lines enhances their efficiency and adoption.

- Heat-sealable closures align with regulatory requirements for secure and hygienic packaging, particularly in pharmaceuticals and diagnostics.

- Heat-sealable closures dominate the market, driven by their reliability, compatibility, and role in maintaining product sterility.

The zip-top segment is anticipated to register the fastest CAGR during the forecast period.

- Zip-top closures are gaining popularity for their ease of use and resealability, catering to patient-friendly packaging needs.

- They are increasingly used in consumer-driven healthcare products, such as diagnostic kits and over-the-counter medications.

- The trends of adopting zip-top closures for packaging smaller or multi-use products supports their rapid adoption.

- Zip-top closures also contribute to reducing product wastage, aligning with sustainability goals and consumer preferences.

- Zip-top closures are expected to grow rapidly, supported by their user-friendly design and increasing adoption in multi-use medical packaging.

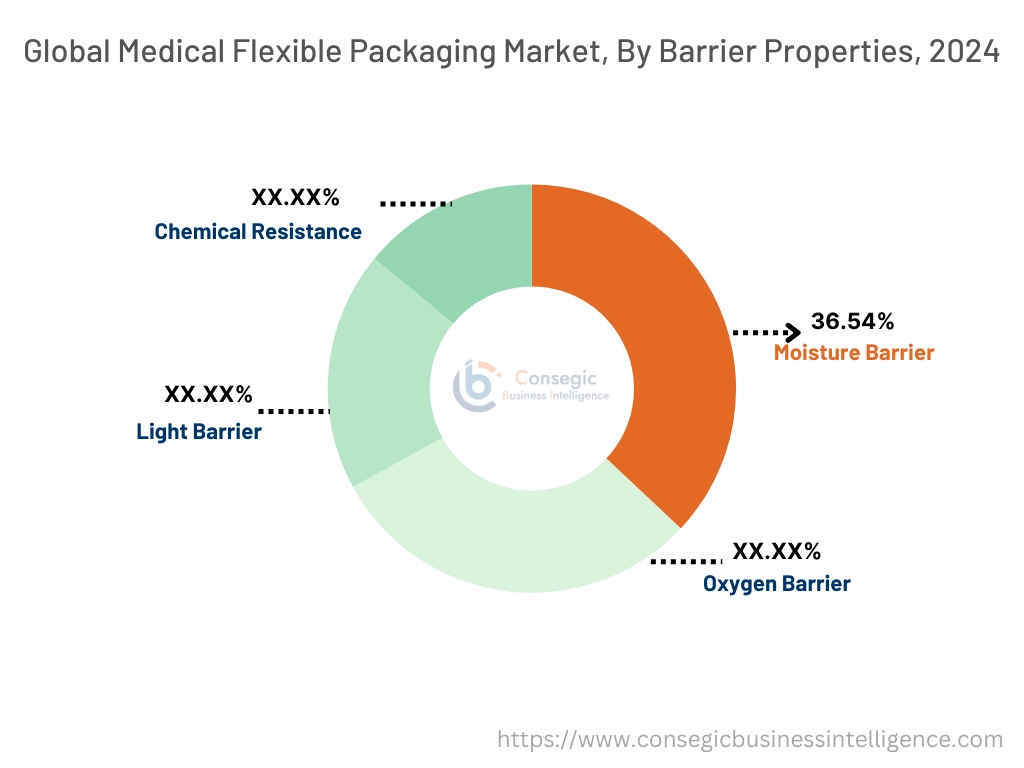

By Barrier Properties:

Based on barrier properties, the market is segmented into moisture barrier, oxygen barrier, light barrier, and chemical resistance.

The moisture barrier segment accounted for the largest revenue share of 36.54% in 2024.

- Moisture barriers protect sensitive pharmaceutical and diagnostic products from humidity, ensuring product stability and efficacy.

- These barriers are widely used for packaging solutions in harsh or varying environmental conditions, enhancing product durability.

- Increasing adoption of multi-layered packaging with enhanced moisture barrier properties caters to high-value biologics and injectable drugs.

- Advancements in moisture barrier films with reduced environmental impact support their growing adoption in sustainable medical packaging.

- As per segmental trends analysis, moisture barriers dominate the market, driven by their critical role in protecting sensitive healthcare products across various environments.

The light barrier segment is anticipated to register the fastest CAGR during the forecast period.

- Light barriers are increasingly used for packaging photosensitive medical products, such as certain drugs and diagnostic reagents.

- Innovations in advanced materials, such as metalized films and high-opacity polymers, enhance light barrier effectiveness while maintaining packaging flexibility.

- Their role in preventing photochemical degradation of medications supports their application in pharmaceutical and diagnostic packaging.

- The growth for protective packaging for light-sensitive products in emerging healthcare markets drives the growth of this segment.

- Light barriers are expected to grow rapidly, supported by their importance in protecting photosensitive healthcare products and expanding applications.

By Application:

Based on application, the market is segmented into pharmaceutical manufacturing, medical device manufacturing, implant manufacturing, diagnostics, and others.

The pharmaceutical manufacturing segment accounted for the largest revenue share in 2024.

- Pharmaceutical manufacturing relies heavily on flexible packaging for ensuring sterility and preventing contamination of medications and injectables.

- Increasing requirement for innovative packaging for biologics, controlled-release drugs, and personalized medications supports the growth of this segment.

- Flexible packaging solutions tailored for high-value drug transportation and storage enhance the reliability and safety of pharmaceutical supply chains.

- Regulatory compliance requirements for pharmaceutical packaging further drive the adoption of advanced flexible packaging materials and designs.

- Hence, pharmaceutical manufacturing leads the market, supported by the growing need for secure, innovative, and compliant packaging solutions.

The diagnostics segment is anticipated to register the fastest CAGR during the forecast period.

- Diagnostics benefit from flexible packaging for reagents, test kits, and at-home diagnostic solutions, ensuring ease of use and protection.

- The rising adoption of compact and travel-friendly packaging for diagnostic kits aligns with the medical flexible packaging market growth for point-of-care and home-use diagnostics.

- Flexible packaging enhances the accessibility and functionality of diagnostic products, particularly in emerging markets with expanding healthcare access.

- Advancements in packaging materials that support extended shelf life and sterility of diagnostic reagents further boost this segment.

- Thus, as per segmental analysis, the diagnostics segment is expected to grow rapidly, supported by increasing demand for accessible, durable, and user-friendly packaging solutions in healthcare.

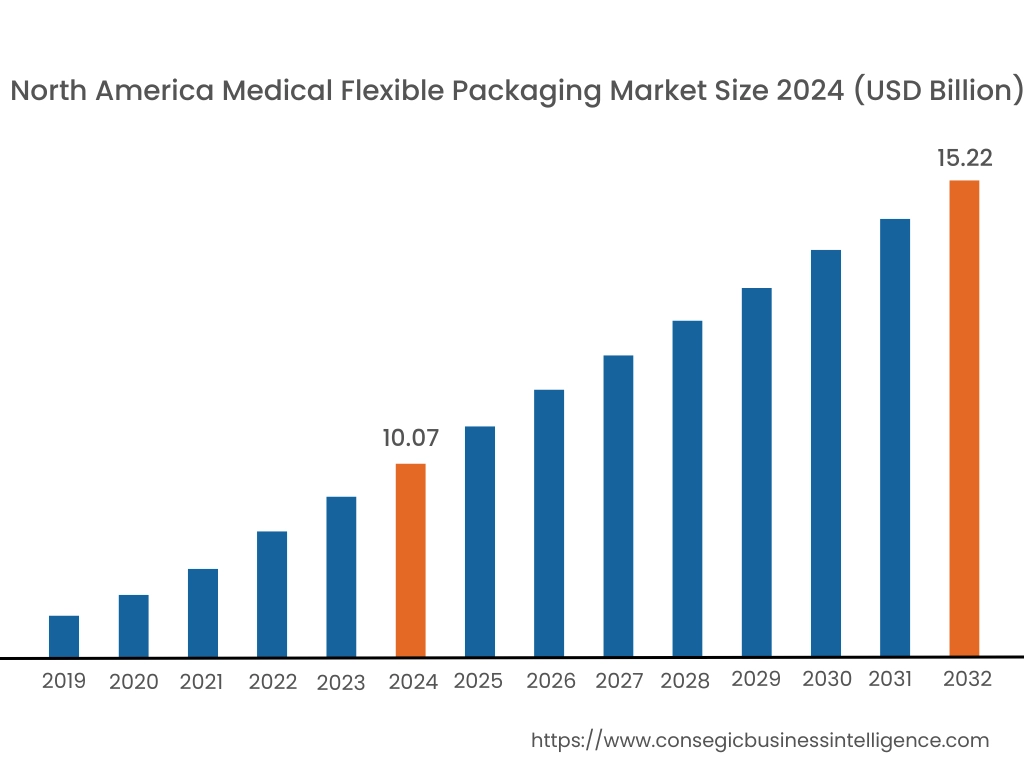

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

In 2024, North America was valued at USD 10.07 Billion and is expected to reach USD 15.22 Billion in 2032. In North America, the U.S. accounted for the highest share of 73.40% during the base year of 2024. The medical flexible packaging market analysis shows that North America holds a significant share of the market, driven by the region's advanced healthcare infrastructure and strong demand for high-quality packaging solutions for pharmaceuticals and medical devices. The U.S. dominates the region due to the widespread adoption of flexible packaging formats such as pouches, sachets, and wraps for sterilized medical equipment and drug delivery systems. Canada also contributes to the market with its increasing focus on sustainable and recyclable packaging materials in the healthcare sector. However, strict regulatory requirements and high production costs for advanced packaging materials may pose challenges for manufacturers.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 6.0% over the forecast period. Asia-Pacific is the fastest-growing region in the medical flexible packaging market analysis, fueled by the expansion of the pharmaceutical and healthcare sectors in China, India, and Japan. China leads the market with its large-scale pharmaceutical manufacturing and rising medical flexible packaging market growth for flexible packaging formats for both domestic use and export. India’s growing healthcare infrastructure and increasing focus on affordable packaging solutions for generic drugs drive the adoption of flexible packaging. Japan emphasizes high-quality and precision packaging solutions for advanced medical devices and pharmaceutical products. However, challenges such as cost sensitivity and inconsistent quality standards across the region may impact the market’s growth in certain areas.

The Middle East & Africa region is witnessing steady advancements in the market, driven by growing investments in healthcare infrastructure and increasing medical flexible packaging market demand for pharmaceutical products. Regional analysis depicts that countries like Saudi Arabia and the UAE are key markets, adopting flexible packaging solutions to ensure the safety and sterility of medical products during storage and transportation. In Africa, South Africa is emerging as a market for flexible packaging in medical devices and pharmaceuticals, supported by efforts to improve healthcare delivery. However, limited local manufacturing capabilities and reliance on imports for advanced materials may restrict medical flexible packaging market expansion in some parts of the region.

Europe is a key market for medical flexible packaging, supported by stringent regulations on pharmaceutical and medical device packaging and the region's focus on sustainability. Countries like Germany, France, and the UK are leading contributors. Germany’s advanced manufacturing capabilities and strong pharmaceutical industry drive the need for flexible packaging that ensures product safety and extends shelf life. France focuses on eco-friendly materials in medical packaging to meet EU directives on waste reduction, while the UK emphasizes innovative solutions for sterile medical packaging. However, compliance with strict regulatory standards and high energy costs associated with production can challenge market growth.

Latin America is an emerging market for medical flexible packaging, with Brazil and Mexico leading the region. Brazil’s expanding pharmaceutical industry and focus on improving healthcare access drive the adoption of flexible packaging for drug delivery systems and sterile equipment. Mexico’s growing medical device manufacturing sector and increasing exports to North America enhance demand for flexible packaging solutions. The region is also seeing interest in sustainable packaging materials to align with global environmental trends. However, economic instability and inconsistent regulatory frameworks may hinder broader adoption of flexible packaging in the region.

Top Key Players & Market Share Insights:

The medical flexible packaging market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global medical flexible packaging market. Key players in the medical flexible packaging industry include -

- Amcor plc (Australia)

- AptarGroup, Inc. (U.S.)

- Huhtamaki Oyj (Finland)

- Coveris Holdings S.A. (Luxembourg)

- WestRock Company (U.S.)

- Becton, Dickinson and Company (U.S.)

- Berry Global Inc. (U.S.)

- WINPAK LTD. (Canada)

- Sealed Air Corporation (U.S.)

- Mondi Group (U.K.)

Medical Flexible Packaging Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 46.95 Billion |

| CAGR (2025-2032) | 5.6% |

| By Material Type |

|

| By Closure Type |

|

| By Barrier Properties |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected growth of the Medical Flexible Packaging Market? +

Medical Flexible Packaging Market size is estimated to reach over USD 46.95 Billion by 2032 from a value of USD 30.36 Billion in 2024 and is projected to grow by USD 31.52 Billion in 2025, growing at a CAGR of 5.6% from 2025 to 2032.

What are the primary drivers of market growth? +

Key drivers include increasing adoption of single-use medical devices to prevent cross-contamination, advancements in home-based healthcare and point-of-care diagnostics, and innovations in lightweight, durable, and sterile flexible packaging solutions.

What challenges does the market face? +

Environmental concerns regarding non-biodegradable medical waste and the complex recycling process for multilayer packaging materials pose significant challenges. Additionally, high production costs for advanced and eco-friendly materials may hinder market expansion.

Which material type dominates the market? +

Polyethylene (PE) leads the market due to its flexibility, durability, and moisture resistance. It is widely used for pharmaceutical and diagnostic packaging, and its recyclability aligns with sustainability goals.

What are the fastest-growing segments by material and application? +

Aluminum foils are anticipated to witness the fastest growth due to their superior barrier properties, while diagnostics is expected to grow rapidly within applications, driven by demand for durable, portable, and user-friendly packaging for at-home and point-of-care testing kits.