- Summary

- Table Of Content

- Methodology

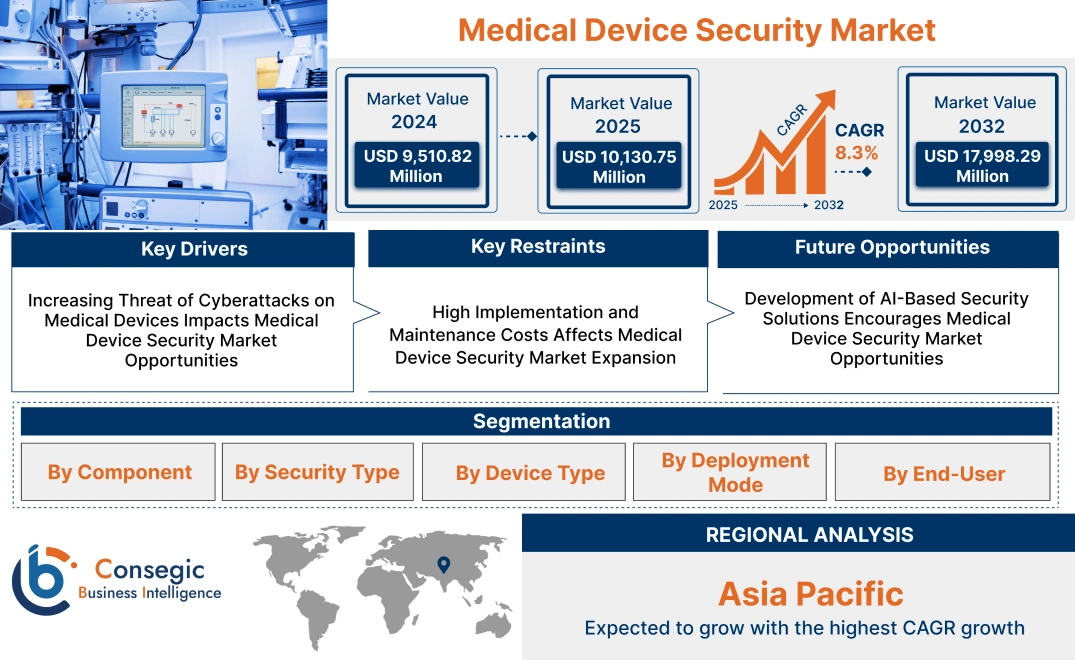

Medical Device Security Market Size:

Medical Device Security Market size is estimated to reach over USD 17,998.29 Million by 2032 from a value of USD 9,510.82 Million in 2024 and is projected to grow by USD 10,130.75 Million in 2025, growing at a CAGR of 8.3% from 2025 to 2032.

Medical Device Security Market Scope & Overview:

Medical device security refers to the protection of medical devices and healthcare systems from unauthorized access, cyber threats, and data breaches. These devices include diagnostic machines, wearable health devices, and connected equipment used in healthcare settings.

Key features of medical device security include encryption, access control, threat detection, and compliance with regulatory standards. The benefits include enhanced patient safety, data integrity, and protection from malicious attacks.

Applications of medical device security are found in hospitals, clinics, research institutions, and healthcare service providers. The market serves healthcare professionals, device manufacturers, and cybersecurity firms in ensuring secure and reliable operation of medical devices.

Medical Device Security Market Dynamics - (DRO) :

Key Drivers:

Increasing Threat of Cyberattacks on Medical Devices Impacts Medical Device Security Market Opportunities

As medical devices become more connected to healthcare networks, they are increasingly vulnerable to cyberattacks. With more devices linked to the Internet of Medical Things (IoMT), security risks are heightened, especially in hospitals and clinics. For example, pacemakers, infusion pumps, and diagnostic imaging systems are now being targeted by malicious actors seeking to disrupt medical services or steal sensitive patient data. Medical device security systems help protect against these cyberattacks by securing communication channels, detecting vulnerabilities, and preventing unauthorized access.

Therefore, the escalating risk of cyberattacks on connected medical devices is driving the medical device security market trend for robust security solutions in the healthcare sector.

Key Restraints:

High Implementation and Maintenance Costs Affects Medical Device Security Market Expansion

Implementing comprehensive security measures for medical devices can be costly. Healthcare organizations often face financial challenges in adopting advanced security technologies, such as encryption, intrusion detection systems, and regular software updates, which are essential for protecting sensitive medical data. The integration of security features into medical devices also requires specialized hardware, software, and regular testing, further increasing costs. Smaller healthcare providers, particularly in developing regions, may struggle with these expenses, limiting the widespread adoption of effective medical device security solutions.

This financial burden acts as a significant barrier, hindering the medical device security market growth.

Future Opportunities :

Development of AI-Based Security Solutions Encourages Medical Device Security Market Opportunities

The use of artificial intelligence (AI) in medical device security holds great promise for the future. AI-powered security systems can analyze vast amounts of data in real time, detect abnormal device behavior, and identify potential security threats faster and more accurately than traditional methods. AI can also predict potential vulnerabilities by continuously learning from new data, providing more proactive security. With AI technologies becoming more sophisticated, their integration into medical device security solutions is expected to enhance the protection of devices against emerging cyber threats.

Thus, the development and adoption of AI-based medical device security solutions present a significant opportunity for medical device security market growth in the near future.

Medical Device Security Market Segmental Analysis :

By Component:

Based on the component, the market is segmented into solutions and services.

The solutions segment accounted for the largest revenue in medical device security market share in 2024.

- The solutions category includes encryption solutions, antivirus & anti-malware solutions, identity & access management solutions, risk management solutions, and intrusion detection and prevention systems (IDS/IPS).

- These solutions are crucial in protecting medical devices from cyber threats, ensuring data confidentiality, integrity, and availability.

- Encryption solutions play a significant role in safeguarding sensitive patient data, while antivirus & anti-malware solutions help in defending against malicious software attacks.

- Identity & access management ensures only authorized users can access critical medical data, and risk management solutions mitigate the overall security risks. IDS/IPS systems monitor and protect devices from external cyber threats by detecting and preventing unauthorized access.

- The medical device security market trend for these solutions is increasing as healthcare organizations face rising cybersecurity risks.

- Therefore, according to medical device security market analysis, the solutions segment holds the largest revenue share due to its comprehensive range of products designed to mitigate cybersecurity risks.

The services segment is anticipated to register the fastest CAGR during the forecast period.

- The services category is further divided into professional services and managed services.

- These services support the implementation, maintenance, and monitoring of medical device security solutions.

- Managed services, in particular, are expected to grow rapidly, as healthcare providers seek external expertise to handle complex cybersecurity challenges.

- These services allow healthcare institutions to focus on patient care while experts ensure continuous protection of their medical devices.

- Thus, according to medical device security market analysis, the services segment is expected to experience the fastest trend, driven by the increasing reliance on external support to manage security for medical devices.

By Security Type:

Based on security type, the market is segmented into endpoint security, network security, cloud security, application security, and others.

The endpoint security segment accounted for the largest revenue in Medical Device Security Market share in 2024.

- Endpoint security focuses on protecting individual devices, such as hospital medical devices, wearable medical devices, and other connected healthcare devices.

- It involves deploying security measures like antivirus software, encryption, and access controls to ensure that each device is secure from cyber threats.

- With the growing use of connected devices in healthcare, the importance of securing endpoints has become a top priority for medical device manufacturers and healthcare providers.

- The segment is crucial for preventing data breaches and ensuring the safe operation of medical devices.

- Therefore, according to market analysis, endpoint security holds the largest market share, as it protects critical devices in the healthcare ecosystem.

The cloud security segment is anticipated to register the fastest CAGR during the forecast period.

- As healthcare providers increasingly adopt cloud-based systems for data storage and medical device management, cloud security has become essential.

- This segment involves securing medical data and applications stored in the cloud to prevent unauthorized access, data breaches, and cyberattacks. The rise of cloud adoption in healthcare and the growing need for secure data sharing and collaboration are key factors contributing to the rapid trend of the cloud security segment.

- Thus, according to market analysis, cloud security is set to experience the fastest growth, driven by the shift toward cloud-based solutions in medical device management and healthcare IT infrastructure.

By Device Type:

Based on device type, the market is segmented into hospital medical devices, wearable and external medical devices, embedded medical devices, and others.

The hospital medical devices segment accounted for the largest revenue share in 2024.

- Hospital medical devices include critical equipment like infusion pumps, diagnostic imaging systems, and patient monitoring systems, all of which are integral to patient care.

- These devices are increasingly connected to hospital networks and require robust cybersecurity measures to protect against threats such as ransomware and unauthorized access.

- The large number of hospital devices and their critical role in healthcare operations contribute to this segment’s dominant share of the market.

- Therefore, according to market analysis, hospital medical devices dominate the market due to their widespread use and critical function in patient care.

The wearable and external medical devices segment is anticipated to register the fastest CAGR during the forecast period.

- Wearable and external medical devices, such as wearable heart rate monitors, fitness trackers, and continuous glucose monitors, have gained popularity due to their convenience and ability to collect real-time health data.

- As these devices become more interconnected, securing their communications and the data they collect is increasingly vital. The growing adoption of consumer health technology is expected to drive the demand for robust security solutions for wearable and external medical devices.

- Thus, according to market analysis, wearable and external medical devices are expected to see the fastest trend as healthcare moves towards more personalized and connected health solutions.

By Deployment Mode:

Based on deployment mode, the market is segmented into on-premise and cloud-based solutions.

The cloud-based deployment mode accounted for the largest revenue share in 2024.

- Cloud-based solutions offer flexibility, scalability, and remote access, making them ideal for healthcare organizations managing large numbers of medical devices.

- These solutions enable real-time monitoring and updates, improving security while reducing the need for on-site infrastructure.

- Cloud solutions also facilitate easier data sharing and collaboration among healthcare providers.

- As healthcare organizations increasingly migrate their data and operations to the cloud, the demand for cloud-based security solutions continues to grow.

- Therefore, according to market analysis, cloud-based solutions dominate the deployment mode segment, driven by their scalability and ease of access.

The on-premise deployment mode is anticipated to register the fastest CAGR during the forecast period.

- Despite the dominance of cloud-based solutions, on-premise solutions are expected to grow rapidly as some healthcare organizations prefer to maintain complete control over their security infrastructure.

- On-premise solutions provide added security for organizations concerned about the risks of storing sensitive data offsite.

- Thus, according to market analysis, on-premise solutions are expected to experience the fastest trend as organizations look for secure, localized options to protect their medical devices.

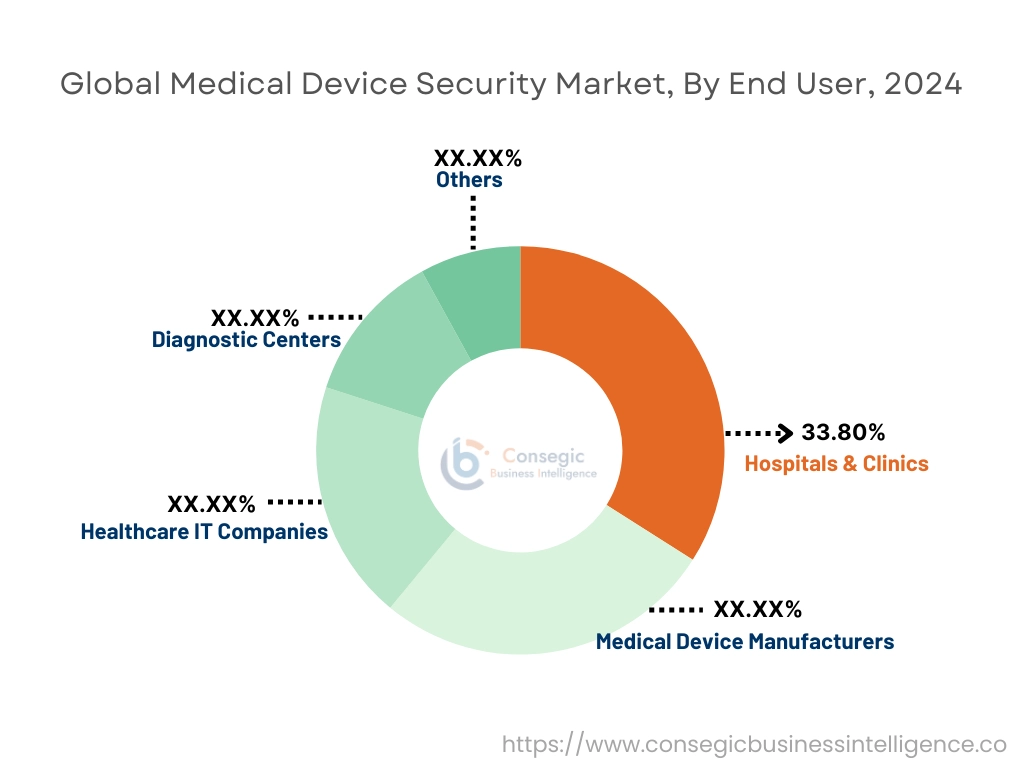

By End User:

Based on end-user, the market is segmented into hospitals & clinics, medical device manufacturers, healthcare IT companies, diagnostic centers, and others.

The hospitals & clinics segment accounted for the largest revenue share by 33.80% in 2024.

- Hospitals and clinics are the largest end-users of medical devices, and they require advanced security solutions to protect patient data and medical equipment from cyber threats.

- As medical devices become increasingly interconnected, the need for comprehensive security systems to safeguard sensitive health information and ensure device functionality has risen.

- This segment includes a wide range of devices used in patient care, diagnostics, and treatment, all of which require robust cybersecurity measures.

- Therefore, according to market analysis, hospitals & clinics remain the largest end-users of medical device security solutions, driven by the vast number of devices used in patient care.

The healthcare IT companies segment is anticipated to register the fastest CAGR during the forecast period.

- Healthcare IT companies provide critical infrastructure and services for managing medical devices, healthcare data, and network security.

- These companies are focused on developing and implementing advanced cybersecurity solutions to protect healthcare organizations from the growing threat of cyberattacks.

- The increased reliance on technology in healthcare and the need for specialized cybersecurity expertise are driving the rapid trend of this segment.

- Thus, according to market analysis, healthcare IT companies are expected to see the fastest growth as medical device security market demand for specialized security solutions in healthcare continues to rise.

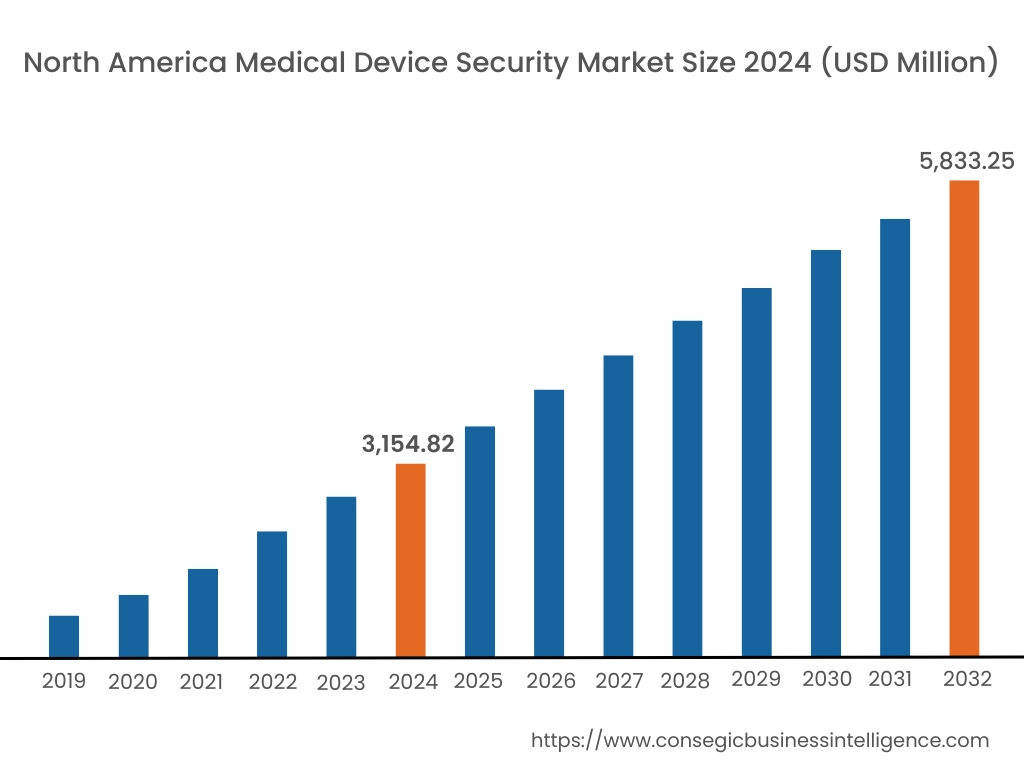

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

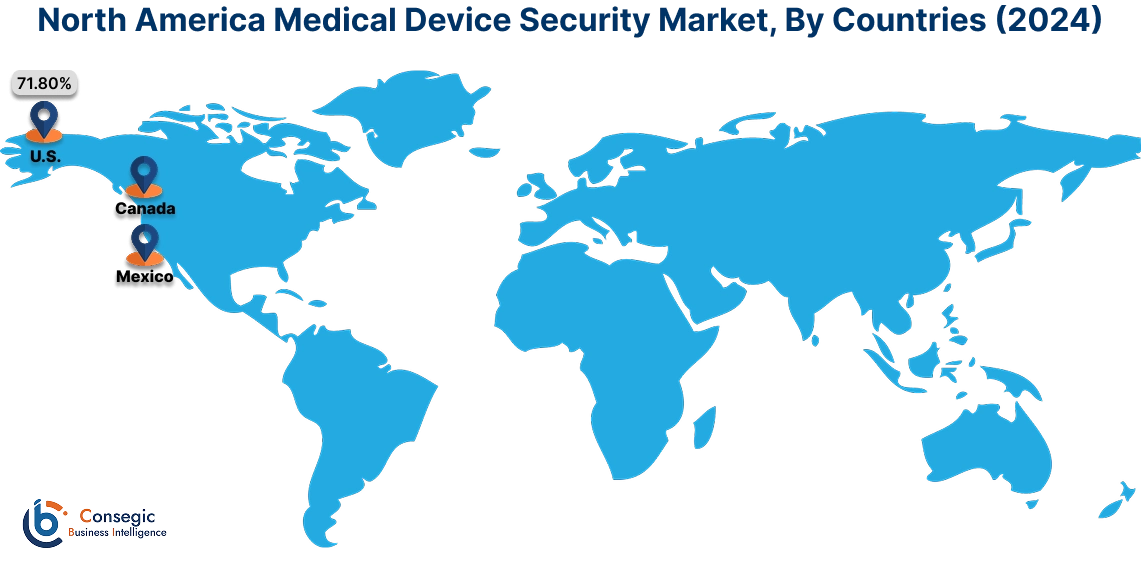

In 2024, North America was valued at USD 3,154.82 Million and is expected to reach USD 5,833.25 Million in 2032. In North America, the U.S. accounted for the highest share of 71.80% during the base year of 2024.

North America dominates the medical device security market due to the high adoption of advanced technologies and stringent regulatory frameworks. The United States, in particular, stands as a key player with an established healthcare system and significant investments in cybersecurity for medical devices. The rising number of cyberattacks on healthcare organizations fuels demand for robust security solutions. Additionally, regulations such as HIPAA and the FDA’s cybersecurity guidance play a critical role in shaping market trends. The presence of major healthcare institutions and security vendors further enhances market growth in this region.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 8.8% over the forecast period.

The Asia-Pacific region is experiencing rapid growth in the medical device security market, driven by the medical device security market expansion of healthcare infrastructure and increasing digitalization in healthcare systems. Countries like Japan, China, and India are focusing on integrating advanced medical technologies with greater emphasis on security. China, with its large population and growing healthcare sector, is witnessing heightened investments in secure medical device systems. However, challenges such as regulatory complexities and the varying pace of cybersecurity awareness across the region could impact market performance. Government initiatives to enhance cybersecurity awareness are expected to support future growth.

Europe holds a strong position in the medical device security market, supported by comprehensive regulatory standards, such as the EU Medical Device Regulation (MDR). The region has seen significant investments in securing medical devices against cyber threats. Leading countries, including Germany, the United Kingdom, and France, have advanced healthcare systems and are prioritizing cybersecurity to protect patient data. However, market challenges include the implementation of security solutions in smaller healthcare facilities and addressing regional disparities in cybersecurity infrastructure. Increased focus on patient privacy and data protection fuels medical device security market demand in this region.

The Middle East and Africa (MEA) region faces several challenges in the medical device security market, including limited cybersecurity infrastructure and healthcare digitization in some countries. However, the United Arab Emirates (UAE) and Saudi Arabia are making notable investments in healthcare technology, including secure medical devices. These countries aim to enhance their healthcare systems by integrating advanced digital solutions while improving data protection standards. Africa’s healthcare sector remains in the early stages of adopting comprehensive medical device security systems, with many countries focusing on building the necessary infrastructure to support future developments.

The medical device security market in Latin America is in its nascent stages, with several countries, including Brazil and Mexico, showing increased interest in cybersecurity for healthcare devices. The rise in digital health adoption and the need for protecting patient data have brought attention to securing medical devices. However, the region faces challenges such as a lack of awareness, regulatory inconsistencies, and insufficient investments in healthcare cybersecurity. Nevertheless, government and private sector efforts to improve digital health systems and data protection regulations will likely support market development in the coming years.

Top Key Players and Market Share Insights:

The Global Medical Device Security Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global Medical Device Security Market. Key players in the Medical Device Security industry include-

- Johnson & Johnson (United States)

- Medtronic PLC (Ireland)

- Resideo Technologies, Inc. (United States)

- Imprivata, Inc. (United States)

- Check Point Software Technologies Ltd. (Israel)

- GE Healthcare (United States)

- Philips Healthcare (Netherlands)

- Siemens Healthineers (Germany)

- AbbVie Inc. (United States)

- Biotronik (Germany)

Recent Industry Developments :

Partnerships & Collaborations:

- In August 2023, MedCrypt, a provider of proactive cybersecurity solutions for medical device manufacturers, partnered with NetRise, a company specializing in visibility into embedded device security. This collaboration focuses on creating and managing Software Bills of Materials (SBOMs) to help device makers proactively identify and address potential security risks, ensuring the safety and integrity of medical devices.

- In July 2023, Cynerio, a leader in healthcare IoT cybersecurity, joined forces with Check Point Software Technologies to provide comprehensive security for medical IoT devices. The integration of Cynerio's 360 Platform with Check Point's Quantum IoT Protect offers healthcare organizations enhanced device discovery, patch guidance, micro-segmentation, attack detection, and threat prevention capabilities.

- In April 2024, CloudWave renewed its Memorandum of Understanding with the U.S. Food and Drug Administration (FDA) to share critical threat intelligence concerning medical device security. This partnership aims to foster collaboration and communication to proactively mitigate cybersecurity threats in the healthcare and public health sectors.

Mergers and Acquisitions:

- In August 2024, Johnson & Johnson's purchase of V-Wave, a medical device maker, went up to $1.7 billion. This move aims to enhance J&J's portfolio in the heart disease market. The transaction includes an upfront payment of $600 million, with additional payments contingent on regulatory and commercial milestones.

Medical Device Security Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 17,998.29 Million |

| CAGR (2025-2032) | 8.3% |

| By Component |

|

| By Security Type |

|

| By Device Type |

|

| By Deployment Mode |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Medical Device Security Market? +

In 2024, the Medical Device Security Market was USD 9,510.82 million.

What will be the potential market valuation for the Medical Device Security Market by 2032? +

In 2032, the market size of Medical Device Security Market is expected to reach USD 17,998.29 million.

What are the segments covered in the Medical Device Security Market report? +

The component, security type, device type, deployment mode, and end-users are the segments covered in this report.

Who are the major players in the Medical Device Security Market? +

Johnson & Johnson (United States), Medtronic PLC (Ireland), GE Healthcare (United States), Philips Healthcare (Netherlands), Siemens Healthineers (Germany), AbbVie Inc. (United States), Biotronik (Germany), Resideo Technologies, Inc. (United States), Imprivata, Inc. (United States), Check Point Software Technologies Ltd. (Israel) are the major players in the Medical Device Security market.