- Summary

- Table Of Content

- Methodology

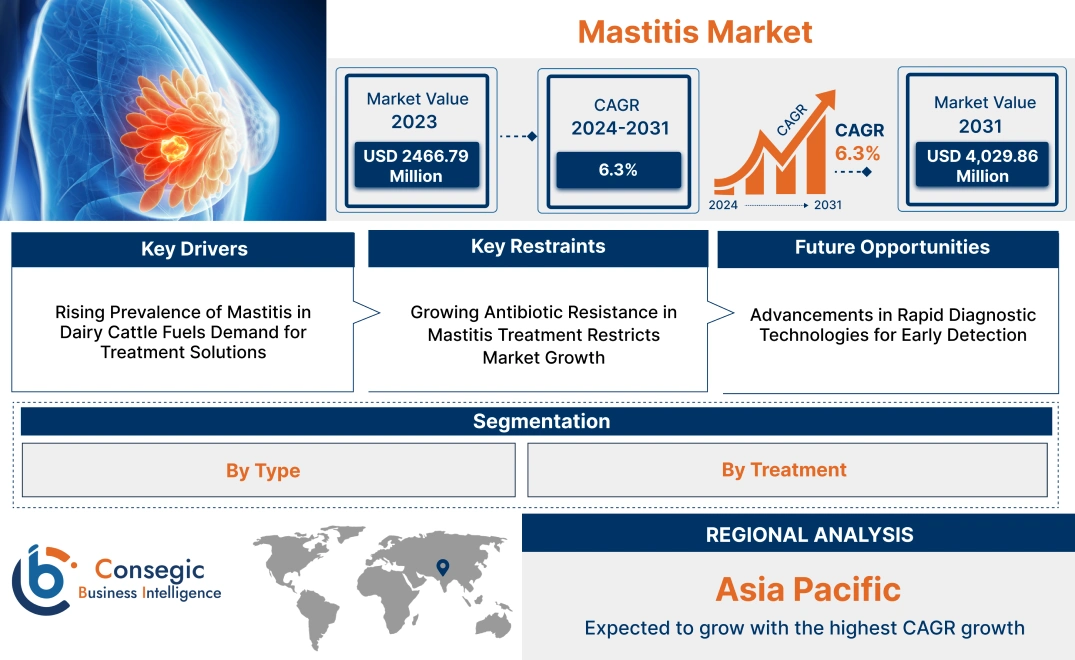

Mastitis Market Size:

Mastitis Market size is estimated to reach over USD 4,029.86 Million by 2031 from a value of USD 2466.79 Million in 2023 and is projected to grow by USD 2,578.93 Million in 2024, growing at a CAGR of 6.3% from 2024 to 2031.

Mastitis Market Scope & Overview:

The Mastitis therapeutics focuses on the diagnosis, treatment, and prevention of mastitis, an inflammatory condition of the mammary gland commonly affecting dairy animals and lactating women. This condition is caused by bacterial infections or physical injuries and can significantly impact milk production and quality. The treatments include antibiotics, pain relievers, anti-inflammatory drugs, and preventive solutions such as vaccines and teat sealants. Key characteristics of mastitis management solutions include rapid effectiveness, minimal side effects, and ease of application. The benefits of these treatments are improved animal health, enhanced milk yield, and reduced economic losses for dairy farmers. Applications span veterinary care for livestock and human healthcare for managing lactation mastitis. The end-users include veterinary clinics, dairy farms, and hospitals, driven by the rising prevalence of new mastitis market opportunities, increasing focus on animal health, and advancements in therapeutic and preventive solutions.

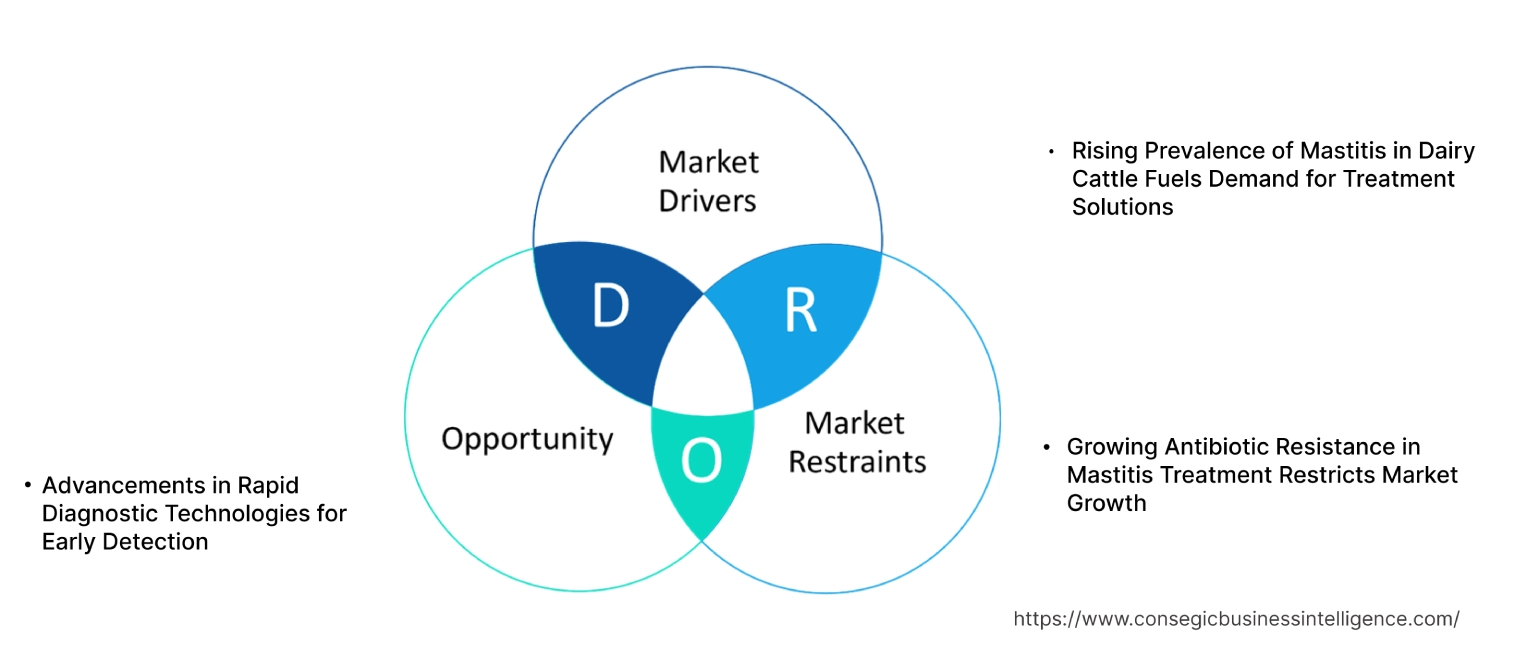

Mastitis MarketDynamics - (DRO) :

Key Drivers:

Rising Prevalence of Mastitis in Dairy Cattle Fuels Demand for Treatment Solutions

The increasing incidence of mastitis in dairy cattle is a critical driver of the mastitis market. It is one of the most common diseases affecting dairy cattle, significantly impacting milk production, quality, and overall farm profitability. Factors such as improper milking practices, poor farm hygiene, environmental stressors, and bacterial infections caused by pathogens like Escherichia coli and Staphylococcus aureus contribute to its high prevalence. Subclinical mastitis, often undetected due to the absence of visible symptoms, further exacerbates milk yield losses and herd health issues.

The rising development of effective mastitis management solutions, including intramammary antibiotics, non-steroidal anti-inflammatory drugs (NSAIDs), and advanced teat sealants, is driving the market. Additionally, the development of tailored veterinary care protocols and preventive strategies, such as post-milking teat disinfectants and improved housing conditions, is gaining traction. The economic burden of mastitis, coupled with increasing awareness among dairy farmers about early intervention and control measures, continues to drive innovation and adoption of treatment solutions globally.

Key Restraints :

Growing Antibiotic Resistance in Mastitis Treatment Restricts Market Growth

The growing prevalence of antibiotic-resistant bacterial strains in mastitis treatment poses a significant restraint for the market. Prolonged and indiscriminate use of antibiotics in dairy cattle has led to the emergence of multidrug-resistant pathogens, such as methicillin-resistant Staphylococcus aureus (MRSA), compromising the efficacy of traditional therapies. This resistance not only reduces the success of treatment but also raises concerns about the transfer of antibiotic residues to milk, impacting food safety and public health.

In human mastitis, similar challenges are observed, with resistance limiting the effectiveness of widely used antibiotics for lactational infections. Regulatory authorities worldwide are tightening restrictions on the use of antibiotics in livestock and encouraging alternative approaches, such as targeted antibiotic use and integrated disease management practices. While these measures aim to combat resistance, they also increase the cost and complexity of mastitis management, particularly for smaller dairy farms and healthcare providers, restricting market growth.

Future Opportunities :

Advancements in Rapid Diagnostic Technologies for Early Detection

The development of advanced diagnostic technologies offers transformative potential for the market by enabling early detection and targeted treatment. Traditional diagnostic methods for mastitis, such as milk culture testing, are time-consuming and may delay treatment initiation, leading to further complications. Recent advancements, including biosensors, molecular diagnostics, and point-of-care testing devices, provide real-time identification of specific pathogens causing mastitis. For instance, biosensors integrated into milking systems can detect somatic cell counts and microbial contamination, offering immediate alerts to farmers.

In human mastitis, innovations such as portable diagnostic kits and non-invasive imaging techniques enable healthcare providers to diagnose infections early and recommend appropriate therapies. These tools not only reduce reliance on empirical treatments but also mitigate the risk of antibiotic resistance by facilitating targeted drug administration. As these technologies become more accessible and cost-effective, they are expected to play a crucial role in improving disease outcomes and supporting sustainable mastitis management strategies.

Mastitis Market Segmental Analysis :

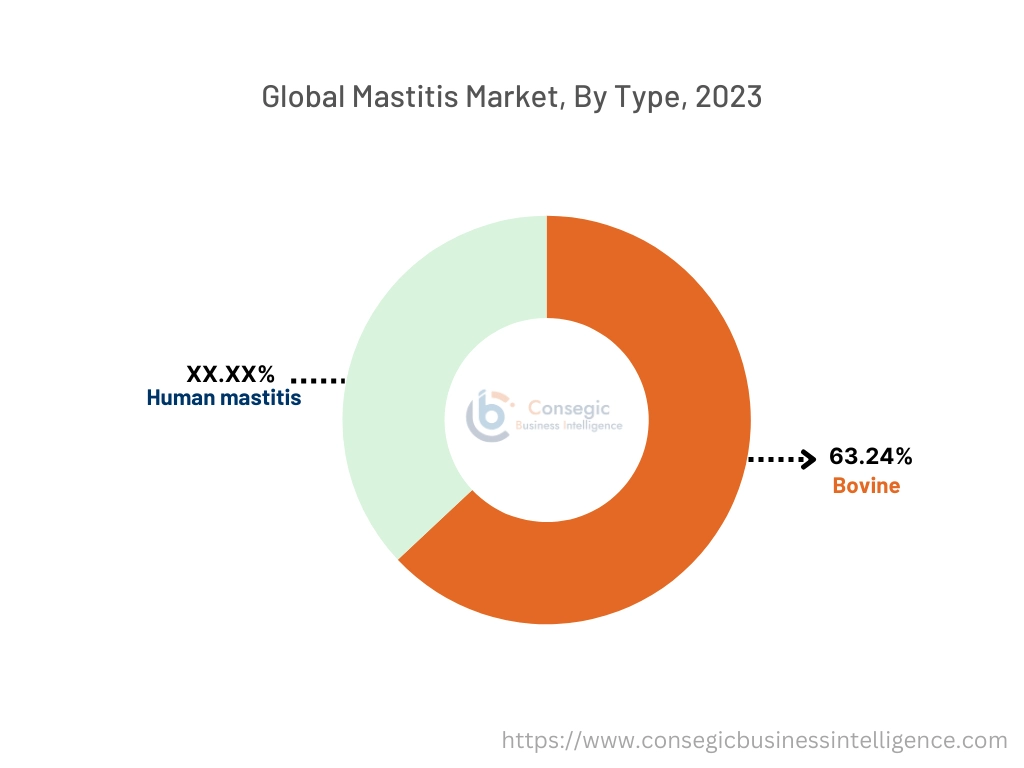

By Type:

Based on type, the market is segmented into bovine (contagious mastitis, environmental mastitis, and opportunist mastitis) and human mastitis (non-infectious mastitis and infectious mastitis).

The bovine mastitis segment accounted for the largest revenue of 63.24% in 2023.

- Bovine mastitis, which affects dairy cattle, is a major economic burden in the dairy industry due to its impact on milk yield and quality.

- Contagious mastitis, caused by pathogens such as Staphylococcus aureus and Streptococcus agalactiae, spreads within herds and requires stringent control measures.

- Environmental mastitis, often linked to unhygienic living conditions, is primarily caused by environmental pathogens like Escherichia coli and Klebsiella

- Opportunist mastitis, caused by minor pathogens, generally occurs when udder health is already compromised.

- The increasing adoption of automated milking systems with integrated mastitis detection and the development of pathogen-specific diagnostic tools are driving the market for bovine mastitis treatments.

- Bovine mastitis leads the market due to its widespread prevalence in the dairy industry, driving mastitis market trends for effective management solutions and advanced diagnostic technologies.

The human mastitis segment is anticipated to register the fastest CAGR during the forecast period.

- Human mastitis, predominantly affecting lactating women, includes non-infectious forms (caused by milk stasis or duct blockages) and infectious types (caused by bacterial infections such as Staphylococcus aureus).

- Non-infectious mastitis requires supportive care and management, while infectious mastitis necessitates antibiotics and proper lactation techniques.

- Increased awareness among lactating women and advancements in mastitis management protocols, including improved pain management and targeted antibiotic therapies, are boosting the surge of this segment.

- Human mastitis analysis is expected to grow rapidly, driven trends by heightened awareness and advancements in treatment approaches, particularly in postnatal care facilities.

By Treatment:

Based on treatment, the market is segmented into bovine (antibiotics and vaccines) and human mastitis (pain relievers and antibiotics) treatments.

The antibiotics segment in bovine mastitis accounted for the largest revenue share in 2023.

- Antibiotics remain the primary treatment for bacterial mastitis in cattle, targeting both contagious and environmental pathogens.

- Long-acting intramammary formulations are widely used to ensure effective pathogen clearance during lactation and the dry period.

- However, rising concerns over antimicrobial resistance (AMR) have led to stricter regulations and increased focus on alternative therapies, including vaccines and probiotics.

- The development of pathogen-specific antibiotics and targeted therapies further enhances treatment efficacy.

- Antibiotics dominate the trends for bovine mastitis treatment market analysis, driven by their effectiveness in managing bacterial infections, while regulatory focus on AMR is spurring innovation in alternative therapies.

The pain relievers segment in human mastitis is anticipated to register the fastest CAGR during the forecast period.

- Pain relievers, including nonsteroidal anti-inflammatory drugs (NSAIDs), are widely used to manage the discomfort and inflammation associated with both infectious and non-infectious mastitis.

- Increasing focus on improving the quality of life for lactating women and the growing availability of over-the-counter (OTC) NSAIDs are boosting advancement in this segment.

- The incorporation of pain management as an integral part of mastitis treatment protocols further supports mastitis market growth.

- Pain reliever’s analysis is expected to grow trends rapidly, driven by their essential role in improving the quality of life for lactating women experiencing mastitis.

By End-User:

Based on end-users, the market is segmented into veterinary centers and hospitals & clinics.

The veterinary centers segment accounted for the largest revenue share in 2023.

- Veterinary centers play a critical role in diagnosing and managing bovine mastitis, offering services like milk culture testing, treatment protocols, and herd management strategies.

- The increasing adoption of precision livestock farming and automated mastitis detection systems in veterinary centers is driving the mastitis market demand for treatment.

- Additionally, the integration of advanced diagnostic tools and tailored herd health programs in these facilities supports market surge.

- Veterinary centers dominate the market trends, driven by their role in providing comprehensive mastitis management solutions for dairy cattle.

The hospitals & clinics segment is anticipated to register the fastest CAGR during the forecast period.

- Hospitals and clinics are key end-users for human mastitis management, particularly for severe cases requiring antibiotics and specialized care.

- The growing awareness of mastitis-related complications among healthcare providers and advancements in postnatal care are driving the appeal for hospital-based treatments.

- Additionally, increasing investments in maternal healthcare infrastructure globally support the surge of this segment.

- Hospitals & clinics are expected to grow rapidly, supported by increasing trends and awareness of mastitis-related complications and advancements in postnatal care services.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

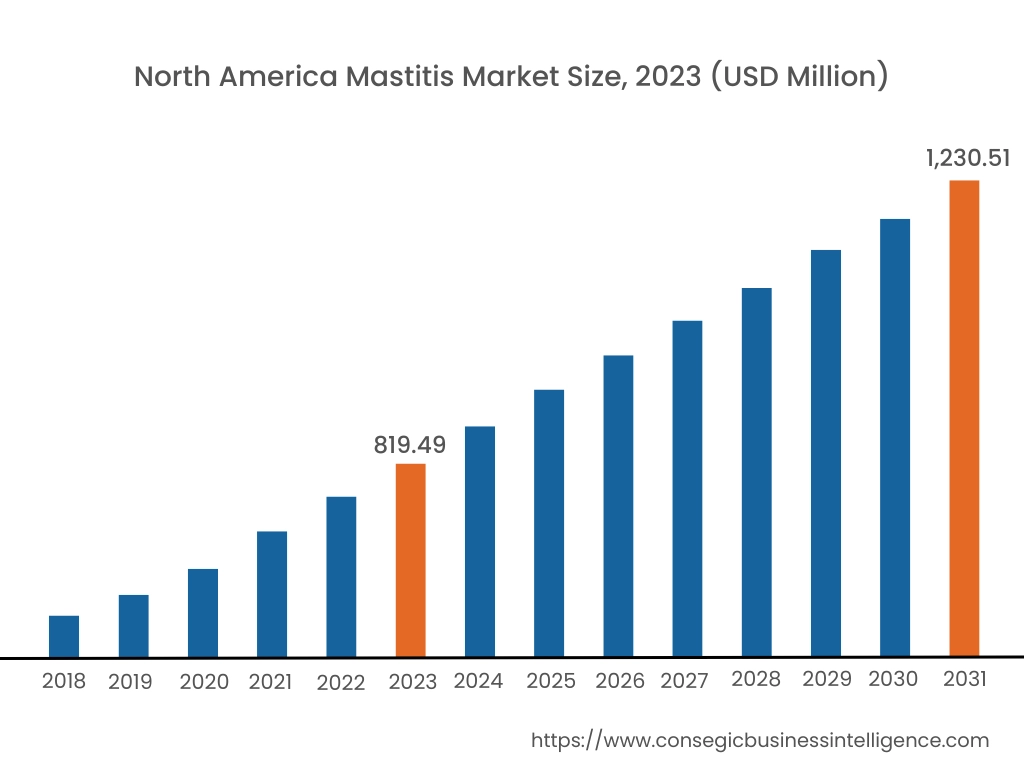

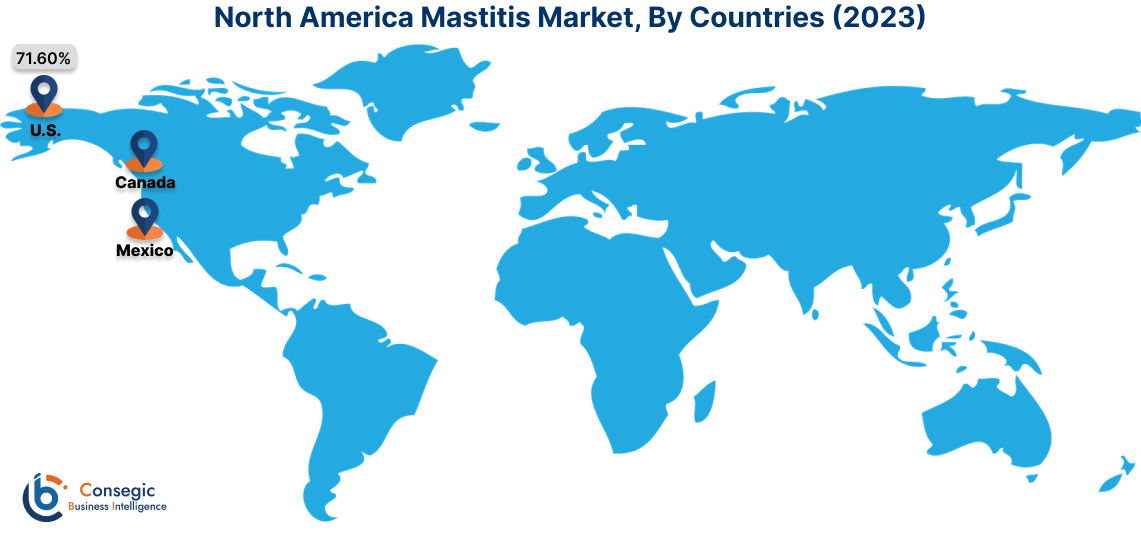

In 2023, North America accounted for the highest market share at 33.24% and was valued at USD 819.49 Million and is expected to reach USD 1,230.51 Million in 2031. In North America, the U.S. accounted for the highest share of 71.60% during the base year of 2023. North America dominates the market due to its well-developed dairy farming industry and advanced veterinary healthcare infrastructure. The U.S. leads the region with a high prevalence of mastitis cases in dairy cattle and significant investments in treatment and prevention methods. The adoption of antibiotics, vaccines, and advanced diagnostic tools is widespread among large dairy farms to improve milk quality and reduce economic losses. Canada also contributes significantly, focusing on mastitis prevention through herd management programs and the use of advanced diagnostic technologies. However, regulatory restrictions on antibiotic use in animals may challenge mastitis market expansion in the region.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 5.6% over the forecast period. The market is driven by the increasing prevalence of mastitis in dairy cattle and expanding dairy farming operations in China, India, and Australia. China’s rapidly growing dairy industry adopts advanced diagnostic tools and therapeutic solutions to improve milk production and quality. India’s large dairy sector is focusing on mastitis management through affordable antibiotics and herd management practices, supported by government initiatives to enhance milk safety. Australia emphasizes the use of vaccines and advanced diagnostic techniques in its highly organized dairy industry. However, limited awareness among small-scale farmers and inadequate veterinary healthcare infrastructure in rural areas pose challenges.

Europe holds a significant share in the mastitis market, supported by a strong dairy farming sector and stringent regulations on milk quality. Countries like Germany, France, and the UK are leading contributors. Germany’s focus on preventive veterinary care drives the adoption of vaccines and diagnostic tools for mastitis management. France emphasizes sustainable dairy farming practices, including the use of natural remedies and herd health monitoring systems to minimize antibiotic usage. The UK’s increasing focus on reducing antimicrobial resistance encourages the adoption of alternative treatments such as probiotics and advanced diagnostic technologies. However, strict regulatory frameworks on veterinary medicines may limit the use of certain treatments.

The Middle East & Africa region is witnessing steady advancements in the mastitis market, driven by increasing investments in dairy farming and rising awareness of milk quality standards. Countries like Saudi Arabia and the UAE are focusing on adopting advanced veterinary solutions, including vaccines and diagnostic tools, to reduce mastitis prevalence in large-scale dairy farms. In Africa, South Africa is emerging as a key market, with growing adoption of antibiotics and herd health monitoring systems to manage mastitis in dairy cattle. However, limited access to veterinary care and lack of awareness in small-scale farms remain barriers to market growth in certain parts of the region.

Latin America is an emerging market for mastitis treatment and prevention, with Brazil and Argentina leading the region due to their large dairy farming industries. Brazil emphasizes the use of antibiotics and vaccines for mastitis management to enhance milk production efficiency. Argentina is focusing on improving herd health through advanced diagnostic tools and better farm management practices. The region also sees growing awareness of sustainable dairy farming, encouraging the adoption of preventive measures. However, economic instability and inconsistent veterinary healthcare infrastructure may hinder market development across the region.

Top Key Players & Market Share Insights:

The Mastitis market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Mastitis market. Key players in the Mastitis industry include -

- Merck & Co., Inc. (United States)

- Zoetis Inc. (United States)

- Vetoquinol S.A. (France)

- Norbrook Laboratories (United Kingdom)

- Huvepharma (Bulgaria)

- Boehringer Ingelheim GmbH (Germany)

- Bayer AG (Germany)

- Elanco Animal Health (United States)

- Ceva Santé Animale (France)

- West Way Health (Ireland)

Recent Industry Developments :

Fundings:

- In September 2022, The USDA's National Institute of Food and Agriculture funded initiatives focused on developing comprehensive mastitis control solutions for organic dairy farms. These projects prioritize preventive measures and management strategies during the dry period to reduce mastitis cases and enhance milk quality.

Mastitis Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 4,029.86 Million |

| CAGR (2024-2031) | 6.3% |

| By Type |

|

| By Treatment |

|

| By Key Players |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Mastitis Market? +

Mastitis Market size is estimated to reach over USD 4,029.86 Million by 2031 from a value of USD 2466.79 Million in 2023 and is projected to grow by USD 2,578.93 Million in 2024, growing at a CAGR of 6.3% from 2024 to 2031.

What specific segmentation details are covered in the Mastitis Market report? +

The Mastitis market report includes segmentation details for type (bovine mastitis and human mastitis), treatment (antibiotics, vaccines, pain relievers), end-user (veterinary centers, hospitals & clinics), and region.

Which segment is expected to register the fastest growth in the Mastitis Market? +

The human mastitis segment is anticipated to register the fastest CAGR during the forecast period, driven by increased awareness and advancements in treatment approaches, particularly in postnatal care facilities.

Who are the major players in the Mastitis Market? +

The major players in the Mastitis market include Merck & Co., Inc. (USA), Zoetis Inc. (USA), Boehringer Ingelheim International GmbH (Germany), Elanco Animal Health (USA), and Vetoquinol SA (France).