- Summary

- Table Of Content

- Methodology

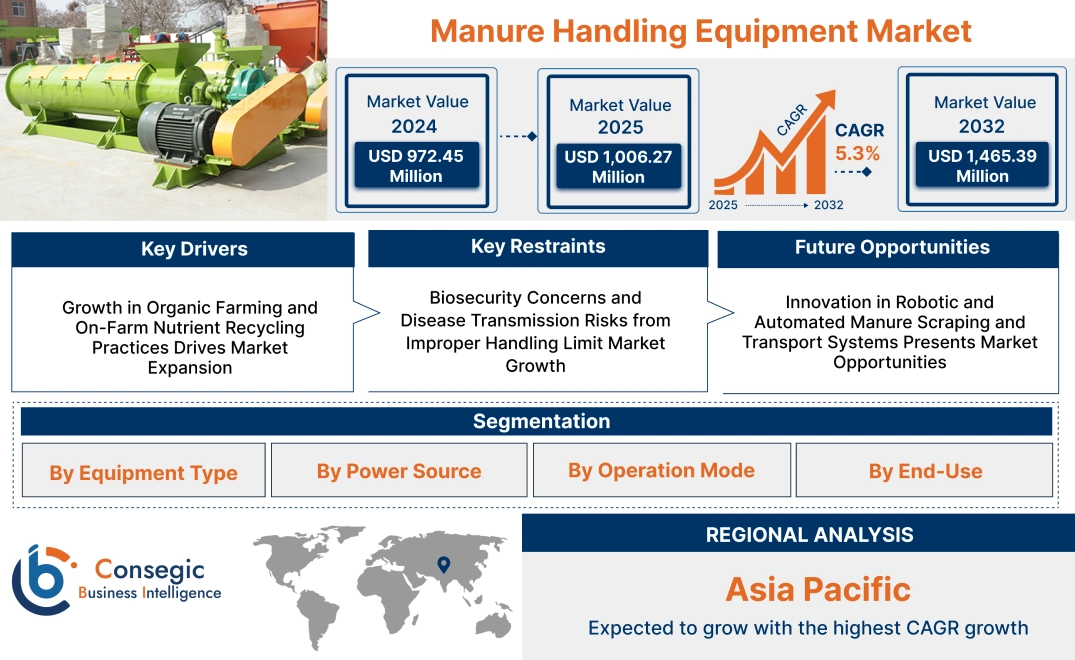

Manure Handling Equipment Market Size:

Manure Handling Equipment Market size is estimated to reach over USD 1,465.39 Million by 2032 from a value of USD 972.45 Million in 2024 and is projected to grow by USD 1,006.27 Million in 2025, growing at a CAGR of 5.3% from 2025 to 2032.

Manure Handling Equipment Market Scope & Overview:

Manure handling equipment is a variety of machinery utilized for the collection, processing, transport, and distribution of livestock waste effectively. Some of the common systems involve scrapers, separators, agitators, pumps, spreaders, and storage facilities—each designed to handle solid and liquid manure in various agricultural operations.

These systems are built using corrosion-proof materials and include hydraulics, automated controls, and precision dispensing systems to simplify waste management. Modular design and adjustable capacity configurations enable the customization of equipment based on farm size and livestock density.

Manure management equipment makes hygienic conditions possible, decreases labor input, and allows recycling of nutrients through proper waste distribution in fields. Through support of continuous waste flow, odor management, and low environmental disturbance, it improves productivity in dairy, poultry, and swine production. Through its inclusion in farm infrastructure, it aids the adherence to regulatory requirements and encourages sustainable nutrient management in intensive and extensive livestock systems.

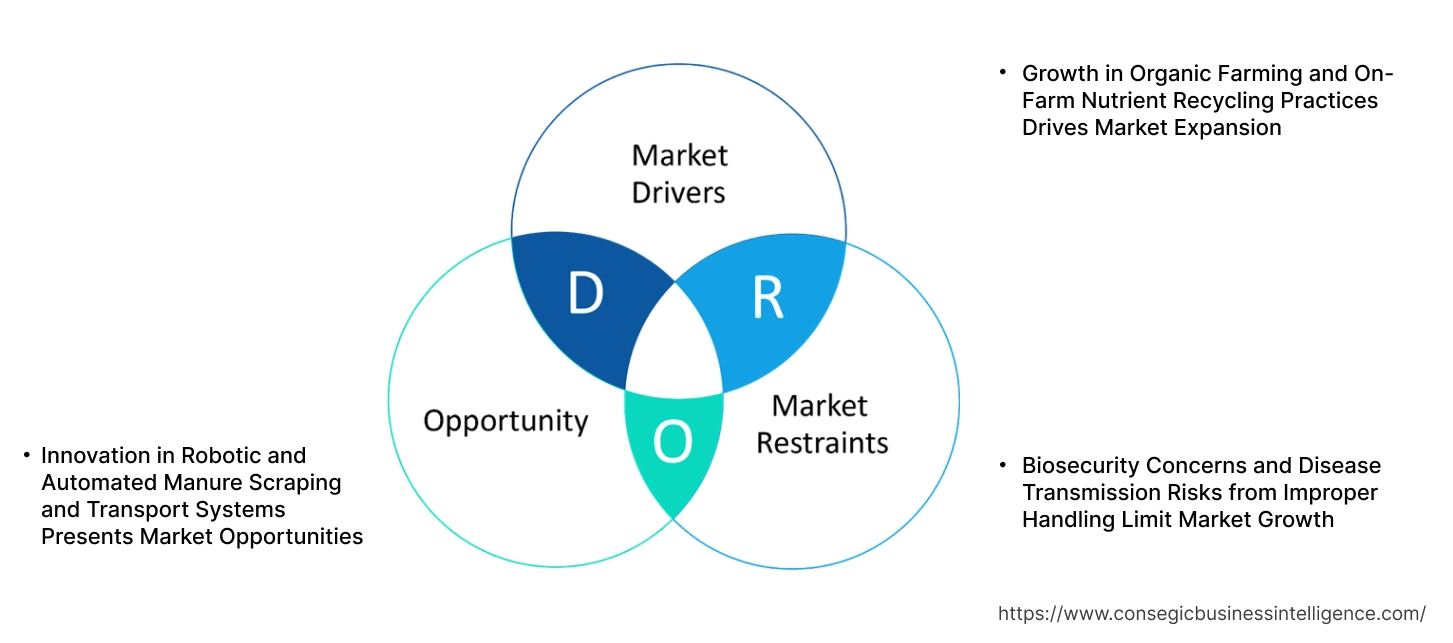

Manure Handling Equipment Market Dynamics - (DRO) :

Key Drivers:

Growth in Organic Farming and On-Farm Nutrient Recycling Practices Drives Market Expansion

The growing trend toward organic and regenerative production methods is propelling adoption of equipment that facilitates effective use of manure. Livestock manure is an essential input for soil fertility in organic systems, and farmers are investing in equipment that facilitates composting, aeration, and even application across the field. Recycling nutrients on the farm helps farmers reduce reliance on synthetic fertilizers while enhancing soil structure and microbial health. Environmental sustainability of nutrient management is needed particularly strongly in Western Europe, North America, and regions of Asia where organic certification and ecologging affect access to markets. Windrow turners, compost spreaders, and slurry mixers are equipment that promote nutrient retention and minimize odor emissions. With circular nutrient strategies on more farms, the demand for sophisticated manure processing equipment is increasing, thereby driving the continued manure handling equipment market expansion.

Key Restraints:

Biosecurity Concerns and Disease Transmission Risks from Improper Handling Limit Market Growth

Poor sanitation during manure management activities poses the threat of cross-contamination and disease transfer throughout livestock operations. Pathogens such as Salmonella, E. coli, and avian influenza tend to be transferred by common equipment or inadequately cleaned spreaders and tankers. In their transit among barns or farms without disinfection, manure acts as a vector for outbreaks with negative consequences on animal health and compliance with regulations. During disease-sensitive periods, farms reduce or suspend equipment use to avoid biosecurity breaches, decreasing system utilization and replacement demand. High-risk zones also face stricter operational protocols, increasing complexity and operating costs. Despite the rising need for waste management efficiency, these health concerns create adoption hesitancy in sensitive livestock environments, ultimately restraining manure handling equipment market growth.

Future Opportunities :

Innovation in Robotic and Automated Manure Scraping and Transport Systems Presents Market Opportunities

Manure management automation is becoming an important solution to intensive livestock facilities' labor shortage and hygiene issues. Robotic scrapers in alleyways, automatic slurry cleaners, and conveyor transport systems are being implemented in new dairy barns and pig facilities to allow continuous removal of waste with reduced manual intervention. The technologies cut labor dependence, enhance barn cleanliness, and promote uniform bedding conditions—boosting animal welfare as a whole. Integration with mobile monitoring software and sensor-based tracking systems offers real-time performance monitoring and predictive maintenance functions. There is increasing demand for precision-controlled, low-maintenance systems in Europe, North America, and sophisticated operations in Asia. With increasing scale and modernization of livestock operations, the adoption of robotic and automated handling equipment is opening up huge manure handling equipment market opportunities driven by necessity and growth in mechanized livestock management.

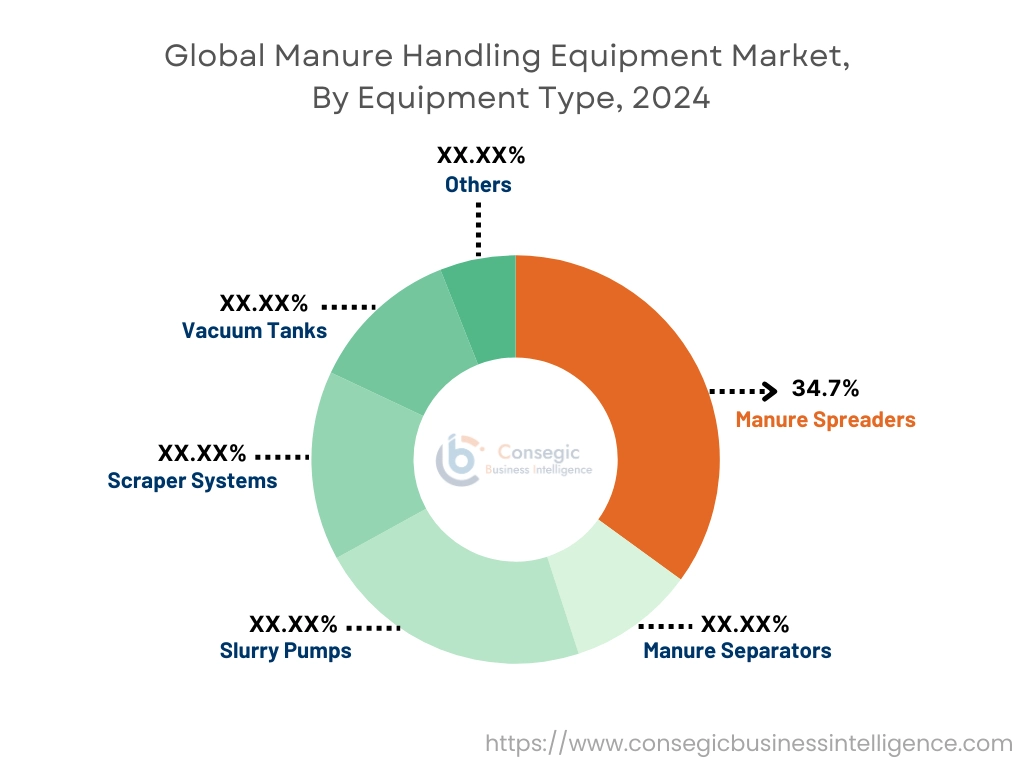

Manure Handling Equipment Market Segmental Analysis :

By Equipment Type:

Based on equipment type, the market is segmented into manure spreaders, manure separators, slurry pumps, scraper systems, vacuum tanks, and others.

The manure spreaders segment accounted for the largest manure handling equipment market share of 34.7% in 2024.

- Manure spreaders are widely used for distributing manure evenly across fields, enhancing soil fertility and nutrient cycling.

- These systems are favored in both livestock-heavy and mixed farming regions due to their operational efficiency and large capacity.

- Availability of broadcast, vertical beaters, and side discharge designs caters to diverse farm sizes and manure types.

- As per the manure handling equipment market analysis, spreaders dominate due to their critical role in nutrient management and field productivity.

The slurry pumps segment is projected to register the fastest CAGR during the forecast period.

- Slurry pumps are essential for transferring liquid manure from storage pits to tanks or treatment facilities, improving waste flow efficiency.

- Advanced models with remote control, auto-priming, and corrosion-resistant components are gaining traction.

- Their importance is increasing in large-scale dairy and swine farms, particularly in countries adopting lagoon-based storage.

- According to manure handling equipment market trends, slurry pump adoption is expanding due to stringent waste handling standards.

By Power Source:

Based on power source, the market is segmented into hydraulic, electric, PTO-driven, and mechanical.

The PTO-driven segment held the largest revenue share in 2024.

- PTO (Power Take-Off) systems are commonly used with tractors to operate spreaders, pumps, and agitators on medium to large farms.

- These systems are known for their simplicity, durability, and compatibility with existing farm equipment.

- Their affordability and low maintenance make them highly suitable for small and mid-sized operations.

- As per manure handling equipment market trends, PTO-driven units remain preferred due to their flexible application across multiple implements.

The electric segment is projected to grow at the fastest CAGR during the forecast period.

- Electric-powered manure handling systems offer energy efficiency, low noise, and reduced emissions, aligning with sustainable farming goals.

- These systems are being adopted in confined operations and automated barn setups with consistent power availability.

- Technological advances in electric motor efficiency and smart controls are enhancing usability and performance.

- Therefore, electrification is contributing to the manure handling equipment market expansion in progressive agricultural systems.

By Operation Mode:

Based on operation mode, the market is segmented into automatic, semi-automatic, and manual.

The semi-automatic segment accounted for the largest manure handling equipment market share in 2024.

- Semi-automatic equipment balances cost and labor savings, making it ideal for medium-scale farms transitioning from manual systems.

- Operators retain control over application rates and movement while benefiting from mechanical assistance.

- This mode supports integration with rotary dairies and mid-sized poultry barns without major infrastructure upgrades.

- As per the manure handling equipment market analysis, semi-automatic systems are dominant due to their practicality and versatility.

The automatic segment is expected to grow at the fastest CAGR during the forecast period.

- Automatic manure systems enhance biosecurity, labor efficiency, and environmental compliance in high-volume livestock operations.

- Integration with IoT sensors enable scheduled cleaning, load monitoring, and alerts for clogs or malfunctions.

- These systems are favored by large dairy and pig farms looking to optimize waste handling and minimize human intervention.

- For instance, in September 2024, Lely introduced the sand flush, an accessory for the Discovery Collector manure robots to enable their utilization in dairy barns with sand bedding. The automatic robot cleans the barns by collecting and dumping the manure into pits. The product offers flexibility in terms of barn set-up and cleaning schedule.

- Hence, automation is key to scaling operations, improving animal welfare and meeting manure handling equipment market demand.

By End-Use:

Based on end-use, the manure handling equipment market is segmented into individual farms, cooperative farms, corporate farms, and others.

The individual farms segment held the largest revenue share in 2024.

- Small and family-run farms form the backbone of livestock production in emerging and developed economies alike.

- These operations commonly use PTO-driven and semi-automatic systems tailored for limited acreage and daily manure volumes.

- Growing awareness of soil health and organic fertilization supports equipment use among individual operators.

- Affordability and reliability ensured by individual farms are driving consistent manure handling equipment market growth.

The corporate farms segment is projected to witness the fastest CAGR during the forecast period.

- Large-scale, vertically integrated farms are investing in comprehensive waste management systems to meet sustainability and regulatory goals.

- These entities deploy advanced technologies such as automated scrapers, robotic monitoring, and centralized slurry processing.

- The requirement is rising for high-capacity spreaders and separators integrated with nutrient recovery and biogas production systems.

- Thus, corporate farming structures are leading innovation adoption and driving market modernization, as well as contributing to the manure handling equipment market demand.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

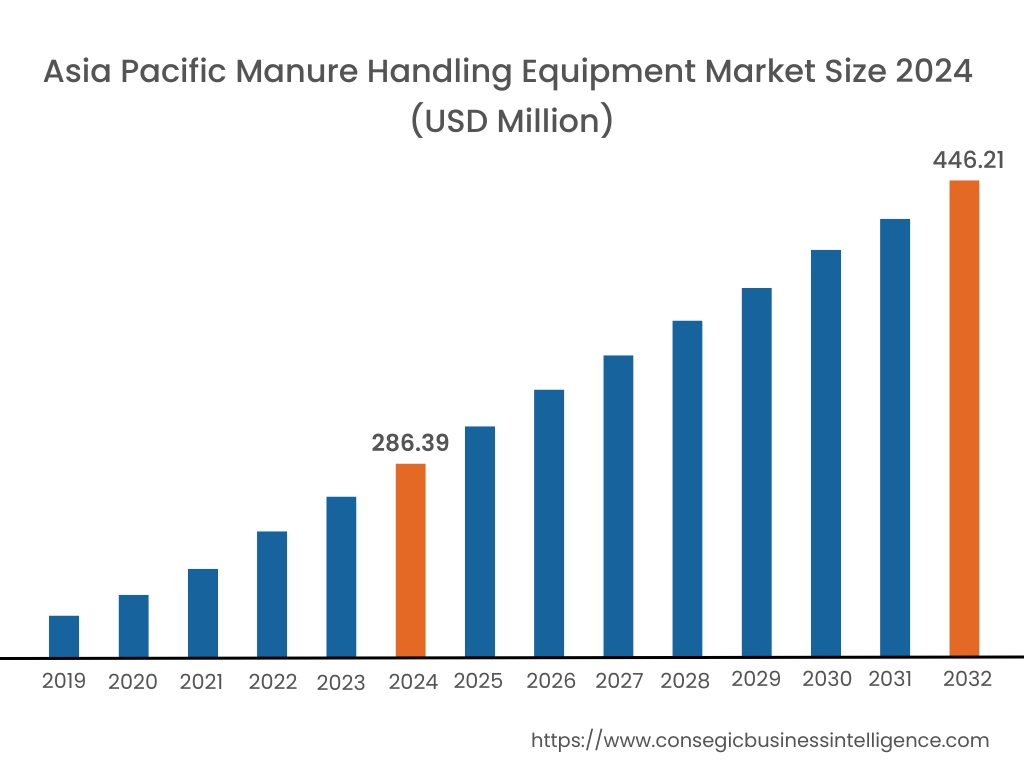

Asia Pacific region was valued at USD 286.39 Million in 2024. Moreover, it is projected to grow by USD 297.19 Million in 2025 and reach over USD 446.21 Million by 2032. Out of this, China accounted for the maximum revenue share of 32.2%. The Asia-Pacific region is the most rapidly growing area, driven by very fast-growing livestock populations in China, India, and Southeast Asia. Market research indicates that the growing concentration of dairy and poultry farms, coupled with water pollution and odor concerns, is propelling the transition from manual disposal systems to semi-automatic and fully automatic systems. In nations such as China, regulations for centralized waste treatment in peri-urban areas are stimulating investment in slurry pumps, separators, and bio-digesters. Japan and South Korea, however, are embracing slim robotic solutions appropriate for small-space applications. The opportunity for manure handling equipment in this region is additionally facilitated by government incentives encouraging rural farm modernization.

North America is estimated to reach over USD 474.93 Million by 2032 from a value of USD 322.57 Million in 2024 and is projected to grow by USD 333.15 Million in 2025. North America is at the forefront of technological maturity for manure management systems, especially in the United States and Canada where large-scale dairy, beef, and swine operations are common. Market analysis indicates high usage of mechanized scrapers, vacuum tankers, and slurry injectors to improve labor efficiency and minimize nutrient runoff. Strict environmental regulations—especially regarding phosphorus and nitrogen leaching—are encouraging livestock operators to upgrade to precision spreading and storage systems. Moreover, the inclusion of anaerobic digesters and nutrient recovery units in manure handling processes is facilitating sustainability goals. Ongoing development is prompted by financing for on-farm sustainability enhancement and demand to reduce the environmental footprint of large-scale animal feeding operations.

Europe has a regulation-dominated environment, with manure management being heavily dictated by EU directives like the Nitrates Directive and the Farm to Fork strategy. Nations such as the Netherlands, Germany, and Denmark are leaders in using advanced containment, separation, and spreading technologies. Market research suggests that adherence to nutrient application restrictions and greenhouse gas reduction levels is driving the adoption of enclosed systems and slurry treatment equipment. Demand for mobile and compact machinery is also on the rise for small to mid-sized farms that want to decrease emissions while enjoying operational flexibility. The European manure handling equipment industry is increasingly supporting the region's wider climate neutrality targets.

Latin America is experiencing increasing adoption, especially in Brazil, Argentina, and Chile, where intensive livestock production and export-based agribusinesses prevail. Market analysis points towards higher investment in manure spreaders, composting units, and storage tanks as farms address soil health issues and sustainable certification demands. As more producers look to maintain nutrients for applications to crops and minimize chemical fertilizer use, need for complete manure nutrient management solutions grows. Regional development schemes and private-public partnerships are also contributing to making equipment more readily available to medium and large farms.

The Middle East and Africa are slowly increasing their adoption of mechanized manure systems, mainly in countries with developing dairy and poultry sectors. South Africa, Egypt, and Saudi Arabia are leading the charge, incorporating waste management into intensive agriculture operations. Market analysis reveals that water shortages and land degradation are driving the need for growing interest in dry manure spreading, composting, and nutrient recycling systems. Still, infrastructure constraints and limited technical training continue to be hindrances. Regardless of these hurdles, the manure handling equipment market opportunity exists through focused development programs encouraging climate-resilient agriculture and better farm hygiene standards.

Top Key Players and Market Share Insights:

The manure handling equipment market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global manure handling equipment market. Key players in the manure handling equipment industry include -

- GEA Group (Germany)

- Bauer Group (Austria)

- Schauer Agrotronic GmbH (Austria)

- JOZ B.V. (Netherlands)

- Daritech (USA)

- Lely (Netherlands)

- Vogelsang GmbH & Co. KG (Germany)

- BouMatic (USA)

- Pellon Group Oy (Finland)

- DeLaval Inc. (Sweden)

Recent Industry Developments :

Acquisitions:

- In June 2023, Oxbo, known for its specialty harvesting and controlled application technology, acquired the hay and forage equipment manufacturer H&S Manufacturing. This enabled them to deliver enhanced value to clients and optimize farming technologies.

Manure Handling Equipment Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 1,465.39 Million |

| CAGR (2025-2032) | 5.3% |

| By Equipment Type |

|

| By Power Source |

|

| By Operation Mode |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Manure Handling Equipment Market? +

Manure Handling Equipment Market size is estimated to reach over USD 1,465.39 Million by 2032 from a value of USD 972.45 Million in 2024 and is projected to grow by USD 1,006.27 Million in 2025, growing at a CAGR of 5.3% from 2025 to 2032.

What specific segmentation details are covered in the Manure Handling Equipment Market report? +

The Manure Handling Equipment market report includes specific segmentation details for equipment type, power source, operation mode and end-use.

What are the end-use of the Manure Handling Equipment Market? +

The end-use of the Manure Handling Equipment Market are individual farms, cooperative farms, corporate farms, and others.

Who are the major players in the Manure Handling Equipment Market? +

The key participants in the Manure Handling Equipment market are GEA Group (Germany), Bauer Group (Austria), Lely (Netherlands), Vogelsang GmbH & Co. KG (Germany), BouMatic (USA), Pellon Group Oy (Finland), DeLaval Inc. (Sweden), Schauer Agrotronic GmbH (Austria), JOZ B.V. (Netherlands) and Daritech (USA).