- Summary

- Table Of Content

- Methodology

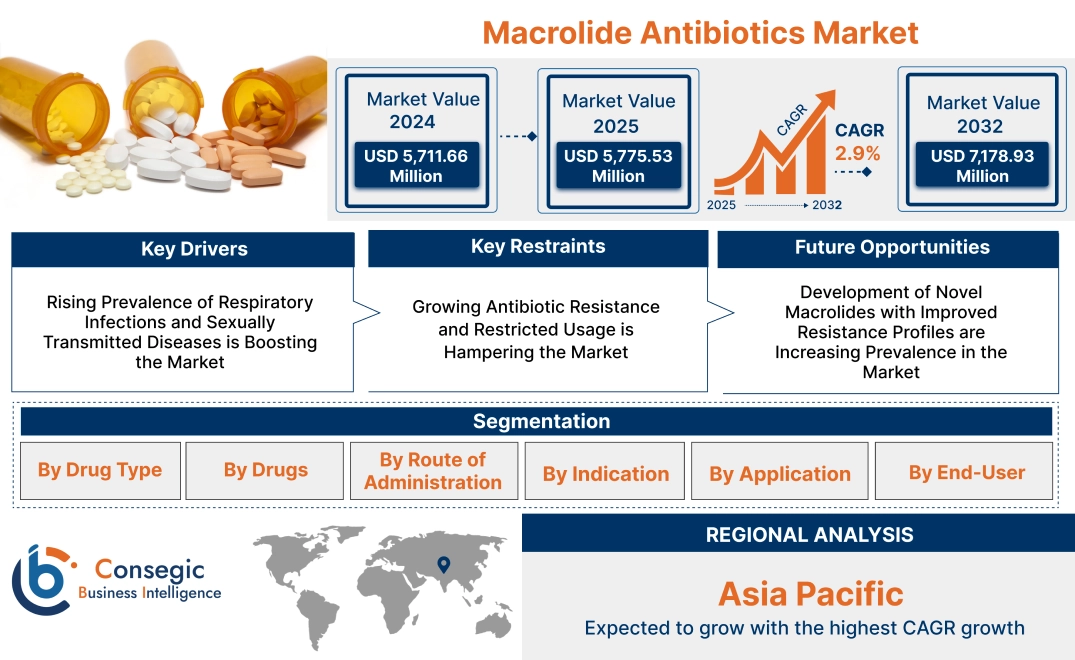

Macrolide Antibiotics Market Size:

Macrolide Antibiotics Market size is estimated to reach over USD 7,178.93 Million by 2032 from a value of USD 5,711.66 Million in 2024 and is projected to grow by USD 5,775.53 Million in 2025, growing at a CAGR of 2.9% from 2025 to 2032.

Macrolide Antibiotics Market Scope & Overview:

Macrolide antibiotics are a class of antibacterial agents known for their effectiveness against a wide range of bacterial infections. Macrolides, including erythromycin, azithromycin, and clarithromycin, are widely used to treat respiratory infections, skin conditions, and sexually transmitted infections due to their bacteriostatic properties and ability to inhibit bacterial protein synthesis.

Its key characteristics include broad-spectrum activity, high tissue penetration, and relatively low toxicity. The benefits include effective treatment of bacterial infections, shorter treatment durations, and reduced risk of antibiotic resistance when used appropriately.

Applications span respiratory tract infections, soft tissue infections, and prophylaxis in certain conditions such as rheumatic fever. End-users include hospitals, clinics, and retail pharmacies, driven by the rising prevalence of bacterial infections, growing awareness about antimicrobial stewardship, and ongoing research into macrolide derivatives to address antibiotic resistance.

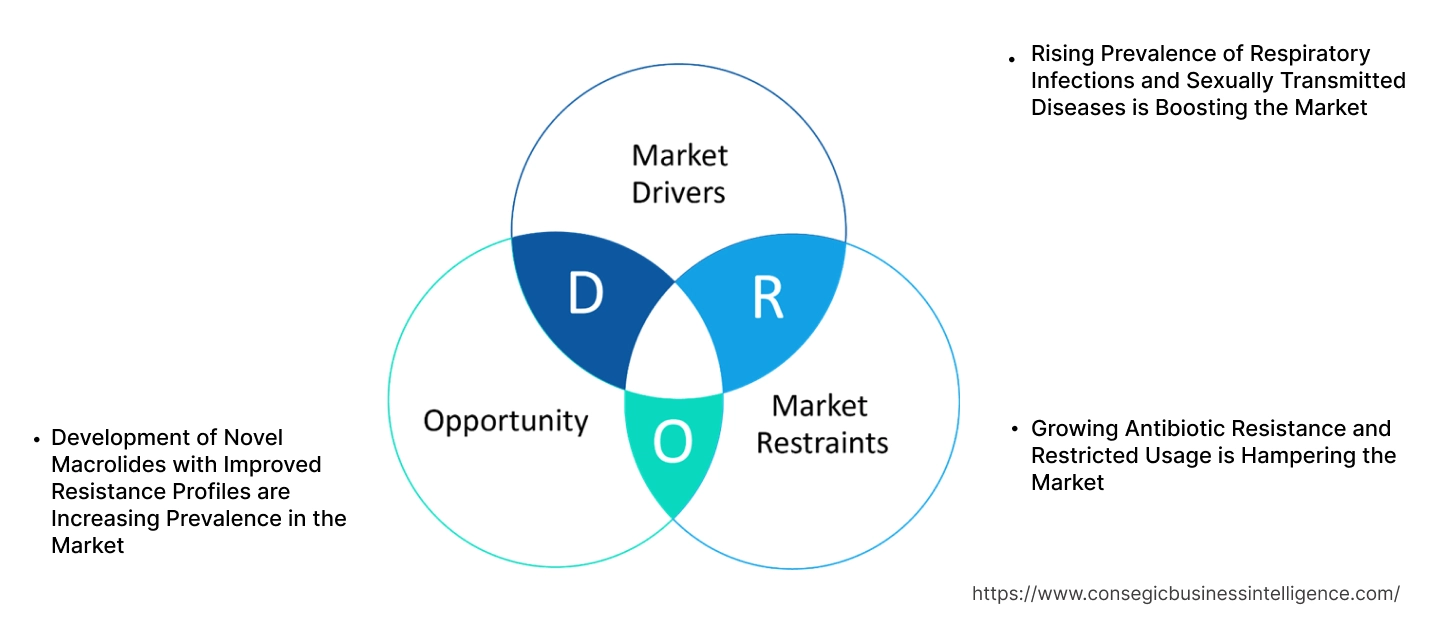

Macrolide Antibiotics Market Dynamics - (DRO) :

Key Drivers:

Rising Prevalence of Respiratory Infections and Sexually Transmitted Diseases is Boosting the Market

The macrolide antibiotics market expansion is driven by the increasing prevalence of respiratory tract infections such as pneumonia, bronchitis, and sinusitis, along with sexually transmitted diseases (STDs) like chlamydia and gonorrhea. Macrolides, including azithromycin, clarithromycin, and erythromycin, are widely prescribed for their broad-spectrum antibacterial activity and efficacy against Gram-positive and some Gram-negative bacteria. Their ability to treat infections caused by atypical pathogens, such as Mycoplasma pneumoniae and Legionella pneumophila, has further solidified their role in the treatment of respiratory infections. Additionally, the rising incidence of STDs globally, particularly in developing countries with limited healthcare infrastructure, has increased the demand for macrolide antibiotics due to their efficacy and ease of administration.

Key Restraints:

Growing Antibiotic Resistance and Restricted Usage is Hampering the Market

A major restraint for the macrolide antibiotics industry is the increasing prevalence of antimicrobial resistance (AMR) associated with macrolides. Overprescription and misuse of macrolides have led to the emergence of resistant strains of pathogens, such as Streptococcus pneumoniae and Mycoplasma genitalium, diminishing the clinical efficacy of these drugs. Regulatory authorities in several countries are implementing stricter guidelines to curb antibiotic misuse, which includes limiting the use of macrolides to cases with confirmed susceptibility. Furthermore, the development of newer antibiotics with enhanced efficacy and fewer resistance issues has reduced reliance on macrolides, creating challenges for market growth in regions with advanced healthcare systems.

Future Opportunities :

Development of Novel Macrolides with Improved Resistance Profiles are Increasing Prevalence in the Market.

The ongoing development of next-generation macrolides with improved resistance profiles presents a significant opportunity for market advancement. Pharmaceutical companies are investing in research to design macrolides with structural modifications that enhance their activity against resistant strains while minimizing side effects. For example, ketolides, a subclass of macrolides, have shown promising efficacy against macrolide-resistant pathogens and are being explored for their potential to address antimicrobial resistance. Additionally, advancements in drug formulation technologies, such as extended-release and targeted delivery systems, are improving patient compliance and expanding the therapeutic applications of macrolides. The integration of these innovations, combined with a focus on addressing global AMR challenges, positions the market for growth, particularly in regions with high infection burdens.

These dynamics underscore the critical role of macrolide antibiotics in managing respiratory and sexually transmitted infections while highlighting the challenges posed by antimicrobial resistance. The development of novel macrolides and strategies to combat resistance will be pivotal in sustaining market opportunities and meeting the evolving needs of global healthcare systems.

Macrolide Antibiotics Market Segmental Analysis :

By Drug Type:

Based on drug type, the macrolide antibiotics market is segmented into 14-membered macrolides, 15-membered macrolides, and 16-membered macrolides.

The 14-membered macrolides segment accounted for the largest revenue share in 2024.

- 14-membered macrolides, including erythromycin and clarithromycin, are widely used due to their effectiveness against respiratory and skin infections.

- High adoption in treating common bacterial infections, supported by their broad-spectrum activity, has driven this segment's analysis.

- Increasing use in pediatric and adult populations for infections caused by Gram-positive bacteria is boosting trends.

- Advancements in formulations, such as extended-release options, have enhanced patient compliance and supported segment analysis.

The 15-membered macrolides segment is anticipated to register the fastest CAGR during the forecast period.

- Azithromycin, a 15-membered macrolide, is preferred for its once-daily dosing regimen and superior tissue penetration.

- Rising adoption for respiratory tract infections and sexually transmitted infections (STIs) is driving segment trends.

- Increasing recommendations for azithromycin in guidelines for Mycoplasma pneumoniae infections are boosting advancement.

- Ongoing research into expanding indications for 15-membered macrolides is expected to propel macrolide antibiotics market growth.

By Drugs:

Based on drugs, the market is segmented into azithromycin, clarithromycin, erythromycin, fidaxomicin, and telithromycin.

The azithromycin segment accounted for the largest revenue share in 2024.

- Azithromycin is extensively used due to its broad-spectrum activity, once-daily dosing, and short treatment duration.

- High efficacy in treating respiratory infections and STIs has made azithromycin the most prescribed macrolide antibiotic.

- Increasing use in combination therapy for COVID-19 and other emerging infectious diseases has boosted macrolide antibiotics market demand.

- Expanding availability in generic formulations has improved accessibility and affordability globally.

The fidaxomicin segment is anticipated to register the fastest CAGR during the forecast period.

- Fidaxomicin is gaining traction for its targeted activity against Clostridium difficile infections, reducing recurrence rates.

- Increasing adoption in hospitals and specialty clinics for severe gastrointestinal infections is driving macrolide antibiotics market growth.

- Rising awareness about the importance of antibiotic stewardship programs is supporting the uptake of fidaxomicin.

- Ongoing development of novel fidaxomicin formulations for broader indications is expected to propel macrolide antibiotics market trends.

By Route of Administration:

Based on route of administration, the market is segmented into oral, intravenous (IV), and topical.

The oral segment accounted for the largest revenue share in 2024.

- Oral macrolides are preferred for their convenience, ease of administration, and widespread use in outpatient settings.

- High availability of oral formulations, including tablets, capsules, and liquid suspensions, supports segment dominance.

- Increasing use of oral macrolides for mild to moderate respiratory and skin infections is driving advancement.

- Advancements in bioavailability and extended-release formulations have enhanced the efficacy of oral macrolides.

The intravenous (IV) segment is anticipated to register the fastest CAGR during the forecast period.

- IV macrolides are critical in treating severe infections, such as pneumonia and cerebral toxoplasmosis, in hospitalized patients.

- Growing trends in critical care settings for rapid and effective antibiotic therapy is boosting adoption.

- Advancements in IV formulations, including ready-to-use solutions, are simplifying administration and driving growth.

- Increasing prevalence of multidrug-resistant bacterial infections is expected to propel macrolide antibiotics market demand for IV macrolides.

By Indication:

Based on indication, the market is segmented into infections due to Mycoplasma pneumoniae, Legionella sp. or Bordetella Pertussis, symptomatic cat-scratch disease, bacillary angiomatosis, peliosis hepatis in AIDS patients, cerebral toxoplasmosis, uncomplicated skin infections, and others.

The infection due to Mycoplasma pneumoniae segment held the largest share in 2024.

- Azithromycin and clarithromycin are widely used in treating respiratory infections caused by Mycoplasma pneumoniae, ensuring their dominant market presence.

- The increasing trend of antibiotic resistance has led to extensive research and development of advanced macrolide formulations, improving treatment efficacy.

- Market analysis highlights that the growing prevalence of community-acquired pneumonia (CAP) is fueling demand for effective treatment solutions.

- The trend of shifting towards targeted therapies and combination treatments is enhancing the role of macrolides in respiratory infections.

The cerebral toxoplasmosis segment is expected to achieve the fastest CAGR during the forecast period.

- Cerebral toxoplasmosis is a life-threatening condition in immunocompromised patients, particularly those with HIV/AIDS, increasing the demand for effective macrolide-based treatments.

- Azithromycin is frequently used as part of combination therapy, improving patient outcomes in severe toxoplasmosis cases.

- Market analysis suggests that increased global efforts to improve access to HIV/AIDS treatments are driving the need for reliable antimicrobial options.

- The trend of increasing research into macrolide derivatives for treating opportunistic infections is expected to expand the market in this segment.

By Application:

Based on application, the market is segmented into respiratory tract infections, skin and soft tissue infections, sexually transmitted infections, otitis media, gastrointestinal infections and others.

The respiratory tract infections segment accounted for the largest revenue in macrolide antibiotics market share in 2024.

- Macrolides are first-line treatments for respiratory infections such as community-acquired pneumonia and bronchitis, driving development.

- Increasing prevalence of respiratory infections globally, especially in pediatric and elderly populations, supports segment advancement.

- Rising adoption of macrolides in outpatient and hospital settings for respiratory conditions is boosting market share.

- Ongoing research into macrolide efficacy against emerging respiratory pathogens is further supporting surge.

The gastrointestinal infections segment is anticipated to register the fastest CAGR during the forecast period.

- Fidaxomicin’s targeted efficacy against Clostridium difficile has driven growth in the gastrointestinal infections segment.

- Increasing awareness about the role of macrolides in reducing antibiotic-associated diarrhea is boosting demand.

- Rising focus on controlling healthcare-associated infections in hospitals is driving trends in this segment.

- Expansion of antibiotic stewardship programs promoting the use of macrolides for gastrointestinal indications is expected to propel macrolide antibiotics market trends.

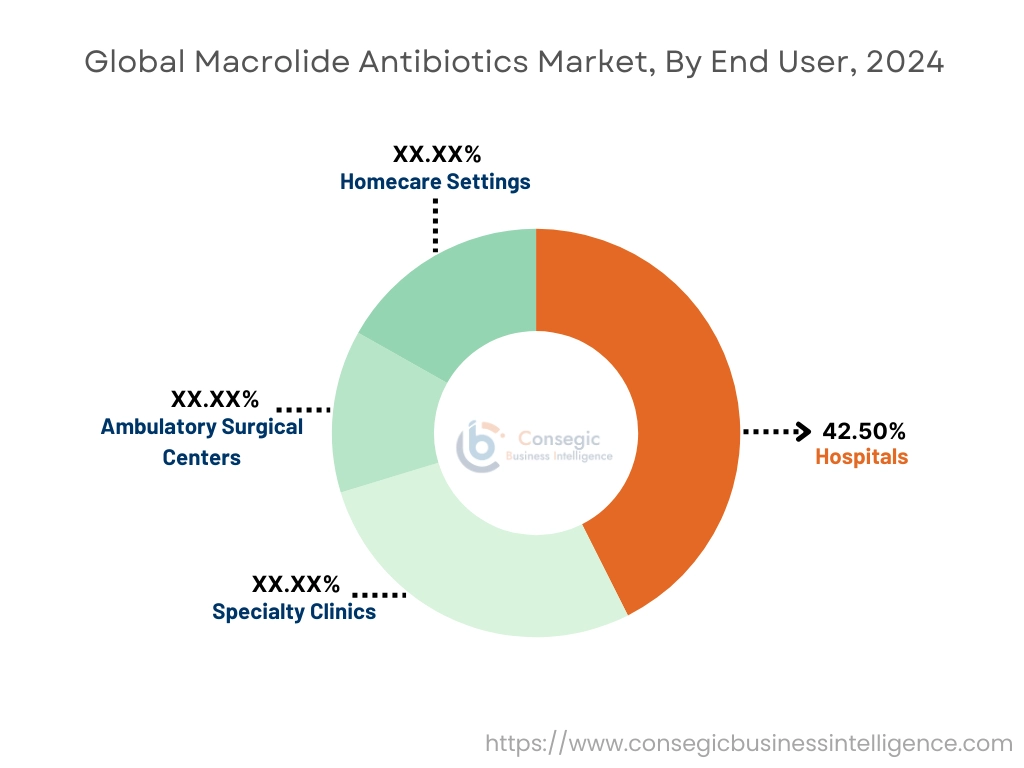

By End-User:

Based on end-user, the market is segmented into hospitals, specialty clinics, ambulatory surgical centers, and homecare settings.

The hospitals segment accounted for the largest revenue in macrolide antibiotics market share of 42.50% in 2024.

- Hospitals are primary settings for administering IV macrolides and managing severe infections requiring close monitoring.

- Increasing hospital admissions for respiratory and gastrointestinal infections have driven surge for macrolides.

- Availability of multidisciplinary care and advanced diagnostic facilities in hospitals supports their dominance in the market.

- Rising focus on hospital-acquired infection prevention has increased the use of targeted macrolide therapies in this setting.

The homecare settings segment is anticipated to register the fastest CAGR during the forecast period.

- Growing adoption of oral macrolides for self-administration and outpatient care is driving demand in homecare settings.

- Rising availability of user-friendly formulations, such as liquid suspensions and extended-release tablets, is boosting development.

- Increasing emphasis on cost-effective and convenient treatment options for chronic and mild infections supports market expansion.

- Expanding telehealth services and remote monitoring solutions are enhancing access to macrolide-based treatments in homecare settings.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

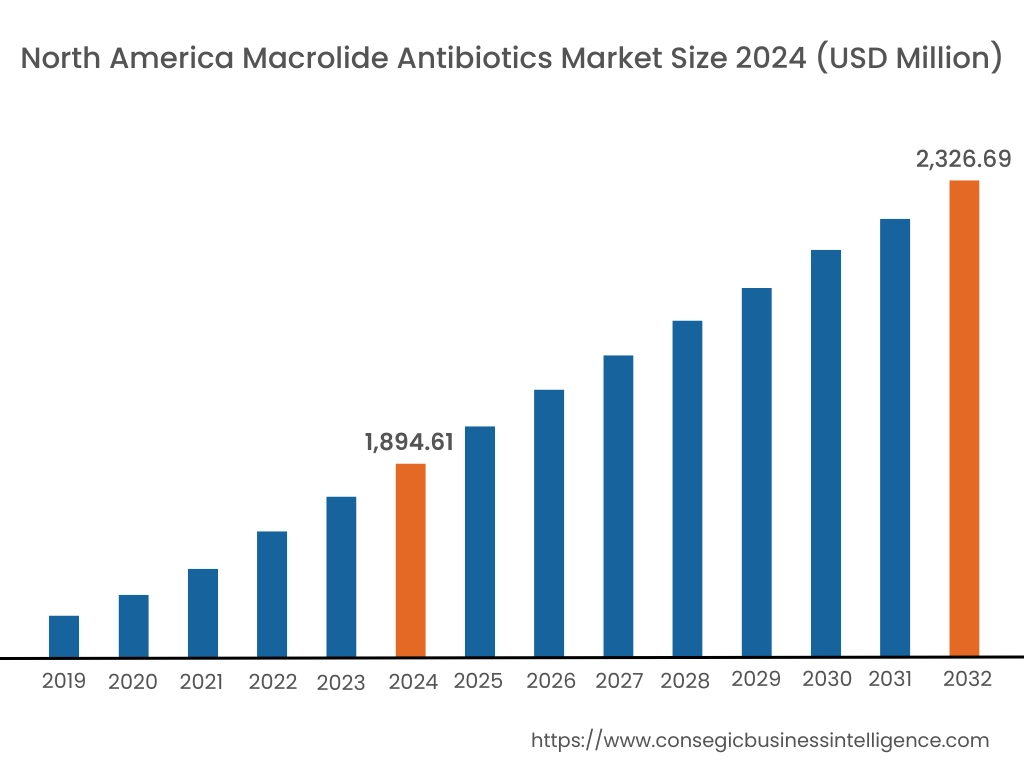

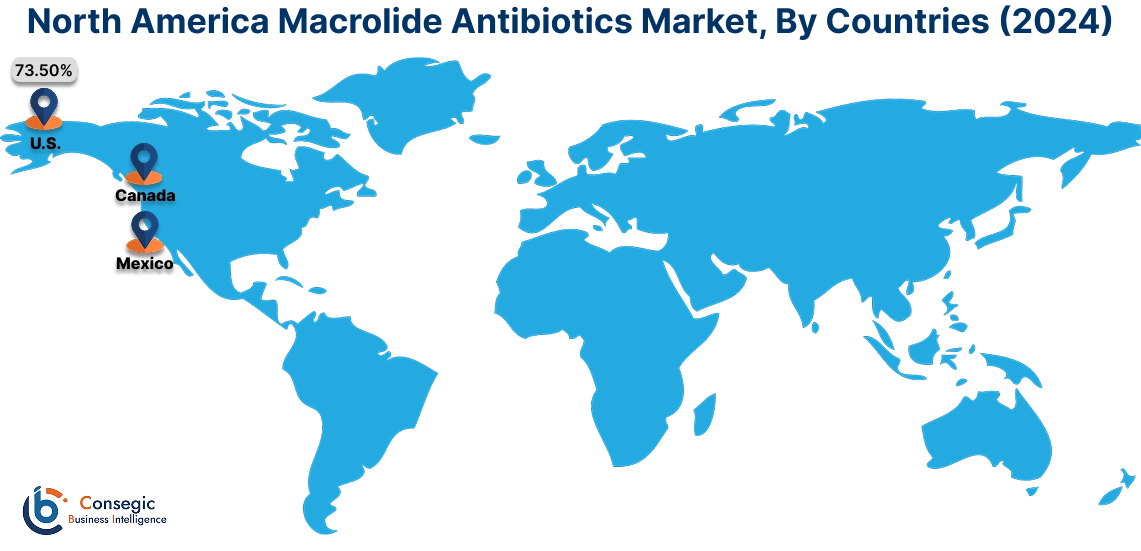

In 2024, North America was valued at USD 1,894.61 Million and is expected to reach USD 2,326.69 Million in 2032. In North America, the U.S. accounted for the highest share of 73.50% during the base year of 2024.

North America holds a significant stake in the global macrolide antibiotics market, driven by a high prevalence of bacterial infections, advanced healthcare infrastructure, and increasing awareness about antimicrobial resistance. The U.S. dominates the region due to its extensive use in treating respiratory tract infections and skin infections. The availability of advanced formulations and robust R&D investments in antibiotic development further supports market enlargement. As per the macrolide antibiotics market analysis, Canada contributes through rising healthcare spending and growing development for antibiotics in rural and urban areas. However, stringent FDA regulations and rising concerns about antibiotic overuse may limit macrolide antibiotics market expansion.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 3.3% over the forecast period. The macrolide antibiotics market analysis is fueled by increasing prevalence of infectious diseases, rapid urbanization, and improving healthcare infrastructure in China, India, and Southeast Asia. China dominates the market with rising demand for macrolides in treating community-acquired infections and expanding pharmaceutical manufacturing capabilities. India’s growing healthcare sector supports the widespread use of generic macrolide antibiotics, particularly in rural areas. Japan emphasizes advanced formulations and strict antimicrobial stewardship programs to ensure appropriate antibiotic usage. However, lack of awareness about antimicrobial resistance in rural areas and over-the-counter availability of antibiotics may hinder proper usage.

Europe is a prominent market for macrolide antibiotics, supported by a growing elderly population, increasing bacterial infection rates, and strong healthcare systems. Countries like Germany, France, and the UK are key contributors. Germany drives demand through its focus on innovative macrolide formulations and widespread use in hospitals for severe infections. As per the regional analysis France emphasizes the role of macrolides in outpatient treatments, particularly for respiratory and soft tissue infections. The UK focuses on tackling antimicrobial resistance while promoting appropriate antibiotic usage. However, stringent EU guidelines on antibiotic prescriptions may challenge market progress in certain regions.

The Middle East & Africa region is experiencing steady growth in macrolide antibiotics market, driven by increasing healthcare investments and rising prevalence of bacterial infections. In the Middle East, countries like Saudi Arabia and the UAE are adopting macrolide antibiotics for respiratory infections and skin conditions, supported by government-led healthcare modernization efforts. In Africa, South Africa is emerging as a key market, leveraging public health programs to combat infectious diseases with macrolide antibiotics. However, limited access to advanced healthcare infrastructure and overuse of antibiotics in some regions may restrict broader market development.

Latin America is an emerging market for macrolide antibiotics, with Brazil and Mexico leading the region. Brazil’s expanding healthcare sector and increasing prevalence of respiratory infections drive progress for macrolides in both public and private healthcare settings. Mexico focuses on improving access to affordable antibiotics through government programs and partnerships with pharmaceutical companies. The region also sees growing awareness campaigns about appropriate antibiotic usage. However, economic instability and inconsistent healthcare policies may pose challenges to create new macrolide antibiotics market opportunities in smaller economies.

Top Key Players & Market Share Insights:

The macrolide antibiotics market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global macrolide antibiotics market. Key players in the macrolide antibiotics industry include -

- Pfizer Inc. (United States)

- Merck & Co., Inc. (United States)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Bayer AG (Germany)

- Zydus Lifesciences Limited (India)

- Novartis AG (Switzerland)

- AbbVie Inc. (United States)

- Sanofi S.A. (France)

- AstraZeneca plc (United Kingdom)

- GlaxoSmithKline plc (United Kingdom)

Macrolide Antibiotics Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 7,178.93 Million |

| CAGR (2025-2032) | 2.9% |

| By Drug Type |

|

| By Drugs |

|

| By Route of Administration |

|

| By Indication |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Macrolide Antibiotics Market by 2031? +

Macrolide Antibiotics Market size is estimated to reach over USD 7,178.93 Million by 2032 from a value of USD 5,711.66 Million in 2024 and is projected to grow by USD 5,775.53 Million in 2025, growing at a CAGR of 2.9% from 2025 to 2032.

What factors are driving the Macrolide Antibiotics Market? +

The market is driven by the rising prevalence of respiratory tract infections and sexually transmitted diseases (STDs). The increasing demand for effective antibiotics, particularly in developing regions, further supports market growth.

What challenges are restraining market growth? +

The increasing prevalence of antimicrobial resistance (AMR) and regulatory restrictions on antibiotic usage are major challenges. Overprescription and misuse of macrolides have led to the emergence of resistant bacterial strains, limiting their clinical efficacy and restricting market growth.

What opportunities exist in the Macrolide Antibiotics Market? +

The development of next-generation macrolides with improved resistance profiles presents significant growth opportunities. Advancements in drug formulations, such as extended-release and targeted delivery systems, and the introduction of ketolides are expected to address AMR challenges and expand the market.

Which drug type dominates the Macrolide Antibiotics Market? +

The 14-membered macrolides segment, including erythromycin and clarithromycin, accounted for the largest revenue share in 2024 due to their broad-spectrum activity and widespread use in treating respiratory and skin infections.