- Summary

- Table Of Content

- Methodology

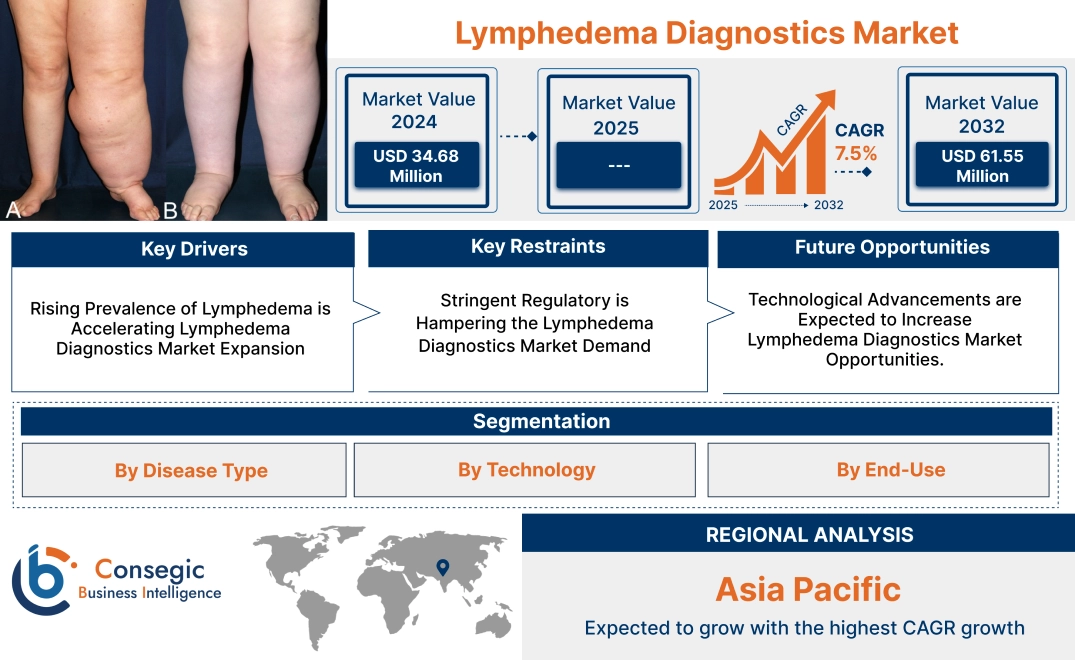

Lymphedema Diagnostics Market Size:

Lymphedema Diagnostics Market size is growing with a CAGR of 7.5% during the forecast period (2025-2032), and the market is projected to be valued at USD 61.55 Million by 2032 from USD 34.68 Million in 2024.

Lymphedema Diagnostics Market Scope & Overview:

Lymphedema diagnostics involve techniques used to identify and assess the extent of lymphedema, which is a chronic condition caused by a blockage or damage to the lymphatic system, leading to the accumulation of lymph fluid in tissues, resulting in swelling, typically in the arms or legs. This disease is further categorized into primary and secondary. Primary lymphedema is caused by congenital abnormalities in the lymphatic system, while secondary lymphedema results from damage to the lymphatic system due to factors such as cancer treatment, surgery, infection, or injury. This disease is diagnosed through various methods. Lymphedema diagnosis typically begins with a thorough medical history and physical examination to assess symptoms and identify potential risk factors. Imaging techniques also play a crucial role, including lymphoscintigraphy, which uses radioactive tracers to map lymph flow, ultrasound to identify fluid accumulation, MRI to visualize lymphatic vessels, and CT scans to detect blockages. Accurate diagnosis is crucial for early intervention, preventing progression, minimizing complications such as infections or fibrosis, and improving quality of life through appropriate therapies.

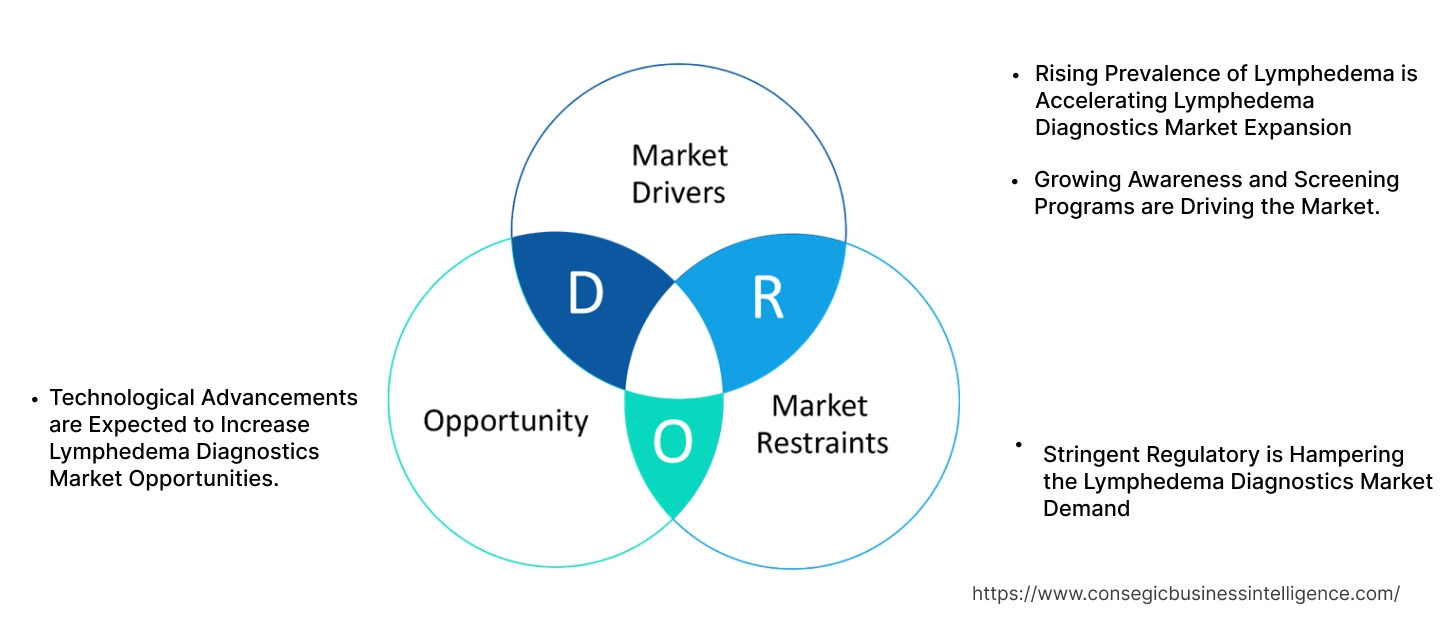

Lymphedema Diagnostics Market Dynamics - (DRO) :

Key Drivers:

Rising Prevalence of Lymphedema is Accelerating Lymphedema Diagnostics Market Expansion

Lymphedema is a chronic condition caused by the accumulation of lymph fluid, leading to swelling in various body parts. Common symptoms of diseases include persistent swelling, heaviness or tightness in affected areas, restricted range of motion, pain, and recurrent infections. The condition significantly impacts daily life, leading to difficulty in performing routine activities, such as walking, dressing, or exercising. Emotional and psychological effects, such as anxiety and depression, also arise due to the visible swelling and the chronic nature of the disease.

With the increasing incidence of cancer, particularly breast cancer, prostate cancer, and other malignancies treated through surgery and radiation therapy, the risk of developing lymphedema is also rising. Additionally, an aging global population contributes to a higher prevalence, as older individuals are more susceptible to chronic conditions.

- According to an article published by the National Center for Biotechnology Information, in 2022, up to 250 million people worldwide is affected by lymphedema. This has led to a heightened demand for early diagnosis, thereby positively influencing the lymphedema diagnostics market trends.

Overall, the high increase in lymphedema cases is significantly boosting the lymphedema diagnostics market expansion.

Growing Awareness and Screening Programs are Driving the Market.

Increased public and professional awareness about lymphedema, particularly among cancer patients, healthcare providers, and the general population, is playing a crucial role in early detection and diagnosis. The condition, which is overlooked or misdiagnosed, is now recognized as a significant issue due to its impact on patients' quality of life. Campaigns, educational programs, and blogs from healthcare organizations, government bodies, and patient advocacy groups are emphasizing the importance of identifying lymphedema early to prevent it from progressing into more severe stages.

- Mayo Clinic published an article, in 2024, providing an overview of lymphedema, covering its definition, types, causes, risk factors, the importance of timely diagnosis, and various diagnostic methods available, such as lymphoscintigraphy, ultrasound, MRI, and CT scans. This has increased visits regarding lymphedema, positively influencing the lymphedema diagnostics market trends.

Additionally, screening programs, particularly in oncology settings, are becoming more prevalent. These programs aim to identify at-risk individuals, such as cancer patients undergoing treatment, and monitor them for signs of lymphedema. Regular screening allows for the timely detection of swelling, further boosting the market.

Overall, growing awareness and screening programs are accelerating the global lymphedema diagnostics market growth.

Key Restraints:

Stringent Regulatory is Hampering the Lymphedema Diagnostics Market Demand

Regulatory challenges pose a significant restraint in the global lymphedema diagnostics market growth. Regulatory bodies such as the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and other national authorities have stringent approval processes for medical devices and diagnostic technologies. For instance, imaging technologies such as lymphoscintigraphy, MRI, or near-infrared fluorescence imaging require comprehensive clinical trials to demonstrate their safety and efficacy before they are marketed.

These lengthy approval processes delay product launches and significantly increase the costs of bringing a new diagnostic tool to the market. Companies must also navigate varying regulations in different regions, further complicating the approval process. Regulatory requirements for consumables, such as contrast agents or fluorescent dyes used in lymphedema diagnosis, are also subject to rigorous testing and quality control standards. This regulatory burden restricts the availability of newer, more advanced diagnostic technologies, especially in emerging markets where regulatory frameworks are not as established or efficient.

Overall, stringent regulatory requirements for medical devices and diagnostic technologies, including lengthy approval processes and varying regional regulations, are hampering the lymphedema diagnostics market demand.

Future Opportunities :

Technological Advancements are Expected to Increase Lymphedema Diagnostics Market Opportunities.

Technological advancements are a significant driver of the global market, as they improve the accuracy, efficiency, and non-invasiveness of diagnostic techniques. One of the most notable advancements is the development of near-infrared fluorescence (NIRF) imaging, which allows for real-time visualization of lymphatic flow and is less invasive compared to traditional methods. This technology provides clearer, more accurate images of lymphatic vessels, enabling early detection and better monitoring of disease progression.

Another innovation is bioimpedance analysis (BIA), a non-invasive method that measures changes in the electrical impedance of body tissue to assess fluid retention and lymphatic health. BIA offers a quicker, less painful alternative to more invasive procedures, making it an attractive option for widespread use in screening programs. Furthermore, artificial intelligence (AI) and machine learning are also transforming lymphedema diagnostics.

- According to an article published by National Center for Biotechnology Information, in 2024, AI-based classification of ICG lymphography patterns significantly enhances the accuracy and objectivity of lymphedema diagnosis, potentially improving clinical decision-making and patient outcomes. This has increased its applications, creating the potential for the market.

Overall, technological advancements, including NIRF imaging, bioimpedance analysis, and AI-powered analysis are expected to increase lymphedema diagnostics market opportunities.

Lymphedema Diagnostics Market Segmental Analysis :

By Disease Type:

Based on disease type, the market is categorized into primary lymphedema and secondary lymphedema.

Trends in Disease Type:

- Improved survival rates for cancer patients are leading to a larger population at risk for secondary lymphedema.

- Aging populations are at increased susceptibility to various conditions that contribute to secondary lymphedema.

The secondary lymphedema segment accounted for the largest market share in 2024 and is expected to grow at the fastest CAGR over the forecast period.

- Secondary lymphedema is a type of swelling that occurs when the lymphatic system is damaged or blocked, but this form is not acquired by birth, and it occurs later in life due to external factors.

- Conditions leading to secondary lymphedema are obesity, trauma, and infections such as filariasis.

- Moreover, surgical removal of lymph nodes, radiation therapy, and chemotherapy, all of which are common cancer treatments, result in damage to the lymphatic system, leading to secondary lymphedema.

- For instance, according to a study published by the National Center for Biotechnology Information, in 2022, a significant percentage of patients develop lymphedema following breast cancer (7-77%) and gynecological surgeries (0-70%). This has required increased demand for diagnostic procedures, thus driving the segment.

- Additionally, the risk of lymphedema is further increased by treatments such as radiotherapy and chemotherapy, particularly those involving taxanes.

- The growing awareness of the importance of early detection and management of secondary lymphedema is contributing to its emergence. Early diagnosis enables timely intervention, which reduces complications, improves quality of life, and lowers healthcare industry costs.

- Overall, as per the market analysis, increasing prevalence due to cancer treatments and growing awareness of its impact are driving segmental growth.

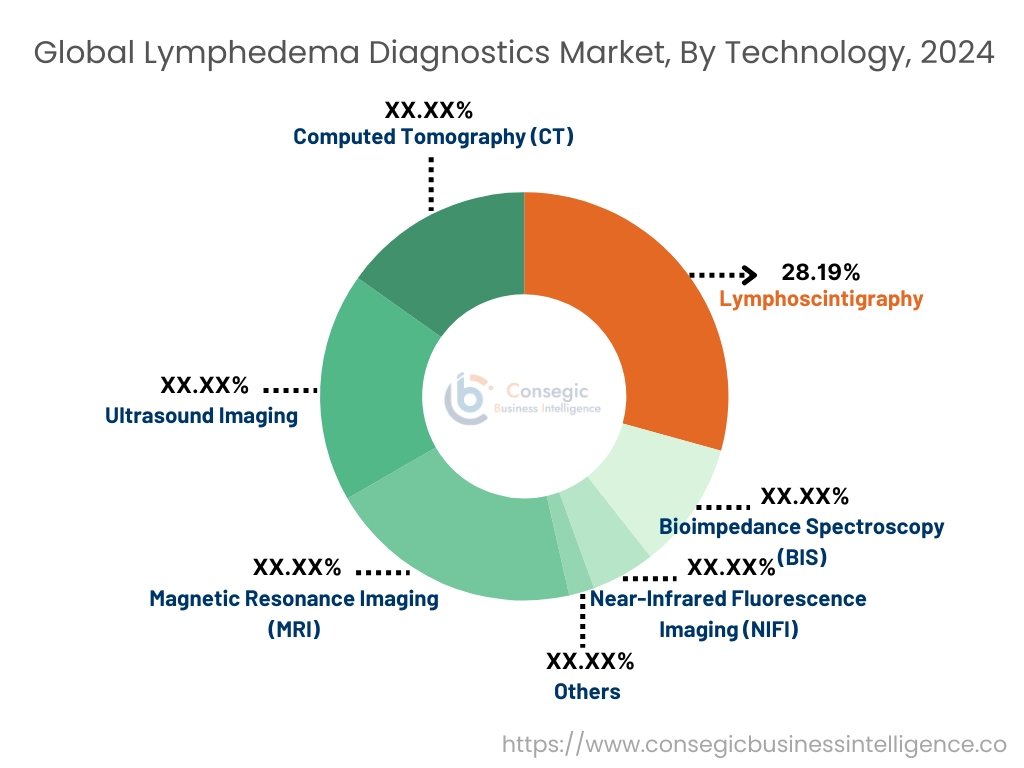

By Technology:

The technology segment is categorized into magnetic resonance imaging (MRI), ultrasound imaging, computed tomography (CT), lymphoscintigraphy, bioimpedance spectroscopy (BIS), near-infrared fluorescence imaging (NIFI), and others.

Trends in the Technology:

- The development of portable and point-of-care ultrasound devices is enabling accurate and efficient diagnosis.

- Development of 3D and 4D imaging techniques for better visualization of lymphatic structure.

The lymphoscintigraphy segment accounted for the largest market share of 28.91% in 2024.

- Lymphoscintigraphy is dominating the market as it is widely regarded as the gold standard for visualizing lymphatic function and diagnosing lymphedema.

- This nuclear imaging technique involves injecting a small amount of radioactive tracer into the affected area, followed by imaging to track the flow of lymphatic fluid and identify blockages or abnormalities.

- It is highly effective in confirming lymphedema and differentiating it from other conditions causing swelling, such as venous insufficiency or lipedema. It is a well-established technique, widely used in clinical practice for both research and patient care. Protocols for lymphoscintigraphy are standardized, ensuring consistent results across healthcare settings.

- The rising prevalence of cancer and its treatments, which significantly increase the risk of secondary lymphedema, is driving the segment. Moreover, growing awareness among healthcare professionals and the general public about lymphedema is leading to earlier diagnosis, positively impacting the demand for

- Overall, as per the market analysis, the rising prevalence of secondary lymphedema and increased awareness about the condition are driving this segmental growth in the lymphedema diagnostics industry.

The near-infrared fluorescence imaging (NIFI) segment is expected to grow at the fastest CAGR over the forecast period.

- Near-infrared fluorescence imaging is emerging as a promising technology in diagnosing lymphedema due to its non-invasive, real-time, and highly sensitive capabilities for visualizing lymphatic flow.

- This technology uses fluorescent dyes, such as indocyanine green (ICG), which, when injected, bind to the lymphatic fluid and emit fluorescence under near-infrared light. The emitted light is captured using specialized cameras, providing detailed images of lymphatic vessels and their functionality.

- NIFI does not involve radioactive tracers, making it safer and more patient-friendly, with reduced discomfort. Moreover, it has high sensitivity and accuracy.

- For instance, according to a study published in MDPI, near-infrared fluorescence imaging is employed to assess the superficial structure of the lymphatic system. In individuals with lymphedema, three distinct patterns of dysfunctional dermal backflow are identified, which was not possible with traditional methods. This has increased the approaches and reach for diagnostics.

- Overall, patients and clinicians preferring non-radioactive and safer diagnostic techniques, especially for routine screenings, create the potential for the segment in the upcoming years.

By End User:

The end-user segment is categorized into hospitals, diagnostic centers, and others.

Trends in End-User:

- Increase diagnostic services in community-based healthcare settings to expand reach.

- Investment in advanced imaging technologies and equipment to improve diagnosis and patient outcomes.

The hospitals segment accounted for the largest market share in 2024.

- Hospitals dominate due to their comprehensive capabilities, infrastructure, and high patient influx. They are the first point of care for patients experiencing symptoms of lymphedema.

- Moreover, hospitals house advanced diagnostic technologies such as lymphoscintigraphy, MRI, CT scans, and NIRF imaging, making them well-equipped for accurate and early diagnosis.

- Additionally, hospitals handle a higher patient volume compared to diagnostic centers, especially for inpatient care and follow-up treatments. This is particularly true for secondary lymphedema cases arising from cancer therapies, as hospitals are central to oncological care and surgical interventions.

- Furthermore, hospitals employ specialized healthcare professionals, including radiologists and oncologists, who are skilled in using complex diagnostic tools and interpreting results. Hospitals are adopting new technologies such as AI-powered diagnostic tools.

- For instance, Luke’s Hospital collaborated with GE Healthcare to install 76 ultrasound systems powered by artificial intelligence on the campus. This new type of collaboration has led to an increase in the volume of diagnostic procedures, while being the most accurate, thus driving the segment.

- Overall, high patient volume, advanced infrastructure, and ongoing adoption of innovative diagnostic tools are driving the segment.

The diagnostics centers segment is expected to grow at the fastest CAGR over the forecast period.

- Diagnostic centers are emerging in the market as they provide focused diagnostic solutions for lymphedema, leveraging advanced technologies such as bioimpedance spectroscopy (BIS), near-infrared fluorescence imaging (NIRF), and ultrasound.

- Moreover, one key reason for their growth is increased accessibility. Diagnostic centers are in urban and semi-urban areas, making them convenient for patients who do not need the comprehensive care provided by hospitals. They typically offer shorter waiting times and faster results, which appeal to patients seeking immediate diagnostics.

- Additionally, cost-effectiveness is another driving factor. Compared to hospitals, diagnostic centers provide lymphedema imaging and testing at lower costs, which is particularly beneficial for routine screening and early-stage detection.

- As awareness about lymphedema grows, patients are seeking affordable and specialized options, that will drive the segment for the forecasted years.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

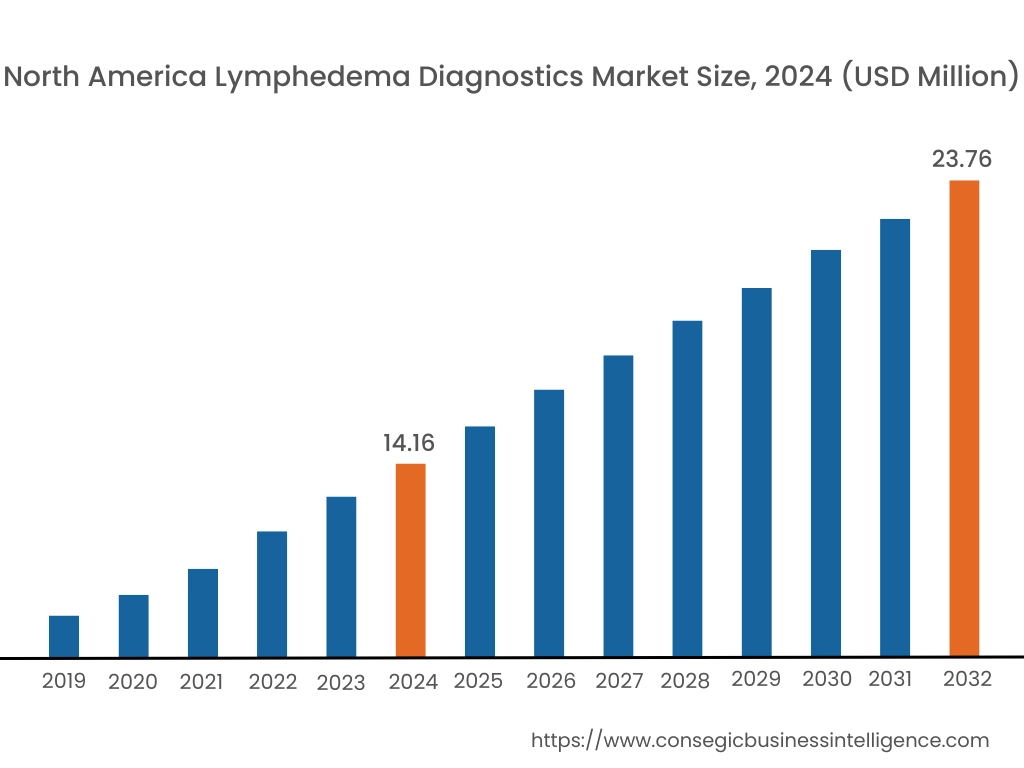

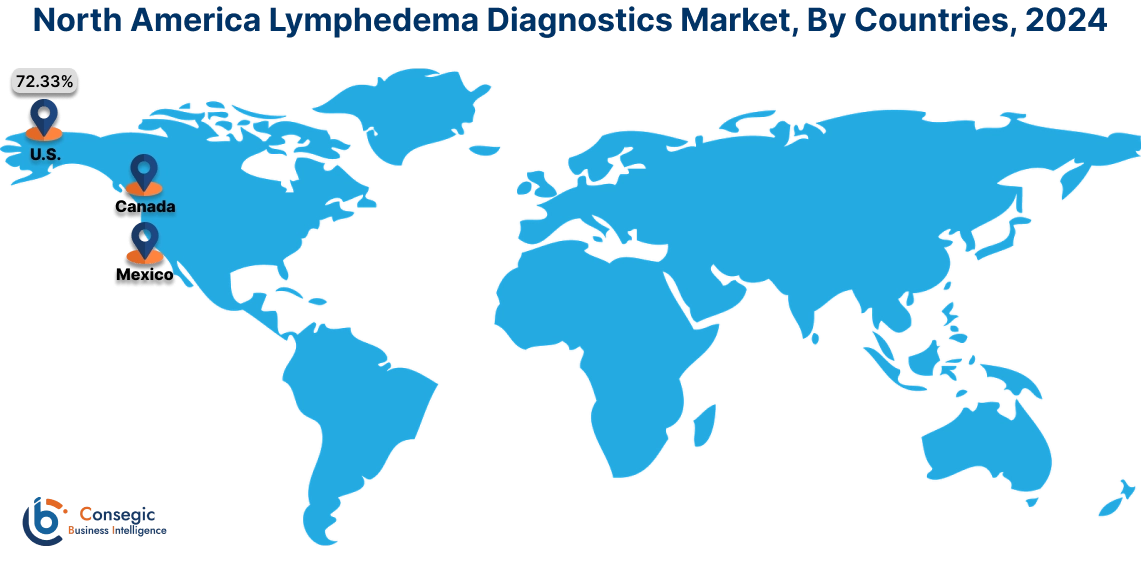

In 2024, North America accounted for the highest lymphedema diagnostics market share at 40.82% and was valued at USD 14.16 Million and is expected to reach USD 23.76 Million in 2032. In North America, the U.S. accounted for the highest lymphedema diagnostics market share of 72.33% during the base year of 2024. The region’s well-established healthcare systems provide widespread access to cutting-edge diagnostic technologies such as bioimpedance spectroscopy, and near-infrared fluorescence imaging. This infrastructure ensures accurate and early diagnosis, a key factor in effective lymphedema management. Moreover, the rising incidence of secondary lymphedema, particularly from cancer treatments, significantly contributes to the market’s dominance in North America.

According to cancer statistics, the U.S. has one of the highest cancer rates globally, with breast cancer and other lymph node-invasive cancers being major contributors to lymphedema. Additionally, the region also benefits from the presence of key market players and ongoing technological advancements. Innovations in diagnostic tools, combined with significant investment in healthcare R&D, further strengthen North America’s market position.

For instance,

- In 2024, GE HealthCare launched the new Versana Premier ultrasound systems, featuring advanced automation and AI-powered tools designed to streamline workflows, enhance clinical efficiency, and improve diagnostic accuracy. These new product launches have increased the reach of lymphedema diagnostics, positively influencing the market in the region.

Overall, the North America market is dominated by trends such as widespread access to advanced technologies, high cancer incidence, strong presence of key players, and continuous technological advancements, leading to early detection.

In Asia Pacific, the lymphedema diagnostics market is experiencing the fastest growth with a CAGR of 8.9% over the forecast period. APAC has the largest population globally, with a significant proportion experiencing risk factors for lymphedema, such as cancer treatments, infections, and obesity. This large patient pool drives demand for diagnostics. Moreover, governments and private sectors in countries such as China, India, and Japan are heavily investing in healthcare infrastructure, including diagnostic technologies, making lymphedema care more accessible. Additionally, APAC’s healthcare systems are focusing on affordable diagnostic methods such as ultrasound and bioimpedance spectroscopy (BIS), making testing accessible to middle-income populations. Furthermore, growing awareness campaigns and government initiatives aimed at lymphedema education and screening programs drive the need for diagnostic services. Also, the increasing aging population in the region also adds to the disease burden, as older adults are more likely to undergo surgeries or treatments that disrupt lymphatic function.

Europe's lymphedema diagnostics market analysis states that several trends are responsible for the progress of the market in the region. Countries such as Germany, the UK, and France are leading the market owing to the widespread adoption of advanced diagnostic technologies like lymphoscintigraphy and MRI. Europe also benefits from universal healthcare coverage, which makes diagnostics accessible to a larger population. Moreover, the region is actively involved in clinical research and technological innovation, with collaborations between healthcare providers and universities driving advancements in imaging tools. Additionally, awareness campaigns by organizations such as the European Lymphology Society have improved early diagnosis rates. The increasing adoption of telemedicine and mobile health technologies also supports the market, especially in rural areas.

The Middle East and Africa (MEA) lymphedema diagnostics market analysis states that the region is also witnessing a notable surge. The market is driven by improving healthcare infrastructure and increasing medical awareness. Wealthy nations such as the UAE and Saudi Arabia dominate due to significant investments in healthcare facilities and advanced diagnostic tools such as MRI and CT scans. Moreover, in contrast, much of Sub-Saharan Africa faces challenges such as limited access to diagnostic technologies and a lack of skilled healthcare professionals. However, the prevalence of filariasis-induced lymphedema in tropical regions is a unique factor driving the need for diagnostics. Non-governmental organizations and global health initiatives are playing a crucial role in addressing lymphedema through awareness programs and subsidized diagnostics.

Latin America's lymphedema diagnostics market size is also emerging. A key trend is the expansion of public healthcare programs aimed at improving access to diagnostics, especially for low-income populations. Governments are prioritizing early detection of lymphedema through affordable screening programs. Moreover, the region is experiencing increased collaborations between local healthcare providers and international diagnostic companies, facilitating the introduction of advanced technologies such as NIRF imaging. Additionally, the rising prevalence of lymphedema is linked to cancer treatments and obesity. Countries such as Brazil, Mexico, and Argentina lead the market, supported by growing awareness and the adoption of diagnostic technologies. However, the region also faces challenges, such as uneven healthcare access and low awareness levels in remote areas.

Top Key Players and Market Share Insights:

The Lymphedema Diagnostics market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global Lymphedema Diagnostics market. Key players in The Lymphedema Diagnostics industry include-

- GE Healthcare (U.S.)

- Philips Healthcare (Netherlands)

- Stryker Corporation (U.S.)

- Mindray Medical (China)

- Shimadzu Corporation (Japan)

- Siemens Healthineers (Germany)

- Canon Medical Systems (Japan)

- Fujifilm Medical Systems (Japan)

- Hitachi (Japan)

- Esaote SpA (Italy)

Recent Industry Developments :

Product Launch:

- In July 2024, FUJIFILM Healthcare announced the U.S. launch of APERTO Lucent, a powerful open 0.4T MRI system. This new MRI system, with its RADAR motion compensating technology, enhances image quality by reducing the need for rescans and minimizing the impact of motion artifacts on workflow, ultimately improving diagnostic accuracy and efficiency.

- In November 2023, Samsung's digital radiography and ultrasound business announced the launch of the V6, their latest ultrasound system. This advanced system offers exceptional imaging capabilities across 2D, 3D, and color modes.

Lymphedema Diagnostics Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 61.55 Million |

| CAGR (2025-2032) | 7.5% |

| By Disease Type |

|

| By Technology |

|

| By End Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Lymphedema Diagnostics market? +

In 2024, the Lymphedema Diagnostics market is USD 34.68 Million.

Which is the fastest-growing region in the Lymphedema Diagnostics market? +

Asia Pacific is the fastest-growing region in the Lymphedema Diagnostics market.

What specific segmentation details are covered in the Lymphedema Diagnostics market? +

Disease Type and Technology segmentation details are covered in the Lymphedema Diagnostics market

Who are the major players in the Lymphedema Diagnostics market? +

GE Healthcare (U.S.), Philips Healthcare (Netherlands), Siemens Healthineers (Germany), Canon Medical Systems (Japan), Fujifilm Medical Systems (Japan), Hitachi (Japan), Esaote SpA (Italy), Stryker Corporation (U.S.), Mindray Medical (China), and Shimadzu Corporation (Japan).