- Summary

- Table Of Content

- Methodology

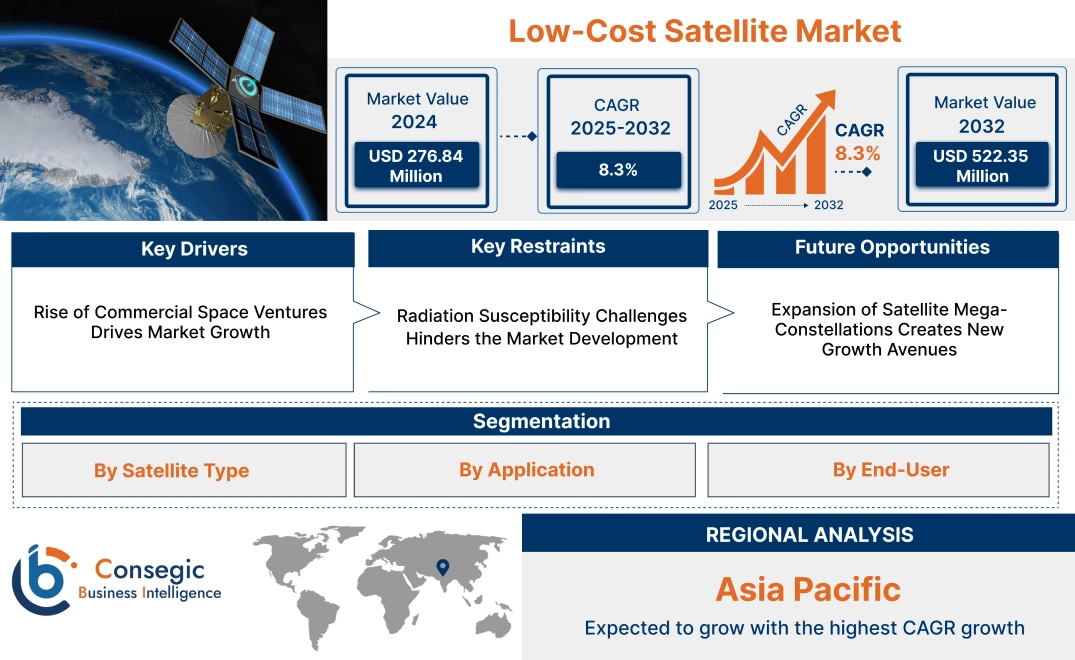

Low-Cost Satellite Market Size:

Low-Cost Satellite Market size is estimated to reach over USD 522.35 Million by 2032 from a value of USD 276.84 Million in 2024 and is projected to grow by USD 294.77 Million in 2025, growing at a CAGR of 8.3% from 2025 to 2032.

Low-Cost Satellite Market Scope & Overview:

The low-cost satellite market focuses on compact and affordable satellite systems designed to perform various functions, such as Earth observation, communication, navigation, and scientific research. These satellites are characterized by their reduced development and deployment costs, making them accessible to a broader range of organizations, including startups, academic institutions, and emerging space agencies. They are often deployed in constellations to provide enhanced coverage and functionality.

The satellites leverage advancements in miniaturization and modular design, enabling high-performance capabilities in small packages. These systems are integrated with technologies such as advanced sensors, communication modules, and propulsion systems, ensuring reliability and efficiency. They are compatible with smaller launch vehicles, further reducing operational expenses and facilitating rapid deployment.

End-users of these satellites include commercial enterprises, government agencies, and research organizations seeking cost-effective solutions for applications such as disaster management, environmental monitoring, and broadband connectivity. These satellites play a significant role in democratizing access to space-based technologies and expanding the scope of satellite-based services.

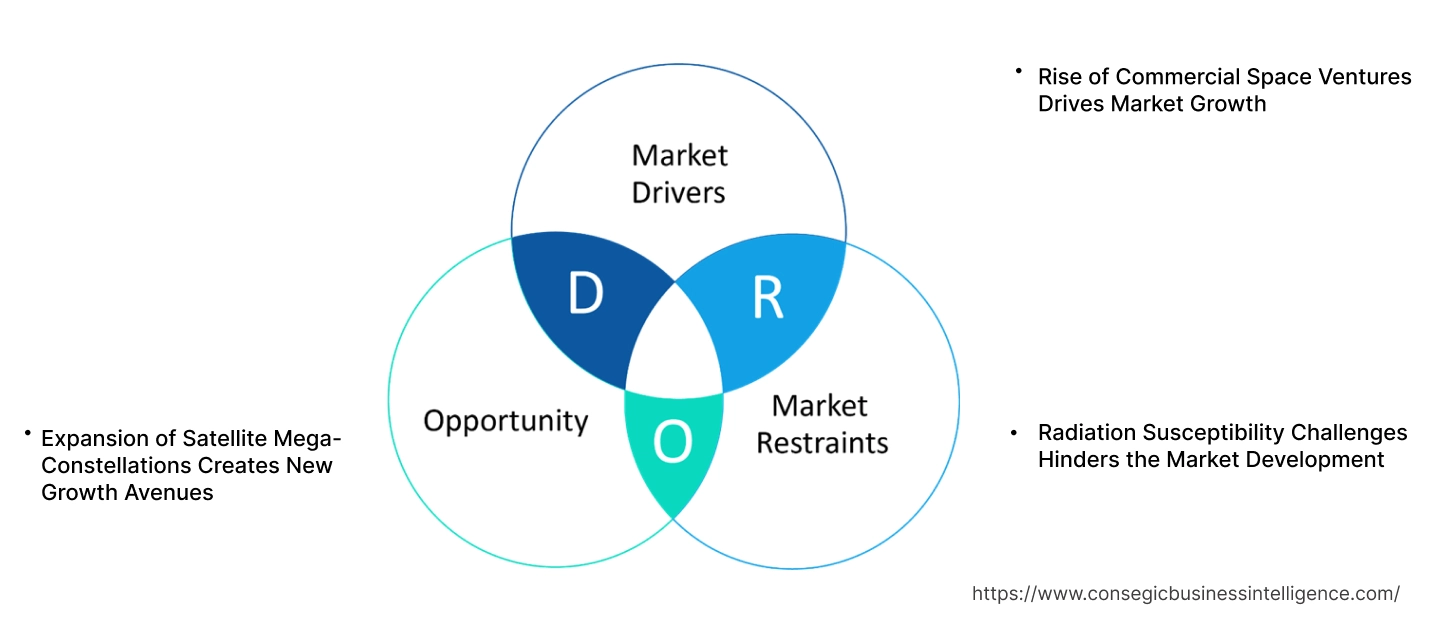

Low-Cost Satellite Market Dynamics - (DRO) :

Key Drivers:

Rise of Commercial Space Ventures Drives Market Growth

The entry of private companies into the space sector has revolutionized the satellite market, driving the rise of cost-efficient solutions for applications like Earth observation and broadband connectivity. With innovations in satellite miniaturization and manufacturing, private players are now able to deploy affordable, high-performing satellites at scale. The ongoing commercial space race, spearheaded by companies offering reusable launch vehicles, has significantly reduced launch costs, making satellite deployment more accessible than ever. This shift has catalyzed a surge in satellite production, enabling services such as global internet coverage, precision agriculture, and climate monitoring. The competition among private ventures is fostering rapid technological advancements, enhancing satellite capabilities while lowering operational expenses. As a result, the commercial space sector is playing a pivotal role in expanding the accessibility and affordability of satellite-based services across various industries and regions, driving low-cost satellite market growth.

Key Restraints:

Radiation Susceptibility Challenges Hinders the Market Development

Small satellites face heightened susceptibility to radiation-induced anomalies due to their limited size and weight, which restricts the integration of advanced radiation shielding. Exposure to high-energy particles in space disrupts satellite operations, degrade electronic components, and shorten the overall lifespan of these systems. This vulnerability is particularly significant in harsh environments, such as high-altitude orbits or regions near the Van Allen radiation belts. The lack of robust shielding options not only compromises the reliability of small satellites but also raises concerns for critical applications, including defense, Earth observation, and global communications. As a result, radiation susceptibility poses a key constraint for the widespread adoption of small satellite systems, particularly in missions requiring long-term operational stability. Thus, the aforementioned factors are hampering the low-cost satellite market demand.

Future Opportunities :

Expansion of Satellite Mega-Constellations Creates New Growth Avenues

The expansion of satellite mega-constellations is transforming the global connectivity and Earth observation landscape. These systems consist of hundreds to thousands of interconnected satellites in low Earth orbit (LEO), designed to provide seamless communication and high-speed broadband access worldwide. Companies are leveraging this technology to address connectivity gaps in remote and underserved regions, driving digital inclusion and bridging the digital divide. Additionally, mega-constellations support real-time Earth observation, enabling applications in disaster management, environmental monitoring, and precision agriculture. The scalability and reduced latency of these constellations make them ideal for supporting emerging technologies such as IoT and autonomous systems. As the demand for global coverage grows, investments in satellite mega-constellations are opening up new low-cost satellite market opportunities for service providers, fostering innovation, and reshaping the satellite sector on a global scale.

Low-Cost Satellite Market Segmental Analysis :

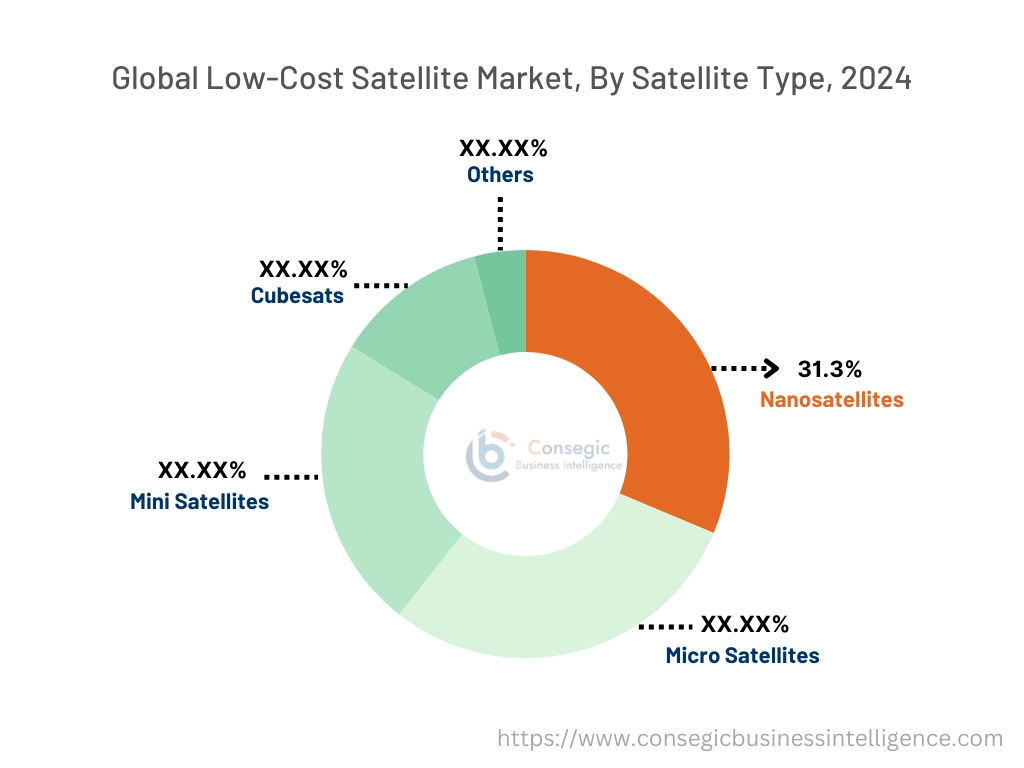

By Satellite Type:

Based on satellite type, the market is segmented into nanosatellites, micro satellites, mini satellites, CubeSats, and others.

The nano satellites segment held the largest revenue of 31.3% of the total low-cost satellite market share in 2024.

- Nano satellites are widely utilized due to their cost efficiency and ease of deployment for applications such as Earth observation and communication.

- These satellites enable governments and commercial entities to rapidly deploy low-cost solutions for research and navigation purposes.

- Their adaptability for educational and experimental missions further strengthens their dominance in the market.

- As per industry trends, increasing demand for compact and efficient satellites drives innovation in nano satellite designs, contributing to the low-cost satellite market expansion.

The CubeSats segment is projected to register the fastest CAGR during the forecast period.

- CubeSats are increasingly popular for space exploration and commercial communication due to their modular design and affordability.

- Advancements in CubeSat technologies have enabled their usage in sophisticated applications such as Earth observation and scientific research.

- Their compact size and interoperability allow multiple CubeSats to be deployed in a single launch, reducing launch costs significantly.

- As per the low-cost satellite market analysis, growing investments in small satellite constellations by private and government organizations further fuel the segment's extension.

By Application:

Based on application, the market is segmented into communication, Earth observation, navigation, scientific research, remote sensing, and others.

The communication segment accounted for the largest revenue of the total low-cost satellite market share in 2024.

- Low-cost satellites are increasingly being deployed to support global communication networks, including rural connectivity and IoT applications.

- Emerging economies rely on communication satellites to bridge the digital divide and improve access to broadband services.

- The rising adoption of satellite-based internet services by businesses and consumers drives the communication segment's growth.

- As per the low-cost satellite market trends, continuous investments in expanding satellite constellations, such as Starlink and OneWeb, further solidify the segment’s dominance.

The Earth observation segment is expected to grow at the fastest CAGR during the forecast period.

- Earth observation satellites are widely used for environmental monitoring, disaster management, and agricultural planning.

- Advancements in imaging and remote sensing technologies enhance the capabilities of low-cost satellites in this segment.

- Governments and private organizations leverage Earth observation data for resource management and infrastructure planning.

- As per the market analysis, the segment's rapid growth is driven by increasing demand for real-time data and high-resolution imagery across multiple industries, fueling the low-cost satellite market growth.

By End-User:

Based on end-use, the market is segmented into commercial and government.

The government segment held the largest revenue share in 2024.

- Government entities deploy low-cost satellites for military communication, surveillance, and disaster response operations.

- National space agencies increasingly collaborate with private players to design and launch cost-effective satellites.

- These satellites are crucial for countries aiming to establish their presence in space without incurring high operational costs.

- Thus, growing interest in space exploration and satellite-based monitoring further supports the dominance of this segment, boosting low-cost satellite market demand.

The commercial segment is expected to register the fastest CAGR during the forecast period.

- Commercial enterprises leverage low-cost satellites for expanding broadband services, enabling IoT solutions, and supporting space tourism initiatives.

- Start-ups and private firms are driving the segment by innovating lightweight satellite technologies and reducing manufacturing costs.

- Increased reliance on satellite-based solutions for navigation, weather forecasting, and global connectivity boosts this segment.

- As per market analysis, rising investments in small satellite constellations and private sector launches accelerate the segment’s progress, which further facilitates the low-cost satellite market expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

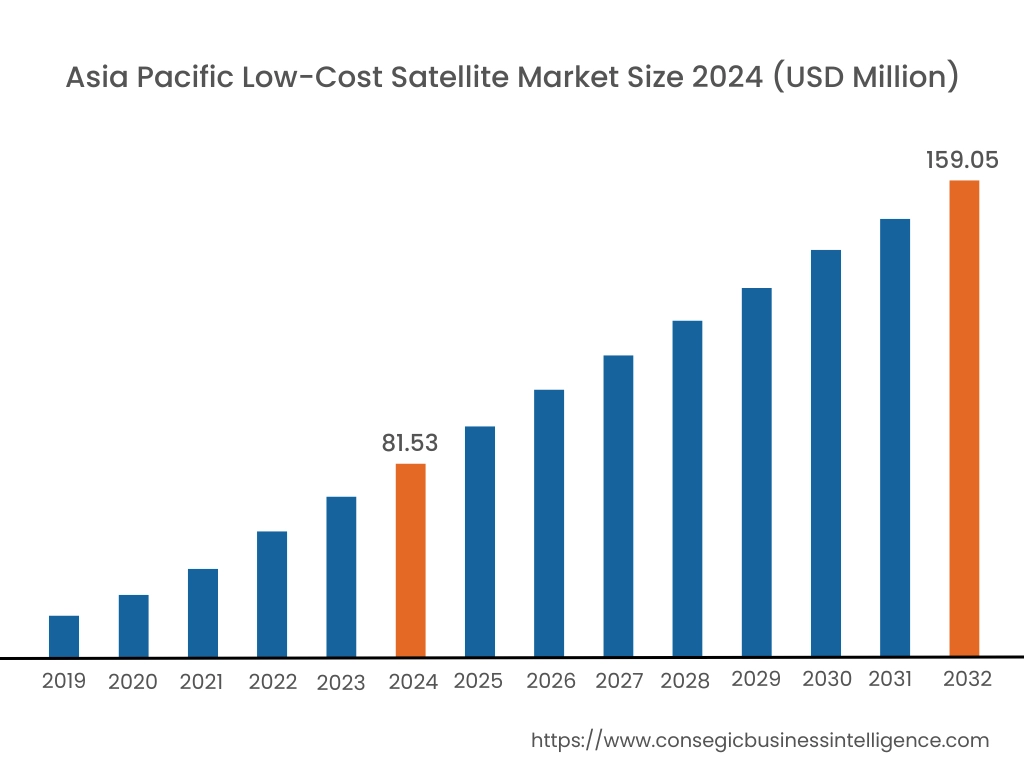

Asia Pacific region was valued at USD 81.53 Million in 2024. Moreover, it is projected to grow by USD 87.06 Million in 2025 and reach over USD 159.05 Million by 2032. Out of this, China accounted for the maximum revenue share of 37.1%. The Asia-Pacific region is experiencing rapid advancements in the low-cost satellite market, driven by industrial enlargement and technological progress in countries such as China, Japan, and India. The proliferation of digital services and the increasing demand for scalable communication infrastructure have intensified the adoption of these satellites. Government initiatives supporting digital economies further influence low-cost satellite market opportunities.

North America is estimated to reach over USD 169.29 Million by 2032 from a value of USD 91.83 Million in 2024 and is projected to grow by USD 97.59 Million in 2025. This region holds a substantial share of the market, driven by early adoption of advanced space technologies and a robust presence of private space enterprises. The United States, in particular, has integrated low-cost satellites across sectors such as communication, Earth observation, and defense. A prominent trend is the incorporation of small satellites, including nanosatellites and microsatellites, to enhance operational efficiency and reduce launch costs. The low-cost satellite market trends indicate that the presence of key industry players and continuous investment in research and development bolster the region's market leadership.

Europe represents a significant segment of the global low-cost satellite market, with countries like Germany, France, and the United Kingdom at the forefront of adoption and innovation. The region's focus on digital transformation and stringent data protection regulations has accelerated the deployment of satellites to ensure compliance and operational agility. Analysis reveals a growth in the trend toward utilizing these satellites in hybrid communication networks to optimize resource utilization and reduce costs.

The Middle East & Africa region is gradually embracing low-cost satellite technologies, particularly within the telecommunications and financial sectors. Nations like the United Arab Emirates are investing in innovative space solutions to enhance service delivery and comply with international standards. Analysis suggests an emerging trend towards adopting low-cost satellites to improve data management efficiency and support digital transformation initiatives.

Latin America is an emerging market with countries such as Brazil and Mexico contributing to its development. The region's focus on modernizing IT infrastructure and improving business agility has spurred interest in low-cost satellite solutions. As per the low-cost satellite market analysis, government policies aimed at enhancing technological capabilities influence market trends.

Top Key Players and Market Share Insights:

The Low-Cost Satellite market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Low-Cost Satellite market. Key players in the Low-Cost Satellite industry include -

- SpaceX (USA)

- OneWeb (UK)

- Thales Alenia Space (France)

- Surrey Satellite Technology Limited (SSTL) (UK)

- Astrocast (Switzerland)

- Planet Labs (USA)

- Rocket Lab (USA)

- Blue Canyon Technologies (USA)

- AAC Clyde Space (Sweden)

- Sierra Nevada Corporation (USA)

Recent Industry Developments :

Partnerships & Collaborations:

- In September 2023, SpinLaunch and Sumitomo Corporation partnered to advance the global commercialization of low-cost, sustainable space solutions. SpinLaunch's electric-powered mass accelerator technology reduces fuel usage and emissions for small satellite launches. Sumitomo, now an investor, will represent this technology in Japan, enhancing access to space for national security and private sectors. Both aim to meet rising satellite demands while promoting environmentally sustainable practices, aligning with industry trends for rapid, affordable, and eco-friendly space services.

Low-Cost Satellite Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 522.35 Million |

| CAGR (2025-2032) | 8.3% |

| By Satellite Type |

|

| By Application |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Low-Cost Satellite Market? +

The Low-Cost Satellite Market size is estimated to reach over USD 522.35 Million by 2032 from a value of USD 276.84 Million in 2024 and is projected to grow by USD 294.77 Million in 2025, growing at a CAGR of 8.3% from 2025 to 2032.

What are the key segments in the Low-Cost Satellite Market? +

The Low-Cost Satellite market is segmented by satellite type (nano satellites, micro satellites, mini satellites, CubeSats, others), application (communication, Earth observation, navigation, scientific research, remote sensing, others), end-use (commercial, government), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which segment is expected to grow the fastest in the Low-Cost Satellite Market? +

The CubeSats segment is expected to register the fastest CAGR during the forecast period. This growth is driven by their modular design, affordability, and versatility in space exploration and communication applications.

Who are the major players in the Low-Cost Satellite Market? +

Major players in the Low-Cost Satellite market include SpaceX (USA), OneWeb (UK), Planet Labs (USA), Rocket Lab (USA), Blue Canyon Technologies (USA), AAC Clyde Space (Sweden), Sierra Nevada Corporation (USA), Thales Alenia Space (France), Surrey Satellite Technology Limited (SSTL) (UK), and Astrocast (Switzerland).