- Summary

- Table Of Content

- Methodology

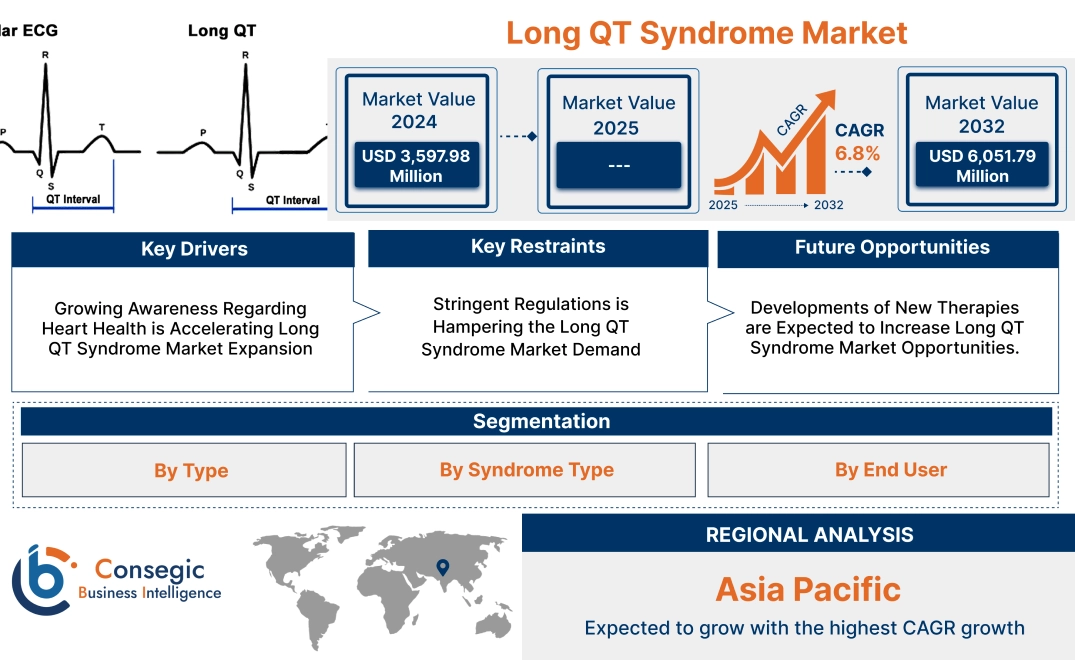

Long QT Syndrome Market Size:

Long QT Syndrome Market size is growing with a CAGR of 6.8% during the forecast period (2025-2032), and the market is projected to be valued at USD 6,051.79 Million by 2032 from USD 3,597.98 Million in 2024.

Long QT Syndrome Market Scope & Overview:

Long QT syndrome (LQTS) is a heart rhythm disorder that affects the electrical activity of the heart, causing prolonged QT intervals on an electrocardiogram (ECG). LQTS is congenital (inherited) or acquired. Congenital LQTS arises from genetic mutations affecting ion channels in heart cells, with subtypes such as LQT1, LQT2, and LQT3. Acquired LQTS occurs due to external factors such as certain medications (e.g., antiarrhythmics, antidepressants, antibiotics), electrolyte imbalances, or medical conditions such as hypothyroidism. Symptoms include palpitations, dizziness, fainting, seizures, or cardiac arrest, especially during physical exertion, emotional stress, or sleep. Some individuals remain asymptomatic but are still at risk. Treatment depends on severity and type. Medications such as beta-blockers (e.g., propranolol, nadolol) are commonly used to prevent arrhythmias. Severe cases require surgical devices such as implantable cardioverter defibrillators (ICDs) or pacemakers to regulate heart rhythms. Left cardiac sympathetic denervation (LCSD) surgery is performed in resistant cases. Lifestyle modifications, such as avoiding triggers, are also essential for managing the condition.

Long QT Syndrome Market Dynamics - (DRO) :

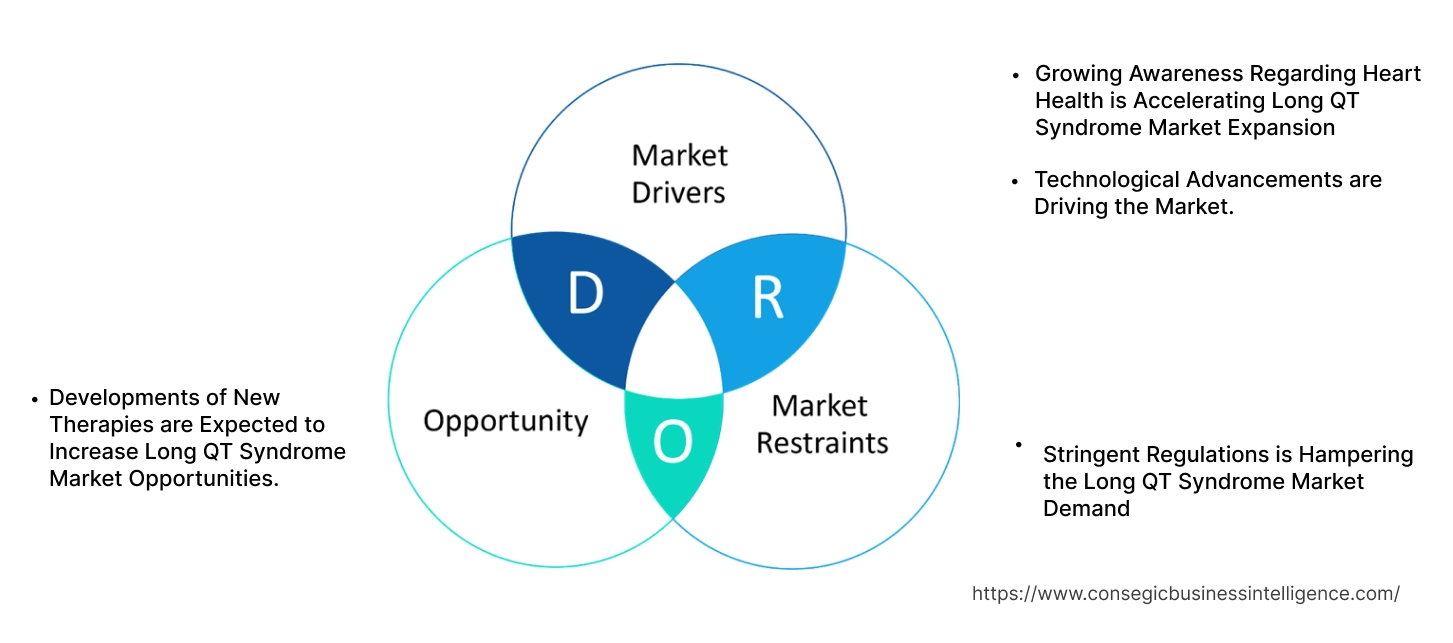

Key Drivers:

Growing Awareness Regarding Heart Health is Accelerating Long QT Syndrome Market Expansion

Growing awareness of LQTS is a crucial driver for the market, as it directly influences the early detection, diagnosis, and management of the condition. LQTS, a potentially life-threatening heart rhythm disorder, goes undiagnosed due to its asymptomatic nature or misinterpretation of symptoms. However, there have been concerted efforts by medical societies, patient advocacy groups, and healthcare organizations to educate people about the risks and signs of LQTS.

- Mayo Clinic published an article, in 2024, providing comprehensive information on long QT syndrome, encompassing its definition, key symptoms, underlying causes, contributing risk factors, potential complications, and preventative measures. This has increased visits regarding LQTS, positively influencing the long QT syndrome market trends.

Moreover, awareness campaigns emphasize recognizing symptoms such as fainting, palpitations, and seizures, particularly during physical activity or emotional stress. This is especially critical for congenital LQTS, which affects children and adolescents, where early diagnosis prevents sudden cardiac events. Additionally, healthcare providers are becoming more knowledgeable about LQTS, and improving screening protocols during routine check-ups, pre-surgery evaluations, and ECG monitoring.

Overall, growing awareness is significantly boosting the long QT syndrome market expansion.

Technological Advancements are Driving the Market.

Technological advancements are significantly shaping the market, enhancing diagnostics, monitoring, and treatment options. One key area of innovation is advanced genetic testing technology, which has made testing faster, more accurate, and widely accessible. These advancements enable early detection of LQTS by identifying specific genetic mutations, allowing for personalized treatment approaches.

Moreover, diagnostic technologies such as advanced electrocardiogram (ECG) machines, Holter monitors, and wearable devices are transforming how LQTS is identified and monitored. Wearable ECG devices now offer real-time heart monitoring, providing continuous data on QT intervals, even during everyday activities, and improving patient outcomes. Additionally, AI also enhances diagnosis.

- According to an article published in the National Center for Biotechnology Information, in 2024, AI models are trained on large datasets of genetically confirmed cases, which then identify subtle ECG features beyond the QT interval. This enhances diagnostic accuracy and aids risk stratification. This has increased its applications, positively influencing the long QT syndrome market trends.

Overall, technological advancements, including advanced genetic testing, advanced ECGs, wearable devices, and AI-powered diagnostics are accelerating the global long QT syndrome market growth.

Key Restraints:

Stringent Regulations is Hampering the Long QT Syndrome Market Demand

Regulatory hurdles are one of the significant barriers to market long QT syndrome market growth. Medical devices and medicines used in treatments are subject to strict regulations by authorities such as the U.S. FDA, the European Medicines Agency (EMA), and other national regulatory bodies. These regulations ensure the safety, efficacy, and quality of products, but this process is time-consuming and expensive, requiring significant investment from manufacturers.

The approval process for these medicines and medical devices is lengthy and costly. Manufacturers must conduct extensive trials, including preclinical studies, phase 1, 2, and 3 clinical trials which demonstrate compliance with safety standards of their products before they receive approval. This process not only delays the availability but also increases the cost of development, which is ultimately passed on to consumers and healthcare providers.

Furthermore, variations in regulatory standards across different regions further complicate market entry for companies. What is approved in one country takes additional time in another, making it difficult for global companies to maintain a seamless product launch strategy.

Overall, analysis shows that the stringent regulatory requirements along with lengthy approval processes and varying regulatory standards across different regions are hampering the long QT syndrome market demand.

Future Opportunities :

Developments of New Therapies are Expected to Increase Long QT Syndrome Market Opportunities.

The development of new therapies creates potential for the market, driven by the growing demand for innovative, effective, and patient-specific treatment solutions. Traditional therapies such as beta blockers and antiarrhythmics have limitations, including side effects and variable efficacy, particularly across different LQTS subtypes (e.g., LQT1, LQT2, LQT3). As a result, there is a strong focus on research and development (R&D) to create targeted therapies that address these challenges.

- In 2024, Thryv Therapeutics Inc. announced positive top-line results from their Wave I Part 2 proof-of-concept clinical study. This study investigated the efficacy and safety of LQT-1213, a new drug, in treating patients with congenital long QT syndrome type 2 and 3. This type of upcoming therapy could offer a novel treatment option for patients with these specific subtypes of LQTS, potentially improving their quality of life, and creating potential for the market.

Moreover, biologics and gene therapies offer transformative potential by addressing the root causes of LQTS rather than just managing symptoms. Innovations in RNA-based treatments and CRISPR technology could positively influence the management of congenital LQTS.

Overall, the development of new therapies is expected to increase long QT syndrome market opportunities.

Long QT Syndrome Market Segmental Analysis :

By Type:

Based on type, the market is categorized into diagnosis and treatment.

Trends in Type:

- Increased accuracy and accessibility of genetic testing, including next-generation sequencing (NGS).

- Longer-lasting and more sophisticated ICDs with advanced features are improving treatment outcomes.

The treatment segment accounted for the largest market share in 2024 and is expected to grow at the fastest CAGR over the forecast period.

- Treatment is further categorized into medications, and surgical. The treatment segment dominates the market because it directly addresses the life-threatening nature of the disorder. LQTS, if left untreated, leads to sudden cardiac arrest or other severe arrhythmias, making effective treatment essential.

- Currently, the primary treatments involve beta-blockers, antiarrhythmic medications, and implantable cardioverter defibrillators (ICDs). These interventions are critical in managing symptoms and preventing sudden cardiac death, particularly in high-risk patients. New product launches with better outcomes for patients are driving the segment.

- For instance, in 2024, MicroPort received approval for their PLATINIUM implantable cardioverter defibrillator. It is designed for long-term use, with an expected lifespan exceeding 14 years, minimizing the need for frequent replacements. Also, it incorporates advanced algorithms to accurately identify heart rhythms and avoid unnecessary treatments. This has increased its reach for patients, thus driving the segment in the market.

- Furthermore, at the same time, treatment is emerging due to significant advancements in gene therapy, biologics, and personalized medicine. Targeted therapies are being developed to address specific genetic mutations, offering more precise and effective treatments with fewer side effects.

- Overall, as per the market analysis, the availability of advanced treatments and the emergence of novel therapies are driving segmental growth.

By Syndrome Type:

The syndrome type segment is categorized into congenital and acquired.

Trends in the Syndrome Type:

- Increased emphasis on understanding the genetic basis of congenital LQTS subtypes and their impact on treatment outcomes.

- Significant efforts are being made to improve early detection and screening programs for acquired LQTS.

The congenital segment accounted for the largest market share in 2024.

- As a hereditary condition, congenital LQTS is passed down through genetic mutations, making it a well-defined and widely studied form of the disorder.

- The lifelong nature of congenital LQTS necessitates continuous monitoring and management, driving a consistent demand for diagnostic tests, medications such as beta-blockers, and potentially implantable devices such as ICDs.

- The ability to detect congenital LQTS early, in infancy or childhood, has driven significant advancements in genetic testing and screening methods, such as genetic panels and ECGs, which are key for identifying at-risk individuals before symptoms appear. Technological advancements in congenital screening are driving the segment.

- For instance, according to an article published in the National Center for Biotechnology Information, in 2024, a deep learning model has a better ability to enhance the detection of congenital long QT syndrome and effectively differentiate between its various genetic subtypes. This adoption of a deep learning model has helped in early detection, leading to better management strategies and positively influencing the market share.

- Overall, as per the market analysis advancements in diagnosis and treatment options are driving this segmental growth in the long QT syndrome industry.

The acquired segment is expected to grow at the fastest CAGR over the forecast period.

- Acquired LQTS is emerging as a significant segment in the market due to the increasing prevalence of conditions that contribute to its onset, particularly the growing use of medications that prolong the QT interval and the rising incidence of cardiovascular diseases.

- Acquired LQTS is triggered by external factors such as certain medications, electrolyte imbalances, or underlying medical conditions such as heart disease, diabetes, and kidney dysfunction. The broader use of medications, particularly antiarrhythmics, antibiotics, and antidepressants, known to cause QT prolongation, has contributed to an increase in acquired LQTS diagnoses.

- As the aging population and the use of polypharmacy rise, the risk of acquired LQTS becomes more pronounced, leading to greater recognition and treatment demand in this segment.

- The increasing awareness of the acquired LQTS, coupled with its link to more common and treatable conditions, creates the potential for the segment in the upcoming years.

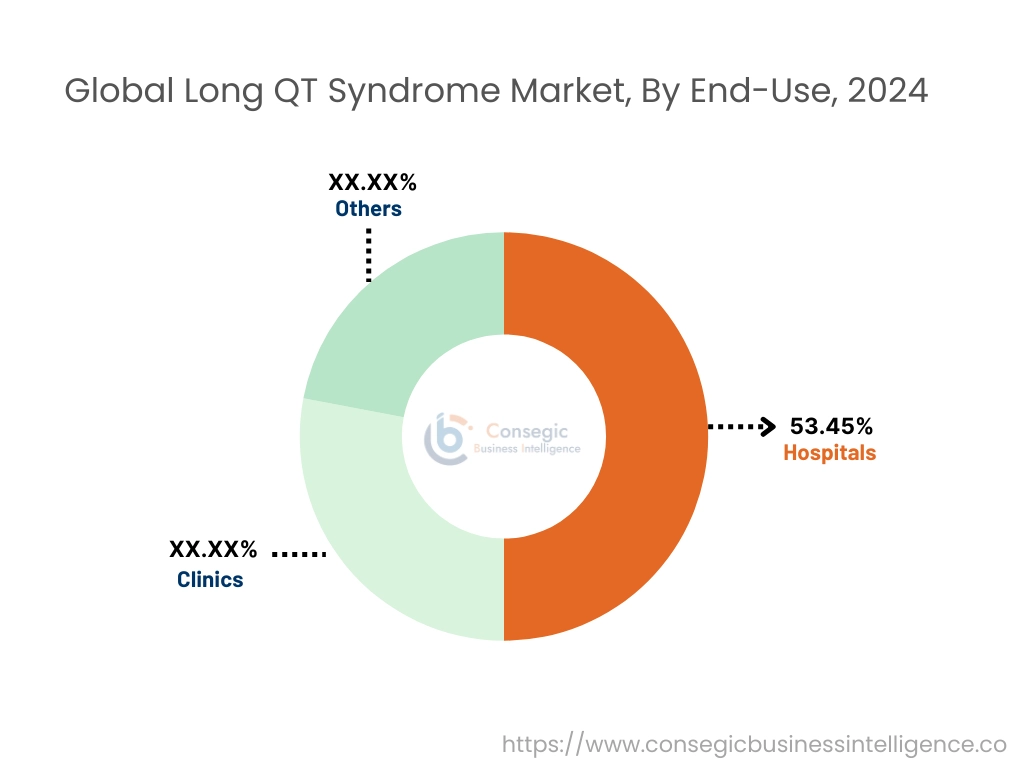

By End User:

The end-use segment is categorized into hospitals, clinics, and others.

Trends in End-Use:

- Integration of AI and machine learning in hospitals for improved diagnosis and risk stratification.

- Focus on patient education and awareness programs within clinic settings.

The hospital's segment accounted for the largest market share of 53.45% in 2024.

- LQTS requires advanced diagnostic testing, urgent interventions, and long-term management, all of which are typically best handled in a hospital setting.

- Moreover, for patients with severe symptoms, such as life-threatening arrhythmia or sudden cardiac arrest, hospitals offer the necessary infrastructure for emergency care, including advanced ECG monitoring, genetic testing, and implantable cardioverter defibrillators, which are crucial for stabilizing patients and preventing fatalities.

- Their dominance is further driven by the high influx of patients due to referral systems, insurance coverage, and the trust associated with hospital-based treatments. The development of healthcare industry infrastructure, especially in emerging economies, also boosts the requirements.

- For instance, according toFinancial Express, the number of hospitals in India increased by 27% from 20219 to 2024, rising from 30,000 to 38,000. Consequently, this surge in hospitals has contributed to a higher volume of diagnostics and treatments related to LQTS, positively driving the segment in the market.

- Overall, high patient volume, advanced infrastructure, and a rising number of hospitals are driving the segment.

The clinics segment is expected to grow at the fastest CAGR over the forecast period.

- Clinics are emerging in the LQTS market due to their growing role in providing accessible, specialized, and cost-effective care for early diagnosis and long-term management of the condition.

- With advancements in diagnostic tools such as ECG screenings, genetic testing, and portable cardiac monitors, clinics are increasingly equipped to detect and monitor LQTS in outpatient settings. This shift aligns with the healthcare trend toward preventive care and early intervention, making clinics an essential point of contact for patients seeking timely and less invasive management of LQTS.

- One of the main reasons for the emergence of clinics is their convenience and affordability compared to hospital visits. Patients with mild or moderate symptoms, or those requiring routine follow-ups, prefer clinics for their shorter wait times, personalized care, and reduced costs.

- Clinics also cater to patients for long-term treatments, such as beta-blockers or antiarrhythmic medications, by offering consistent monitoring and adjustments to therapy plans.

- According to market analysis, the increasing prevalence of LQTS and growing awareness of its symptoms among the general population and healthcare providers have led to increased referrals to cardiology and genetic counseling clinics and that will drive segmental growth for the upcoming years.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

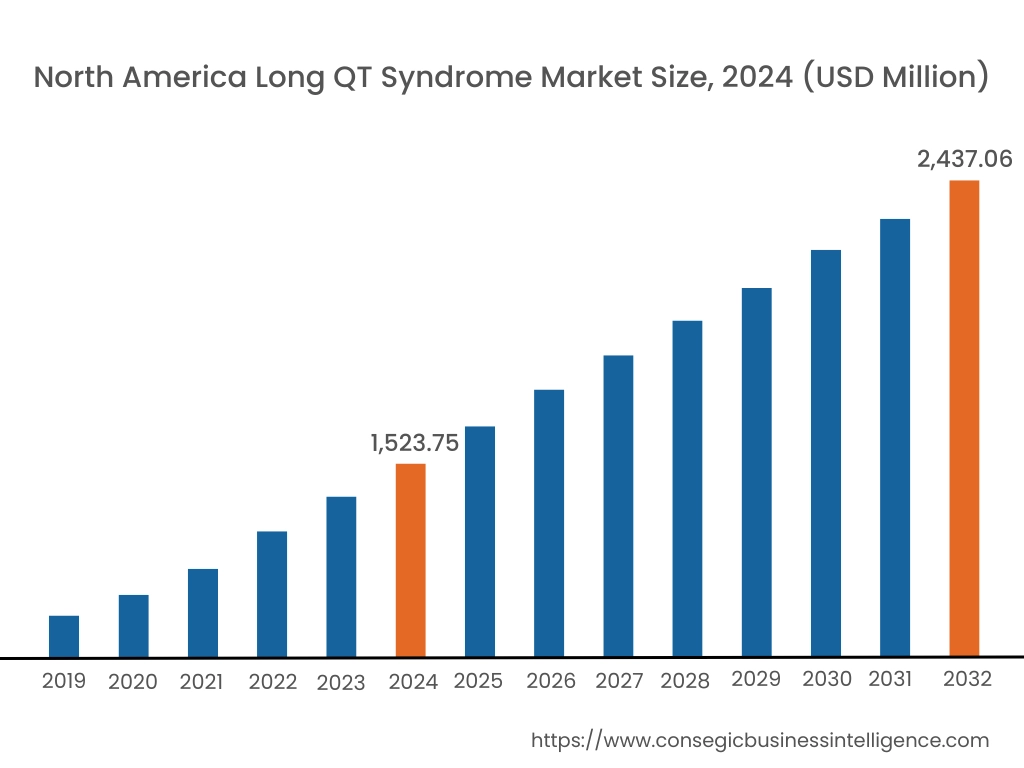

In 2024, North America accounted for the highest long QT syndrome market share at 42.36% and was valued at USD 1,523.75 Million and is expected to reach USD 2,437.06 Million in 2032. In North America, the U.S. accounted for the highest long QT syndrome market share of 71.18% during the base year of 2024. The market is driven by several key trends. The region benefits from the widespread availability of cutting-edge diagnostic technologies such as genetic testing, ECG monitoring systems, and advanced cardiac imaging tools, which enable early detection and management of LQTS.

- In 2023, Quest Diagnostics announced the launch of its first consumer-initiated genetic test called genetic insights, which allows individuals to assess their risk of developing inheritable heart health conditions by analyzing their DNA through a saliva sample. This test provides personalized health reports and access to genetic counseling. This type of new method has increased the reach of testing and screening, positively influencing market in the region.

Moreover, North America has a well-established network of specialized cardiology centers and hospitals that cater to both congenital and acquired LQTS cases, providing comprehensive care. Additionally, the prevalence of LQTS in North America is also linked to better disease awareness and proactive healthcare practices. Regular health check-ups and screening programs, especially for at-risk populations, contribute to higher detection rates of congenital and acquired LQTS. Furthermore, the region’s robust healthcare policies and insurance systems also ensure greater access to diagnostic and treatment options, including the use of beta-blockers, antiarrhythmic drugs, and implantable cardioverter defibrillators. Overall, the North American market is driven by factors such as widespread access to advanced diagnostics, a robust healthcare infrastructure, high disease awareness, and proactive healthcare practices, leading to early detection and improved patient outcomes.

In Asia Pacific, the long QT syndrome market is experiencing the fastest growth with a CAGR of 8.0% over the forecast period. The region has witnessed significant improvements in healthcare access, particularly in countries such as China, India, and Japan, where government initiatives and private investments are strengthening the capabilities of healthcare facilities. This expansion is enabling earlier diagnosis and better management of both congenital and acquired LQTS. Moreover, the prevalence of acquired LQTS is on the rise in APAC due to the growing aging population and the increasing incidence of cardiovascular diseases, diabetes, and other chronic conditions. Additionally, the widespread use of medications known to cause QT prolongation, such as antibiotics and antidepressants, has amplified the need for screening and treatment solutions. This has led to greater demand for ECGs, genetic testing, and cardiac monitoring devices in the region. Rising awareness campaigns and educational programs are also contributing to the growth of the market in APAC.

Europe's long QT syndrome market analysis states that several trends are responsible for the progress of the market in the region. The market is driven by its strong healthcare infrastructure, established medical research capabilities, and high prevalence of cardiovascular disorders. Countries such as Germany, France, and the UK are leading in the adoption of advanced diagnostic tools, such as genetic testing and high-resolution ECGs, to identify LQTS cases. Moreover, European regulatory agencies also promote patient safety by closely monitoring medications known to cause acquired LQTS, reducing the risk of drug-induced complications. Additionally, Europe has a growing focus on public health awareness campaigns addressing congenital heart conditions, driving early diagnosis and intervention. The increasing availability of implantable devices such as pacemakers and ICDs in developed countries is further propelling market growth. The European market is also benefiting from collaborations between research institutions and pharmaceutical companies for the development of gene therapies targeting hereditary LQTS, enhancing treatment options.

The Middle East and Africa (MEA) long QT syndrome market analysis states that the region is also witnessing a notable surge. The market is driven by rising awareness of cardiac health and improving healthcare infrastructure in key countries such as Saudi Arabia, the UAE, and South Africa. Governments in the Gulf Cooperation Council (GCC) region are investing in modern healthcare facilities equipped with ECG monitoring systems and genetic testing capabilities, which support early diagnosis of congenital LQTS. In Africa, the prevalence of acquired LQTS is increasing due to antimalarial drug use and limited regulation of QT-prolonging medications. Efforts by non-governmental organizations and international partnerships are addressing this issue by enhancing healthcare accessibility and training programs for healthcare workers. However, limited awareness and affordability issues in low-income regions remain challenges to market.

Latin America's long QT syndrome market size is also emerging. The market is driven by trends such as increasing awareness of hereditary cardiac conditions and improving healthcare systems across countries such as Brazil, Mexico, and Argentina. Brazil leads the market with its advanced cardiology centers and ongoing initiatives for early genetic screening programs. Mexico is also investing in electrophysiology labs to diagnose arrhythmias, contributing to the market. Moreover, telehealth services are gaining traction in rural areas, enabling long-term monitoring for LQTS patients using wearable ECG devices. Additionally, the availability of affordable beta-blockers and antiarrhythmic drugs is enhancing treatment accessibility. Latin America is also attracting clinical trials for novel therapies, leveraging its diverse genetic population to advance research on congenital LQTS. Despite these advancements, the region faces challenges such as uneven healthcare access and insufficient insurance coverage for specialized treatments.

Top Key Players and Market Share Insights:

The Long QT Syndrome market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global Long QT Syndrome market. Key players in The Long QT Syndrome industry include-

- Boston Scientific (U.S.)

- Medtronic, Inc (Ireland)

- Thermo Fisher Scientific (U.S.)

- Abbott Laboratories (U.S.)

- Boehringer Ingelheim (Germany)

- Pfizer (U.S.)

- Lupin Pharmaceuticals, Inc. (U.S.)

- AstraZeneca (U.S.)

- Biotronik (Germany)

- Teva Pharmaceutical (Israel)

Recent Industry Developments :

Product Launch:

- In October 2023, Medtronic received FDA approval for its Aurora EV-ICD MRI SureScan and Epsila EV MRI SureScan defibrillation This system is designed to treat potentially fatal heart rhythm disorders, such as those that lead to sudden cardiac arrest.

Long QT Syndrome Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 6,051.79 Million |

| CAGR (2025-2032) | 6.8% |

| By Type |

|

| By Syndrome Type |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Long QT Syndrome market? +

In 2024, the Long QT Syndrome market is USD 3,597.98 Million.

Which is the fastest-growing region in the Long QT Syndrome market? +

Asia Pacific is the fastest-growing region in the Long QT Syndrome market.

What specific segmentation details are covered in the Long QT Syndrome market? +

Type and Syndrome Type segmentation details are covered in the Long QT Syndrome market.

Who are the major players in the Long QT Syndrome market? +

Boston Scientific (U.S.), Medtronic, Inc. (Ireland), Pfizer (U.S.), Lupin Pharmaceuticals, Inc. (U.S.), AstraZeneca (U.S.), Biotronik (Germany), Teva Pharmaceutical (Israel), Thermo Fisher Scientific (U.S.), Abbott Laboratories (U.S.), and Boehringer Ingelheim (Germany).