- Summary

- Table Of Content

- Methodology

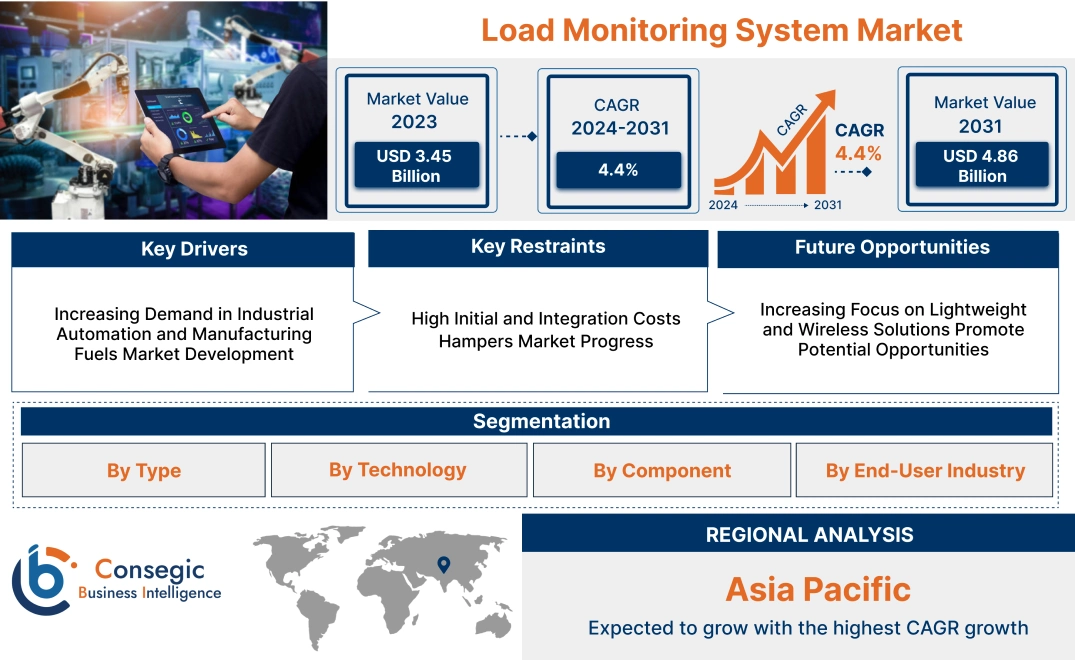

Load Monitoring System Market Size:

Load Monitoring System Market size is estimated to reach over USD 4.86 Billion by 2031 from a value of USD 3.45 Billion in 2023 and is projected to grow by USD 3.54 Billion in 2024, growing at a CAGR of 4.4% from 2024 to 2031.

Load Monitoring System Market Scope & Overview:

A load monitoring system is an advanced solution designed to measure and monitor the weight or force applied to a structure or equipment in real time. These systems utilize load cells, sensors, and data acquisition devices to provide accurate and reliable measurements, ensuring safety and efficiency in various industrial applications. Load monitoring systems are integral to operations in industries such as manufacturing, construction, aerospace, and energy, where precise load measurement is critical to maintaining operational integrity and preventing equipment failure.

These systems are available in different configurations, including wireless and wired setups, catering to specific operational requirements. They are engineered for high accuracy and durability, even in challenging environments, such as high-pressure or extreme temperature conditions. Modern load monitoring systems also integrate with advanced software platforms, allowing users to collect, analyze, and transmit data for enhanced decision-making and operational control.

End-users of these systems include construction firms, aerospace manufacturers, logistics companies, and energy sector operators, who depend on precise load measurement to ensure compliance with safety standards, optimize resource utilization, and enhance operational performance across various applications.

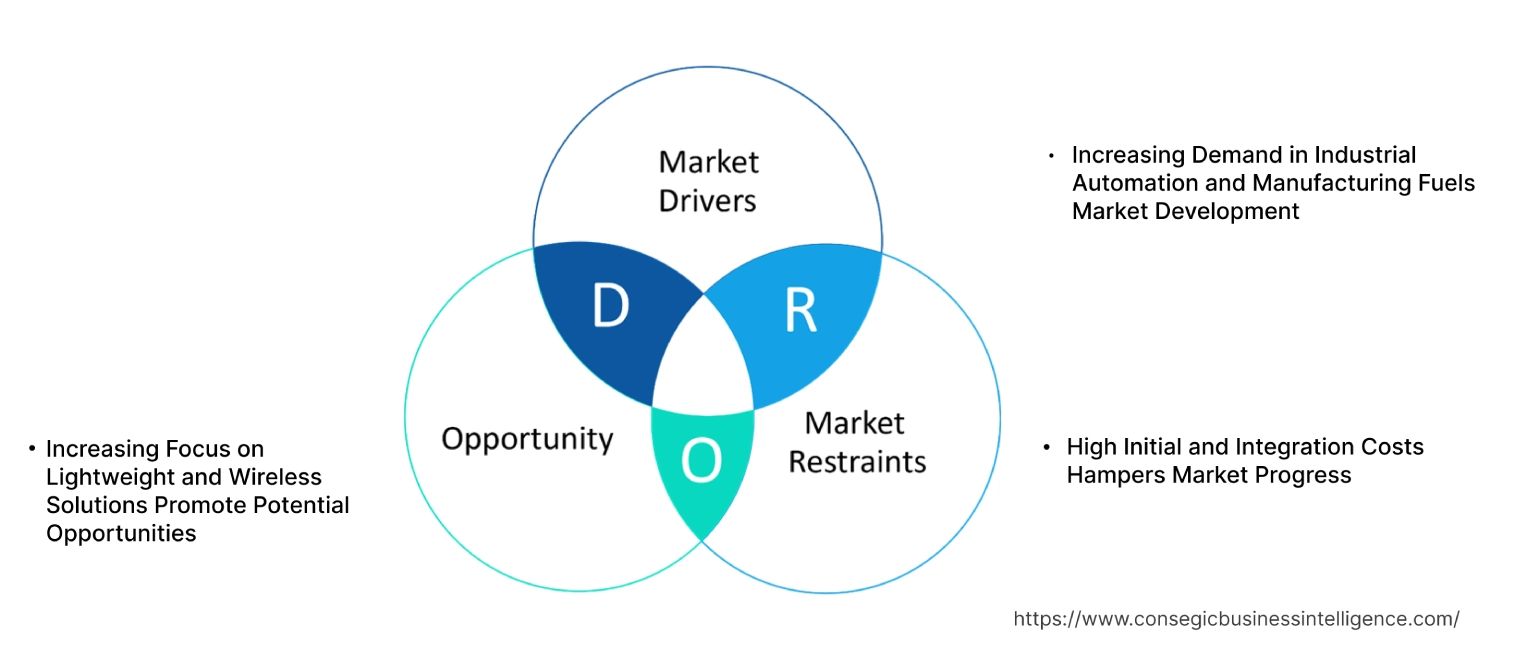

Load Monitoring System MarketDynamics - (DRO) :

Key Drivers:

Increasing Demand in Industrial Automation and Manufacturing Fuels Market Development

The rapid adoption of industrial automation is driving the need for advanced monitoring systems that provide precise load measurement and control in manufacturing processes. Industries such as automotive, aerospace, and electronics are increasingly relying on real-time data to improve production efficiency, maintain product quality, and reduce operational downtime. Load monitoring systems play a critical role in accurately measuring force, weight, and tension, ensuring smooth operations and enabling predictive maintenance to prevent equipment failures.

Emerging trends in manufacturing, such as robotics, smart factories, and advanced material handling systems, are further accelerating the demand for these solutions. They enhance operational efficiency by integrating with automated workflows, optimizing machine performance, and supporting compliance with stringent safety standards. As automation continues to transform industrial processes, these systems are becoming indispensable for maintaining precision, reliability, and productivity in modern manufacturing environments, driving load monitoring system market growth.

Key Restraints :

High Initial and Integration Costs Hampers Market Progress

The implementation of advanced monitoring systems often involves high initial costs, including expenses for sensors, hardware, software, and the technical expertise required for deployment. These costs are particularly restraining for small and medium-sized enterprises (SMEs) with limited budgets. Additionally, integrating monitoring systems into existing infrastructure or legacy equipment requires significant investment in customization and compatibility solutions, further increasing expenses.

The complexity of installation and calibration processes also adds to the total cost, especially in industries with unique operational requirements, such as aerospace, manufacturing, and energy. For some organizations, these financial barriers hinder the adoption of advanced monitoring technologies, particularly in cost-sensitive regions or sectors. The combination of high upfront investment and the demand for specialized integration creates constraints for widespread adoption, slowing load monitoring system market demand in certain applications and industries.

Future Opportunities :

Increasing Focus on Lightweight and Wireless Solutions Promote Potential Opportunities

The shift toward lightweight and wireless monitoring systems is revolutionizing the market by addressing critical challenges in portability and installation efficiency. Wireless systems eliminate the need for complex cabling, reducing setup time and costs, and making them ideal for temporary or mobile applications, such as event management, short-term construction projects, and disaster response. Their compact and modular design also facilitates easy integration into existing systems without significant modifications.

Emerging trends in industries like manufacturing, logistics, and energy are driving the adoption of these systems in remote and hard-to-access locations, where traditional wired solutions are impractical. Wireless solutions also enable real-time data transmission and monitoring, enhancing operational flexibility and scalability. As industries increasingly prioritize efficiency, mobility, and connectivity, lightweight and wireless monitoring systems are positioned to meet evolving demands, ensuring load monitoring system market opportunities across diverse applications and geographies.

Load Monitoring System Market Segmental Analysis :

By Type:

Based on type, the market is segmented into Analog Load Monitoring and Digital Load Monitoring.

The Digital Load Monitoring segment accounted for the largest revenue of the total load monitoring system market share in 2023.

- Digital load monitoring systems provide precise measurements and seamless data integration with modern software solutions, making them ideal for industries requiring high accuracy.

- These systems are widely adopted in manufacturing and automotive industries for applications such as quality control and performance testing.

- Digital solutions support real-time monitoring and predictive maintenance, reducing downtime and operational inefficiencies.

- As per load monitoring system market analysis, trends in industrial automation and the adoption of Industry 4.0 are driving the adoption of this segment across various sectors.

The Analog Load Monitoring segment is expected to register the fastest CAGR during the forecast period.

- Analog systems are cost-effective and offer reliable performance in applications where basic load measurement is sufficient, such as small-scale manufacturing and construction.

- These systems are preferred in regions with limited access to advanced infrastructure or high-speed connectivity.

- The rapid growth of this segment is supported by its simplicity, ease of installation, and long-standing presence in traditional industries.

- Market trends indicate that analog systems continue to play a crucial role in operations requiring durable and low-maintenance monitoring solutions, contributing to the load monitoring system market expansion.

By Technology:

Based on technology, the market is segmented into Wired Load Monitoring and Wireless Load Monitoring.

The Wireless Load Monitoring segment held the largest revenue of the total load monitoring system market share in 2023.

- Wireless systems are increasingly favored for their flexibility, ease of installation, and ability to operate in remote or hard-to-access locations.

- These systems are widely used in the aerospace and construction sectors, where traditional wired connections are impractical.

- Wireless solutions support real-time data transmission to centralized control systems, enhancing operational efficiency and decision-making.

- As per load monitoring system market trends, the dominance of this segment is driven by trends in remote monitoring and the need for scalable solutions in complex industrial environments.

The Wired Load Monitoring segment is expected to register the fastest CAGR during the forecast period.

- Wired systems are known for their reliability and accuracy, making them ideal for applications in manufacturing and energy industries.

- These systems offer uninterrupted data transmission, ensuring consistent performance even in environments with high electromagnetic interference.

- The rapid growth of this segment reflects its importance in critical applications requiring stable and precise load measurements.

- As per market analysis, wired systems remain a preferred choice in applications with fixed setups and long-term operations, facilitating the load monitoring system market growth.

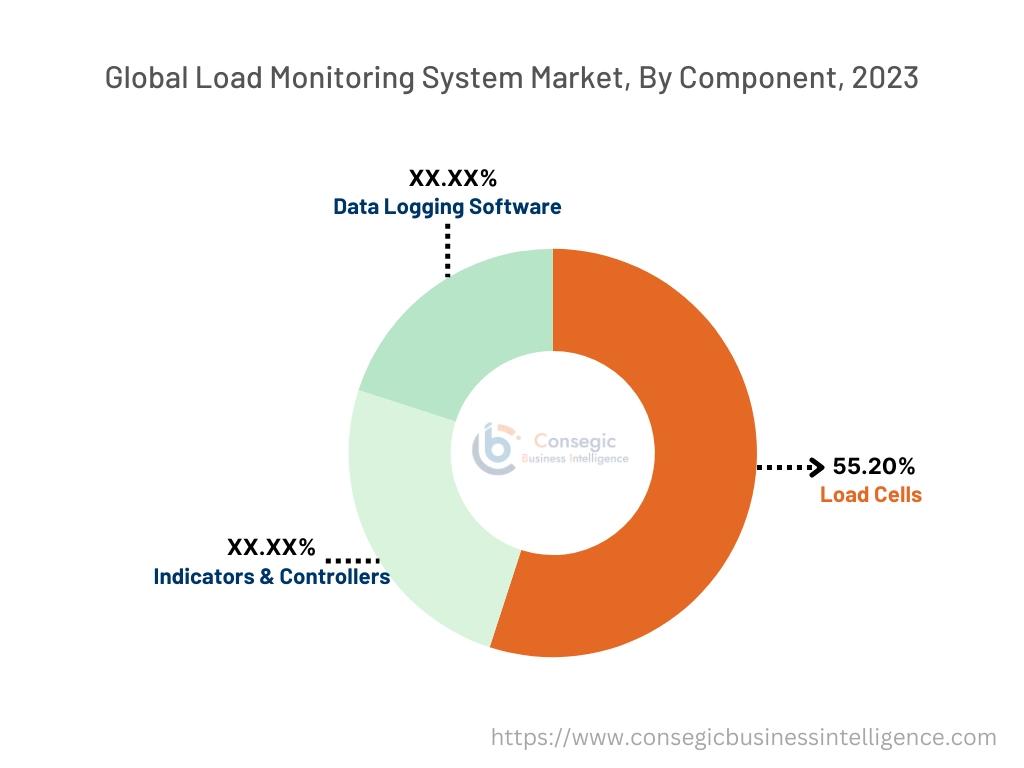

By Component:

Based on components, the market is segmented into Load Cells, Indicators & Controllers, and Data Logging Software.

The Load Cells segment held the largest revenue of 55.20% share in 2023.

- Load cells are the primary sensing components in load monitoring systems, providing accurate force and weight measurements across various applications.

- They are widely used in manufacturing, automotive, and aerospace industries for testing, quality control, and safety assurance.

- Innovations in load cell technology, such as miniaturization and enhanced durability, are expanding their use in compact and harsh environments.

- As per load monitoring system market analysis, the dominance of this segment reflects its critical role in enabling accurate and reliable load monitoring across diverse industries.

The Data Logging Software segment is expected to register the fastest CAGR during the forecast period.

- Data logging software enables real-time data visualization, analysis, and reporting, ensuring actionable insights for process optimization.

- These tools are widely adopted in energy and automotive industries for predictive maintenance and performance benchmarking.

- Market trends highlight the increasing integration of AI and machine learning algorithms in data logging software for advanced analytics and decision-making.

- The rapid growth of this segment is driven by the rising focus on data-driven operations and continuous performance improvement, which contributes to the load monitoring system market demand.

By End-User Industry:

Based on end-user industry, the market is segmented into Manufacturing, Aerospace & Defense, Construction, Energy & Utilities, Automotive, and Others.

The Manufacturing segment held the largest revenue share in 2023.

- Load monitoring systems are extensively used in manufacturing for applications such as material testing, equipment calibration, and process control.

- The adoption of load monitoring solutions supports operational safety, quality assurance, and regulatory compliance in industrial operations.

- Trends in smart factories and industrial automation are driving the integration of these systems with advanced robotics and control systems.

- The dominance of this segment reflects its essential role in optimizing manufacturing processes and ensuring operational efficiency, driving load monitoring system market expansion.

The Aerospace & Defense segment is expected to register the fastest CAGR during the forecast period.

- The aerospace and defense sector relies on load monitoring systems for aircraft testing, structural analysis, and component validation.

- These systems are critical for ensuring safety and reliability in applications requiring high precision and performance under extreme conditions.

- Market trends highlight the increasing use of wireless load monitoring solutions in aerospace for remote and complex testing scenarios.

- The rapid growth of this segment reflects its importance in meeting stringent safety standards and operational requirements in the aerospace sector, fueling load monitoring system market opportunities.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

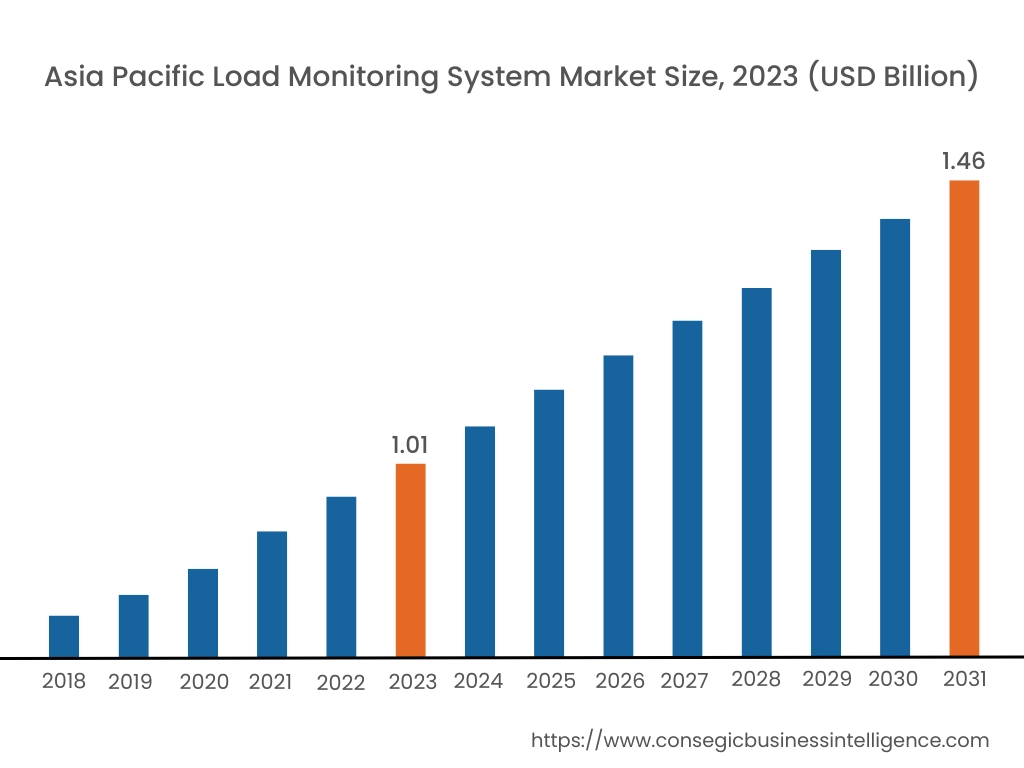

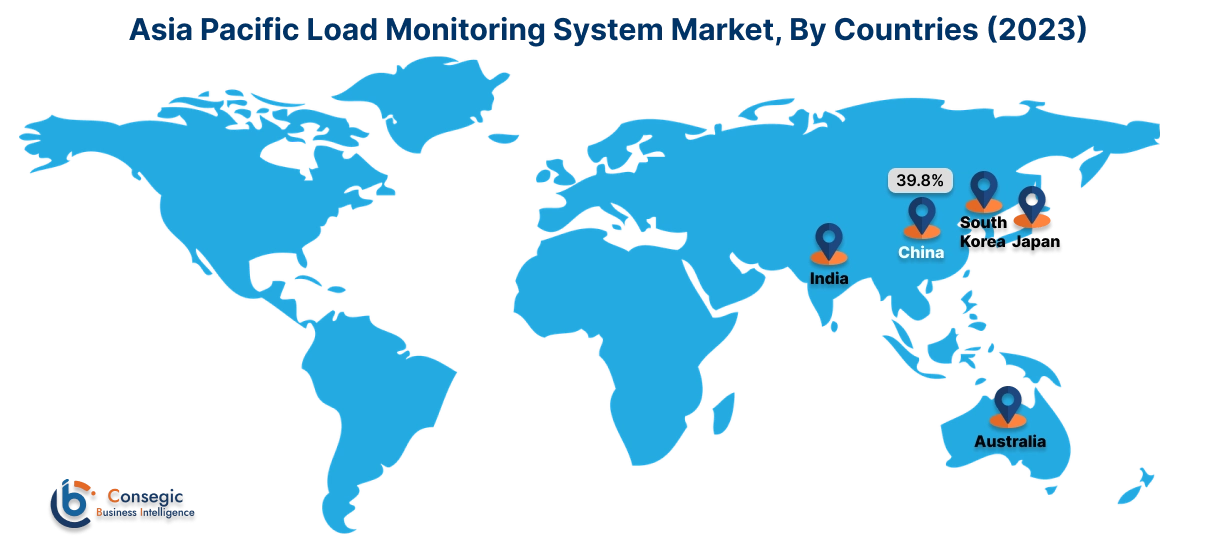

Asia Pacific region was valued at USD 1.01 Billion in 2023. Moreover, it is projected to grow by USD 1.04 Billion in 2024 and reach over USD 1.46 Billion by 2031. Out of these, China accounted for the largest share of 39.8% in 2023. The Asia-Pacific region is experiencing rapid growth in the market, driven by industrialization and infrastructural development in countries like China, India, and Japan. The expansion of manufacturing activities and the construction sector has led to increased adoption of load monitoring systems to ensure safety and compliance. As per the load monitoring system market trends, technological advancements, and government initiatives promoting industrial automation further influence market growth.

North America is estimated to reach over USD 1.60 Billion by 2031 from a value of USD 1.15 Billion in 2023 and is projected to grow by USD 1.18 Billion in 2024. This region maintains a significant position in the load monitoring system market, primarily due to its advanced industrial sector and early adoption of innovative technologies. The United States, in particular, has integrated these extensively across industries such as automotive, aerospace, and healthcare. The trend towards automation and the Industrial Internet of Things (IIoT) has further propelled the utilization of these systems for enhanced operational efficiency and safety.

Europe represents a substantial share of the global load monitoring system market, with countries like Germany, France, and the United Kingdom at the forefront. The region's strong manufacturing base, particularly in the automotive and aerospace sectors, drives the adoption of load monitoring systems. Additionally, stringent safety regulations and a focus on energy efficiency contribute to market progress. The analysis indicates a growing inclination towards digital load monitoring solutions, aligning with Europe's Industry 4.0 initiatives.

The Middle East & Africa region shows a growing interest in load monitoring systems, particularly in the construction and oil & gas industries. Countries like Saudi Arabia and the United Arab Emirates are investing in infrastructure projects, necessitating the use of load monitoring systems for safety and efficiency. The analysis suggests that the adoption of digital load monitoring solutions is gradually increasing, supported by technological advancements and a focus on operational excellence.

Latin America is an emerging market with Brazil and Mexico being key contributors. The region's industrial sector, including automotive and manufacturing, is adopting load monitoring systems to enhance productivity and safety. Government initiatives aimed at modernizing industrial operations and improving safety standards drive market development.

Top Key Players & Market Share Insights:

The Load Monitoring System market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Load Monitoring System market. Key players in the Load Monitoring System industry include -

- Flintec Inc. (USA)

- Mettler Toledo (Switzerland)

- Precia Molen (France)

- Spectris Plc (UK)

- JCM Load Monitoring Ltd (UK)

- Vishay Precision Group Inc. (USA)

- Dynamic Load Monitoring Ltd (UK)

- LCM Systems (UK)

- Keli Electric Manufacturing Co. Ltd (China)

- Straightpoint (UK)

Recent Industry Developments :

Product Enhancements:

- In May 2024, Dynamic Load Monitoring (DLM) introduced a SaaS solution to its load monitoring range, enhancing real-time data access and analytics capabilities. The software supports industries like maritime and construction by offering cloud-based monitoring for load cells and other equipment. This upgrade improves operational efficiency, safety, and equipment tracking, aligning with DLM's commitment to innovative load management solutions.

Partnerships & Collaborations:

- In March 2023, Dynamic Load Monitoring partners with its sister company, Vulcan Offshore, to offer comprehensive services in load monitoring, fabrication, welding, and CNC machining for marine and subsea industries. Their synergy supports offshore wind and renewable energy projects, meeting increased demand in Asia and the U.S.

Load Monitoring System Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 4.86 Billion |

| CAGR (2024-2031) | 4.4% |

| By Type |

|

| By Technology |

|

| By Component |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Load Monitoring System Market? +

Load Monitoring System Market size is estimated to reach over USD 4.86 Billion by 2031 from a value of USD 3.45 Billion in 2023 and is projected to grow by USD 3.54 Billion in 2024, growing at a CAGR of 4.4% from 2024 to 2031.

What specific segmentation details are covered in the Load Monitoring System Market report? +

The Load Monitoring System Market report includes segmentation details by type (Analog Load Monitoring, Digital Load Monitoring), technology (Wired Load Monitoring, Wireless Load Monitoring), component (Load Cells, Indicators & Controllers, Data Logging Software), end-user industry (Manufacturing, Aerospace & Defense, Construction, Energy & Utilities, Automotive, Others), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which is the fastest-growing segment in the Load Monitoring System Market? +

The Wireless Load Monitoring segment is expected to register the fastest CAGR during the forecast period. Wireless systems are increasingly favored for their flexibility, ease of installation, and ability to operate in remote or hard-to-access locations.

Who are the major players in the Load Monitoring System Market? +

The major players in the Load Monitoring System Market include Flintec Inc. (USA), Mettler Toledo (Switzerland), Precia Molen (France), Spectris Plc (UK), JCM Load Monitoring Ltd (UK), Vishay Precision Group Inc. (USA), Dynamic Load Monitoring Ltd (UK), LCM Systems (UK), Keli Electric Manufacturing Co. Ltd (China), and Straightpoint (UK).