- Summary

- Table Of Content

- Methodology

Lithium Battery Charger ICs Market Size:

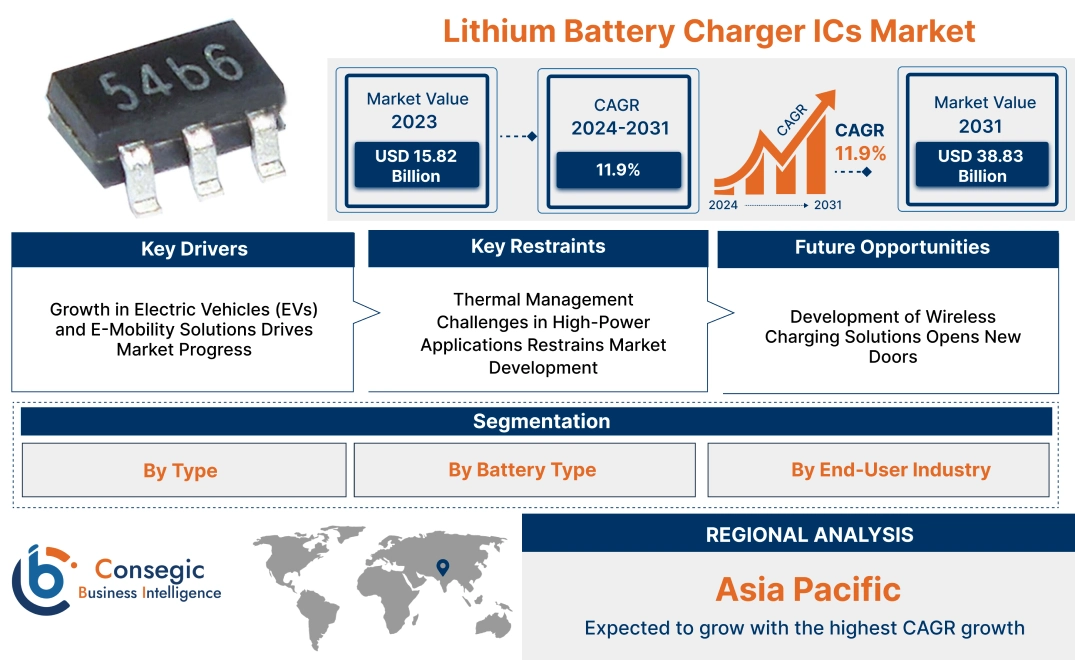

Lithium Battery Charger ICs Market size is estimated to reach over USD 38.83 Billion by 2031 from a value of USD 15.82 Billion in 2023 and is projected to grow by USD 17.42 Billion in 2024, growing at a CAGR of 11.9% from 2024 to 2031.

Lithium Battery Charger ICs Market Scope & Overview:

Lithium battery charger ICs are specialized integrated circuits designed to manage the charging process of lithium-ion and lithium-polymer batteries. These ICs ensure safe, efficient, and precise charging by regulating voltage and current levels, preventing overcharging, overheating, and other potential issues that could damage the battery or reduce its lifespan. They are widely used in portable electronic devices, electric vehicles, medical equipment, and energy storage systems, where reliable and compact charging solutions are critical. These charger ICs support various charging methods, including constant current (CC) and constant voltage (CV), to meet specific battery requirements.

Additionally, they often feature multiple protection mechanisms such as short-circuit protection, thermal shutdown, and reverse polarity protection, ensuring safe operation under diverse conditions. Modern lithium battery charger ICs are compact and integrate advanced functionalities like power path management and fast charging capabilities to enhance overall performance. End-users of these ICs include manufacturers of consumer electronics, automotive systems, and industrial equipment, who rely on efficient charging solutions to ensure optimal battery performance and longevity in their products. Lithium battery charger ICs play a vital role in supporting the growing demand for high-performance battery-powered applications.

Lithium Battery Charger ICs MarketDynamics - (DRO) :

Key Drivers:

Growth in Electric Vehicles (EVs) and E-Mobility Solutions Drives Market Progress

The global shift toward electric vehicles (EVs) and e-mobility solutions, such as e-bikes and scooters, is significantly driving demand for high-performance charging ICs. EVs rely on lithium-ion batteries that require advanced charger ICs to ensure optimal charging speed, energy efficiency, and precise thermal management. As EV adoption grows, manufacturers are increasingly integrating ICs with features like adaptive charging and power path control to enhance battery performance and longevity. These advanced ICs play a crucial role in managing complex battery systems, addressing challenges like overcharging, overheating, and power fluctuations, particularly in high-power applications.

Moreover, the rising adoption of fast-charging infrastructure for EVs further emphasizes the need for innovative IC solutions capable of supporting rapid and safe charging. With e-mobility gaining momentum worldwide, these charging ICs are becoming integral to improving battery management systems and meeting the growing demand for sustainable transportation solutions, contributing to the lithium battery charger ICs market growth.

Key Restraints :

Thermal Management Challenges in High-Power Applications Restrains Market Development

In high-power applications like electric vehicles (EVs) and industrial energy storage systems, managing heat generation is a critical issue. Charger ICs operating at elevated power densities produce significant heat, which compromises their efficiency, reliability, and operational lifespan. Excessive heat impacts the performance of lithium-ion batteries by accelerating degradation and increasing the risk of thermal runaway, making effective thermal management essential.

Developing robust thermal management systems for high-power ICs involves additional complexity, such as incorporating advanced heat dissipation mechanisms, thermal sensors, and specialized cooling systems. These requirements not only increase the design and manufacturing costs but also limit adoption in cost-sensitive industries. The constraint is particularly pronounced in applications demanding compact and high-efficiency solutions, such as EV fast chargers, where maintaining thermal stability while delivering high performance is a critical but resource-intensive task, posing a restraint to lithium battery charger ICs market demand.

Future Opportunities :

Development of Wireless Charging Solutions Opens New Doors

The advancement of wireless charging technologies is creating significant growth opportunities for charger ICs tailored to support contactless charging. Applications such as wireless charging pads, smartphones, wearables, and even electric vehicles (EVs) are driving demand for ICs capable of efficiently managing inductive and resonant charging methods. These ICs play a critical role in ensuring seamless power transfer, optimized energy efficiency, and effective thermal management during the charging process.

Wireless charging eliminates the need for physical connectors, enhancing convenience and durability, particularly for consumer electronics and automotive applications. For EVs, advanced charger ICs enable efficient integration into wireless charging stations, ensuring high-power delivery with minimal energy loss. As per market analysis, the growing adoption of smart devices and IoT-enabled systems and the need for wireless charging solutions is expected to rise, positioning charger ICs with features like power modulation and heat dissipation as essential components in this expanding ecosystem, creating significant lithium battery charger ICs market opportunities.

Lithium Battery Charger ICs Market Segmental Analysis :

By Type:

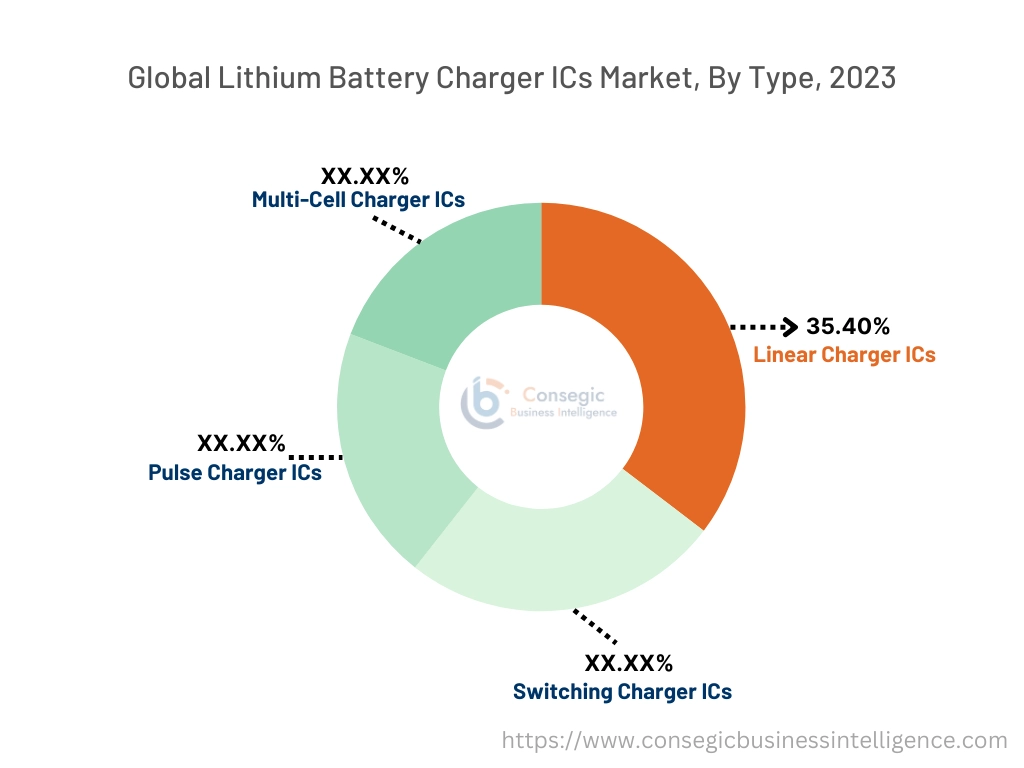

Based on type, the market is segmented into Linear Charger ICs, Switching Charger ICs, Pulse Charger ICs, and Multi-Cell Charger ICs.

The Linear Charger ICs segment held the largest revenue of 35.40% of the total lithium battery charger ICs market share in 2023.

- Linear charger ICs are widely used in compact and low-power devices due to their simplicity, cost-effectiveness, and low electromagnetic interference (EMI).

- These ICs are ideal for applications in consumer electronics, including smartphones, tablets, and wearables, where space and cost constraints are critical.

- Linear charger ICs offer thermal efficiency and reliability in single-cell lithium-ion batteries, making them a preferred choice for portable devices.

- Trends indicate the increasing integration of linear charger ICs in IoT-enabled devices and energy-efficient applications across industries, fueling lithium battery charger ICs market expansion.

The Switching Charger ICs segment is expected to register the fastest CAGR during the forecast period.

- Switching charger ICs are favored for their high efficiency in charging multi-cell batteries, especially in applications requiring fast charging and high current output.

- These ICs are commonly adopted in automotive and industrial equipment, where power efficiency and performance are critical.

- The segment's rapid growth is supported by advancements in power management technologies, reducing heat generation and improving energy conversion.

- Market analysis highlights the role of switching charger ICs in addressing energy needs in high-performance applications, contributing to lithium battery charger ICs market growth.

By Battery Type:

Based on battery type, the market is segmented into Lithium-Ion (Li-Ion), Lithium Iron Phosphate (LiFePO4), and Lithium Polymer (LiPo).

The Lithium-Ion (Li-Ion) segment held the largest revenue of the total lithium battery charger ICs market share in 2023.

- Lithium-ion batteries are the most widely used rechargeable batteries, supporting applications in consumer electronics, automotive, and industrial sectors.

- These batteries offer high energy density, longer lifespan, and low self-discharge rates, making them ideal for powering portable devices and electric vehicles.

- Charger ICs for Li-ion batteries are designed to ensure optimal charging performance and safety, with features like overcharge protection and temperature monitoring.

- Trends in renewable energy storage and EV adoption are driving the need for lithium-ion charger ICs in both residential and industrial settings, driving lithium battery charger ICs market demand.

The Lithium Polymer (LiPo) segment is expected to register the fastest CAGR during the forecast period.

- LiPo batteries are increasingly used in compact and lightweight devices, such as drones, wearables, and medical devices, due to their flexible form factor.

- Charger ICs for LiPo batteries are engineered to handle their specific charging requirements, ensuring safety and efficiency.

- The segment's rapid growth is driven by the rising adoption of LiPo batteries in innovative applications, including robotics and portable healthcare devices.

- Market analysis emphasizes the increasing integration of LiPo charger ICs in applications demanding high energy efficiency and space optimization, which further boosts the lithium battery charger ICs market expansion.

By End-User Industry:

Based on end-user industry, the market is segmented into IT & Telecom, Healthcare, Automotive, Aerospace & Defense, Consumer Electronics, and Others.

The Consumer Electronics segment accounted for the largest revenue share in 2023.

- Consumer electronics, including smartphones, laptops, and wearables, are the primary users of lithium battery charger ICs due to their high dependence on rechargeable batteries.

- These ICs ensure faster charging times and improved energy management, enhancing user convenience and device performance.

- Trends in smart home devices and IoT-enabled gadgets are fueling the adoption of advanced charger ICs in the consumer electronics sector.

- As per lithium battery charger ICs market analysis, the dominance of this segment reflects the increasing reliance on lithium-based batteries for everyday electronics.

The Automotive segment is expected to register the fastest CAGR during the forecast period.

- The automotive sector uses lithium battery charger ICs for electric vehicles (EVs) and hybrid electric vehicles (HEVs), focusing on high-efficiency and fast-charging capabilities.

- Charger ICs play a vital role in enhancing battery performance, supporting features like regenerative braking and energy recovery.

- The rapid growth of this segment is supported by advancements in EV technology and global initiatives promoting sustainable transportation.

- The lithium battery charger ICs market trends highlights the critical role of charger ICs in addressing the unique charging requirements of automotive applications, such as multi-cell battery packs.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

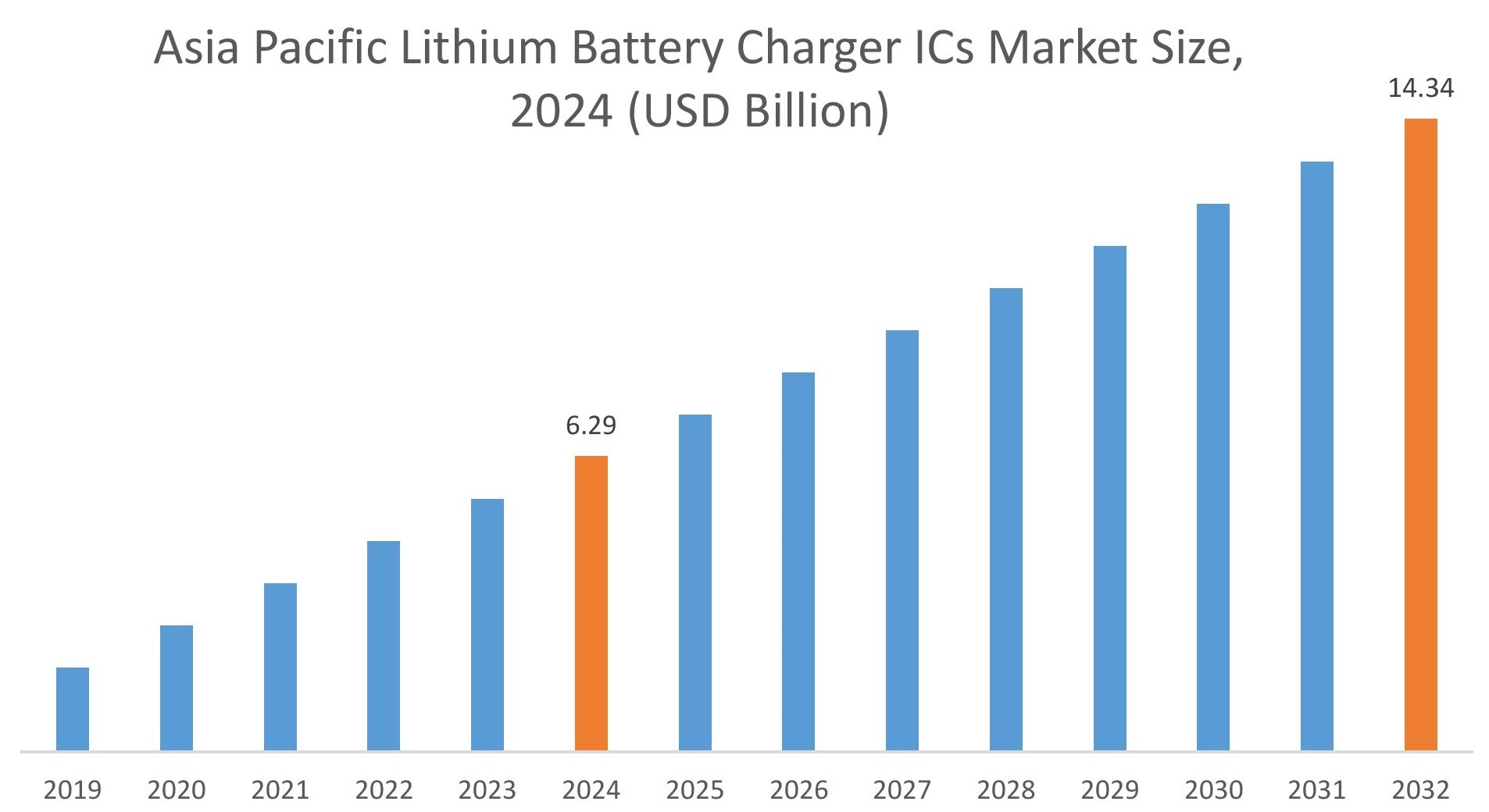

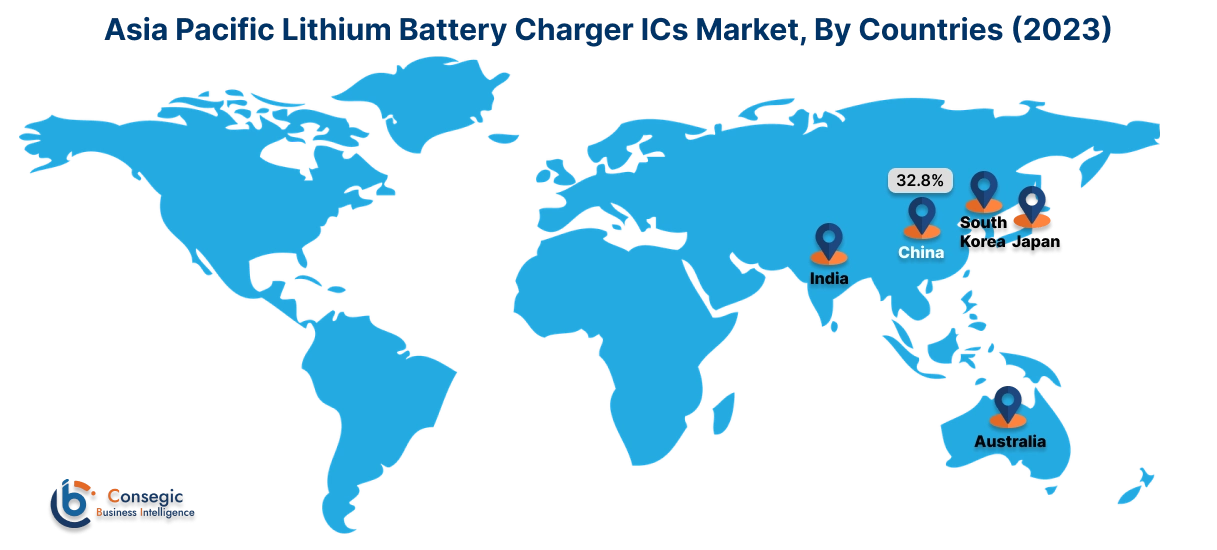

Asia Pacific region was valued at USD 4.65 Billion in 2023. Moreover, it is projected to grow by USD 5.13 Billion in 2024 and reach over USD 11.65 Billion by 2031. Out of which, China accounted for the largest share of 32.8% in 2023. The Asia-Pacific region is experiencing rapid growth in the lithium battery charger ICs market, driven by industrialization and a burgeoning consumer electronics market in countries like China, India, and Japan. The proliferation of smartphones, wearable devices, and the increasing adoption of EVs have intensified the need for efficient charging solutions. Technological advancements and government initiatives promoting electric mobility further influence lithium battery charger ICs market opportunities.

Asia Pacific region was valued at USD 4.65 Billion in 2023. Moreover, it is projected to grow by USD 5.13 Billion in 2024 and reach over USD 11.65 Billion by 2031. Out of which, China accounted for the largest share of 32.8% in 2023. The Asia-Pacific region is experiencing rapid growth in the lithium battery charger ICs market, driven by industrialization and a burgeoning consumer electronics market in countries like China, India, and Japan. The proliferation of smartphones, wearable devices, and the increasing adoption of EVs have intensified the need for efficient charging solutions. Technological advancements and government initiatives promoting electric mobility further influence lithium battery charger ICs market opportunities.

North America is estimated to reach over USD 12.77 Billion by 2031 from a value of USD 5.26 Billion in 2023 and is projected to grow by USD 5.78 Billion in 2024. This region holds a significant position in the lithium battery charger ICs market, primarily due to the widespread adoption of portable electronic devices and electric vehicles (EVs). The United States, in particular, has seen a surge in the use of smartphones, laptops, and EVs, necessitating efficient charging solutions. The trend towards renewable energy storage systems further amplifies the need for advanced charger ICs.

Europe represents a substantial share of the global lithium battery charger ICs market, with countries like Germany, France, and the United Kingdom leading in technological advancements. The region's strong emphasis on sustainability and clean energy has propelled the adoption of lithium-ion batteries across various applications, including automotive and industrial sectors. The lithium battery charger ICs market analysis indicates a growing trend towards integrating fast-charging technologies and wireless charging capabilities, aligning with the region's focus on innovation.

The Middle East & Africa region shows a growing interest in lithium battery charger ICs, particularly in the renewable energy and telecommunications sectors. Countries like the United Arab Emirates and South Africa are investing in solar energy projects and expanding mobile networks, necessitating efficient energy storage and charging solutions. The analysis suggests an increasing trend towards adopting advanced charger ICs to enhance energy efficiency and support sustainable initiatives.

Latin America is an emerging market for lithium battery charger ICs, with Brazil and Mexico being key contributors. The region's growing consumer electronics market and initiatives to promote renewable energy have spurred the adoption of lithium-ion batteries and associated charging solutions. As per lithium battery charger ICs market trends, government policies aimed at modernizing infrastructure and enhancing energy efficiency influence market trends.

Top Key Players & Market Share Insights:

The Lithium Battery Charger ICs market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Lithium Battery Charger ICs market. Key players in the Lithium Battery Charger ICs industry include –

- Silergy Corporation (China)

- Holtek Semiconductor Inc. (Taiwan)

- ON Semiconductor Corporation (USA)

- New Japan Radio Co. (Japan)

- Texas Instruments Inc. (USA)

- Analog Devices Inc. (USA)

- Richtek Technology Corporation (Taiwan)

- NXP Semiconductors N.V. (Netherlands)

- Toshiba Corporation (Japan)

- Maxim Integrated (USA)

Recent Industry Developments :

Product Launches:

- In June 2024, HiDi Micro introduces the HL7137, a dual-phase 7.5A, 34W charge pump IC optimized for Li-ion and Li-polymer batteries in smartphones, tablets, and IoT devices. With 97.11% efficiency at 4.5V/5A output and 2:1 CP mode for current reduction, it integrates safety features like OVP, OTP, and SCP, alongside CC/CV regulation. Advanced functionality includes a 12-bit ADC for monitoring and a thermal regulation loop for enhanced safety. This highlights HiDi Micro’s focus on efficient, secure charging solutions.

- In May 2024, Nisshinbo Micro Devices Inc. announced the release of the NB7120 series, a high-accuracy 1-cell Li-ion battery protection IC with temperature protection for high-side FETs. This development aims to enhance safety in wearable and hearable devices, which are increasingly prevalent due to the growth of virtual reality (VR) and augmented reality (AR) applications. The NB7120 series offers industry-leading accuracy and incorporates temperature protection features to prevent battery-related issues such as ignition, thereby improving the safety of devices worn directly by users.

- In January 2024, Xidiwei introduced the HL7009A, a 3.6A switch-mode lithium battery charging IC tailored for smartphones, tablets, and IoT devices. It supports USB and AC-DC inputs with a 4.0V–9.5V range, enabling charging even without a battery. Featuring BC1.2 detection, it optimizes input current utilization, while its I²C compatibility allows precise control over charging stages and OTG functionality. With up to 92% efficiency, configurable OTG outputs, and high integration for miniaturized designs, the HL7009A offers a flexible and cost-effective charging solution.

- In November 2023, NXP Semiconductors launched the MC33774, an advanced battery cell controller IC for enhanced battery management systems (BMS). Offering 0.8 mV cell measurement accuracy and robust cell balancing across temperatures, it optimizes capacity and safety for high-voltage Li-ion batteries. Designed for safety-critical applications, the 18-channel analog front-end device supports ASIL D standards, making it ideal for e-mobility and energy storage systems.

Lithium Battery Charger ICs Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 38.83 Billion |

| CAGR (2024-2031) | 11.9% |

| By Type |

|

| By Battery Type |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Lithium Battery Charger ICs Market? +

Lithium Battery Charger ICs Market size is estimated to reach over USD 38.83 Billion by 2031 from a value of USD 15.82 Billion in 2023 and is projected to grow by USD 17.42 Billion in 2024, growing at a CAGR of 11.9% from 2024 to 2031.

What specific segmentation details are covered in the Lithium Battery Charger ICs Market report? +

The Lithium Battery Charger ICs Market report includes segmentation details by type (Linear Charger ICs, Switching Charger ICs, Pulse Charger ICs, Multi-Cell Charger ICs), battery type (Lithium-Ion (Li-Ion), Lithium Iron Phosphate (LiFePO4), Lithium Polymer (LiPo)), end-user industry (IT & Telecom, Healthcare, Automotive, Aerospace & Defense, Consumer Electronics, Others), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which is the fastest-growing segment in the Lithium Battery Charger ICs Market? +

The Lithium Polymer (LiPo) segment is expected to register the fastest CAGR during the forecast period. LiPo batteries are increasingly used in compact and lightweight devices like drones, wearables, and medical devices due to their flexible form factor.

Who are the major players in the Lithium Battery Charger ICs Market? +

The major players in the Lithium Battery Charger ICs Market include Silergy Corporation (China), Holtek Semiconductor Inc. (Taiwan), ON Semiconductor Corporation (USA), New Japan Radio Co. (Japan), Texas Instruments Inc. (USA), Analog Devices Inc. (USA), Richtek Technology Corporation (Taiwan), NXP Semiconductors N.V. (Netherlands), Toshiba Corporation (Japan), and Maxim Integrated (USA).