- Summary

- Table Of Content

- Methodology

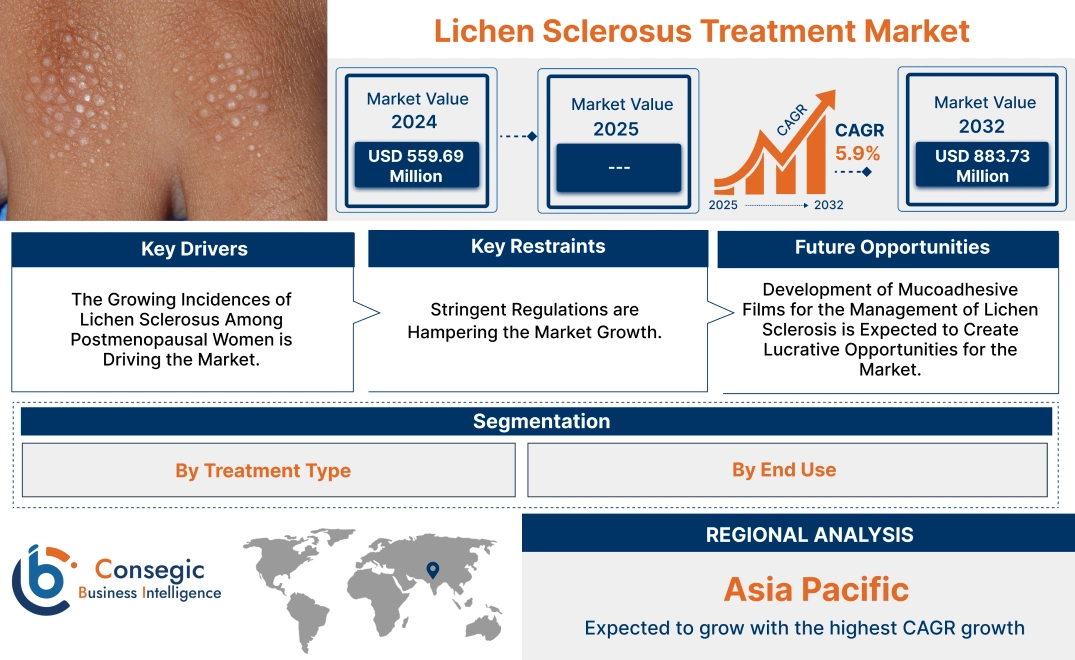

Lichen Sclerosus Treatment Market Size:

Lichen Sclerosus Treatment Market size is growing with a CAGR of 5.9% during the forecast period (2025-2032), and the market is projected to be valued at USD 883.73 Million by 2032 from USD 559.69 Million in 2024.

Lichen Sclerosus Treatment Market Scope & Overview:

Lichen sclerosus (LS) is a chronic skin condition characterized by inflammation that leads to thin, white, and wrinkled skin. This condition primarily affects the genital and anal areas. Extragenital LS comprises areas such as the neck, shoulders, upper trunk, thighs, and oral cavity. Certain individuals have a higher risk of developing this condition. These include postmenopausal women, children, women with autoimmune conditions, men with urinary incontinence, and individuals with a family history of LS. The LS is managed using several treatment options including medications, phototherapy, and surgery. Medications primarily include topical and oral corticosteroids and immunosuppressants. The growing prevalence of LS among postmenopausal women, the adoption of combination therapy, and the development of novel treatment solutions are the factors supporting the market trajectory.

Lichen Sclerosus Treatment Market Dynamics - (DRO) :

Key Drivers:

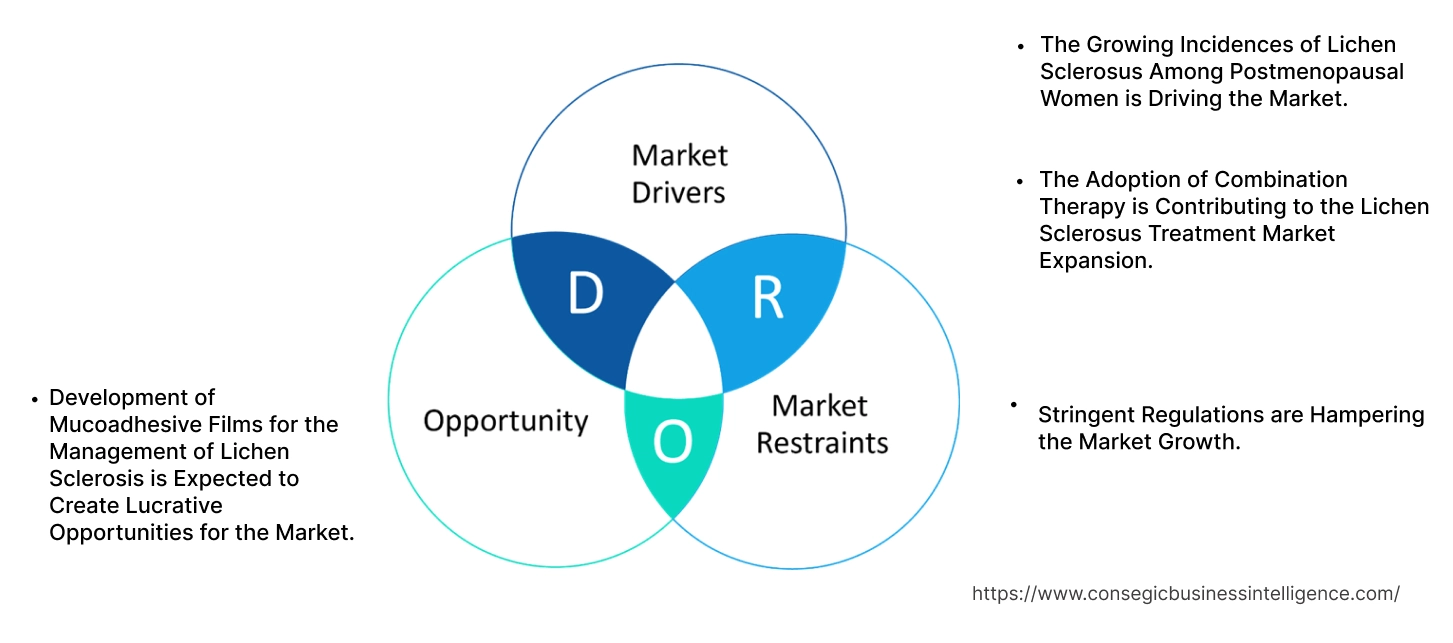

The Growing Incidences of Lichen Sclerosus Among Postmenopausal Women is Driving the Market.

The growing incidences of lichen sclerosus among postmenopausal women is a significant driver of growth within the Lichen Sclerosus treatment as the hormonal shift associated with menopause is considered a key factor in the development of lichen sclerosus. A significant decline in estrogen levels during this life stage, results in changes in the vulvar skin making it more susceptible to the condition. Hence, postmenopausal women are at a higher risk of developing lichen sclerosus.

- For instance, according to the data published in the Journal of Obstetrics and Gynecology International, it is stated that according to the 3 trial year period in a general gynecology practice the incidence of lichen scelrosus is found in 54% of postmenopausal women with a mean age of 52.6 years.

The growing recognition of this key demographic group with a higher incidence of LS has several implications for the lichen scelrosus treatment, including increased demand for effective and safe treatment options, a need to focus on developing and tailoring treatment approaches to the specific needs of postmenopausal women. In conclusion, the increasing diagnosis of LS among postmenopausal women is a crucial factor driving the lichen sclerosus treatment market growth, necessitating a focus on developing and delivering effective and safe lichen scelrosus treatment options that address the specific needs of these patient populations.

The Adoption of Combination Therapy is Contributing to the Lichen Sclerosus Treatment Market Expansion.

LS is a chronic inflammatory skin condition that requires ongoing management. While topical corticosteroids have been the mainstay of treatment, their long-term use presents significant side effects, such as skin thinning and atrophy. This has led to a growing interest in combination therapies that leverage the strengths of different treatment modalities while mitigating their individual limitations.

One common approach involves combining topical corticosteroids with calcineurin inhibitors like tacrolimus or pimecrolimus. This combination therapy enhances efficacy by combining medications with varying mechanisms of action, leading to improved symptom control and faster disease resolution. Additionally, it reduces side effects by allowing for the use of lower doses of each individual medication. Beyond combining topical medications, approaches that combine topical therapies with other modalities, such as phototherapy and laser therapy, are being explored in clinical settings. These combination approaches aim to optimize treatment outcomes, improve patient satisfaction, and ultimately enhance the overall management of LS.

- For instance, according to the research study published by Journal Elsevier, it is stated that the combination strategy of laser therapy and a topical photosensitizer ALA-PDT is effective and well tolerated for hyperkeratotic vulvar lichen sclerosus (VLS) which further improves the efficacy with no recurrence during the follow-up of 1

Overall, as per analysis, the growing adoption of combination therapies for lichen scelrosus is not only improving patient outcomes but also driving lichen sclerosus treatment market expansion by increasing the demand for a wider range of treatment options and fostering the development of new therapeutic approaches for LS.

Key Restraints:

Stringent Regulations are Hampering the Market Growth.

The development of treatment solutions for lichen sclerosus is subject to stringent regulations aimed at ensuring patient safety. The regulations present significant constraints for pharmaceutical companies. One major factor is the lengthy and complex drug development process. Clinical trials are rigorous and time-consuming, requiring substantial investment and resources. This, coupled with stringent regulatory hurdles, delays the approval process, hindering the timely introduction of new medications.

Furthermore, post-market survey and safety monitoring requirements add to the regulatory burden. Companies must continuously monitor the safety and efficacy of their products, which becomes costly and resource-intensive, especially for smaller players. Compliance with these regulations is particularly difficult for smaller companies and startups. The rigorous regulatory environment also hinders innovation within the industry, as companies are hesitant to invest in risky or unconventional approaches due to the high cost of failure. Overall, the regulations delay product approvals, increase costs, and limit profitability, especially for smaller companies further hampering the market trajectory.

Future Opportunities :

Development of Mucoadhesive Films for the Management of Lichen Sclerosis is Expected to Create Lucrative Opportunities for the Market.

A mucoadhesive film is a drug delivery system that sticks to the oral mucosa and releases medication into the body. These films are multi-layered systems that adhere mucosa underlying the skin. These multi-layered systems release medication in a controlled manner, either for local action or for systemic absorption through the mucosal membranes.

Mucoadhesive films offer a novel approach to lichen sclerosus treatment. By adhering specifically to the affected mucosal surfaces, these films enable targeted drug delivery, potentially minimizing systemic side effects associated with oral or topical medications. Moreover, mucoadhesive films enhance patient compliance by offering a more discreet and convenient alternative to traditional topical treatments. Furthermore, these films are formulated to release medication in a controlled and sustained manner, providing prolonged therapeutic effects and potentially reducing the frequency of application.

- For instance, in January 2024, Hyloris Pharmaceuticals SA and AFT Pharmaceuticals announced partnership announced a partnership to develop HY-091, a novel mucoadhesive film for the treatment of vulvar lichen sclerosus. HY-091 is designed to deliver a known molecular entity with extended duration release, offering a convenient application method that enhances patient compliance. This film aims to reduce inflammation and scarring in the affected area while promoting skin structure restoration.

Overall, the development of mucoadhesive films for lichen sclerosus treatment holds a significant lichen sclerosus treatment market opportunity to improve patient outcomes and boost market trajectory.

Lichen Sclerosus Treatment Market Segmental Analysis :

By Treatment Type:

Based on treatment type, the market is categorized into medications, phototherapy, and surgery.

Trends in the Treatment Type:

- The adoption of combination therapy such as combining phototherapy with other treatments, such as topical medication serves as a market trend potentially enhancing treatment outcomes and reducing the risk of side effects.

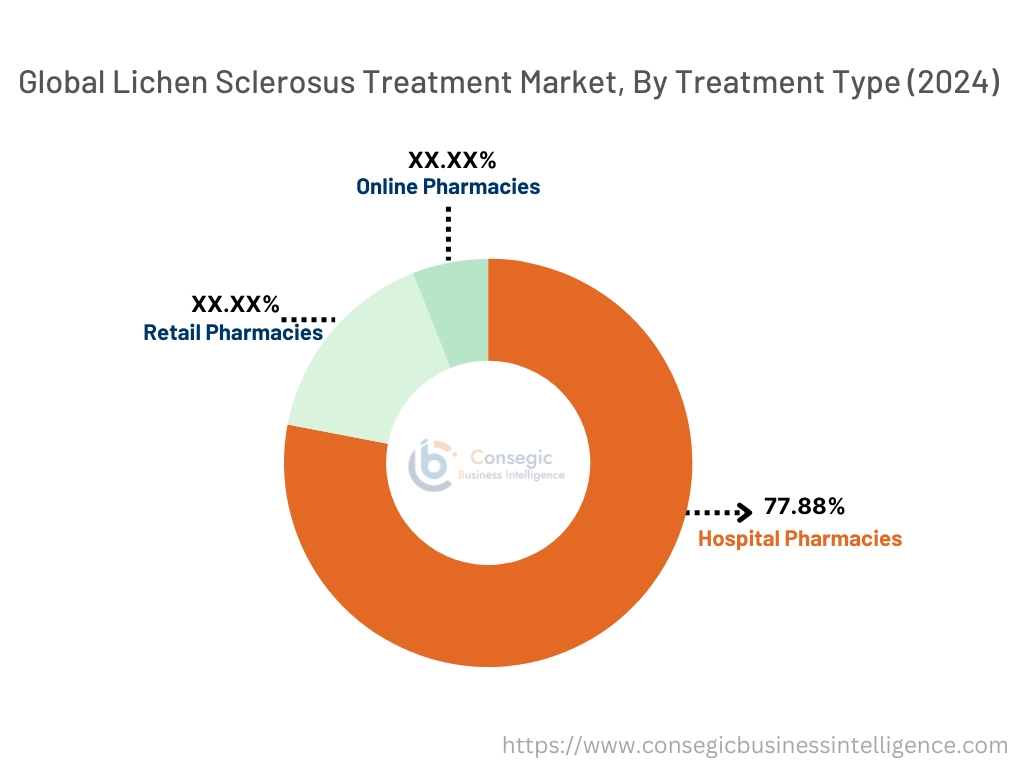

The medications segment accounted for the largest market share of 77.88% in 2024.

- The segment is further categorized into corticosteroids, immunosuppressants, retinoids, and others.

- Medications play a pivotal role in managing lichen sclerosus. Ultrapotent or potent topical corticosteroids, such as clobetasol propionate and triamcinolone acetonide, serve as initial treatment choices, effectively reducing inflammation.

- Immunosuppressants, particularly calcineurin inhibitors such as tacrolimus and pimecrolimus, provide an alternative for long-term management, especially when corticosteroids are not well-tolerated.

- Additionally, retinoids improve skin texture and reduce scarring when used in conjunction with other treatments. Moreover, antihistamines help alleviate itching, and emollients provide soothing hydration to the affected skin.

- The medications segment dominates the lichen sclerosus treatment market share, driven by the availability of various therapeutic options and their crucial role in managing the condition. Lichen Sclerosus is a chronic condition requiring long-term management, creating a sustained need for medications. Further, a growing focus on the development of highly effective medications is supporting the segment trajectory.

- For instance, in November 2023, MC2 Therapeutics announced the enrollment of the first patients in a Phase 2 PoC (proof of concept) trial evaluating the safety and efficacy of an innovative new drug candidate for the treatment of vulvar lichen sclerosus (VLS). MC2-25 VLS is a first-in-class drug candidate for urea-associated skin diseases using a di-peptide as an iso-cyanate scavenger to inhibit carbamylation of amino acids and proteins in the skin and has the potential to become the first approved treatment for VLS.

- Overall, medications dominate the lichen sclerosus treatment market analysis, due to their crucial role in managing the condition. The development of innovative therapies is further contributing to the market trajectory of lichen sclerosus treatment.

The phototherapy segment is expected to grow at the fastest CAGR over the forecast period.

- Phototherapy is a form of treatment that uses ultraviolet light to treat skin conditions.

- Phototherapy, including UVA1 and narrowband UVB, has demonstrated potential in treating Lichen Sclerosus (LS). However, it is generally considered a second-line treatment option, reserved for cases where standard therapies are ineffective.

- Several factors are propelling the trajectory of the phototherapy segment in LS treatment. As awareness of LS increases among both patients and healthcare providers, more cases are being diagnosed, expanding the number of potential patients for phototherapy.

- Furthermore, the limitations of traditional therapies, such as the potential side effects of long-term corticosteroid use and treatment resistance in some patients, are prompting the exploration of alternative options such as phototherapy.

- The emergence of novel phototherapy techniques, including refinements in narrowband UVB technology and ongoing research to enhance the efficacy and safety of photodynamic therapy is also contributing to the segment's growth.

By End-User:

Based on end use, the market is categorized into hospitals, clinics, and others.

Trends in the End Use:

- The adoption of telehealth platforms facilitates remote patient monitoring, medication adherence, and access to specialist consultations, improving the convenience and accessibility of home-based LS management.

The hospitals segment accounted for the largest market share in the year 2024.

- The hospitals segment within the lichen sclerosus treatment market demand is poised for a significant trajectory as they serve a crucial role in the provision of effective treatment for the management of lichen sclerosus particularly for complex or severe cases.

- These medical facilities offer a comprehensive range of diagnostic and treatment services, including access to sophisticated diagnostic tools, a multidisciplinary approach involving collaboration between specialists, and advanced treatment options such as phototherapy and surgical interventions.

- Hospitals are well-equipped to manage complex cases of LS, including those with severe symptoms, comorbidities, and complications.

- Furthermore, hospitals often serve as centers for research and clinical trials, contributing to the advancement of LS treatment. The growing emphasis on multidisciplinary care models, where specialists from different disciplines collaborate to provide comprehensive patient care, is fuelling the trend of the hospital segment in the market for lichen sclerosus treatment.

The clinics segment is expected to grow at the fastest CAGR over the forecast period.

- Clinics including dermatology and gynecology play a pivotal role in the LS treatment market, serving as the primary point of care for patients. These clinics possess specialized expertise in diagnosing and managing skin conditions, including LS. Dermatologists are well-versed in clinical presentation, diagnostic procedures, and treatment options for LS.

- These clinics offer a comprehensive range of services, including detailed medical history and physical examination, skin biopsies for histopathological confirmation, prescription of topical medications, management of phototherapy treatments, and patient education and counseling on disease management and lifestyle modifications.

- Furthermore, dermatology and gynecology clinics provide long-term follow-up, regularly monitoring disease progression, assessing treatment efficacy, and adjusting treatment plans as needed.

- These clinics often prioritize patient-centered care, focusing on individual patient needs and preferences. The integration of advanced technologies, such as telemedicine and digital imaging, enhances patient care and improves communication between patients and dermatologists. Growing demand for clinics for the provision of effective care of skin conditions supports the segment trajectory.

- For instance, according to the report published by NHS England in January 2024, it is stated that one in four people in England and Wales see their general physician about dermal conditions every year, with more than 3.5 million outpatient and day surgery attendances in dermatology. This highlights the importance of effective dermatological care, including the management of conditions like lichen sclerosus.

- Overall, as per analysis, dermatology and gynecology clinics are pivotal in the LS treatment market, offering comprehensive care and driving positive patient outcomes.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

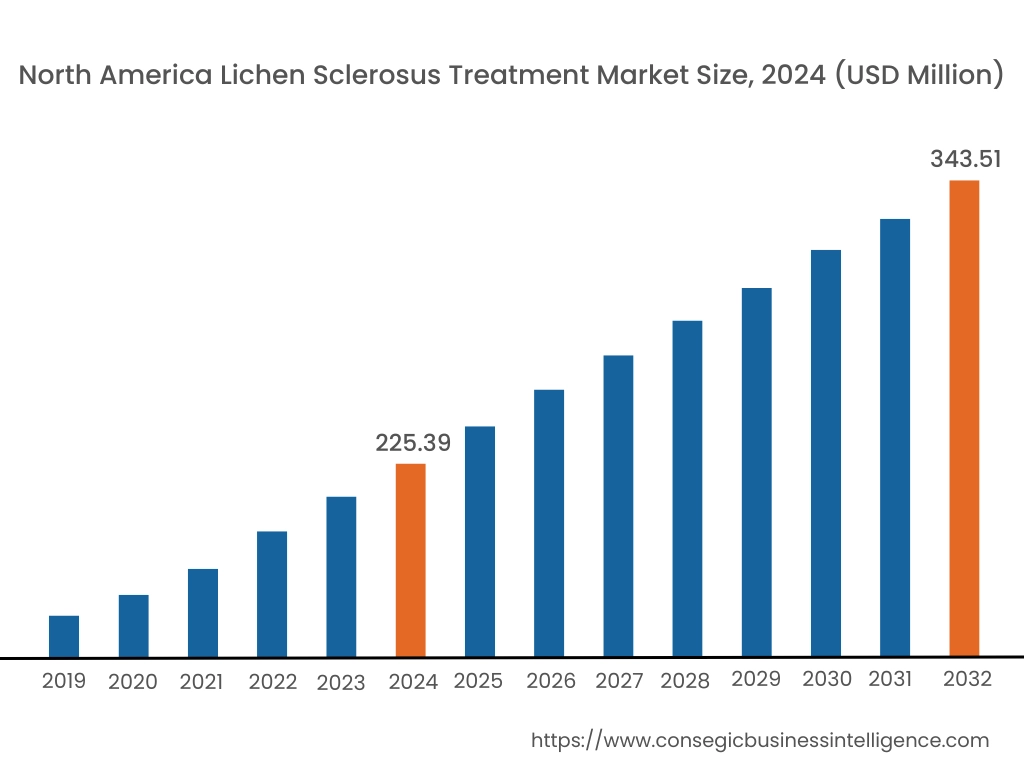

In 2024, North America accounted for the highest market share at 40.27% and was valued at USD 225.39 Million and is expected to reach USD 343.51 Million in 2032. In North America, the U.S. accounted for the highest market share of 71.43% during the base year of 2024.

North America dominates the global lichen sclerosus treatment market demand, owing to the confluence of multiple factors such as the advanced healthcare infrastructure, and well-established pharmaceutical industry. High healthcare expenditure in the United States and Canada further provides robust funding for research, development, and access to advanced treatment options. The region boasts a well-developed healthcare infrastructure with the presence of specialized dermatologists, advanced diagnostic facilities, and access to cutting-edge technologies. Moreover, the region's favorable reimbursement policies and government initiatives such as Medicare and Medicaid provide financial support for lichen sclerosus treatment, especially for vulnerable populations.

- For instance, based on the analysis published by the S. Centers for Medicare & Medicaid Services in December 2024, Medicare spending grew 8.1% to USD 1,029.8 billion in 2023 or 21% of total national healthcare (NHE) spending in the U.S. Medicaid spending grew 7.9% to USD 871.7 billion in 2023 or 18% of total NHE. Medicare provides health coverage for senior citizens, while Medicaid covers health care costs for people with low incomes. This further improves access to the treatment of several skin conditions including lichen sclerosus.

Furthermore, a strong pharmaceutical sector in North America drives research and development of new therapies, contributing to the availability of advanced treatment options for LS. The combination of the aforementioned factors and trends is driving a substantial trajectory in the North American lichen sclerosus treatment market trend.

Asia Pacific is experiencing the fastest growth with a CAGR of 6.6% over the forecast period. Several factors drive this growth, including a large and rapidly growing population, rising disposable incomes, increased government spending on healthcare, and improvements in healthcare infrastructure. Increasing awareness among healthcare providers and the general public regarding LS is leading to earlier diagnosis and improved patient management. Moreover, the rising prevalence of chronic diseases, including LS, due to lifestyle changes and aging populations is driving the need for effective treatment options. Key market drivers include continued economic growth, the adoption of advanced technologies such as telemedicine and digital health solutions, and a growing focus on preventive healthcare and early disease detection.

Europe presents a significant contribution to the lichen sclerosus treatment market analysis. Europe boasts a robust healthcare system with advanced infrastructure, including well-equipped hospitals and clinics, ensuring timely diagnosis and treatment of lichen sclerosus. Additionally, many European countries have strong public healthcare systems that provide access to quality healthcare services, including those for lichen sclerosus further propelling the market. Moreover, Europe presents a strong pharmaceutical sector with a robust research and development pipeline, leading to advancements in treatment solutions. Overall, as per analysis, the combination of accessible primary care, strong public healthcare systems, and advanced diagnostic facilities contributes to the effective management of this condition in Europe, ultimately driving the market trend.

The Middle East and Africa (MEA) region is witnessing notable lichen sclerosus treatment market trends. The growing healthcare sector in the Middle East is playing a pivotal role in demand. Many countries in the MEA region are investing in developing their healthcare infrastructure with advanced diagnostic and treatment facilities. This includes building hospitals, and clinics, and improving access to diagnostic tools which are essential for detecting this condition. The combined impact of these factors is creating a favorable environment for the trajectory of the lichen sclerosus treatment market opportunities in the MEA region.

Latin America is an emerging region in the lichen sclerosus treatment market share, with significant potential for innovation. Growing economies and rising disposable incomes are leading to increased healthcare spending across the region, translating into improved access to healthcare services, including those for skin conditions like LS. Ongoing investments in healthcare infrastructure, such as the development of new hospitals, clinics, and diagnostic centers, are enhancing access to quality healthcare services. While still in its early stages, there is a growing demand for LS treatment in the general public, leading to increased diagnosis and improved patient management. Furthermore, pharmaceutical companies are increasingly focusing on emerging markets like Latin America, leading to increased availability of treatment options.

Top Key Players and Market Share Insights:

The Lichen Sclerosus Treatment market is highly competitive with major players providing precise products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global Lichen Sclerosus Treatment market. Key players in the Lichen Sclerosus Treatment industry include-

- Sandoz Inc. (U.S.)

- Glenmark Pharmaceuticals Inc. (U.S.)

- Astellas Pharma Inc. (Japan)

- MC2 Therapeutics (Denmark)

- Teva Pharmaceuticals (Israel)

- Lupin Pharmaceuticals, Inc (India)

- AdvaCare Pharma (U.S.)

- Pfizer (U.S.)

- GlaxoSmithKline (UK)

- Novartis (Switzerland)

Recent Industry Developments :

Partnership:

- In January 2024, Hyloris Pharmaceuticals SA and AFT Pharmaceuticals announced partnership announced a partnership to develop HY-091, a novel mucoadhesive film for the treatment of vulvar lichen sclerosus. HY-091 is designed to deliver a known molecular entity with extended duration release, offering a convenient application method that enhances patient compliance. This film aims to reduce inflammation and scarring in the affected area while promoting skin structure restoration.

Lichen Sclerosus Treatment Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 883.73 Million |

| CAGR (2025-2032) | 5.9% |

| By Treatment Type |

|

| By End Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Lichen Sclerosus Treatment market? +

In 2024, the Lichen Sclerosus Treatment market is USD 559.69 Million.

Which is the fastest-growing region in the Lichen Sclerosus Treatment market? +

Asia Pacific is the fastest-growing region in the Lichen Sclerosus Treatment market.

What specific segmentation details are covered in the Lichen Sclerosus Treatment market? +

Treatment Type and End Use segmentation details are covered in the Lichen Sclerosus Treatment market.

Who are the major players in the Lichen Sclerosus Treatment market? +

Sandoz Inc. (U.S.), Glenmark Pharmaceuticals Inc. (U.S.), and GlaxoSmithKline (UK) are some of the major players in the market.