- Summary

- Table Of Content

- Methodology

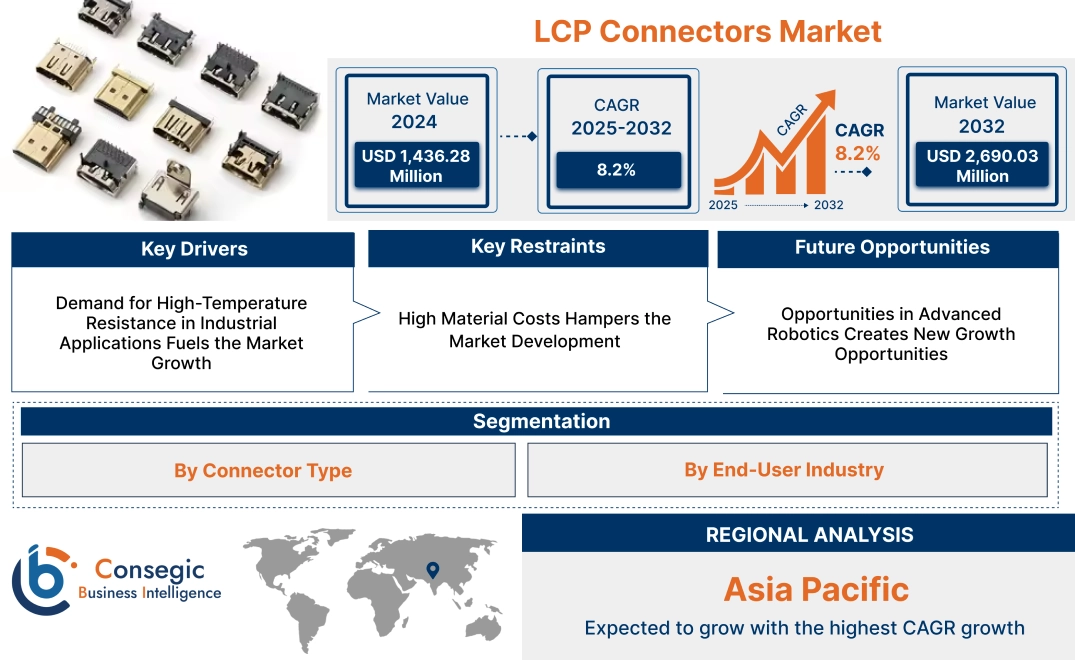

LCP Connectors Market Size:

LCP Connectors Market size is estimated to reach over USD 2,690.03 Million by 2032 from a value of USD 1,436.28 Million in 2024 and is projected to grow by USD 1,527.89 Million in 2025, growing at a CAGR of 8.2% from 2025 to 2032.

LCP Connectors Market Scope & Overview:

LCP connectors are electronic components made using liquid crystal polymer (LCP), a high-performance material known for its excellent mechanical, thermal, and electrical properties. These connectors are designed to provide reliable and efficient connections in electronic systems, particularly in high-frequency and high-temperature applications. They are widely used in industries such as telecommunications, automotive, consumer electronics, and aerospace.

These connectors are available in various configurations, including board-to-board, wire-to-board, and coaxial designs, to meet diverse application requirements. Their unique properties, such as low dielectric constant, high heat resistance, and lightweight construction, make them suitable for compact and high-performance devices. LCP connectors are engineered for durability, ensuring long-lasting performance even in demanding environments.

End-users of these connectors include manufacturers of smartphones, automotive systems, networking equipment, and medical devices, where advanced connectivity solutions are essential. These connectors play a crucial role in enabling reliable and efficient electrical connections in modern electronic systems.

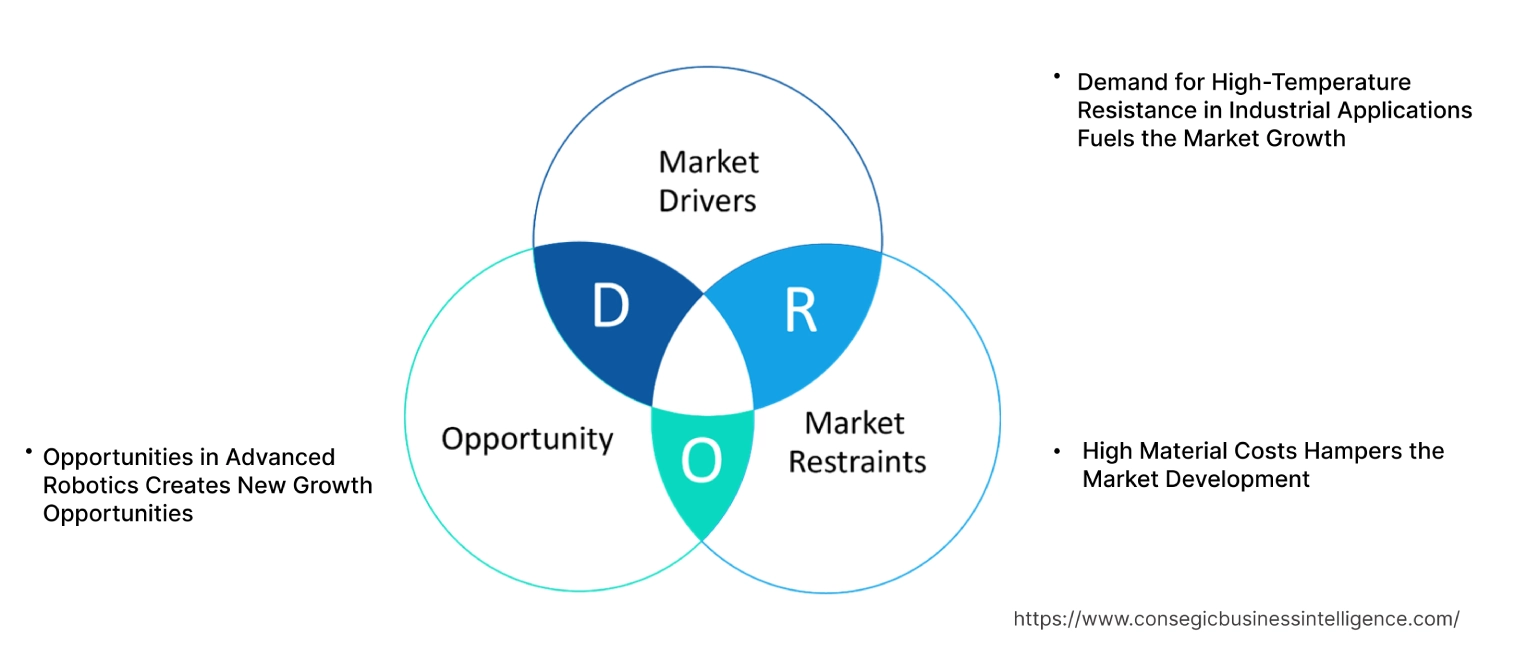

LCP Connectors Market Dynamics - (DRO) :

Key Drivers:

Demand for High-Temperature Resistance in Industrial Applications Fuels the Market Growth

Industrial applications, including manufacturing, energy, and heavy machinery, often operate under extreme conditions involving high temperatures, pressure, and exposure to chemicals. Connectors used in such environments must deliver reliable performance without compromising safety or efficiency. Liquid Crystal Polymer (LCP) connectors, known for their exceptional thermal stability and chemical resistance, have become an ideal choice for these applications. They maintain electrical insulation and mechanical integrity even at elevated temperatures, ensuring durability and long-term functionality. In industrial automation, these connectors support advanced systems such as robotics and power distribution equipment, where precision and reliability are paramount. Additionally, their resistance to corrosion and wear makes them well-suited for energy sectors like oil and gas, as well as renewable energy installations, which require high-performance components in harsh operational conditions. Consequently, the superior properties of LCP connectors are driving their widespread adoption in industrial environments, which further boosts the LCP connectors market growth.

Key Restraints:

High Material Costs Hampers the Market Development

The advanced properties of liquid crystal polymers (LCPs), such as superior thermal stability, chemical resistance, and mechanical strength, make them highly desirable for specialized applications. However, these benefits come with a significant cost, as LCPs are substantially more expensive than conventional polymers like polyethylene or polypropylene. This high material cost often limits their adoption in cost-sensitive industries, particularly where budget constraints dominate decision-making processes. Small-scale manufacturers and applications that do not require extreme performance, opt for less expensive alternatives, further restricting the market penetration of LCP-based connectors and components. Thus, the aforementioned factors limit the LCP connectors market demand.

Future Opportunities :

Opportunities in Advanced Robotics Creates New Growth Opportunities

The growth in the adoption of advanced robotics in manufacturing, healthcare, and consumer applications is driving the need for high-performance connectors. Robotics systems require precise and reliable data transmission to ensure accurate functionality in tasks such as automated assembly, surgical procedures, and service robotics. LCP connectors, known for their lightweight construction and excellent high-frequency signal handling, meet these requirements effectively. Additionally, their resistance to harsh environments, such as high temperatures and vibrations, enhances their suitability for industrial robotics and medical applications. As robotics systems continue to evolve with more complex functionalities, the need for compact and durable connectors that support high data speeds and operational efficiency will grow, positioning LCP connectors as a key enabler of innovation in the robotics sector. This trend aligns with increasing global investments in automation and robotics technology, fostering significant LCP connectors market opportunities.

LCP Connectors Market Segmental Analysis :

By Connector Type:

Based on connector type, the market is segmented into rectangular connectors, circular connectors, card edge connectors, backplane connectors, modular connectors, and others.

The Rectangular connectors accounted for the largest revenue of the total LCP connectors market share in 2023.

- These connectors are widely used due to their versatility and ability to support high-density connections across IT and telecom applications.

- Their durability and reliable signal integrity make them suitable for high-performance electronic devices, further driving their adoption.

- Rectangular connectors are increasingly preferred in automotive systems for connecting control units and sensors.

- As per the LCP connectors market analysis, the segment’s dominance reflects its adaptability across multiple industries, ensuring seamless data transmission and operational efficiency.

The Circular connectors are expected to register the fastest CAGR during the forecast period.

- Their compact design and robust structure make them ideal for demanding environments, such as aerospace and industrial applications.

- Circular connectors are increasingly adopted in healthcare for imaging systems and monitoring equipment due to their secure and interference-free connections.

- Advancements in waterproof and ruggedized circular connectors enhance their usage in outdoor and automotive applications.

- As per the LCP connectors market trends, the segment’s rapid adoption is attributed to the growth in demand for durable and lightweight connectivity solutions in emerging markets.

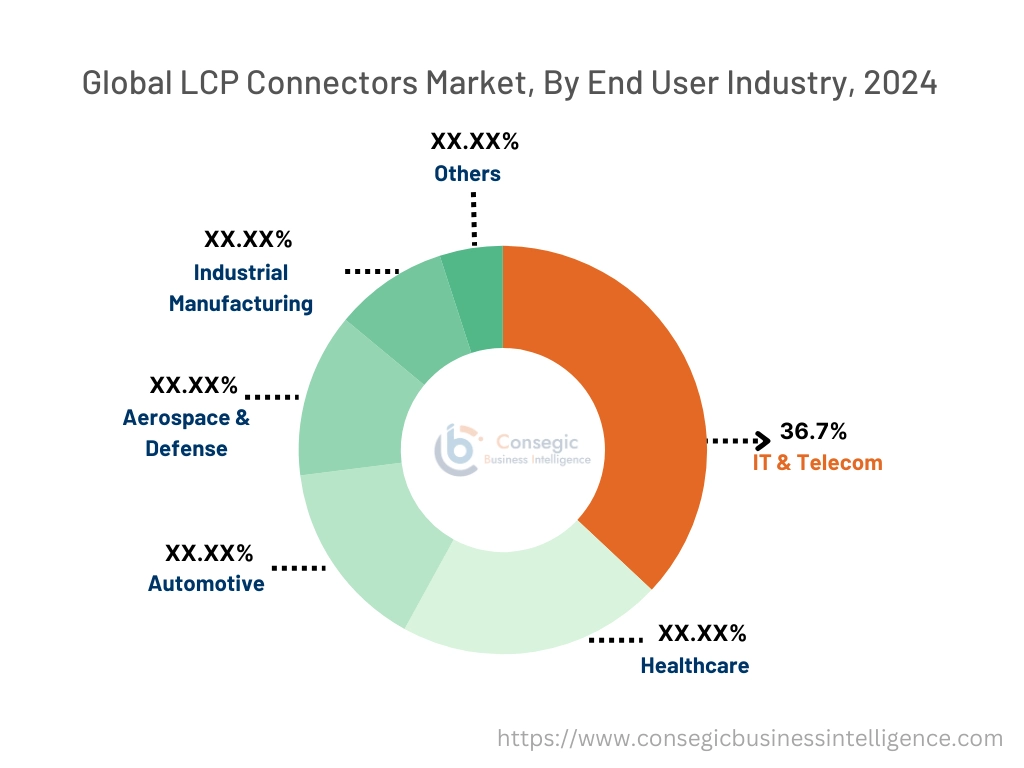

By End-User Industry:

Based on end-user industry, the market is segmented into IT & telecom, healthcare, automotive, aerospace & defense, industrial manufacturing, and others.

The IT & telecom segment held the largest revenue of 36.7% of the total LCP connectors market share in 2024.

- The proliferation of data centers and advancements in 5G networks have increased the demand for high-speed and reliable connectivity solutions.

- LCP connectors are essential in telecom equipment due to their excellent thermal resistance and electrical performance.

- Their usage in networking devices such as routers and switches further supports the IT & telecom segment's dominance.

- As per segmental trends analysis, the rising deployment of cloud computing and IoT solutions strengthens the segment’s position, driving the LCP connectors market expansion.

The automotive segment is projected to grow at the fastest CAGR during the forecast period.

- LCP connectors are crucial in electric vehicles (EVs) and advanced driver-assistance systems (ADAS) for ensuring reliable and compact connections.

- Their lightweight design and ability to operate in harsh conditions enhance their applicability in modern automotive systems.

- Increasing investments in EV infrastructure and connected vehicles drive the adoption of these connectors in the automotive sector.

- The analysis of segmental trends shows that the segment’s growth is also supported by innovations in vehicle electronics, such as infotainment and safety systems, requiring high-performance connectivity solutions, which further boosts the LCP connectors market growth.

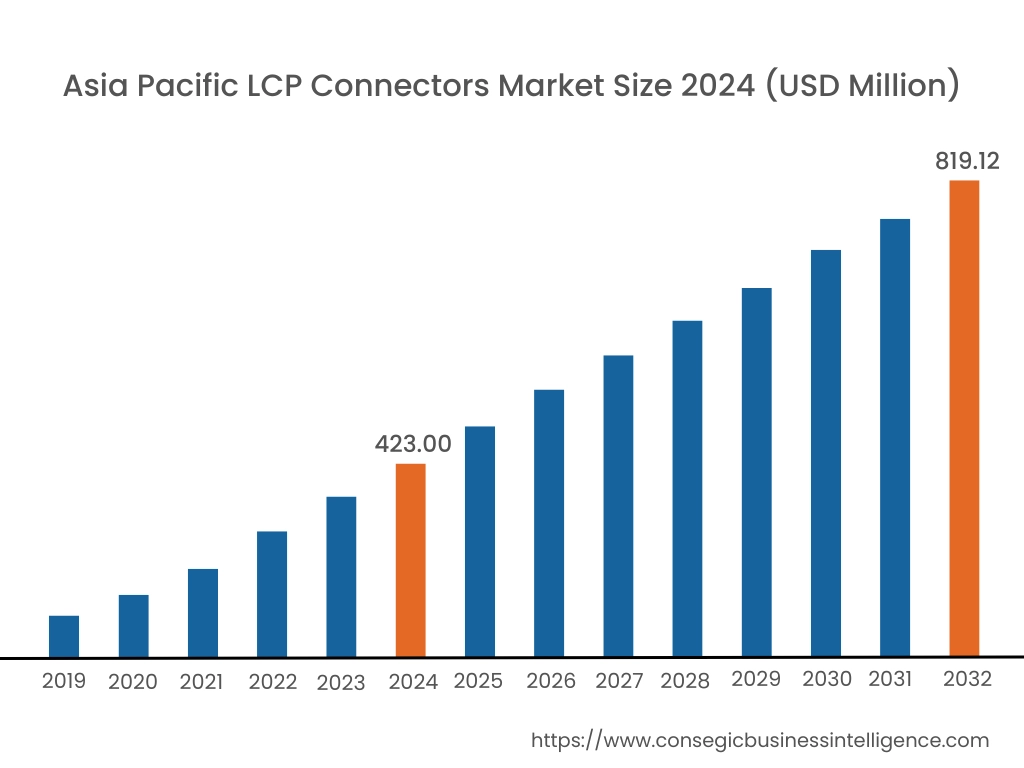

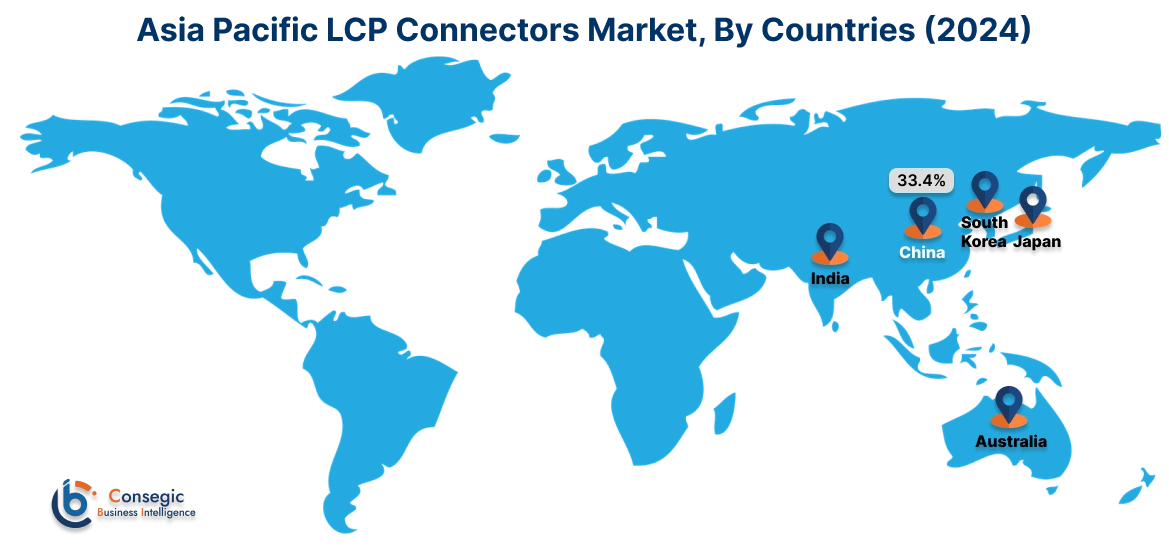

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

Asia Pacific region was valued at USD 423.00 Million in 2024. Moreover, it is projected to grow by USD 451.25 Million in 2025 and reach over USD 819.12 Million by 2032. Out of this, China accounted for the maximum revenue share of 33.4%. The Asia-Pacific region is experiencing rapid development in the LCP connectors market, driven by industrialization and technological advancements in countries such as China, Japan, and South Korea. The expansion of the consumer electronics sector and the rising need for high-performance connectors have intensified the need for advanced materials like LCP. Government initiatives promoting industrial efficiency further influence LCP connectors market demand.

North America is estimated to reach over USD 871.84 Million by 2032 from a value of USD 476.43 Million in 2024 and is projected to grow by USD 505.84 Million in 2025. This region holds a significant share of the LCP connectors market, driven by the increasing adoption of advanced electronic devices and the miniaturization of components. The United States, in particular, has seen a rise in the implementation of these connectors in sectors such as automotive, consumer electronics, and telecommunications. A notable trend is the integration of high-frequency applications due to their superior thermal and mechanical properties. Analysis indicates that the presence of key market players and continuous technological advancements contribute to the region's LCP connectors market expansion.

Europe represents a substantial share of the global LCP connectors market, with countries like Germany, France, and the United Kingdom leading in adoption and innovation. The region's emphasis on sustainability and energy efficiency has propelled the utilization of eco-friendly materials in connector manufacturing. Analysis indicates a growing trend towards the deployment of LCP connectors in automotive and industrial machinery applications, offering flexibility across multiple sectors and creating new LCP connectors market opportunities.

The Middle East & Africa region shows a growing interest in advanced connector solutions, particularly in the telecommunications and industrial sectors. Countries like the United Arab Emirates and South Africa are investing in modern technologies to enhance data transmission capabilities and comply with international standards. The LCP connectors market analysis suggests an increasing trend toward adopting LCP connectors to meet the needs of modern communication networks.

Latin America is an emerging market with Brazil and Mexico being key contributors. The region's growing focus on technological modernization and the automotive sector has spurred the adoption of advanced connector solutions. As per the LCP connectors market trends, government policies aimed at enhancing technological capabilities influence market trends.

Top Key Players and Market Share Insights:

The LCP Connectors market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global LCP Connectors market. Key players in the LCP Connectors industry include -

- Sumitomo Chemical Company (Japan)

- Amphenol Corporation (USA)

- RTP Company (USA)

- HARTING Technology Group (Germany)

- TE Connectivity Ltd. (Switzerland)

- Würth Elektronik GmbH & Co. KG (Germany)

- 3M Company (USA)

- Japan Aviation Electronics Industry, Ltd. (Japan)

- Hirose Electric Co., Ltd. (Japan)

- Celanese Corporation (USA)

LCP Connectors Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 2,690.03 Million |

| CAGR (2025-2032) | 8.2% |

| By Connector Type |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the LCP Connectors Market? +

LCP Connectors Market size is estimated to reach over USD 2,690.03 Million by 2032 from a value of USD 1,436.28 Million in 2024 and is projected to grow by USD 1,527.89 Million in 2025, growing at a CAGR of 8.2% from 2025 to 2032.

What are the key drivers of the LCP Connectors Market? +

Key drivers include the increasing demand for high-temperature resistance in industrial applications, particularly in sectors like manufacturing, energy, and aerospace. LCP connectors offer excellent thermal stability and chemical resistance, making them ideal for harsh environments. Their use in advanced systems like robotics, power distribution, and renewable energy also fuels demand.

What are the key segments of the LCP Connectors Market? +

The market is segmented by connector type (rectangular, circular, card edge, backplane, modular connectors, and others), end-user industry (IT & telecom, healthcare, automotive, aerospace & defense, industrial manufacturing, and others), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Who are the leading players in the LCP Connectors Market? +

Leading players include Sumitomo Chemical Company (Japan), Amphenol Corporation (USA), Würth Elektronik GmbH & Co. KG (Germany), 3M Company (USA), Japan Aviation Electronics Industry, Ltd. (Japan), Hirose Electric Co., Ltd. (Japan), and others.