- Summary

- Table Of Content

- Methodology

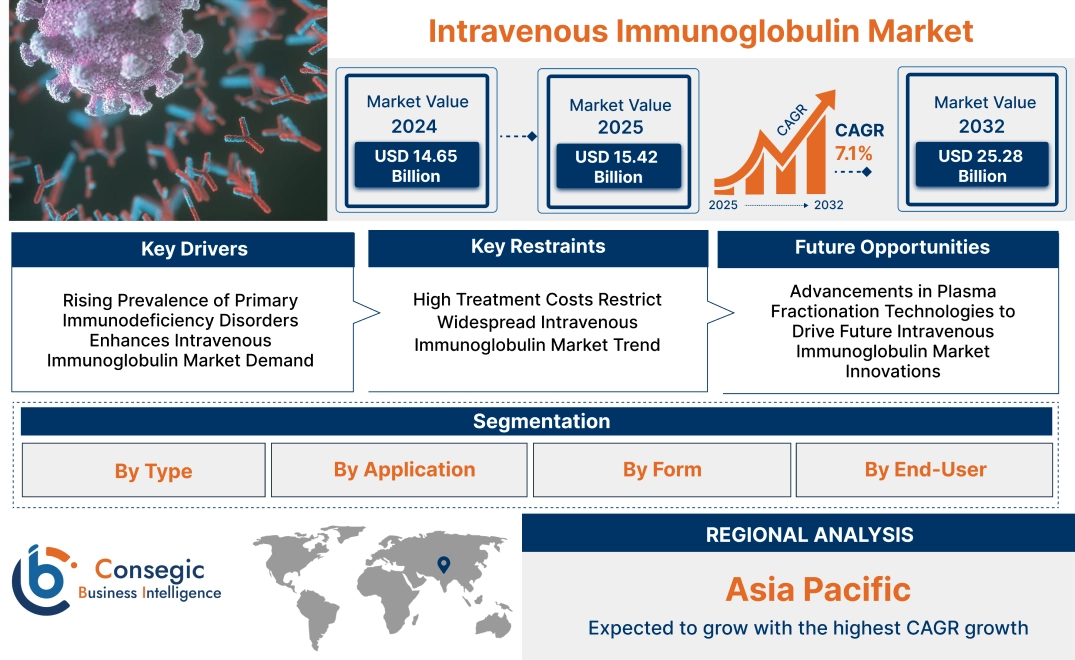

Intravenous Immunoglobulin Market Size:

Intravenous Immunoglobulin Market size is estimated to reach over USD 25.28 Billion by 2032 from a value of USD 14.65 Billion in 2024 and is projected to grow by USD 15.42 Billion in 2025, growing at a CAGR of 7.1% from 2025 to 2032.

Intravenous Immunoglobulin Market Scope & Overview:

Intravenous immunoglobulin (IVIG) is a blood product containing pooled immunoglobulins extracted from plasma donations. It is used for treating immune deficiencies, autoimmune diseases, and neurological disorders. IVIG provides passive immunity by supplying antibodies that help modulate immune responses and reduce inflammation.

Key properties include high purity, stability, and compatibility with human plasma. IVIG formulations are available in different concentrations and are administered through intravenous infusion. It helps manage conditions by preventing infections, modulating immune responses, and reducing disease progression.

Applications include primary immunodeficiency disorders, chronic inflammatory demyelinating polyneuropathy, and immune thrombocytopenia. IVIG is also used in neurology, hematology, and rheumatology. End users include hospitals, specialty clinics, and infusion centers.

Intravenous Immunoglobulin Market Dynamics - (DRO):

Intravenous Immunoglobulin Market Dynamics - (DRO) :

Key Drivers:

Rising Prevalence of Primary Immunodeficiency Disorders Enhances Intravenous Immunoglobulin Market Demand

Primary immunodeficiency disorders (PIDs) weaken the immune system, making individuals more susceptible to infections and other health complications. Intravenous immunoglobulin (IVIG) therapy plays a crucial role in managing these conditions by providing essential antibodies that help fight infections. The increasing diagnosis of PIDs due to improved awareness and advanced diagnostic techniques has led to a surge in trend for IVIG treatments. According to global health reports, the prevalence of primary immunodeficiency disorders is rising, particularly among pediatric and geriatric populations. With IVIG serving as a standard treatment for PIDs, this growing patient base is increasing its trend. Therefore, the expanding prevalence of PIDs is a significant factor propelling the IVIG market.

Key Restraints:

High Treatment Costs Restrict Widespread Intravenous Immunoglobulin Market Trend

The cost of intravenous immunoglobulin therapy is significantly high, making it inaccessible to many patients, particularly in low- and middle-income regions. The production of IVIG involves complex purification and fractionation processes, contributing to elevated manufacturing expenses. Additionally, the need for frequent infusions further increases the financial burden on patients. Healthcare reimbursement policies vary across regions, and in several cases, partial or no coverage is provided, further limiting affordability. For instance, in developing countries, the lack of government-funded healthcare support restricts access to IVIG treatments. This financial barrier hampers the widespread adoption of IVIG therapy, thereby restraining the intravenous immunoglobulin market expansion.

Future Opportunities :

Advancements in Plasma Fractionation Technologies to Drive Future Intravenous Immunoglobulin Market Innovations

Ongoing advancements in plasma fractionation technologies are expected to enhance the production efficiency and quality of intravenous immunoglobulin products. Innovations in purification methods and recombinant technologies are likely to improve yield and reduce impurities, thereby increasing the overall efficacy and safety of IVIG treatments. Researchers are also exploring novel IVIG formulations with extended half-life to reduce dosing frequency, which would benefit patients by lowering the treatment burden. Additionally, the integration of artificial intelligence in plasma screening and purification processes will likely improve consistency and scalability in IVIG production. Therefore, technological advancements in plasma fractionation present a promising intravenous immunoglobulin market opportunity for the future growth of the IVIG market.

Intravenous Immunoglobulin Market Segmental Analysis :

By Type:

Based on type, the intravenous immunoglobulin (IVIG) market is segmented into IgA, IgM, IgD, IgE, and IgG.

The IgG segment accounted for the largest revenue in intravenous immunoglobulin market share in 2024.

- IgG is the most widely used immunoglobulin type in IVIG therapy due to its essential role in immune response modulation and disease management.

- It is primarily used for the treatment of immunodeficiencies, autoimmune disorders, and inflammatory diseases, contributing to its high demand.

- Increasing awareness of immune disorders and the growing number of patients requiring IVIG therapy further support intravenous immunoglobulin market expansion.

- Ongoing research and advancements in IVIG formulations enhance product efficacy and safety.

- According to intravenous immunoglobulin market analysis, extensive clinical applications of IgG in managing immune-related disorders drive its dominance in the market.

The IgM segment is anticipated to register the fastest CAGR during the forecast period.

- IgM plays a crucial role in primary immune responses, making it a key component in immune therapies.

- Rising incidences of severe infections, immunodeficiencies, and autoimmune disorders have boosted the growth for IgM-based IVIG treatments.

- Increased research efforts to enhance the stability and efficacy of IgM formulations contribute to its projected growth.

- According to intravenous immunoglobulin market analysis, technological advancements in production and purification processes further support market expansion.

By Application:

Based on application, the intravenous immunoglobulin (IVIG) market is segmented into primary immunodeficiency diseases, myasthenia gravis, chronic inflammatory demyelinating polyneuropathy (CIDP), hypogammaglobulinemia, multifocal motor neuropathy, Kawasaki disease, Guillain-Barre syndrome, and others.

The chronic inflammatory demyelinating polyneuropathy (CIDP) segment accounted for the largest revenue share in 2024.

- CIDP is a neurological disorder requiring long-term immunoglobulin therapy, making IVIG a primary treatment option.

- IVIG helps reduce inflammation, improve nerve function, and restore mobility in affected patients.

- The increasing prevalence of CIDP and growing awareness among healthcare professionals contribute to the segment's market dominance.

- Segmental analysis suggests, ongoing clinical research and advancements in IVIG formulations enhance treatment effectiveness and patient outcomes.

The myasthenia gravis segment is anticipated to register the fastest CAGR during the forecast period.

- IVIG therapy is increasingly used for managing myasthenia gravis, especially in severe cases and during myasthenic crises.

- The rising incidence of autoimmune neuromuscular disorders is driving trend for IVIG treatments.

- Expanding healthcare access and improved diagnostic capabilities contribute to early detection and treatment trend.

- Market analysis suggests, ongoing research on novel IVIG formulations and treatment protocols supports intravenous immunoglobulin market growth.

By Form:

Based on form, the intravenous immunoglobulin (IVIG) market is segmented into liquid and lyophilized.

The liquid segment accounted for the largest revenue in intravenous immunoglobulin market share in 2024.

- Liquid IVIG is widely preferred due to its ease of administration and reduced preparation time.

- It minimizes the risk of contamination and offers enhanced convenience for both patients and healthcare providers.

- The increasing availability of liquid IVIG formulations across healthcare settings strengthens its market position.

- According to market analysis, advancements in storage and transportation solutions contribute to the continued trend for liquid IVIG.

The lyophilized segment is anticipated to register the fastest CAGR during the forecast period.

- Lyophilized IVIG offers improved stability and longer shelf life, making it a preferred choice in regions with limited cold chain facilities.

- It reduces the risk of degradation, ensuring product efficacy over extended periods.

- The growing adoption of lyophilized IVIG in emerging markets is supporting its rapid expansion.

- Market analysis suggests increasing research on advanced lyophilization techniques enhances the segment's growth potential.

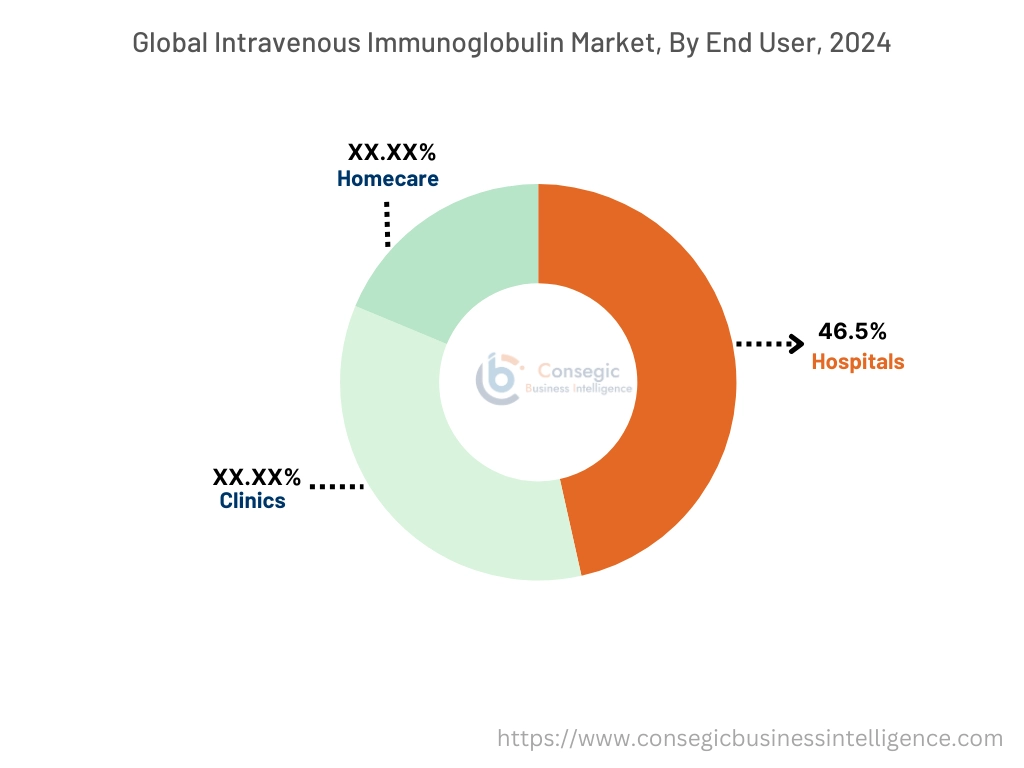

By End-User:

Based on end-user, the intravenous immunoglobulin (IVIG) market is segmented into hospitals, clinics, and homecare.

The hospitals segment accounted for the largest revenue share of 46.5% in 2024.

- Hospitals serve as the primary point of care for IVIG administration, handling complex cases that require continuous monitoring.

- Availability of specialized healthcare professionals and advanced infrastructure supports the segment's dominance.

- Increasing hospital admissions for immune disorders and neurological conditions further boost demand.

- According to market analysis, rising government and private investments in hospital infrastructure enhance accessibility to IVIG treatments.

The homecare segment is anticipated to register the fastest CAGR during the forecast period.

- The shift toward home-based IVIG administration is driven by patient preference for convenience and reduced hospital visits.

- Advancements in infusion technologies and remote patient monitoring support the growing adoption of homecare IVIG treatments.

- Increasing awareness of home-based care and cost-effective treatment options contribute to the segment’s growth.

- Market analysis suggests expanding reimbursement policies for homecare therapies enhance affordability and accessibility.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

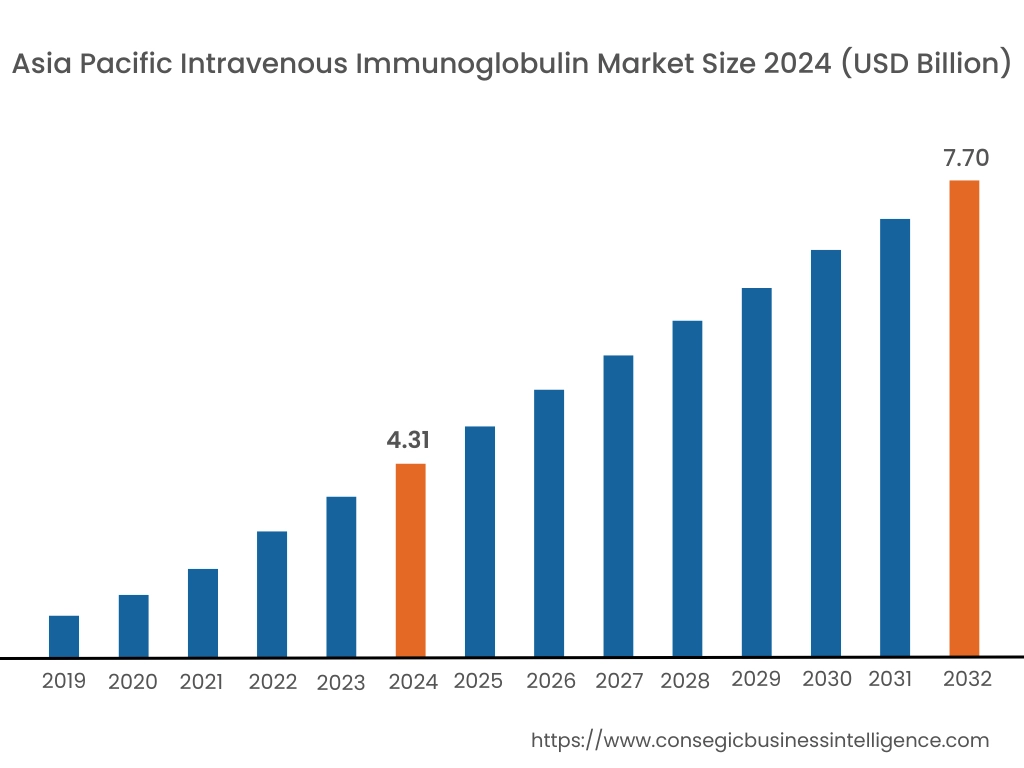

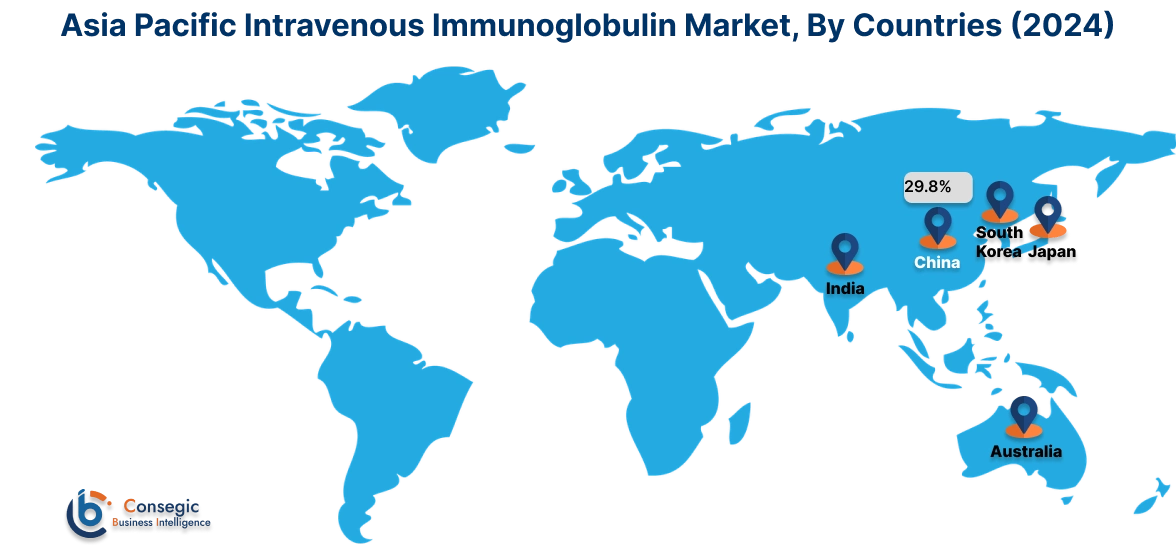

In 2024, Asia-Pacific was valued at USD 4.31 Billion and is expected to reach USD 7.70 Billion in 2032. In Asia-Pacific, China accounted for the highest share of 29.8% during the base year of 2024. Asia-Pacific exhibits increasing trend for intravenous immunoglobulin due to a rising incidence of autoimmune disorders, neuromuscular diseases, and primary immunodeficiency conditions. Expanding healthcare infrastructure in China, Japan, and India supports treatment accessibility. Increasing government investments in plasma fractionation facilities enhance local production capabilities. A growing aging population and rising healthcare expenditures influence intravenous immunoglobulin market demand. Regulatory improvements streamline product approvals and distribution. Expanding medical tourism in countries like Thailand and South Korea increases the availability of specialized treatments. Limited plasma collection infrastructure in some developing countries affects supply chain efficiency.

North America is estimated to reach over USD 8.19 Billion by 2032 from a value of USD 4.86 Billion in 2024 and is projected to grow by USD 5.11 Billion in 2025. North America holds a significant share in the intravenous immunoglobulin market due to the high prevalence of immunodeficiency disorders, autoimmune diseases, and neurological conditions. Advanced healthcare infrastructure supports the adoption of intravenous immunoglobulin therapies. A well-established reimbursement framework ensures patient accessibility to high-cost treatments. Leading biopharmaceutical companies and research institutions contribute to continuous product development and innovation. Rising awareness about primary immunodeficiency diseases and strong government support for plasma-derived therapies influence market performance. The presence of large-scale plasma collection centers ensures a steady supply of immunoglobulin products.

Europe demonstrates steady intravenous immunoglobulin market demand for intravenous immunoglobulin, supported by a well-developed healthcare system and strong regulatory frameworks. The high prevalence of chronic inflammatory demyelinating polyneuropathy (CIDP) and immune thrombocytopenia contributes to market performance. National health insurance programs in countries like Germany, France, and the United Kingdom provide reimbursement coverage for immunoglobulin therapies. Strict regulations on plasma collection and processing impact product availability. Research advancements in plasma-derived therapies support market expansion. Increasing awareness campaigns for rare diseases improve early diagnosis and treatment rates. The presence of major pharmaceutical companies strengthens regional supply chains.

The Middle East and Africa have a developing intravenous immunoglobulin market, influenced by improving healthcare infrastructure and increasing diagnosis rates of immunodeficiency disorders. Rising investments in specialized treatment facilities enhance market performance. The trend for immunoglobulin therapies is growing in countries like Saudi Arabia, the United Arab Emirates, and South Africa. Limited domestic plasma collection facilities lead to a reliance on imported immunoglobulin products. High treatment costs and varying reimbursement policies affect patient accessibility. Expanding government initiatives for rare disease treatment improve intravenous immunoglobulin market opportunities. Awareness programs and collaborations with international pharmaceutical companies support product availability.

Latin America experiences increasing demand for intravenous immunoglobulin due to a rising incidence of immune disorders and neurological conditions. Expanding healthcare coverage in countries like Brazil, Mexico, and Argentina supports intravenous immunoglobulin market growth. Government efforts to improve plasma collection and processing enhance product availability. High treatment costs and economic instability affect patient access to immunoglobulin therapies. Research collaborations with international biopharmaceutical companies contribute to the development of advanced treatment options. Regulatory advancements improve the approval process for new immunoglobulin products. Increasing awareness and diagnostic capabilities lead to better disease management.

Top Key Players and Market Share Insights:

The global intravenous immunoglobulin market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (r&d), product innovation, and end-user launches to hold a strong position in the global intravenous immunoglobulin market. Key players in the intravenous immunoglobulin industry include-

- CSL Behring (Australia)

- Grifols S.A. (Spain)

- Kedrion Biopharma (Italy)

- Octapharma AG (Switzerland)

- Takeda Pharmaceutical Company Limited (Japan)

- Biotest AG (Germany)

- LFB Group (France)

- ADMA Biologics, Inc. (United States)

- China Biologic Products Holdings, Inc. (China)

- Baxter International Inc. (United States)

Recent Industry Developments :

Product Launches:

- In June 2024, Biotest AG, a subsidiary of Grifols, received FDA approval for Yimmugo, an innovative IVIG therapeutic designed to treat primary immunodeficiencies (PID).

- In September 2024, GC Biopharma USA, Inc. launched ALYGLO (immune globulin intravenous, human-stwk), a 10% IVIG therapy for adult patients with primary humoral immunodeficiency.

Intravenous Immunoglobulin Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 25.28 Billion |

| CAGR (2025-2032) | 24.6% |

| By Type |

|

| By Application |

|

| By Form |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Intravenous Immunoglobulin Market? +

In 2024, the Intravenous Immunoglobulin Market was USD 14.65 Billion.

What will be the potential market valuation for the Intravenous Immunoglobulin Market by 2032? +

In 2032, the market size of Intravenous Immunoglobulin Market is expected to reach USD 25.28 Billion.

What are the segments covered in the Intravenous Immunoglobulin Market report? +

The type, application, form, and end-user are the segments covered in this report.

Who are the major players in the Intravenous Immunoglobulin Market? +

CSL Behring (Australia), Grifols S.A. (Spain), Kedrion Biopharma (Italy), Octapharma AG (Switzerland), Takeda Pharmaceutical Company Limited (Japan), Biotest AG (Germany), LFB Group (France), ADMA Biologics, Inc. (United States), China Biologic Products Holdings, Inc. (China), Baxter International Inc. (United States) are the major players in the Intravenous Immunoglobulin market.