- Summary

- Table Of Content

- Methodology

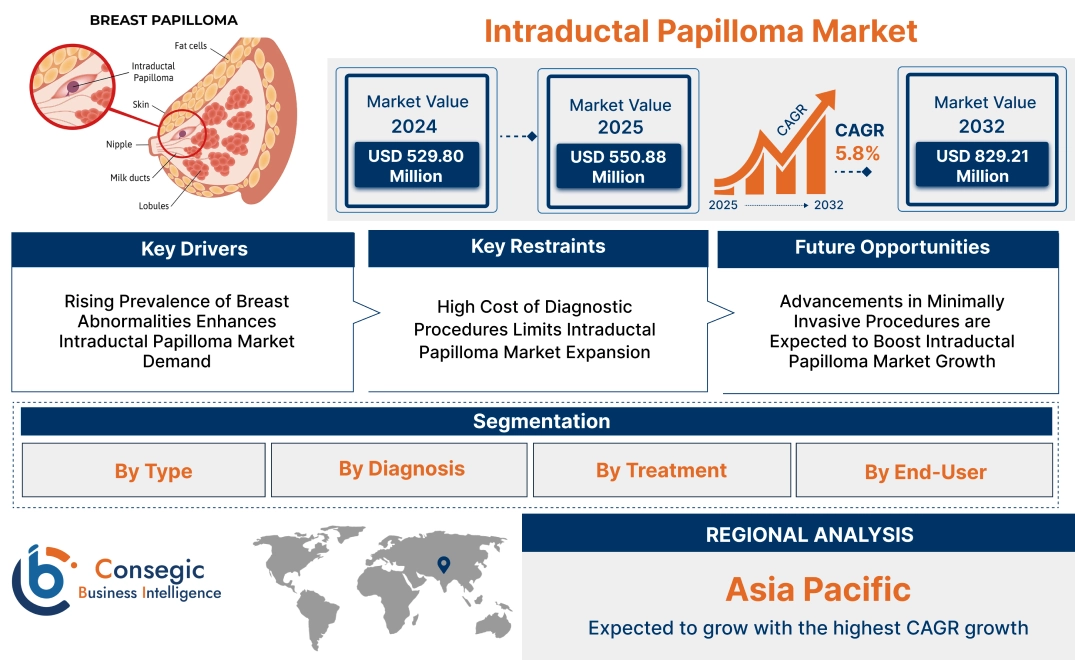

Intraductal Papilloma Market Size:

Intraductal Papilloma Market size is estimated to reach over USD 829.21 Million by 2032 from a value of USD 529.80 Million in 2024 and is projected to grow by USD 550.88 Million in 2025, growing at a CAGR of 5.8% from 2025 to 2032.

Intraductal Papilloma Market Scope & Overview:

Intraductal papilloma is a benign tumor that forms within the milk ducts of the breast. It consists of glandular and fibrous tissues with vascular structures. This condition is commonly diagnosed through imaging techniques and biopsy procedures.

Key characteristics include painless lump formation, nipple discharge, and the presence of a central fibrovascular core. Diagnostic methods involve ultrasound, mammography, and ductography to detect abnormalities in the milk ducts. Treatment options include surgical excision and minimally invasive procedures for lesion removal.

Intraductal papilloma management is essential in hospitals, diagnostic centers, and specialty clinics. It is used in early detection and treatment planning to reduce complications. End users include healthcare providers, research institutions, and pharmaceutical companies involved in developing diagnostic tools and therapeutic approaches.

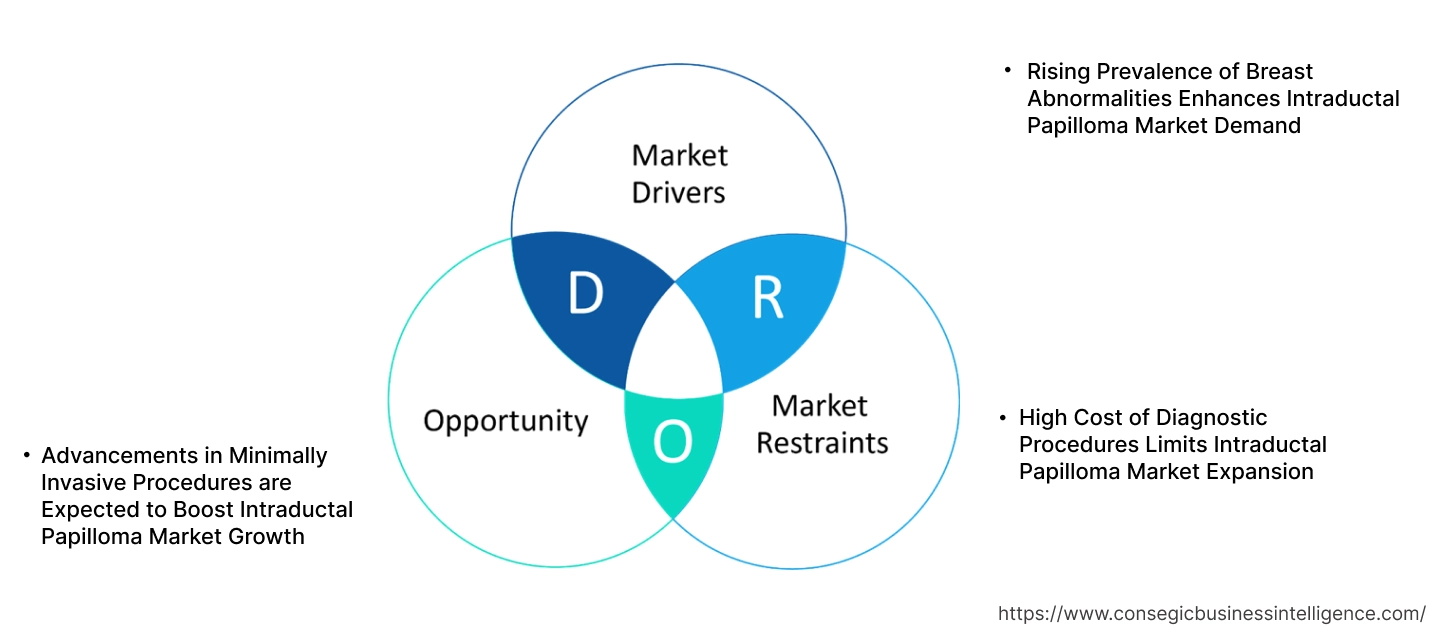

Intraductal Papilloma Market Dynamics - (DRO):

Key Drivers:

Rising Prevalence of Breast Abnormalities Enhances Intraductal Papilloma Market Demand

The increasing prevalence of breast abnormalities, including intraductal papillomas, has led to a greater demand for diagnostic and treatment solutions. They are benign tumors that develop within the milk ducts of the breast, often causing nipple discharge and discomfort. The rising number of breast-related health concerns has resulted in more frequent clinical evaluations and screenings, fueling the need for advanced diagnostic techniques such as mammography and ultrasound. For instance, the growing awareness of early detection has led to an increase in the number of mammography screenings globally. This trend supports the expansion of the intraductal papilloma market by driving trend for accurate diagnostic and treatment options.

Key Restraints:

High Cost of Diagnostic Procedures Limits Intraductal Papilloma Market Expansion

The high cost of diagnostic procedures, including mammography, ultrasound, and biopsy, poses a significant challenge to the market. Many healthcare facilities, particularly in developing regions, lack access to advanced imaging technologies due to financial constraints. Patients often avoid seeking early diagnosis due to the high expenses associated with imaging and biopsy procedures. Additionally, out-of-pocket costs for these diagnostics can be a barrier in regions where insurance coverage is limited. As a result, the adoption of diagnostic solutions remains restricted, hindering the intraductal papilloma market expansion.

Future Opportunities:

Advancements in Minimally Invasive Procedures are Expected to Boost Intraductal Papilloma Market Growth

The development of minimally invasive procedures for diagnosis and treatment is expected to create significant opportunities. Techniques such as vacuum-assisted core biopsy and ultrasound-guided procedures offer less discomfort and quicker recovery times compared to traditional surgical excision. These advancements improve patient outcomes while reducing procedural costs and hospital stays. For instance, ongoing research and technological advancements in image-guided biopsy techniques are expected to enhance precision and diagnostic efficiency. Therefore, the increasing adoption of minimally invasive procedures is likely to propel the growth of the intraductal papilloma market in the coming years.

Intraductal Papilloma Market Segmental Analysis :

By Type:

Based on type, the market is segmented into central/solitary and peripheral/multiple.

The central/solitary segment accounted for the largest revenue in intraductal papilloma market share in 2024.

- This condition typically occurs in the large ducts near the nipple and is often associated with nipple discharge.

- It is commonly diagnosed in middle-aged women and is generally benign, requiring minimal intervention.

- The ease of diagnosis and treatment, coupled with the rising awareness of breast health, contributes to the dominance of this segment.

- The increasing adoption of mammographic screening further enhances early detection rates, leading to a higher number of diagnosed cases.

- Therefore, according to intraductal papilloma market analysis, the aforementioned factors establish central/solitary as the leading segment in revenue generation.

The peripheral/multiple intraductal papilloma segment is anticipated to register the fastest CAGR during the forecast period.

- This type often occurs in the smaller ducts of the breast and has a higher risk of association with atypical hyperplasia or malignancy.

- Advanced imaging techniques such as high-resolution ultrasonography and MRI are improving early detection rates, contributing to intraductal papilloma market opportunities.

- Ongoing research on the malignant potential of multiple papillomas is driving trend for early intervention and biopsy procedures.

- Thus, according to intraductal papilloma market analysis, the above factors indicate significant market growth for the peripheral/multiple segment.

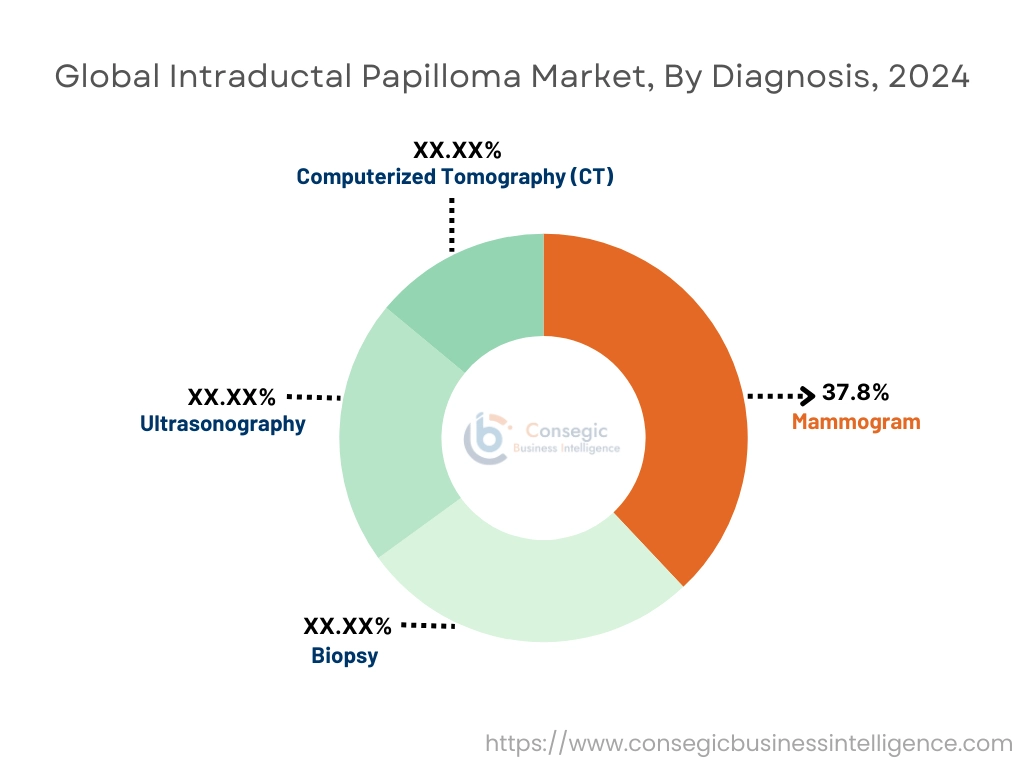

By Diagnosis:

Based on diagnosis, the market is segmented into mammogram, biopsy, ultrasonography, and computerized tomography (CT).

The mammogram segment accounted for the largest revenue in intraductal papilloma market share of 37.8% in 2024.

- Mammograms serve as a primary imaging tool for detecting intraductal papillomas, particularly in women over 40.

- The widespread availability of mammography screening programs enhances early identification rates.

- Continuous improvements in digital mammography and 3D tomosynthesis increase diagnostic accuracy.

- Therefore, according to the market analysis, these factors contribute to the dominance of the mammogram segment in market revenue.

The ultrasonography segment is anticipated to register the fastest CAGR during the forecast period.

- This non-invasive imaging technique is preferred for detecting papillomas in younger women with dense breast tissue.

- Real-time imaging capabilities and lower cost compared to MRI or CT enhance its adoption in clinical settings.

- The rising preference for ultrasound-guided biopsies contributes to the increasing use of ultrasonography.

- Thus, according to the market analysis, the above factors drive the high growth rate of the ultrasonography segment in the market.

By Treatment:

Based on treatment, the intraductal papilloma market is segmented into microdochectomy and total duct excision.

The microdochectomy segment accounted for the largest revenue share in 2024.

- This surgical procedure involves removing a single affected duct, preserving overall breast function.

- It is the preferred approach for treating central papillomas with nipple discharge.

- Minimally invasive techniques and improved surgical outcomes contribute to high adoption rates.

- Therefore, according to the market analysis, the above factors establish microdochectomy as the leading revenue-generating segment.

The total duct excision segment is anticipated to register the fastest CAGR during the forecast period.

- This procedure is recommended for multiple papillomas or cases with atypical hyperplasia.

- The increasing number of patients opting for preventive surgical interventions enhances intraductal papilloma market growth.

- Improved post-surgical outcomes and rising awareness contribute to the high demand for total duct excision.

- Thus, according to the market analysis, these factors highlight the strong trend potential of the total duct excision segment.

By End-User:

Based on end user, the market is segmented into hospitals, clinics, and academic and research institutes.

The hospital segment accounted for the largest revenue share in 2024.

- Hospitals provide comprehensive diagnostic, surgical, and post-operative care services for intraductal papilloma cases.

- The availability of advanced imaging technologies and skilled healthcare professionals ensures accurate diagnosis and treatment.

- Government initiatives promoting breast cancer screening programs contribute to patient volume in hospital settings.

- Therefore, according to the market analysis, these factors drive the dominance of the hospital segment in market revenue.

The clinics segment is anticipated to register the fastest CAGR during the forecast period.

- Specialized breast clinics offer outpatient services, leading to increased accessibility for patients.

- Shorter wait times, cost-effective diagnostic procedures, and minimally invasive treatments support intraductal papilloma market opportunities.

- Growing awareness and preference for private healthcare services contribute to the rapid trend of clinics in the market.

- Thus, according to the market analysis, these factors indicate significant growth potential for the clinics segment in the coming years.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

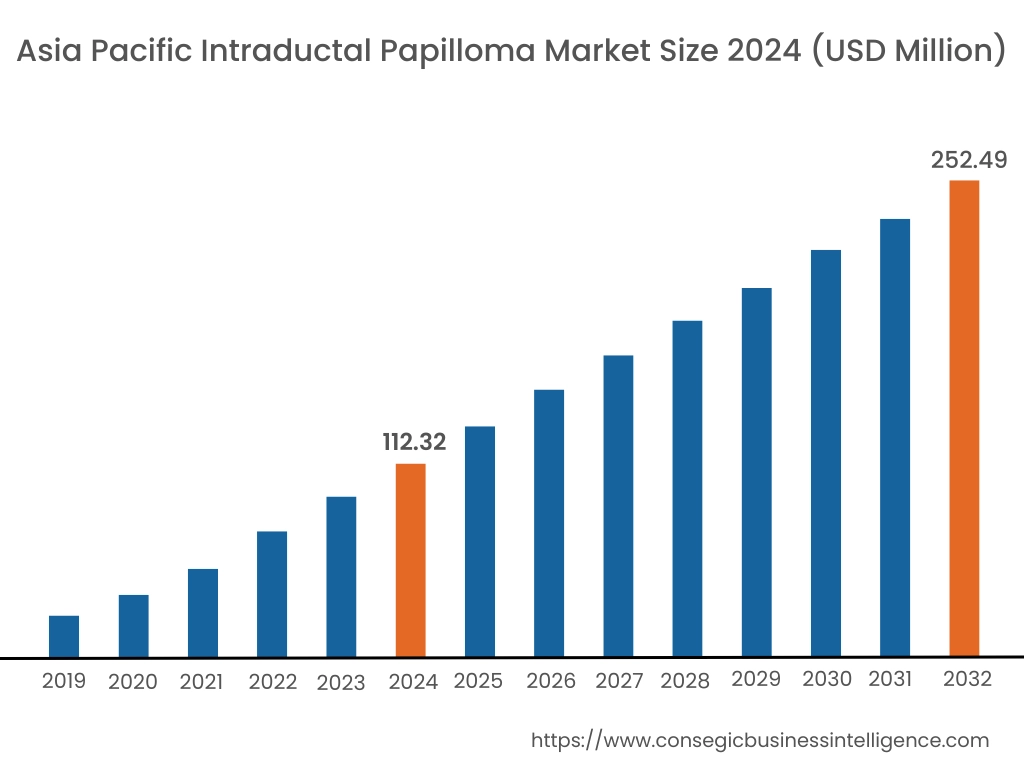

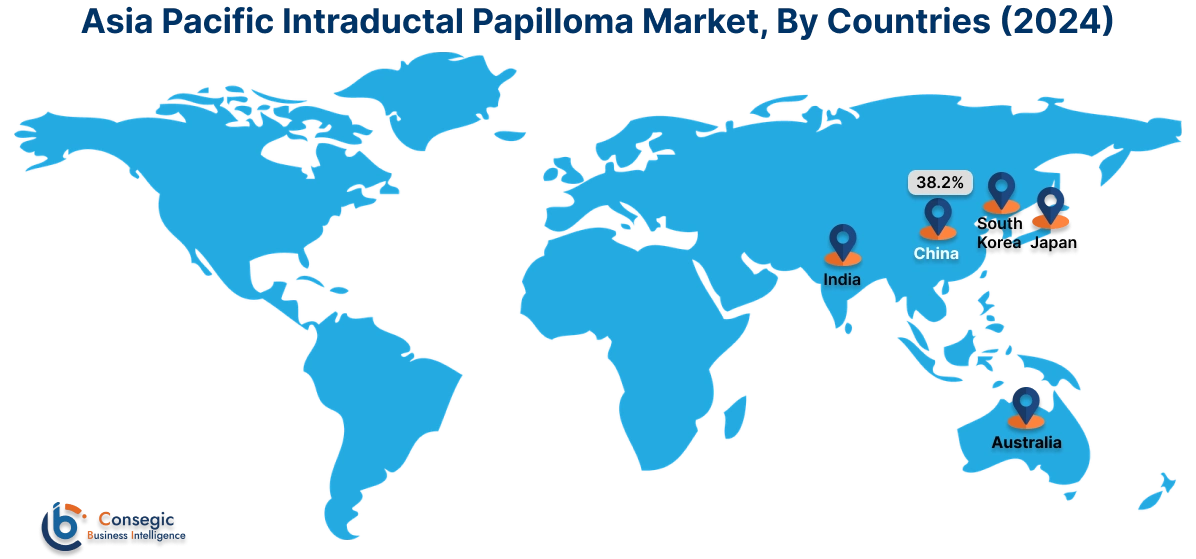

In 2024, Asia-Pacific was valued at USD 112.32 Million and is expected to reach USD 252.49 Million in 2032. In Asia-Pacific, the China accounted for the highest share of 38.2% during the base year of 2024. Asia-Pacific experiences rising trend for intraductal papilloma diagnosis and treatment due to increasing breast cancer awareness. Expanding healthcare infrastructure in China, India, and Japan influences market dynamics. Government initiatives promoting early diagnosis and the adoption of advanced imaging technologies impact market development. The presence of cost-effective treatment options and a large patient base drives medical service accessibility.

North America region was valued at USD 200.02 Million in 2024. Moreover, it is projected to grow by USD 205.53 Million in 2025 and reach over USD 268.75 Million by 2032. North America holds a significant share in the market due to advanced healthcare infrastructure and high awareness of breast health. The presence of leading medical device manufacturers and diagnostic centers supports market expansion. Favorable reimbursement policies and widespread adoption of imaging technologies influence intraductal papilloma market trends. Increased investment in breast cancer research and early detection programs contributes to market activity.

Europe demonstrates steady demand for intraductal papilloma diagnostics and treatment, supported by strong healthcare policies and advanced medical research. The United Kingdom, Germany, and France lead in market activity due to high adoption of digital mammography and biopsy techniques. Stringent regulatory standards influence the development of innovative diagnostic solutions. Increased healthcare expenditure and patient awareness impact market performance.

The Middle East and Africa have a developing intraductal papilloma market, influenced by improvements in medical infrastructure and healthcare accessibility. Expanding breast cancer screening programs in Gulf Cooperation Council (GCC) countries impact market growth. Limited access to specialized diagnostic facilities and delayed disease detection affect market progression. International healthcare collaborations support technological advancements in medical imaging.

Latin America exhibits increasing demand for intraductal papilloma diagnosis and treatment, with Brazil and Mexico leading in healthcare advancements. Rising awareness of breast cancer and government-led screening initiatives influence intraductal papilloma market trends. Economic challenges and disparities in healthcare infrastructure affect market accessibility. Expanding private healthcare investments and the presence of multinational diagnostic companies support market expansion.

Top Key Players & Market Share Insights:

The global intraductal papilloma market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global intraductal papilloma market. Key players in the intraductal papilloma industry include-

- Bayer AG (Germany)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Glenmark Pharmaceuticals (India)

- GlaxoSmithKline plc (United Kingdom)

- Novartis International AG (Switzerland)

- Stellar Pharma (Canada)

- Pfizer Inc. (United States)

- Wockhardt Ltd. (India)

- Ranbaxy Laboratories Limited (India)

- Bristol Laboratories (United Kingdom)

Intraductal Papilloma Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 829.21 Million |

| CAGR (2025-2032) | 5.8% |

| By Type |

|

| By Diagnosis |

|

| By Treatment |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Intraductal Papilloma Market? +

In 2024, the Intraductal Papilloma Market was USD 529.80 million.

What will be the potential market valuation for the Intraductal Papilloma Market by 2032? +

In 2032, the market size of Intraductal Papilloma Market is expected to reach USD 829.21 million.

What are the segments covered in the Intraductal Papilloma Market report? +

The type, diagnosis, treatment, and end-user are the segments covered in this report.

Who are the major players in the Intraductal Papilloma Market? +

Bayer AG (Germany), Teva Pharmaceutical Industries Ltd. (Israel), Stellar Pharma (Canada), Pfizer Inc. (United States), Wockhardt Ltd. (India), Ranbaxy Laboratories Limited (India), Bristol Laboratories (United Kingdom), Glenmark Pharmaceuticals (India), GlaxoSmithKline plc (United Kingdom), Novartis International AG (Switzerland) are the major players in the Intraductal Papilloma market.