- Summary

- Table Of Content

- Methodology

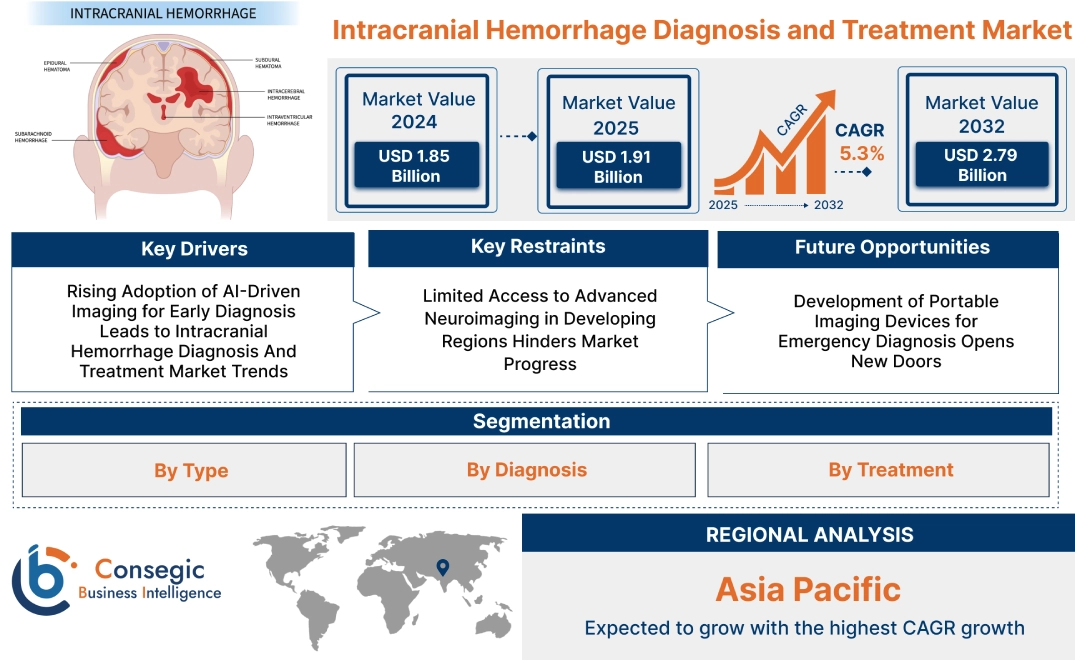

Intracranial Hemorrhage Diagnosis and Treatment Market Size:

Intracranial Hemorrhage Diagnosis and Treatment Market size is estimated to reach over USD 2.79 Billion by 2032 from a value of USD 1.85 Billion in 2024 and is projected to grow by USD 1.91 Billion in 2025, growing at a CAGR of 5.3% from 2025 to 2032.

Intracranial Hemorrhage Diagnosis and Treatment Market Scope & Overview:

Intracranial hemorrhage diagnosis and treatment involve medical techniques to detect and manage bleeding within the skull. These methods help prevent complications and improve patient outcomes. Diagnosis includes imaging technologies such as computed tomography (CT) and magnetic resonance imaging (MRI). Treatment options range from medication management to surgical interventions, depending on the severity and location of the bleeding.

Key characteristics of these solutions include high precision, rapid detection, and non-invasive or minimally invasive approaches. Early diagnosis supports timely medical intervention, reducing the risk of neurological damage. Treatment procedures focus on stabilizing patients, controlling bleeding, and preventing further complications.

These solutions are widely applied in hospitals, specialty clinics, and trauma centers. They assist in managing hemorrhagic strokes, traumatic brain injuries, and vascular disorders. End users include healthcare providers, emergency medical services, and neurosurgical specialists.

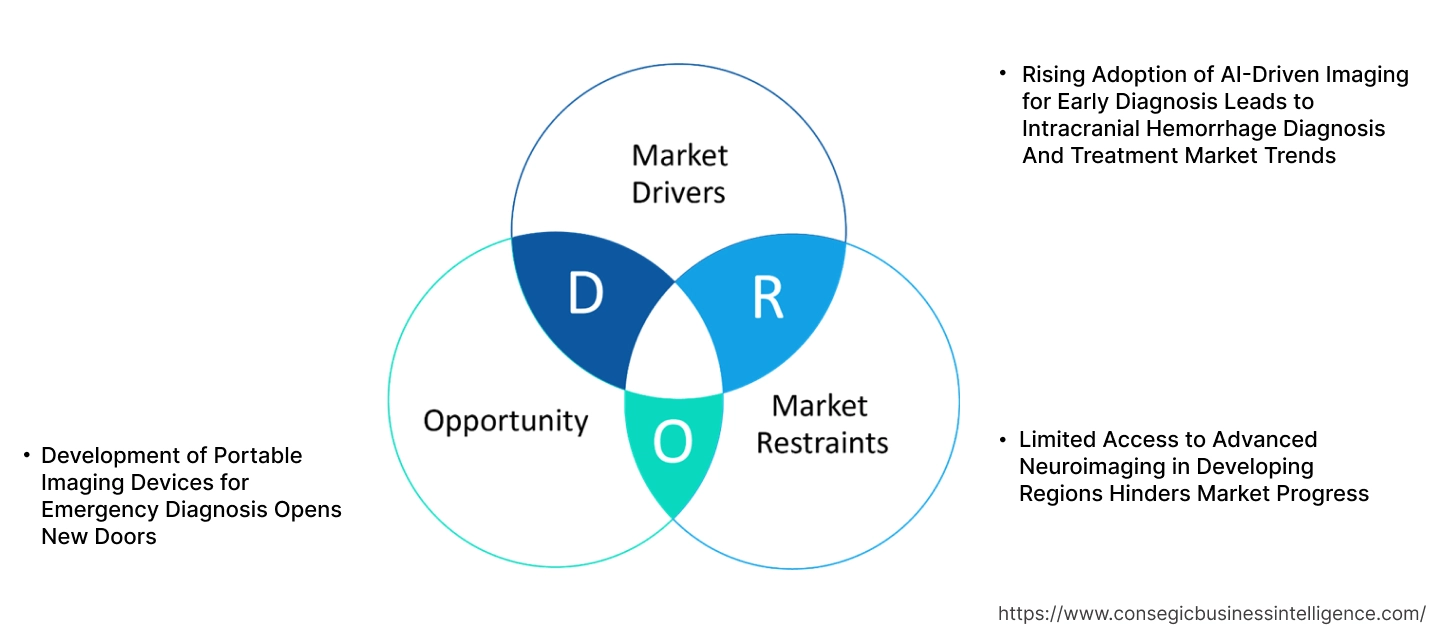

Intracranial Hemorrhage Diagnosis and Treatment Market Dynamics - (DRO):

Key Drivers:

Rising Adoption of AI-Driven Imaging for Early Diagnosis Leads to Intracranial Hemorrhage Diagnosis And Treatment Market Trends

Artificial intelligence (AI) has significantly improved the speed and accuracy of diagnosing intracranial hemorrhages by automating the detection of abnormalities in computed tomography (CT) and magnetic resonance imaging (MRI) scans. AI-powered imaging software enhances radiologists’ ability to detect hemorrhages in real time, reducing diagnostic errors and expediting treatment decisions. These systems utilize deep learning algorithms to highlight potential bleeding areas and issue automated alerts, allowing immediate clinical intervention. Hospitals and diagnostic centers integrate AI-based imaging tools to improve workflow efficiency and optimize patient management.

AI-driven platforms such as Viz.ai and Aidoc are already assisting healthcare providers in rapidly identifying acute hemorrhages, enabling emergency physicians to make prompt treatment decisions. Moreover, AI applications in neuroimaging reduce the burden on radiologists by automating routine image analysis, allowing them to focus on complex cases. These technological advancements play a crucial role in improving patient survival rates by minimizing diagnosis delays and enhancing treatment precision.

Thus, the increasing integration of AI-driven imaging solutions in hospitals and diagnostic centers strengthens the growth for advanced intracranial hemorrhage detection technologies, expanding the market.

Key Restraints:

Limited Access to Advanced Neuroimaging in Developing Regions Hinders Market Progress

The availability of high-resolution neuroimaging technologies such as CT and MRI remains restricted in low- and middle-income countries due to inadequate healthcare infrastructure, high equipment costs, and a shortage of trained professionals. These imaging systems require significant investment in installation, maintenance, and operational expertise, making them financially unfeasible for many healthcare facilities in developing regions. Additionally, the lack of widespread insurance coverage and government funding for advanced diagnostic procedures further limits accessibility.

In rural and remote areas, patients often experience delays in diagnosis and treatment due to the unavailability of neuroimaging facilities. Many patients must travel long distances to specialized hospitals, increasing the risk of complications such as hematoma expansion or neurological deterioration. Furthermore, the shortage of skilled radiologists in these regions leads to increased dependence on general practitioners, who may lack the expertise to accurately interpret neuroimaging scans.

These challenges in accessibility and affordability restrict the widespread trend of advanced intracranial hemorrhage diagnosis and treatment solutions, limiting market growth, particularly in resource-constrained settings.

Future Opportunities:

Development of Portable Imaging Devices for Emergency Diagnosis Opens New Doors

Advancements in medical imaging are leading to the development of portable CT and MRI systems designed for emergency and point-of-care settings. These devices will enable rapid diagnosis of intracranial hemorrhages in ambulances, emergency rooms, stroke units, and remote healthcare facilities, significantly improving early intervention and patient survival rates. Portable imaging solutions will be particularly beneficial in underdeveloped healthcare regions, military medical units, and disaster response teams where access to traditional imaging systems is limited.

Companies such as Hyperfine are pioneering the development of low-cost, transportable MRI systems, which provide real-time brain imaging in non-traditional medical environments. These devices operate with lower power consumption and require minimal infrastructure, making them suitable for use in rural and emergency settings. Additionally, technological advancements in compact ultrasound-based brain monitoring tools are emerging as alternatives for rapid intracranial hemorrhage screening in pre-hospital scenarios.

The growing focus on portable diagnostic technologies will enhance access to intracranial hemorrhage detection, reduce diagnostic delays, and create new opportunities for intracranial hemorrhage diagnosis and treatment market expansion by addressing the unmet need for point-of-care neuroimaging solutions.

Intracranial Hemorrhage Diagnosis and Treatment Market Segmental Analysis :

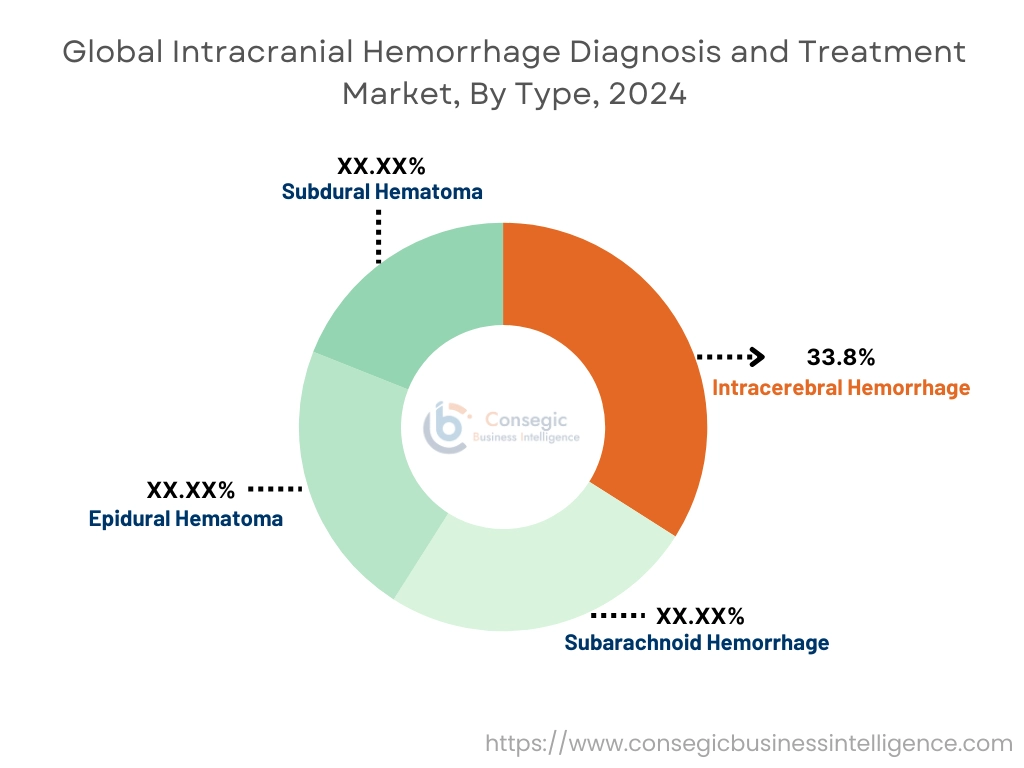

By Type:

Based on type, the intracranial hemorrhage diagnosis and treatment market is segmented into intracerebral hemorrhage, subarachnoid hemorrhage, epidural hematoma, and subdural hematoma.

The intracerebral hemorrhage segment accounted for the largest revenue of 33.8% in intracranial hemorrhage diagnosis and treatment market share in 2024.

- Intracerebral hemorrhage is a severe medical condition characterized by bleeding within the brain tissue.

- Hypertension, trauma, aneurysms, and vascular abnormalities are the primary causes of this condition.

- Advanced imaging techniques such as CT and MRI scans enable accurate and timely diagnosis, ensuring effective treatment.

- Increased prevalence of hypertension and lifestyle disorders has led to a higher incidence of intracerebral hemorrhages.

- Ongoing research and development efforts in treatment methods and surgical interventions support the new intracranial hemorrhage diagnosis and treatment market opportunities of this segment.

- Therefore, according to intracranial hemorrhage diagnosis and treatment market analysis, these factors contribute to the dominance of intracerebral hemorrhage in the market.

The subarachnoid hemorrhage segment is anticipated to register the fastest CAGR during the forecast period.

- Subarachnoid hemorrhage occurs due to bleeding in the space between the brain and the thin tissues covering it.

- Aneurysm rupture, head trauma, or arteriovenous malformations are the major causes of this condition.

- The increasing number of cases linked to lifestyle diseases and high-stress environments is driving the growth for early diagnosis and treatment.

- The trend of advanced neuroimaging techniques enhances the identification and management of subarachnoid hemorrhages.

- Thus, according to intracranial hemorrhage diagnosis and treatment market analysis, these factors contribute to the rapid expansion of the subarachnoid hemorrhage segment.

By Diagnosis:

Based on diagnosis, the market is segmented into computed tomography (CT), magnetic resonance imaging (MRI), and others.

The computed tomography (CT) segment accounted for the largest revenue share in 2024.

- CT scans are widely used for their ability to quickly and accurately detect bleeding within the brain.

- This imaging technique offers high-resolution images, facilitating early diagnosis and effective treatment.

- It is the preferred diagnostic tool in emergency settings due to its rapid imaging capabilities.

- Increasing trend for point-of-care diagnostics and advancements in imaging technology further enhance its market position.

- Therefore, according to the market analysis, these aspects drive the prominence of the CT segment.

The magnetic resonance imaging (MRI) segment is anticipated to register the fastest CAGR during the forecast period.

- MRI provides detailed images of soft tissues and vascular structures, making it effective in detecting even small hemorrhages.

- It is highly beneficial for identifying underlying causes of hemorrhages, such as vascular malformations or tumors.

- Technological advancements, including AI-driven imaging solutions, improve diagnostic accuracy and efficiency.

- Growing investments in healthcare infrastructure and the increasing prevalence of neurological disorders contribute to intracranial hemorrhage diagnosis and treatment market expansion.

- Thus, according to the market analysis, these factors support the rapid growth of the MRI segment.

By Treatment:

Based on treatment, the market is segmented into medication and surgery. The medication segment is further classified into anti-hypertensive drugs, coagulants, and others.

The medication segment accounted for the largest revenue in intracranial hemorrhage diagnosis and treatment market share in 2024.

- Medications such as anti-hypertensive drugs and coagulants play a crucial role in stabilizing patients and preventing further bleeding.

- Anti-hypertensive drugs help control blood pressure, reducing the risk of recurrent hemorrhages.

- Coagulants assist in promoting clot formation and preventing excessive blood loss.

- The rising prevalence of hypertension and blood disorders increases the trend for these medications.

- Therefore, according to the market analysis, these factors reinforce the dominance of the medication segment.

The surgery segment is anticipated to register the fastest CAGR during the forecast period.

- Surgical interventions such as craniotomy and hematoma evacuation are necessary for severe cases of intracranial hemorrhage.

- Advances in neurosurgical techniques, including minimally invasive procedures, improve patient outcomes and recovery rates.

- Increasing awareness and availability of specialized neurosurgical centers drive intracranial hemorrhage diagnosis and treatment market trend.

- The growing number of patients requiring immediate surgical intervention contributes to segmental growth.

- Thus, according to the market analysis, these factors accelerate the expansion of the surgery segment.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

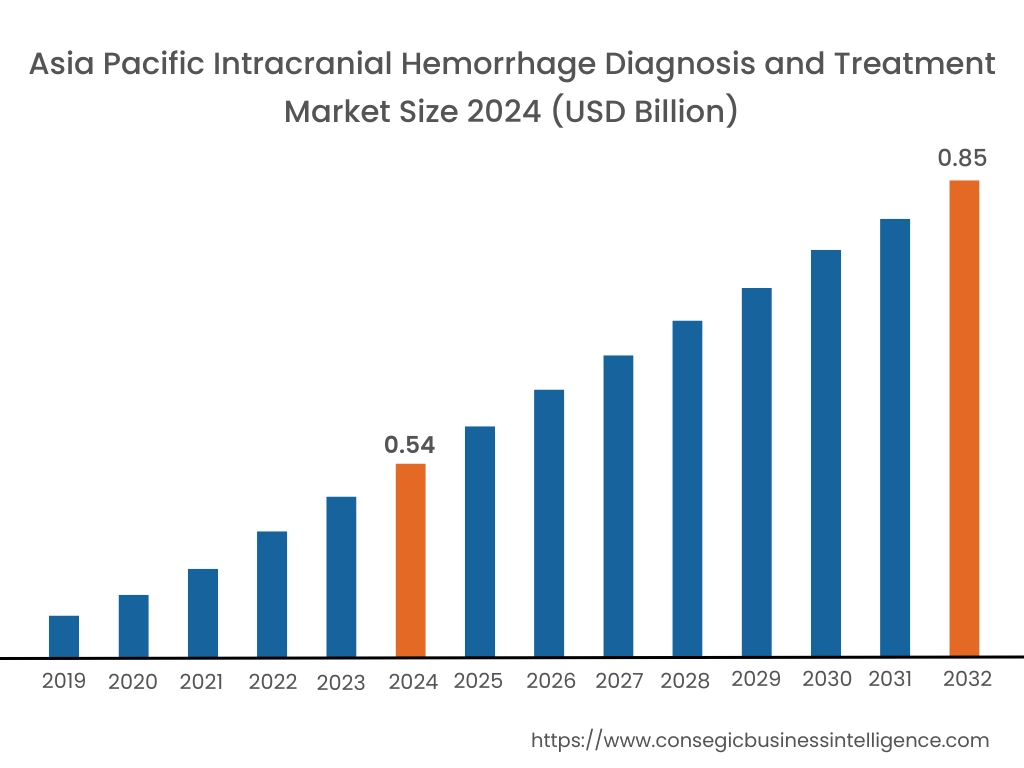

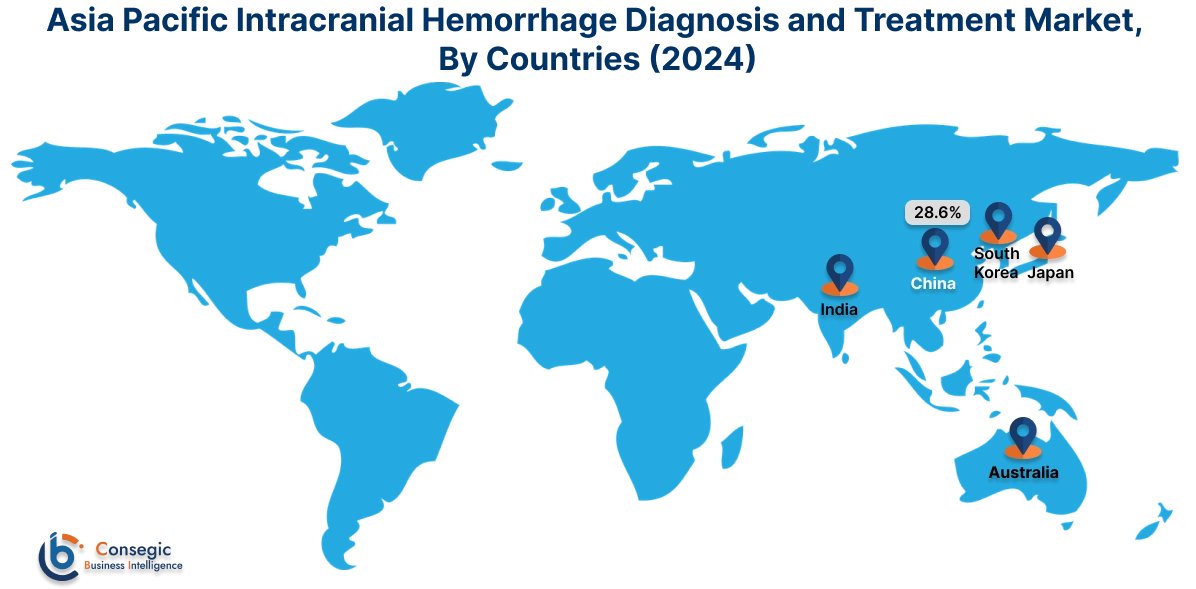

In 2024, Asia Pacific was valued at USD 0.54 Billion and is expected to reach USD 0.85 Billion in 2032. In Asia Pacific, China accounted for the highest share of 28.6% during the base year of 2024. Asia-Pacific exhibits increasing demand for intracranial hemorrhage diagnosis and treatment due to rising cases of stroke, high blood pressure, and head trauma. Expanding healthcare investments in China, India, and Japan support intracranial hemorrhage diagnosis and treatment market opportunities. Governments are implementing stroke awareness programs, improving early diagnosis and treatment rates. Advancements in medical imaging, including AI-assisted diagnostic tools, are enhancing detection accuracy. The growing number of multispecialty hospitals equipped with neurocritical care units affects treatment availability. Increasing medical tourism in countries such as Thailand and Singapore influences the demand for high-end diagnostic services. Regulatory agencies, including China’s NMPA and India’s CDSCO, impact the approval process for medical devices and treatments. High costs associated with advanced imaging technologies create affordability challenges for certain patient demographics. Partnerships between global healthcare firms and regional hospitals improve market penetration.

In 2024, North America was valued at USD 0.61 Billion and is expected to reach USD 0.90 Billion in 2032. The Intracranial Hemorrhage Diagnosis and Treatment market in North America is influenced by well-developed healthcare infrastructure and the presence of leading medical device manufacturers. The rising incidence of traumatic brain injuries, strokes, and hypertension-related hemorrhages contributes to intracranial hemorrhage diagnosis and treatment market demand. The region benefits from extensive reimbursement policies, making advanced diagnostic imaging and surgical treatments more accessible to patients. Technological advancements in imaging modalities, including CT and MRI, improve early detection rates. Increased funding for neurological research enhances innovation in treatment options. The growing trend of artificial intelligence in neurodiagnostic imaging impacts intracranial hemorrhage diagnosis and treatment market opportunities. Regulatory oversight by the FDA affects product approval timelines and commercialization. The presence of specialized stroke centers and neurology hospitals strengthens treatment accessibility. Collaborations between research institutions and biotechnology firms contribute to the development of novel therapies.

Europe's market performance is shaped by a well-established healthcare system and stringent regulatory policies under the European Medicines Agency (EMA). The high prevalence of neurovascular disorders, including intracranial hemorrhage, influences market demand. Government-funded healthcare programs facilitate access to diagnostic imaging and neurosurgical interventions. Increasing research on minimally invasive surgical techniques enhances treatment effectiveness. Leading medical device manufacturers, particularly in Germany, the UK, and France, contribute to market expansion. The presence of advanced stroke care centers strengthens the region’s diagnostic capabilities. Integration of AI in radiology and imaging systems enhances the accuracy of hemorrhage detection. Reimbursement policies under national healthcare systems influence patient access to diagnostic and therapeutic solutions. Strict regulatory requirements for new medical devices impact the commercialization timeline. Increasing elderly populations in European countries contribute to higher rates of stroke-related hemorrhages, affecting intracranial hemorrhage diagnosis and treatment market growth.

The Intracranial Hemorrhage Diagnosis and Treatment market in the Middle East and Africa is driven by improving healthcare infrastructure and growing awareness of neurological conditions. Governments are investing in modernizing hospital facilities, leading to the trend of advanced imaging technologies. Countries such as the UAE and Saudi Arabia are expanding specialized neurology departments in major hospitals. The increasing burden of stroke cases due to lifestyle-related conditions, including hypertension and diabetes, impacts market demand. Limited access to neurosurgical specialists and high-end imaging equipment in rural areas affects treatment accessibility. Collaborations with global medical technology firms facilitate the availability of advanced diagnostic solutions. Regulatory challenges and limited healthcare funding in certain regions slow down market expansion. International partnerships with academic institutions and research centers improve clinical training and diagnostic capabilities. The adoption of AI-driven imaging solutions is gradually increasing in major metropolitan hospitals.

The Latin American market for intracranial hemorrhage diagnosis and treatment is influenced by increasing cases of stroke and traumatic brain injuries. The expansion of private healthcare facilities in Brazil, Mexico, and Argentina supports intracranial hemorrhage diagnosis and treatment market growth. Government initiatives promoting stroke prevention and treatment programs affect diagnostic adoption rates. The availability of high-end medical imaging equipment remains limited in public healthcare settings, impacting early detection. Rising investments in telemedicine and AI-integrated diagnostic imaging contribute to market advancement. Economic constraints affect the affordability of specialized neurological treatments. Regulatory policies established by agencies such as ANVISA (Brazil) and COFEPRIS (Mexico) influence medical device approvals. The growing number of neurology-focused hospitals and research institutions enhances treatment accessibility. Increasing awareness about stroke symptoms and the importance of early intervention affects demand for diagnostic services. International collaborations between regional hospitals and global medical technology firms facilitate access to cutting-edge imaging solutions.

Top Key Players & Market Share Insights:

The global intracranial hemorrhage diagnosis and treatment market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (r&d), product innovation, and end-user launches to hold a strong position in the global intracranial hemorrhage diagnosis and treatment market. Key players in the intracranial hemorrhage diagnosis and treatment industry include-

- Siemens Healthineers [Germany]

- GE HealthCare [USA]

- Integra LifeSciences Corporation [USA]

- Edwards Lifesciences Corporation [USA]

- Penumbra, Inc. [USA]

- Philips Healthcare [Netherlands]

- Medtronic plc [Ireland]

- Canon Medical Systems Corporation [Japan]

- Stryker Corporation [USA]

- Nihon Kohden Corporation [Japan]

Recent Industry Developments :

Partnerships & Collaborations:

- In December 2024, according to PLOS Journal, the INTERACT3 Study Collaboration (2017–2021) took place. The Intensive Care Bundle with Blood Pressure Reduction in Acute Cerebral Hemorrhage Trial (INTERACT3) was a large-scale, international collaboration involving 121 hospitals across nine low- and middle-income countries and one high-income country. This study demonstrated that a multifaceted care bundle, including protocols for managing physiological variables, significantly improved functional recovery in patients with acute intracerebral hemorrhage.

- In December 2024, according to Chinese Neurosurgical Journal by BMC, the Emergency Neurosurgical Hybrid Operating Platform (E-HOPE) Initiative (2019–2023) took place. This initiative involved a collaboration among neurosurgical centers to develop and implement a hybrid operating platform integrating traditional neurosurgery with endovascular therapy capabilities. The platform aimed to enhance the diagnosis and treatment of acute complex intracranial hemorrhages, leading to improved patient outcomes.

- In April 2024, World Stroke Organization and American Heart Association co-hosted a webinar titled "Current Strategies and Challenges for Intracerebral Hemorrhage," focusing on recent advances in diagnosis, treatment, and prevention of intracerebral hemorrhage. The event highlighted the importance of rapid triaging, multispecialty care plans, and appropriate neuroimaging to improve patient outcomes.

Intracranial Hemorrhage Diagnosis and Treatment Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 2.79 Billion |

| CAGR (2025-2032) | 5.3% |

| By Type |

|

| By Diagnosis |

|

| By Treatment |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Intracranial Hemorrhage Diagnosis and Treatment Market? +

In 2024, the Intracranial Hemorrhage Diagnosis and Treatment Market was USD 1.85 Billion.

What will be the potential market valuation for the Intracranial Hemorrhage Diagnosis and Treatment Market by 2032? +

In 2032, the market size of Intracranial Hemorrhage Diagnosis and Treatment Market is expected to reach USD 2.79 Billion.

What are the segments covered in the Intracranial Hemorrhage Diagnosis and Treatment Market report? +

The type, diagnosis and treatment are the segments covered in this report.

Who are the major players in the Intracranial Hemorrhage Diagnosis and Treatment Market? +

Siemens Healthineers [Germany], GE HealthCare [USA], Philips Healthcare [Netherlands], Medtronic plc [Ireland], Canon Medical Systems Corporation [Japan], Stryker Corporation [USA], Nihon Kohden Corporation [Japan], Integra LifeSciences Corporation [USA], Edwards Lifesciences Corporation [USA], Penumbra, Inc. [USA] are the major players in the Intracranial Hemorrhage Diagnosis and Treatment market.