- Summary

- Table Of Content

- Methodology

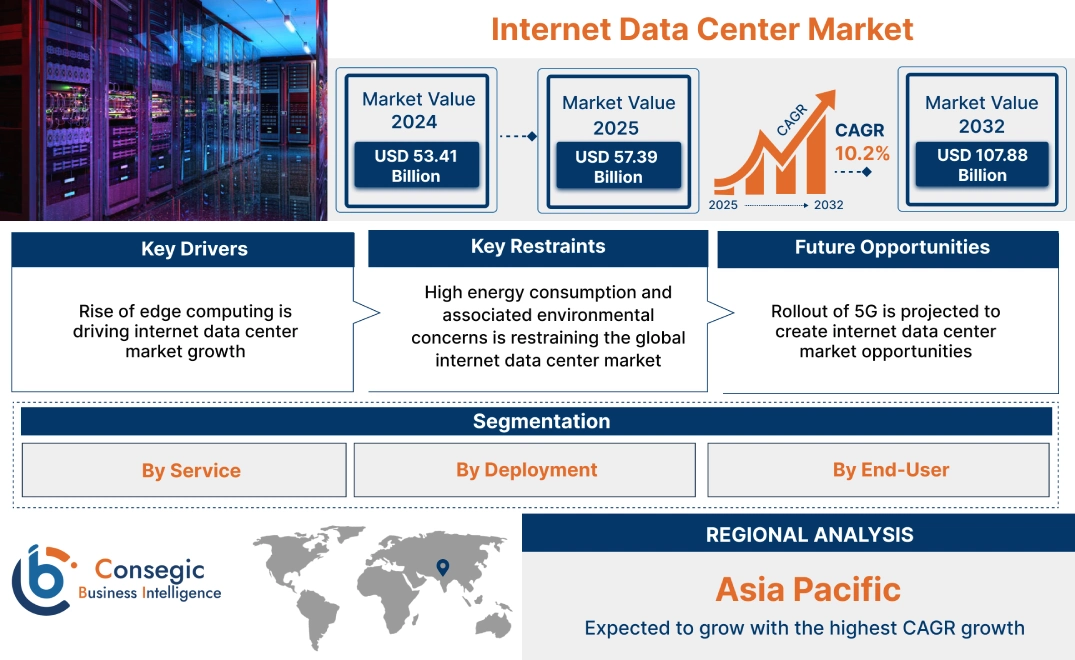

Internet Data Center Market Size:

Internet Data Center Market Size is estimated to reach over USD 107.88 Billion by 2032 from a value of USD 53.41 Billion in 2024 and is projected to grow by USD 57.39 Billion in 2025, growing at a CAGR of 10.2% from 2025 to 2032.

Internet Data Center Market Scope & Overview:

Internet Data Center (IDC), commonly referred to as a data center, is a physical facility that houses critical IT infrastructure, including servers, storage systems, and networking equipment. It serves as the backbone for storing, processing, and distributing vast amounts of data that support internet-based services and applications. These centers are essential for ensuring the reliable and continuous operation of websites, cloud services, and various online platforms, providing the necessary power, cooling, and security to maintain optimal performance.

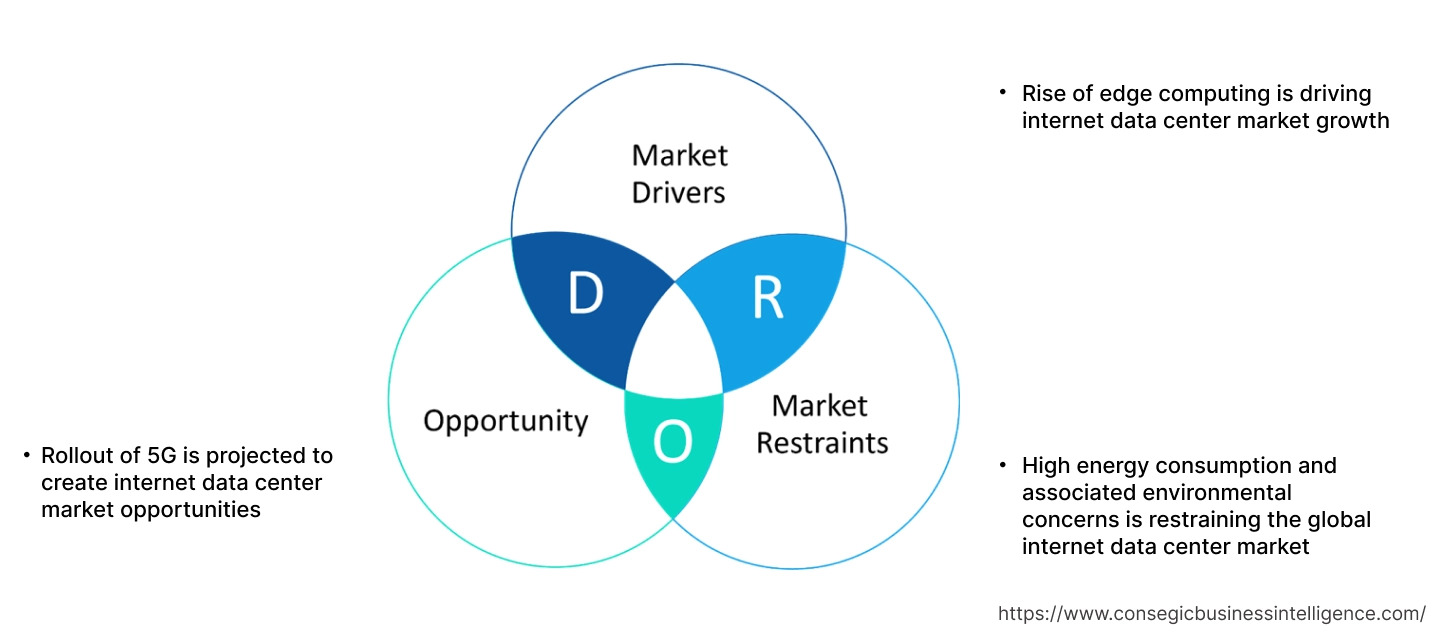

Internet Data Center Market Dynamics - (DRO):

Key Drivers:

Rise of edge computing is driving internet data center market growth

Edge computing minimizes delays by processing data near its origin, essential for real-time applications such as autonomous vehicles, gaming, and industrial automation. This requires distributed data centers located at network edges, leading to increased need for smaller, localized IDCs. Additionally, the proliferation of IoT devices and the rise of applications requiring instant data processing are fueling the need for edge computing, which in turn creates a demand for edge data centers to handle these real-time requirements, hence boosting the internet data center market trend.

- For instance, according to Institute for Operations Research and the Management Sciences (INFORMS) the global spending on edge computing is set for substantial growth. In 2024, worldwide expenditure is projected to climb by 15.4%, reaching USD 232 billion. Furthermore, this trend is expected to continue, with spending nearing USD 350 billion by 2027.

Consequently, growth of edge computing is driving the internet data center market expansion.

Key Restraints:

High energy consumption and associated environmental concerns is restraining the global internet data center market

Data centers face increasing operational costs due to high energy consumption and rising electricity prices. Moreover, they are subject to increasing pressure to reduce their environmental footprint including complying with stricter government regulations and meeting public/investor demands for sustainable practices. This necessitates substantial investments in energy-efficient technologies and renewable energy, thereby restraining the global internet data center market size.

Therefore, as per the analysis, these combined factors are significantly hindering internet data center market expansion.

Future Opportunities:

Rollout of 5G is projected to create internet data center market opportunities

5G's high bandwidth and low latency capabilities will enable a surge in data traffic including data generated by IoT devices, streaming services, and other bandwidth-intensive applications. IDCs are essential for storing, processing, and distributing this massive influx of data. In addition, 5G's low latency is critical for real-time applications like autonomous vehicles, augmented reality (AR), and virtual reality (VR). These applications require immediate data processing, driving the need for edge data centers and high-performance IDCs, thus boosting the internet data center market demand.

- For instance, according to IBEF, there is a significant surge in India's 5G users, jumping from 290 million in 2024 to 770 million by 2028, a 2.65-fold increase. This growth is fuelled by the rising popularity of Fixed Wireless Access (FWA), which has driven average 5G data consumption to 40 GB per user monthly.

Hence, based on the analysis, rollout of 5G is expected to create internet data center market opportunities.

Internet Data Center Market Segmental Analysis :

By Service:

Based on the service, the market is categorized into hosting, colocation, CDN, and others.

Trends in the Service:

- Growing trend towards the adoption of hosting services to facilitate seamless integration with hybrid cloud environments, enabling businesses to manage workloads across on-premises and cloud platforms.

- Increased use of automation for infrastructure management, improving efficiency and reducing downtime.

Colocation accounted for the largest revenue share in 2024.

- The increasing need for high-density computing is driving colocation providers to adopt liquid cooling, as traditional air cooling becomes insufficient, a key factor in driving the internet data center market share.

- Additionally, to achieve faster deployment, providers are leveraging modular designs, offering prefabricated, containerized data center modules that are both quickly deployable and highly customizable.

- Moreover, to optimize infrastructure management, colocation providers are deploying AI and machine learning, enabling advancements in power consumption, cooling efficiency, and security.

- For instance, in Jan 2025, Flexential announced to provide ground support for Lonestar Data Holdings' lunar data center project. The company will offer colocation, interconnection, and professional services, including backup and disaster recovery from their Tampa facility.

- Thus, as per the internet data center market analysis, the aforementioned factors are driving the colocation segment.

CDN is predicted to register the fastest CAGR during the forecast period.

- CDNs are expanding their edge infrastructure to further reduce latency and improve content delivery for real-time applications, thereby driving the internet data center market share.

- CDNs are implementing advanced security measures to protect against DDoS attacks and other cyber threats, hence driving the internet data center market size.

- CDNs are being optimized to support the high bandwidth and low latency requirements of 5G networks.

- The increased need of streaming video, and other high bandwidth content, increases the demand for CDN services.

- Consequently, the aforementioned factors are driving the CDN segment growth during the forecast period.

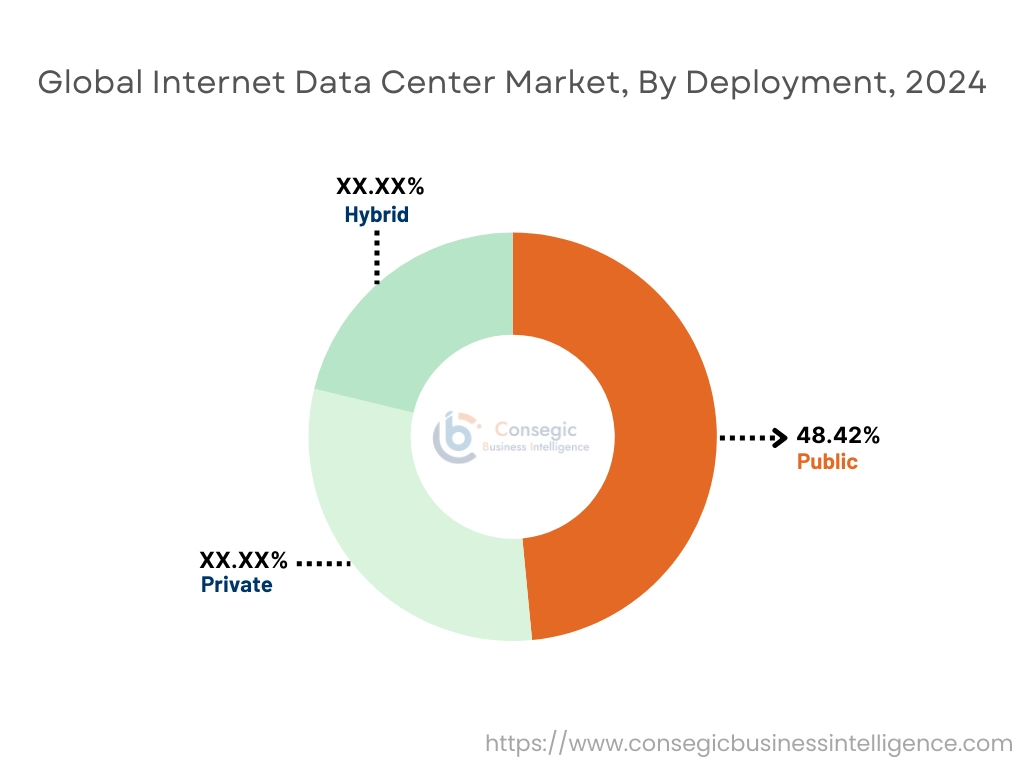

By Deployment:

Based on the deployment, the market is classified into public, private, and hybrid.

Trends in the Deployment:

- Organizations in highly regulated industries, such as finance and healthcare, are deploying private cloud IDCs to maintain control over their data.

- The need for low-latency applications is driving the deployment of edge private clouds, bringing data processing closer to the source.

Public accounted for the largest revenue share of 48.42% in 2024.

- Small and medium-sized enterprises (SMEs) are leveraging public cloud IDCs for their scalability and cost-effectiveness, driving internet data center market trend.

- The rise of serverless computing, which eliminates the need to manage infrastructure, is driving need for public cloud IDCs.

- Moreover, major public cloud providers are expanding their global footprint, establishing new data centers to cater to regional needs and data sovereignty requirements.

- Furthermore, public cloud IDCs are preferred platform for AI and machine learning workloads due to their high-performance computing capabilities and scalability, which is further driving the internet data center market demand.

- For instance, in July 2024, Cloudera launched new features for its Observability Premium service, aiming to streamline data platform management. Specifically, "Cloudera Observability Premium for Public Cloud Data Hub" brings enhanced monitoring, financial control, automation, and data oversight to users of Cloudera's public cloud services in data centers.

- Thus, as per the internet data center market analysis, the aforementioned factors are driving the public cloud segment.

Hybrid is predicted to witness the fastest growth during the forecast period.

- Hybrid cloud is becoming a significant deployment model, allowing organizations to leverage the benefits of both public and private clouds.

- Organizations are using hybrid cloud to optimize workloads, placing sensitive data in private clouds and less sensitive data in public clouds.

- Emphasis is placed on seamless integration between public and private cloud environments, enabling data and application portability.

- Hybrid cloud is being used for disaster recovery and business continuity, providing redundancy and resilience.

- For instance, in March 2025, Red Hat enhanced its AI offerings, called Red Hat AI, to streamline the creation and deployment of AI applications across various data center environments. The updated platform focuses on improving efficiency and ease of use, allowing businesses to flexibly run AI models anywhere within their hybrid cloud setup.

- Therefore, the aforementioned factors are contributing notably in spurring the market growth.

By End-User:

Based on the end user, the market is categorized into telecom, government/public sector, BFSI, media & entertainment, e-commerce & retail, and others.

Trends in End User:

- Governments are prioritizing data sovereignty and security, leading to the deployment of private or government-controlled IDCs.

- BFSI institutions face strict regulatory requirements, necessitating highly secure and compliant IDCs.

Telecom accounted for the largest revenue share in the market in 2024.

- Telecom companies are heavily investing in IDCs to support the rollout of 5G networks and edge computing deployments, is driving the market trend.

- Telecom providers are using IDCs to virtualize network functions, enabling greater flexibility and scalability.

- Moreover, the surge in mobile data consumption and streaming services is driving need for IDCs to manage and process vast amounts of data.

- In conclusion, the aforementioned benefits are bolstering the global internet data center market.

E-commerce & Retail are predicted to register the fastest CAGR during the forecast period.

- E-commerce companies require scalable IDCs to handle peak demand during sales events and seasonal fluctuations.

- Retailers are using IDCs to store and analyze customer data, enabling personalized marketing and recommendations.

- Use of AI and data analytics for demand forecasting, inventory management, and logistics optimization is also driving the internet data center market expansion.

- Furthermore, the integration of online and offline retail channels is driving need for IDCs to support omnichannel strategies, driving the market trend.

- For instance, India's retail sector is experiencing robust progress, evidenced by the opening of over 750 new stores and a substantial Rs. 12,000 crore (USD 1.38 billion) in funding in 2024. The overall market is projected to reach USD 1.6 trillion by 2026, with a 10% CAGR. Modern trade is expected to lead this expansion, growing at 20% annually, while traditional trade will witness a 10% growth rate.

- In conclusion, the above-mentioned factors are contributing significantly in propelling the market.

Regional Analysis:

The global internet data center market has been classified by region into North America, Europe, Asia-Pacific, MEA, and Latin America.

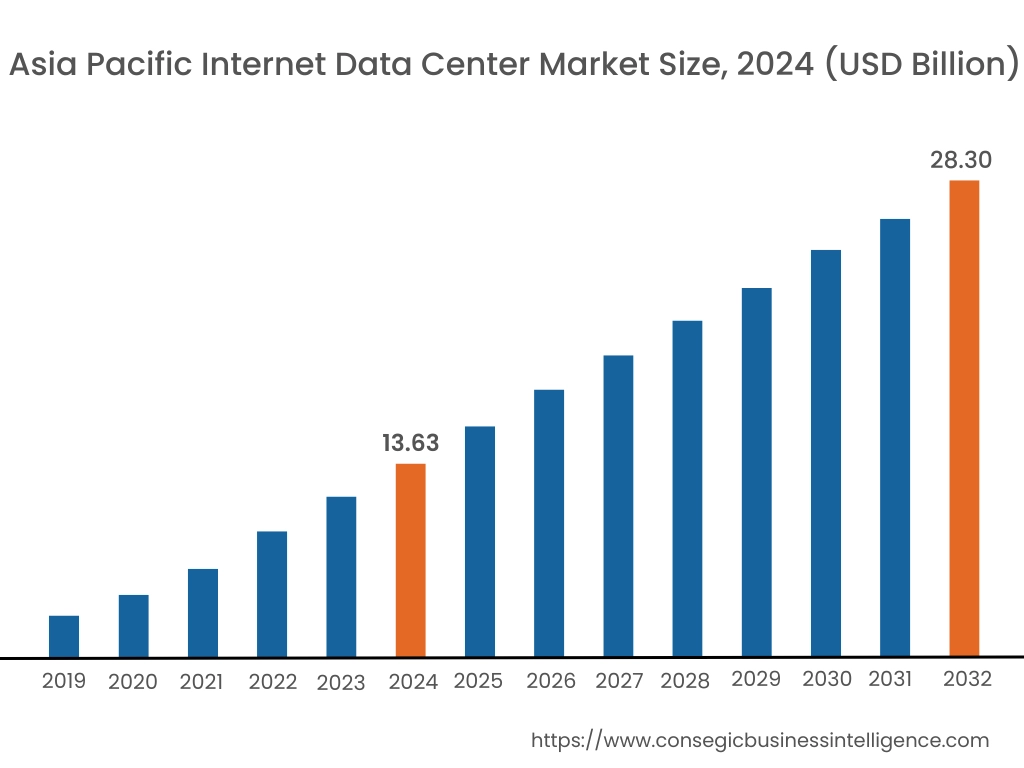

Asia Pacific region was valued at USD 13.63 Billion in 2024. Moreover, it is projected to grow by USD 14.68 Billion in 2025 and reach over USD 28.30 Billion by 2032. Out of these, China accounted for the largest revenue share of 31.99% in 2024. Businesses across APAC are rapidly adopting digital technologies, driving need for robust data center infrastructure. Additionally, the widespread deployment of 5G networks and the proliferation of IoT devices are generating enormous data volumes, necessitating advanced IDC solutions. Moreover, the region's thriving e-commerce sector, with its massive online retail and marketplace activity, requires significant data storage and processing capabilities.

- For instance, according to IBEF, India's e-commerce sector is booming, with projections indicating a market value of USD 325 billion by 2030 and a surge to 17 billion shipments handled by logistics providers within seven years. The sector's strong performance was further highlighted by USD 14 billion GMV during the 2024 festive season, demonstrating a 12% year-over-year increase.

North America was valued at USD 19.41 Billion in 2024. Moreover, it is projected to grow by USD 20.84 Billion in 2025 and reach over USD 38.93 Billion by 2032.

The increasing adoption of edge computing is driving the deployment of distributed data centers closer to end-users, particularly in densely populated areas. Additionally, regulations such as HIPPA, and other industry specific laws, increase the need for high levels of data security. Further major cloud providers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP) are continuously expanding their hyperscale data center footprint to meet the increasing need for cloud services, further driving the internet data center market trend.

- For instance, in March 2025, CIM Group and Novva Data Centers secured USD 2 billion in new funding to expand their network of sustainable and efficient data centers throughout the Western United States, aiming to accelerate their progress in the region.

As per the internet data center market analysis, European IDC market is experiencing steady development, driven by stringent data privacy regulations like GDPR, increasing cloud adoption, and a strong focus on sustainability. Additionally, Latin American IDC market is rapidly expanding, fueled by increasing internet penetration, growing e-commerce, and rising demand for cloud services. Moreover, Middle East and Africa IDC market is witnessing significant increase, driven by government initiatives promoting digital transformation, increasing smartphone penetration, and rising demand for cloud services.

Top Key Players & Market Share Insights:

The market is highly competitive with major players providing internet data center to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the internet data center industry include-

- Amazon Web Services (AWS) (United States)

- Microsoft Azure (United States)

- Google Cloud Platform (GCP) (United States)

- Sify Technologies (India)

- Tata Communications (India)

- Yotta Infrastructure (India)

- Cloudflare (United States)

- Vantage Data Centers (United States)

- Digital Realty (United States)

- Equinix (United States)

- NTT Global Data Centers (Japan)

- CyrusOne (United States)

- GDS Holdings (China)

- KDDI/Telehouse (Japan)

- CtrlS Datacenters (India)

Recent Industry Developments :

Product Enhancements:

- In Sep 2024, Juniper Networks upgraded its data center networking solutions by introducing new AI-powered, cloud-hosted services. These enhancements aim to improve network visibility, analysis, and automation, ultimately leading to better user experiences. The updates provide deeper insights into application performance, including those related to AI workloads, enabling continuous optimization and faster problem resolution within data center environments.

Internet Data Center Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 107.88 Billion |

| CAGR (2025-2032) | 10.2% |

| By Service |

|

| By Deployment |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the internet data center market? +

The internet data center market size is estimated to reach over USD 107.88 Billion by 2032 from a value of USD 53.41 Billion in 2024 and is projected to grow by USD 57.39 Billion in 2025, growing at a CAGR of 10.2% from 2025 to 2032.

What specific segmentation details are covered in the internet data center report? +

The internet data center report includes specific segmentation details for service, deployment, end user, and regions.

Which is the fastest segment anticipated to impact the market growth? +

In the internet data center market, hybrid is the fastest-growing segment during the forecast period.

Who are the major players in the internet data center market? +

The key participants in the internet data center market are Amazon Web Services (AWS) (United States), Microsoft Azure (United States), Google Cloud Platform (GCP) (United States), Digital Realty (United States), Equinix (United States), NTT Global Data Centers (Japan), CyrusOne (United States), GDS Holdings (China), KDDI/Telehouse (Japan), CtrlS Datacenters (India), Sify Technologies (India), Tata Communications (India), Yotta Infrastructure (India), Cloudflare (United States), Vantage Data Centers (United States), and Others.