- Summary

- Table Of Content

- Methodology

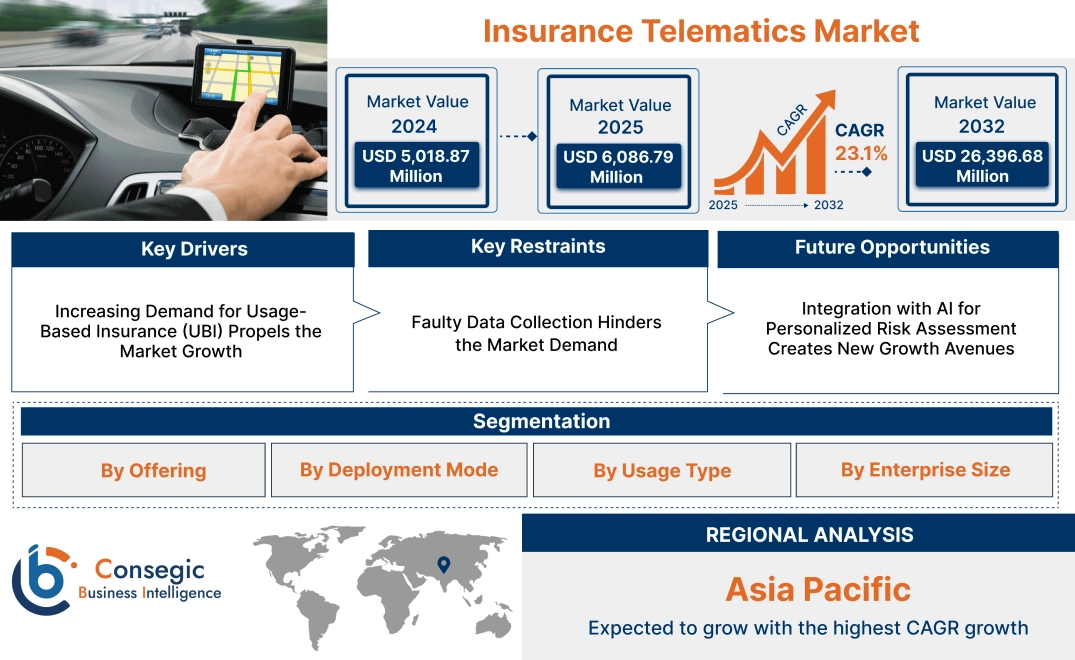

Insurance Telematics Market Size:

Insurance Telematics Market size is estimated to reach over USD 26,396.68 Million by 2032 from a value of USD 5,018.87 Million in 2024 and is projected to grow by USD 6,086.79 Million in 2025, growing at a CAGR of 23.1% from 2025 to 2032.

Insurance Telematics Market Scope & Overview:

Insurance telematics refers to the integration of telecommunication and data collection technologies into the insurance industry to monitor driving behavior and vehicle usage. This technology enables insurers to assess risk profiles more accurately by analyzing real-time data such as speed, mileage, braking patterns, and location. It is primarily used in automotive insurance to offer personalized policies based on driver behavior.

Telematics systems typically include onboard devices or mobile apps that gather data and transmit it to insurance providers for evaluation. These systems are equipped with GPS tracking, accelerometers, and advanced data analytics tools to ensure precise monitoring and reporting. The data collected is then utilized to develop usage-based insurance models, offering flexible premium structures and improved customer engagement.

End-users include insurance providers, fleet management companies, and individual vehicle owners seeking tailored insurance solutions. Insurance telematics plays a critical role in modernizing the insurance industry by enhancing data accuracy and enabling personalized policy offerings.

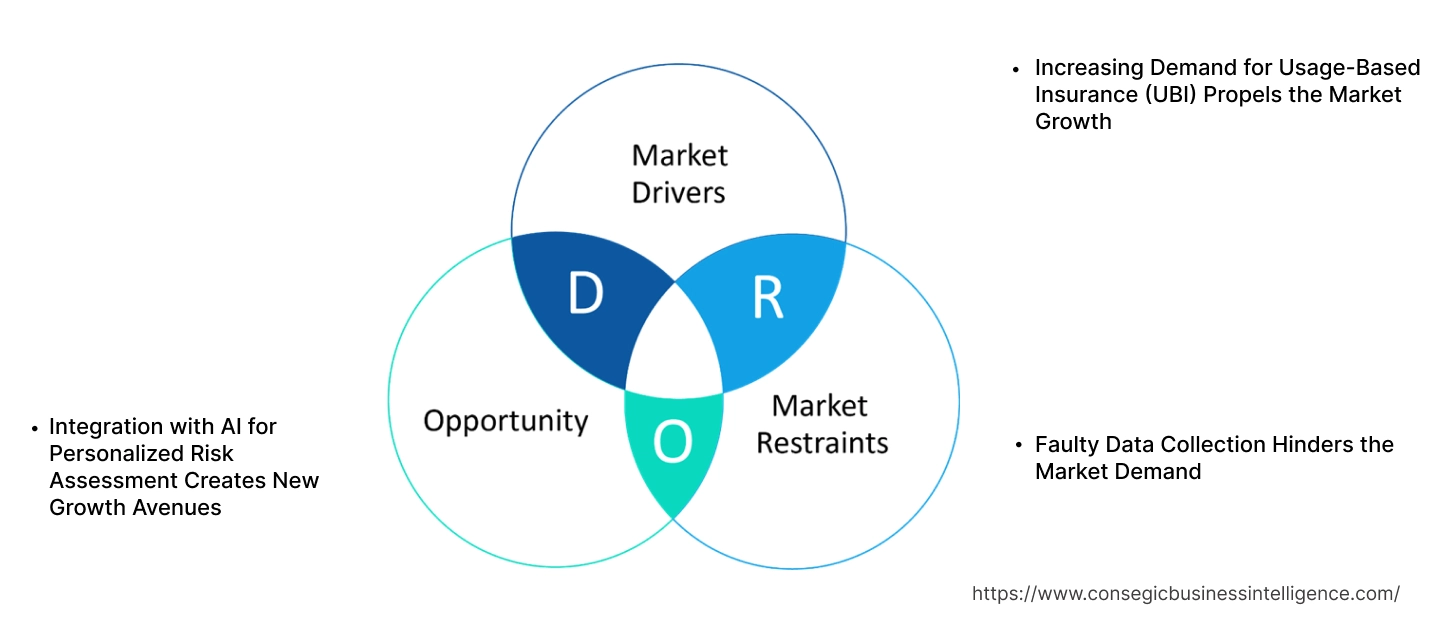

Insurance Telematics Market Dynamics - (DRO) :

Key Drivers:

Increasing Demand for Usage-Based Insurance (UBI) Propels the Market Growth

The growing demand for usage-based insurance (UBI) is a key driver for the adoption of telematics systems in the insurance industry. Consumers are increasingly looking for personalized and cost-effective policies that reflect their individual driving habits. Telematics devices track factors such as speed, braking, mileage, and time of day, enabling insurers to assess risk more accurately and adjust premiums based on actual driving behavior. Safe drivers benefits from discounts, which incentivize responsible driving and help reduce overall insurance costs. This approach offers greater fairness and transparency compared to traditional insurance models, where premiums are typically based on broad factors like age, location, and vehicle type. As consumers demand more tailored policies that align with their behavior, the adoption of telematics-based UBI continues to rise, driving insurance telematics market growth and offering insurers a competitive edge in the evolving insurance landscape.

Key Restraints:

Faulty Data Collection Hinders the Market Demand

One significant restraint in the adoption of telematics-based insurance is the potential for faulty data collection, which leads to inaccurate premium calculations. In some cases, telematics devices malfunction and collect incorrect data, such as continuing to count mileage after the vehicle has been turned off. This results in an inflated mileage count, which directly impacts the premium calculation and cause consumers to pay more than necessary. Inaccurate data on driving behavior, such as excessive speed or harsh braking, also affect the risk assessment, leading to mispriced policies. The reliance on the accuracy of collected data is essential for both consumers and insurers, and any discrepancies in data damages customer trust and hinders insurance telematics market demand. Effective calibration and regular maintenance of devices are crucial to minimizing these issues and ensuring the fairness of usage-based insurance models.

Future Opportunities :

Integration with AI for Personalized Risk Assessment Creates New Growth Avenues

The integration of artificial intelligence (AI) with telematics data offers a significant opportunity to enhance the personalization of insurance premiums. AI algorithms process vast amounts of real-time data from various sources, including driving habits, vehicle performance, weather conditions, and road types, to assess risk more accurately. By analyzing individual driving behaviors—such as speed, braking patterns, and mileage—AI enables insurers to offer highly tailored premiums that reflect the specific risk profile of each driver. This allows for fairer pricing, where safe drivers receive discounts and high-risk drivers are charged accordingly. Additionally, AI-powered models continuously learn and adapt based on new data, improving the accuracy of risk assessment over time. This personalized approach not only benefits consumers by offering more competitive rates but also helps insurers optimize their pricing strategies, reducing the likelihood of underpricing or overpricing policies. This innovation is expected to drive significant insurance telematics market opportunities.

Insurance Telematics Market Segmental Analysis :

By Offering:

Based on offering, the market is segmented into hardware and software.

The hardware segment accounted for the largest revenue of the total insurance telematics market share in 2024.

- Hardware components such as on-board diagnostic (OBD) devices, black boxes, and telematics sensors are critical for collecting real-time vehicle data, including speed, mileage, and driving behavior.

- These devices are widely adopted in commercial fleet operations and individual vehicles to support usage-based insurance (UBI) models.

- Continuous advancements in hardware, such as miniaturized sensors and integrated GPS modules, enhance their accuracy and efficiency, driving their adoption in the market.

- As per insurance telematics market analysis, hardware plays a key role in facilitating reliable data collection, ensuring the effective implementation of telematics-based insurance solutions.

The software segment is anticipated to grow at the fastest CAGR during the forecast period.

- Software platforms enable the processing, analysis, and visualization of telematics data, providing actionable insights for insurers and policyholders.

- Cloud-based software solutions allow insurers to access real-time data for risk assessment and personalized policy pricing, enhancing operational efficiency.

- The integration of advanced analytics tools, such as AI and machine learning, supports predictive modeling and accident risk forecasting, increasing the utility of telematics software.

- As per insurance telematics market trends, the adoption of user-friendly mobile applications for policyholders to track driving performance and manage policies is driving the rapid expansion of the software segment.

By Deployment Mode:

Based on deployment mode, the market is segmented into cloud-based and on-premise.

The cloud-based segment accounted for the largest revenue of the total insurance telematics market share in 2024.

- Cloud-based deployment offers insurers flexibility, scalability, and cost-effectiveness, making it the preferred choice for managing telematics data.

- Real-time data access and storage capabilities provided by cloud platforms enhance risk assessment, policy customization, and claims processing.

- Cloud-based solutions support seamless integration with third-party tools and applications, enabling insurers to expand their service offerings efficiently.

- The increasing focus on digital transformation in the insurance sector further supports the adoption of cloud-based solutions, fueling the Insurance Telematics Market demand.

The on-premise segment is anticipated to grow at the fastest CAGR during the forecast period.

- On-premise deployment is preferred by insurers with stringent data security and compliance requirements, particularly in regions with strict regulatory frameworks.

- These solutions offer complete control over data storage and processing, making them suitable for large insurance firms handling sensitive customer information.

- The segment benefits from technological advancements, including hybrid deployment models that combine on-premise and cloud capabilities for enhanced operational efficiency.

- As per insurance telematics market analysis, on-premise solutions continue to serve a niche market segment requiring high data control and customization.

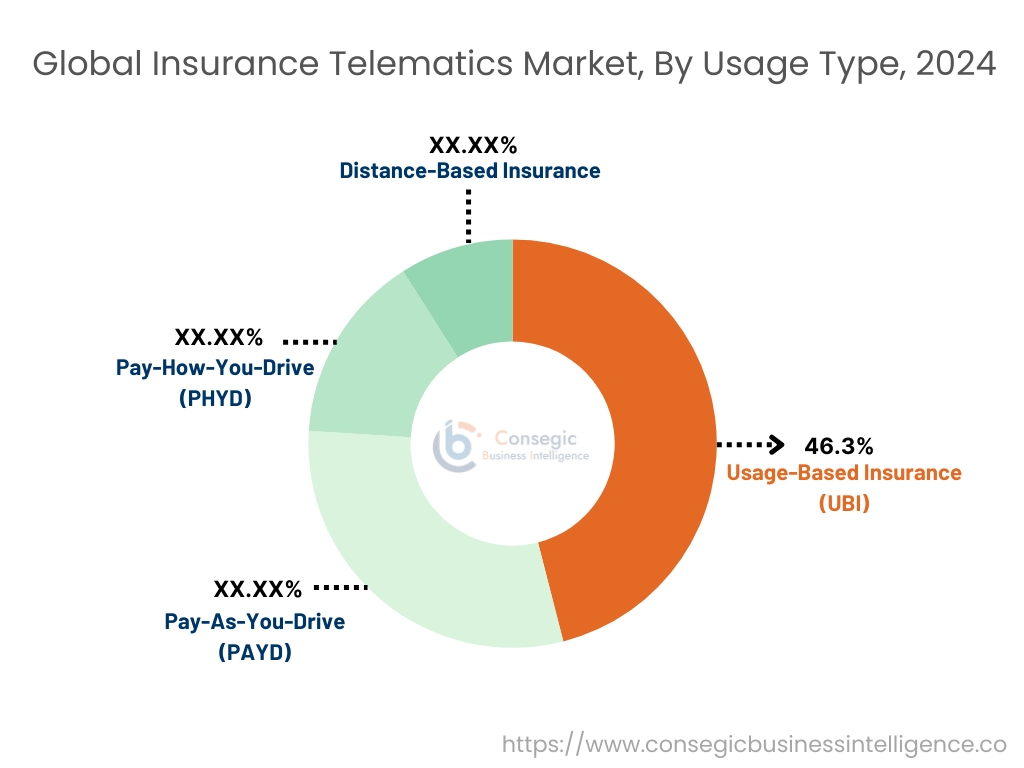

By Usage Type:

Based on usage type, the market is segmented into usage-based insurance (UBI), pay-as-you-drive (PAYD), pay-how-you-drive (PHYD), and distance-based insurance.

The usage-based insurance (UBI) segment accounted for the largest revenue of 46.3% share in 2024.

- UBI models leverage telematics data to assess driving behavior and vehicle usage, offering personalized premiums based on individual risk profiles.

- This segment is widely adopted by insurers as it incentivizes safe driving practices and helps reduce claim costs by aligning premiums with actual vehicle usage.

- The integration of UBI with advanced telematics systems supports real-time monitoring and proactive risk management, ensuring accurate policy pricing.

- As per insurance telematics market trends, UBI’s ability to provide cost savings and foster transparency between insurers and policyholders strengthens its dominance in the market.

The pay-how-you-drive (PHYD) segment is anticipated to grow at the fastest CAGR during the forecast period.

- PHYD models focus on evaluating driving behavior, such as braking, acceleration, and cornering, to determine insurance premiums.

- This segment benefits from advancements in telematics sensors and AI-driven analytics, enabling insurers to accurately assess driving performance.

- The rising emphasis on promoting safe driving habits and reducing road accidents drives the adoption of PHYD insurance models.

- Thus, the increasing use of PHYD in both individual and commercial fleet insurance highlights its growing importance in telematics-based solutions, contributing to the insurance telematics market expansion.

By Enterprise:

Based on enterprise size, the market is segmented into small-medium enterprises (SMEs) and large enterprises.

The large enterprises segment accounted for the largest revenue share in 2024.

- Large insurance firms adopt telematics solutions to streamline operations, improve risk assessment, and offer personalized insurance policies at scale.

- These enterprises leverage advanced telematics systems for managing vast volumes of data, supporting efficient claims processing and fraud detection.

- The availability of resources and infrastructure enables large enterprises to invest in cutting-edge telematics technologies, such as AI and IoT-based platforms.

- Thus, large insurance firms benefit from economies of scale and enhanced customer engagement through advanced telematics integration, fueling the insurance telematics market growth.

The small-medium enterprises (SMEs) segment is projected to grow at the fastest CAGR during the forecast period.

- SMEs are increasingly adopting cloud-based telematics solutions due to their affordability, scalability, and ease of implementation.

- These enterprises leverage telematics to enhance operational efficiency, reduce costs, and offer competitive insurance products in niche markets.

- User-friendly telematics platforms and subscription-based pricing models enable SMEs to adopt telematics without significant upfront investments.

- The growth in awareness of the benefits of telematics in improving customer satisfaction and policy customization drives the adoption of telematics among SMEs, boosting the insurance telematics market opportunities.

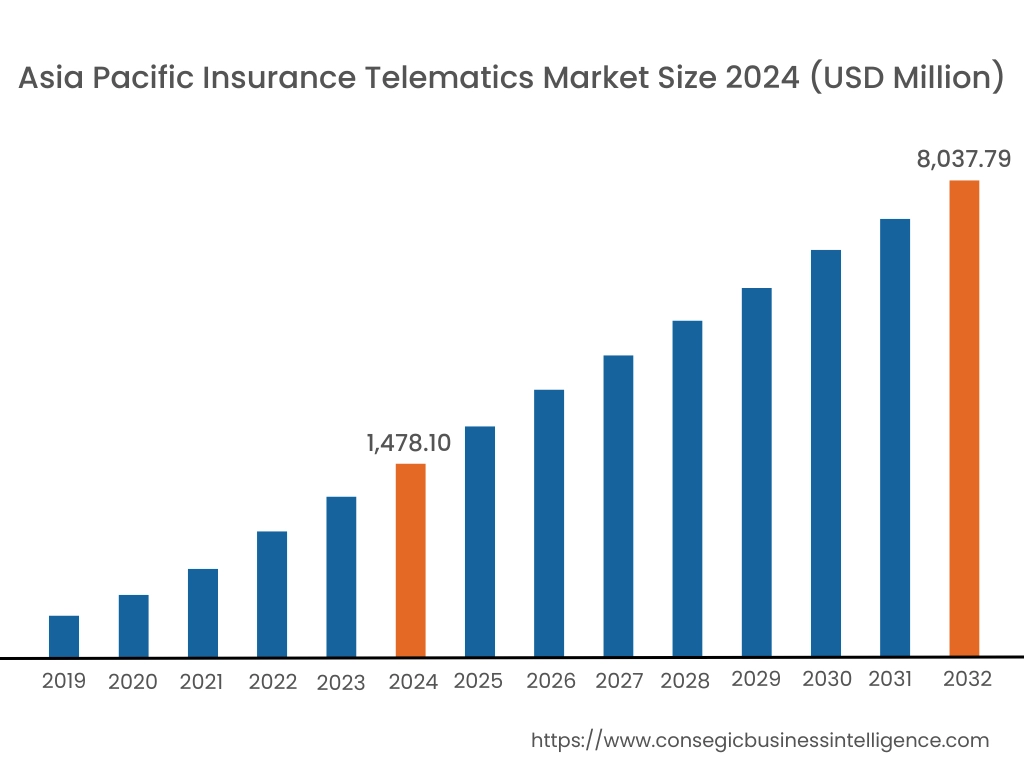

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

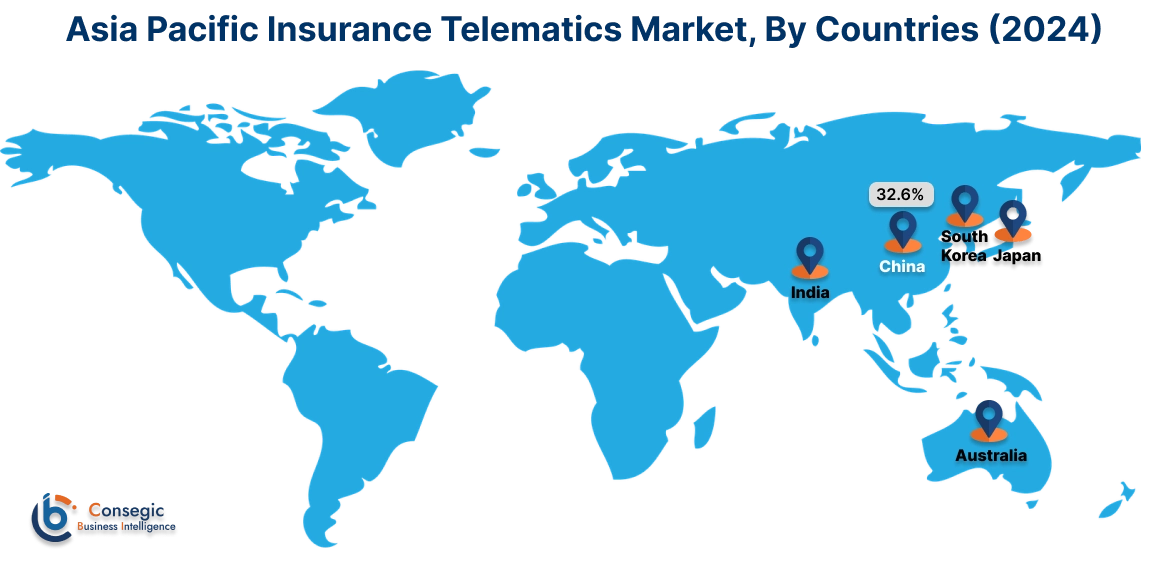

Asia Pacific region was valued at USD 1,478.10 Million in 2024. Moreover, it is projected to grow by USD 1,797.68 Million in 2025 and reach over USD 8,037.79 Million by 2032. Out of this, China accounted for the maximum revenue share of 32.6%. The Asia-Pacific region is witnessing rapid advancements in the insurance telematics market, attributed to increasing vehicle ownership and growing awareness of road safety. A prominent trend is the rising adoption of telematics-enabled insurance policies among fleet operators to monitor driver performance and optimize operational efficiency. Analysis indicates that supportive government policies and collaborations between insurers and telematics providers are contributing to insurance telematics market expansion in this region.

North America is estimated to reach over USD 8,555.16 Million by 2032 from a value of USD 1,664.80 Million in 2024 and is projected to grow by USD 2,015.18 Million in 2025. This region holds a prominent position in the insurance telematics sector, driven by the widespread adoption of connected vehicle technologies and a strong focus on driver safety. A notable trend is the increasing implementation of usage-based insurance (UBI) models, such as pay-as-you-drive and pay-how-you-drive programs, which leverage telematics data to offer personalized premiums. Analysis indicates that favorable regulatory policies and the presence of key industry players contribute to the market dynamics in North America.

European countries are pivotal in the insurance telematics market, emphasizing stringent road safety regulations and environmental sustainability. A significant trend is the integration of telematics systems to monitor driving behavior, aiming to reduce accidents and promote eco-friendly driving practices. Analysis suggests that government initiatives, such as the European Union's eCall mandate, which requires telematics devices in vehicles for emergency response, are driving the adoption of telematics-based insurance solutions in this region.

In the Middle East and Africa, the insurance telematics market is influenced by efforts to enhance road safety and manage traffic congestion. The focus is on utilizing telematics solutions to monitor driving behavior and implement risk-based insurance pricing. As per the market trends suggests that increasing awareness of the benefits of telematics and investments in smart transportation infrastructure are shaping the market landscape in these regions.

Latin American countries are increasingly recognizing the potential of insurance telematics in improving driver safety and reducing insurance fraud. A notable trend is the deployment of telematics devices to gather data on vehicle usage and driver habits, enabling insurers to offer customized policies. The market trends also indicates that economic development and the growth in penetration of connected vehicles are key factors influencing the market growth in this region.

Top Key Players and Market Share Insights:

The Insurance Telematics market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Insurance Telematics market. Key players in the Insurance Telematics industry include -

- Octo Telematics (Italy)

- Cambridge Mobile Telematics (USA)

- Redtail Telematics Corporation (UK)

- MiX Telematics (South Africa)

- IMS (Intelligent Mechatronic Systems) (Canada)

- The Floow Limited (UK)

- LexisNexis Risk Solutions (USA)

- Metromile, Inc. (USA)

- Driveway Software (USA)

Recent Industry Developments :

Partnerships & Collaborations:

- In November 2024, Samsara partnered with Northland Insurance to offer real-time telematics insights and specialized insurance coverage, helping fleets reduce risk, claims, and costs. Qualifying Northland customers can receive up to $300 per vehicle annually toward Samsara AI Dash Cams or a 10% insurance discount, along with tailored coverage and streamlined claims. By leveraging AI-based telematics to detect risky driving behaviors, this collaboration helps prevent accidents, improve fleet monitoring, and enhance driver safety, delivering significant cost savings and risk reduction.

- In October 2023, Howden Driving Data renewed its partnership with ANWB, continuing to provide the technology behind Drive Safe, a telematics-based pay-as-you-drive insurance product. This enables personalized risk-based premiums and driver coaching for safer driving habits. ANWB also leverages Howden’s Smart Beacon solution to analyze Dutch road network data, supporting 190+ road authorities in identifying high-risk areas.

Acquisitions & Mergers:

- In January 2024, Targa Telematics acquired Drive-it, an Israeli spin-off of Earnix, specializing in AI-driven driver behavior analysis. This move establishes Targa Drive, a UBI telematics solution designed to transform insurance risk assessment. Using machine learning, smartphone-based data collection, and predictive scoring, Targa Drive enables insurers to assess driving behavior, detect distractions, and refine risk models.

Product Launches:

- In September 2023, Definity launched Sonnet Shift, a usage-based insurance (UBI) product that adjusts premiums quarterly based on real-time driving scores. Available in Ontario, the program offers up to 35% savings for safe driving and a 10% discount for low mileage. Powered by The Floow telematics and Munich Re Global Consulting, Sonnet Shift analyzes driving habits such as speed, fatigue, and mobile distraction. Customers can track behavior 24/7 via an app, with projected discounts updated weekly.

Insurance Telematics Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 26,396.68 Million |

| CAGR (2025-2032) | 23.1% |

| By Offering |

|

| By Deployment Mode |

|

| By Usage Type |

|

| By Enterprise Size |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Insurance Telematics Market? +

The Insurance Telematics Market size is estimated to reach over USD 26,396.68 Million by 2032 from a value of USD 5,018.87 Million in 2024 and is projected to grow by USD 6,086.79 Million in 2025, growing at a CAGR of 23.1% from 2025 to 2032.

What are the key segments in the Insurance Telematics Market? +

The market is segmented by offering (hardware, software), deployment mode (cloud-based, on-premise), usage type (usage-based insurance, pay-as-you-drive, pay-how-you-drive, distance-based insurance), and enterprise size (small-medium enterprises, large enterprises).

Which segment is expected to grow the fastest in the Insurance Telematics Market? +

The pay-how-you-drive (PHYD) segment is anticipated to grow at the fastest CAGR during the forecast period, driven by advancements in telematics sensors and AI-driven analytics for accurate driving performance assessment.

Who are the major players in the Insurance Telematics Market? +

Key players in the Insurance Telematics Market include Octo Telematics (Italy), Cambridge Mobile Telematics (USA), The Floow Limited (UK), LexisNexis Risk Solutions (USA), Metromile, Inc. (USA), Driveway Software (USA), Redtail Telematics Corporation (UK), MiX Telematics (South Africa), IMS (Intelligent Mechatronic Systems) (Canada).