- Summary

- Table Of Content

- Methodology

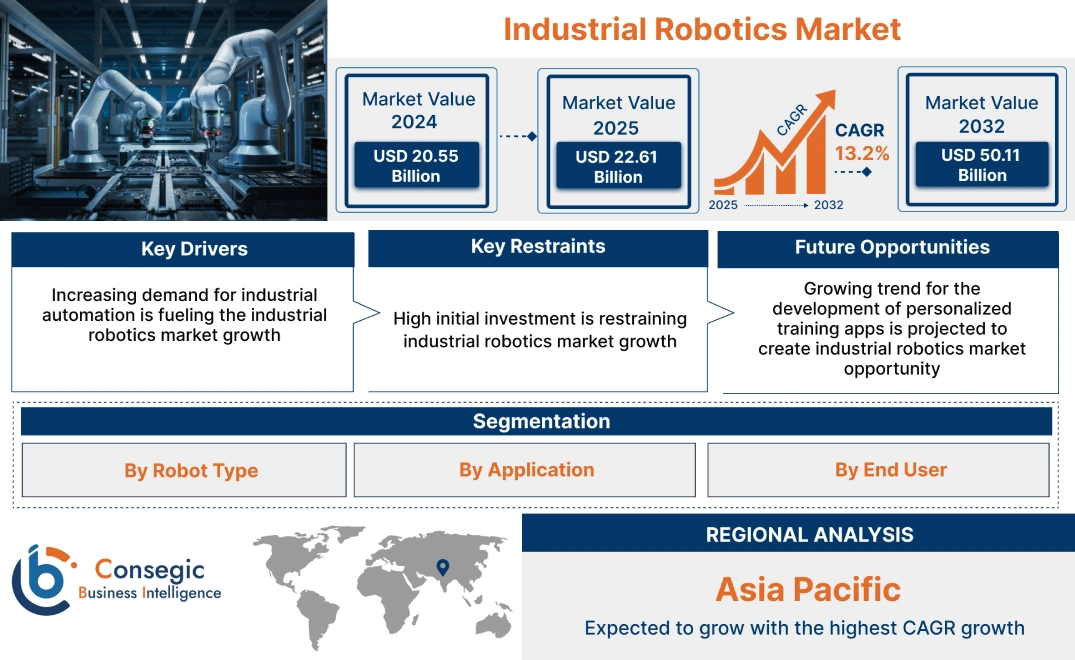

Industrial Robotics Market Size:

Industrial Robotics Market Size is estimated to reach over USD 50.11 Billion by 2032 from a value of USD 20.55 Billion in 2024 and is projected to grow by USD 22.61 Billion in 2025, growing at a CAGR of 13.2% from 2025 to 2032.

Industrial Robotics Market Scope & Overview:

Industrial robotics involves the use of automated, programmable machines within manufacturing and industrial settings to perform a variety of tasks. These robots are designed to handle repetitive, precise, and heavy-duty operations, such as assembly, welding, material handling, and painting. Characterized by their ability to enhance efficiency, improve product quality, and increase safety, industrial robots are crucial components of modern automated production systems.

Industrial Robotics Market Dynamics - (DRO) :

Key Drivers:

Increasing demand for industrial automation is fueling the industrial robotics market growth

Industrial automation, powered by robotics, allows businesses to streamline their operations, leading to increased production output with fewer resources. Robots perform repetitive tasks with greater speed and accuracy than humans, minimizing errors and maximizing throughput. Additionally, automation reduces long-term operational costs by minimizing labor expenses and improving efficiency, crucial in industries facing rising labor costs and shortages. Robots are capable of performing precise and consistent tasks, resulting in higher product quality and fewer defects, which are important in industries, such as automotive and electronics manufacturing. Also, modern industrial robots, especially collaborative robots (cobots), are designed to be flexible and adaptable, allowing businesses to quickly adjust their production lines, thereby driving the industrial robotics market size.

- For instance, according to gov, automation is a leading driver for companies adopting AI and robotics, surpassing other advanced technologies. Approximately 30% of US workers are exposed to automation-related technologies, with manufacturing labor facing the highest impact. While improving production quality remains the primary overall motivation for tech adoption (68-80% of workers), AI and robots specifically are most frequently used for automation purposes (54-66% of workers), indicating a strong trend towards labor substitution.

Consequently, increasing industrial automation is driving the industrial robotics market expansion.

Key Restraints:

High initial investment is restraining industrial robotics market growth

The cost of purchasing robots, coupled with expenses for installation, integration, programming, and training, creates a substantial financial burden, which deter businesses, with limited capital, from adopting robotic solutions. Additionally, SMEs represent a significant portion of manufacturing, lack the financial resources to invest in advanced robotic systems. This limits their ability to automate processes and improve competitiveness, hindering market growth. Moreover, the substantial upfront cost of robotics discourages rapid adoption, pushing companies towards cheaper, less effective solutions, further hindering the global industrial robotics market size.

Therefore, as per the analysis, these combined factors are significantly hindering industrial robotics market share.

Future Opportunities :

Growing trend for the development of personalized training apps is projected to create industrial robotics market opportunity

Personalized training apps are expected to revolutionize the market by providing access to specialized skills, effectively bridging the growing workforce gap. By offering tailored, interactive learning experiences, these apps reduce training costs and facilitate remote learning. This increased accessibility not only ensures a skilled workforce capable of handling advanced robotics but also promotes continuous learning and supports the wider adoption of collaborative robots, thus significantly boosting industrial robotics market demand.

- For instance, in Mar 2025, ABB introduced RoboMasters, a mobile application designed to simplify robot programming and operation training. This app offers modular courses, allowing users of all skill levels to customize their learning journey and progress at their own speed, significantly enhancing accessibility to ABB robot education.

Hence, based on the analysis, the development of personalized training apps is expected to create industrial robotics market opportunities.

Industrial Robotics Market Segmental Analysis :

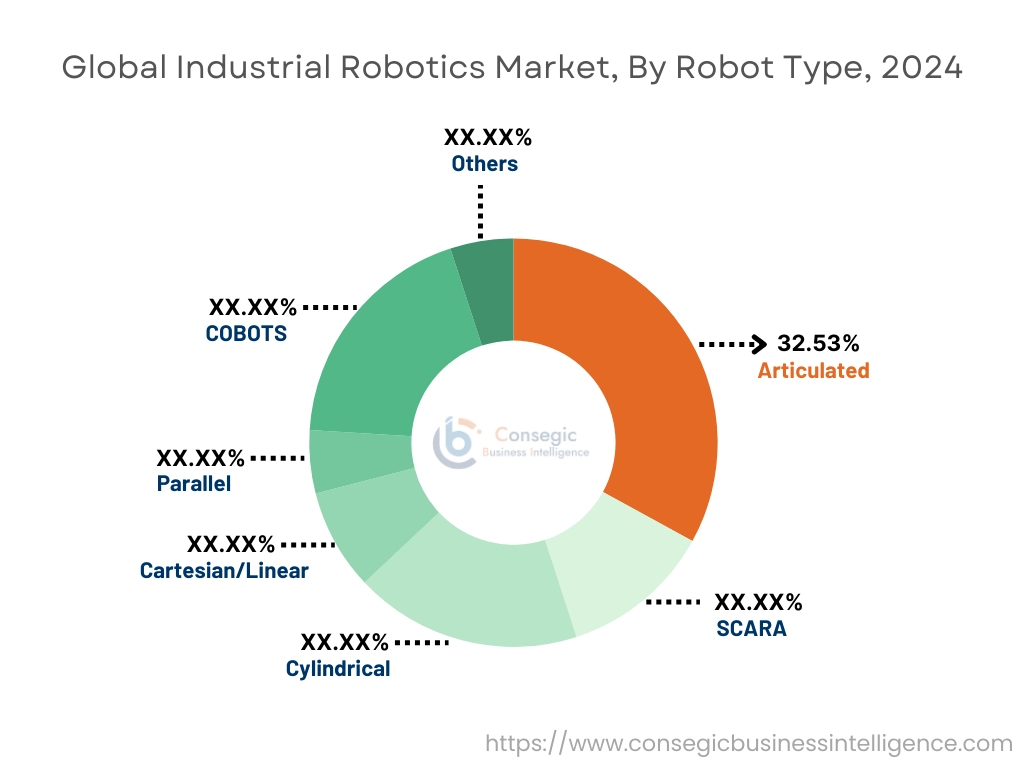

By Robot Type:

Based on the robot type, the market is categorized into articulated, SCARA, cylindrical, cartesian/linear, parallel, COBOTS, and others.

Trends in the Robot Type:

- Cartesian robots excel in applications requiring linear movements, such as pick-and-place and material handling.

- Growing trend for the adoption of parallel robots in packaging and high-speed pick-and-place applications for their high speed and accuracy.

Articulated accounted for the largest revenue share of 32.53% in the market in 2024.

- Increasing integration of articulated robots with the Industrial Internet of Things (IIoT), enabling enhanced data collection and real-time optimization is driving industrial robotics market share.

- Additionally, articulated robots offer faster cycle times for increased productivity, which in turn is boosting industry.

- Moreover, these robots are also equipped with up to 16 I/O connections (C1+C2) for more sophisticated/complex applications.

- For instance, ABB launched IRB 1100 designed to boost manufacturing productivity with 35% faster cycle times and superior precision. It offers the highest payload in its class and has a smaller footprint and lighter design than its predecessors, ideal for efficient installation, particularly in electronics manufacturing.

- Thus, as per the industrial robotics market analysis, the aforementioned factors are driving the articulated robots segment.

COBOTS are predicted to register the fastest growth during the forecast period.

- Advancements in safety features, such as improved sensors and collision detection are expected to drive the adoption of COBOTS during the forecast period.

- Additionally, increased adoption in small and medium-sized enterprises (SMEs) due to their affordability and ease of use is also accelerating the market trend.

- Integration with AI and machine learning for enhanced adaptability and task execution and increased use in wider applications, such as welding is driving industrial robotics market demand.

- For instance, in Nov 2024, Collaborative Robotics introduced Proxie, designed for seamless human-robot interaction. Proxie distinguishes itself with its "Glide 360" mobility for smooth navigation, "Scout Sense" for human-like situational awareness, "Flex Grasp" for versatile object handling, and an "Empathetic Design" that builds trust through stability and visual cues.

- In conclusion, the above-mentioned factors are contributing significantly in spurring the market.

By Application:

Based on the application, the market is classified into pick & place, welding & soldering, material handling, assembling, cutting & processing, and others.

Trends in the Application:

- Pick & Place application is witnessing a surge in demand, particularly in e-commerce and logistics, driven by the need for faster order fulfillment.

- Growing trend towards the adoption of robots for welding & soldering in automotive, aerospace, and electronics manufacturing.

Material Handling accounted for the largest revenue share in 2024 and is also projected to register the fastest CAGR.

- Automation of material handling is crucial for improving efficiency and safety in manufacturing and warehousing.

- Use of autonomous mobile robots (AMRs) for flexible material transport, as well as the integration of robotic arms with vision systems for automated loading and unloading is further driving the industrial robotics market demand.

- For instance, in Oct 2024, Bear Robotics launched the Carti 100, a robot designed to revolutionize material handling in logistics. Capable of carrying up to 220 lbs, it utilizes advanced AI and multi-robot orchestration to improve efficiency and lower costs in factories and warehouses, enabling businesses to better manage modern supply chain demands.

- Thus, as per the industrial robotics market analysis, the aforementioned factors are driving material handling segment.

By End User:

Based on the end user, the market is categorized into automotive, electrical & electronics, healthcare & pharmaceutical, food & beverages, rubber & plastic, metals & machinery, and others.

Trends in the End User:

- Trends include the development of robots for handling sterile environments, cobots for patient assistance, and AI-powered robots for diagnostic support.

- Robots are used in molding, extrusion, and material handling in the rubber and plastics industry.

Electrical & Electronics accounted for the largest revenue share in 2024.

- Electrical & Electronics sector is characterized by high-precision assembly, pick-and-place, and testing applications.

- Additionally, the use of SCARA robots for high-speed assembly, vision-guided robots for quality inspection, and the increasing adoption of robots in microelectronics manufacturing.

- Consequently, the expanding electronics industry is contributing remarkably in spurring the growth of the industrial robotics market.

- For instance, India's electronics export sector has seen a rapid expansion, with a 26% annual growth rate from fiscal year 2016 to 2025.

- Thus, as per the industrial robotics market analysis, the aforementioned factors are driving the electrical & electronics segment size.

Automotive are predicted to register the fastest growth during the forecast period.

- Growing focus on automation in assembly, welding, painting, and material handling is driving the need for industrial robotics from the automotive sector.

- Increased adoption of cobots for collaborative tasks, AI-powered robots for quality control, and the integration of robots into electric vehicle (EV) production lines is expected to drive the market expansion.

- Additionally, there is a greater need for robots that can handle battery assembly and paint repair.

- For instance, in Feb 2025, 3M and General Motors collaborated to implement the first robotic paint repair system on a moving assembly line. GM is utilizing 3M's Finesse-it Robotic Paint Repair System, which combines robotics, specialized software, process modeling, and advanced abrasives, to automatically correct paint defects on vehicles during production.

- In conclusion, the above-mentioned factors are contributing significantly in spurring the market trend.

Regional Analysis:

The global industrial robotics market has been classified by region into North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America.

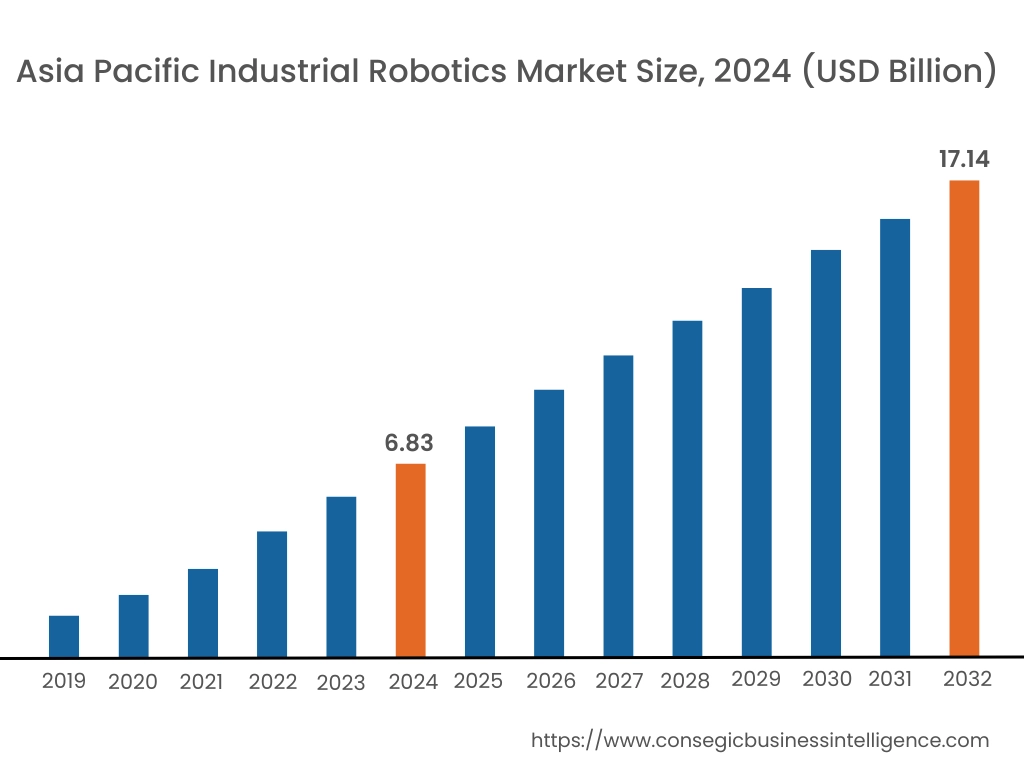

Asia Pacific was valued at USD 6.83 Billion in 2024. Moreover, it is projected to grow by USD 7.54 Billion in 2025 and reach over USD 17.14 Billion by 2032. Out of these, China accounted for the largest revenue share of 42.97% in 2024.

Countries like China, Japan, South Korea, and Taiwan are global leaders in industries such as electronics, automotive, and consumer goods. These industries heavily rely on automation to enhance productivity, improve quality, and reduce costs, leading to a significant need for industrial robots. In addition, the region is experiencing a surge in the adoption of automation technologies, driven by factors such as rising labor costs, labor shortages, and the need to improve operational efficiency. Moreover, the presence of key players in the region is also contributing significantly in driving the industrial robotics market growth.

- For instance, in Nov 2023, Yaskawa Electric introduced the MOTOMAN NEXT series, a pioneering line of adaptive industrial robots designed to revolutionize factory automation. These robots, available in five payload capacities, feature an open platform and are the first in the industry to autonomously adapt to their environment and make decisions. This launch is a key component of Yaskawa's i3-Mechatronics initiative, aimed at leveraging digital data to address societal challenges through advanced robotics.

North America region was valued at USD 6.18 Billion in 2024. Moreover, it is projected to grow by USD 6.79 Billion in 2025 and reach over USD 14.83 Billion by 2032. The increasing integration of advanced technologies like AI, machine learning, and the Industrial Internet of Things (IIoT) is enhancing the capabilities of robots and expanding their applications in American countries. Additionally, the need to address labor shortages and rising labor costs is prompting companies to invest in robotic automation to improve productivity and efficiency. Moreover, North American companies are increasingly focusing on innovation and automation to maintain a competitive edge in the global market.

- For instance, in Apr 2025, DoorDash expanded its sidewalk robot delivery service in the U.S. in collaboration with Coco. Following a successful pilot program in Helsinki through its Wolt division, DoorDash is now offering robot deliveries in Los Angeles and Chicago from nearly 600 merchants.

As per the industrial robotics market analysis, Initiatives and funding from the European Union and national governments are promoting the adoption of robotics and related technologies in European countries. Additionally, rising manufacturing activity across various sectors is creating a demand for automation solutions to improve efficiency and productivity in Latin America countries. Moreover, Middle East and Africa region rising investments in various sectors, including automotive, electronics, and healthcare, are fueling the need for industrial robots.

Top Key Players and Market Share Insights:

The market is highly competitive with major players providing industrial robotics to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the industrial robotics industry include-

- ABB (Switzerland)

- FANUC (Japan)

- Yaskawa Motoman (Japan)

- Epson Robots (Japan)

- Denso Robotics (Japan)

- Hyundai Robotics (South Korea)

- Techman Robot (Taiwan)

- Doosan Robotics (South Korea)

- KUKA AG (Germany)

- Universal Robots (Denmark)

- Kawasaki Robotics (Japan)

- Mitsubishi Electric (Japan)

- Omron Automation (Japan)

- Stäubli Robotics (Switzerland)

- Comau Robotics (Italy)

Recent Industry Developments :

Product Launch:

- In Nov 2023, Universal Robots launched the UR30, a new 30 kg payload cobot, expanding its next-generation product line. Built on the same architecture as the UR20, the compact UR30 offers significant lifting capacity and precise motion control, enabling faster and heavier load handling.

- In Mar 2025, ABB launched two new AI-powered modules, the Fashion Inductor and Parcel Inductor, for its Item Picking family, enhancing logistics and e-commerce supply chains. These modules, utilizing ABB's AI vision technology, automate item picking and sorter induction, critical processes in the industry.

Collaboration:

- In Apr 2025, Accenture and Schaeffler collaborated to advance industrial humanoid robot applications, showcasing at Hannover Messe 2025 how NVIDIA and Microsoft's AI and simulation technologies can optimize factory workflows. They're using Agility Robotics' Digit, and other robots like Sanctuary AI's Phoenix and Schaeffler's EMMA, within a digital twin environment to demonstrate various automation scenarios, including human-robot collaboration and full automation for tasks like material handling.

- In Apr 2025, ABB Robotics and Stena Recycling collaborated to transform wood waste into new furniture, significantly boosting material recycling rates. This collaboration shifts from energy recovery to material reuse, offering enhanced environmental benefits. By processing ABB's wood waste into particle boards, they're contributing to a more sustainable furniture production cycle.

Partnership:

- In May 2024, Neura Robotics and OMRON formed a partnership to introduce AI-powered cognitive robots into manufacturing. This collaboration will combine their expertise to develop advanced robotic systems that improve efficiency and safety on factory floors by using AI to adapt to dynamic production environments.

Industrial Robotics Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 50.11 Billion |

| CAGR (2025-2032) | 13.2% |

| By Robot Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the industrial robotics market? +

The industrial robotics market size is estimated to reach over USD 50.11 Billion by 2032 from a value of USD 20.55 Billion in 2024 and is projected to grow by USD 22.61 Billion in 2025, growing at a CAGR of 13.2% from 2025 to 2032.

What specific segmentation details are covered in the industrial robotics report? +

The industrial robotics report includes specific segmentation details for robot type, application, end user, and regions.

Which is the fastest segment anticipated to impact the market growth? +

In the industrial robotics market, COBOTS is the fastest-growing segment during the forecast period.

Who are the major players in the industrial robotics market? +

The key participants in the industrial robotics market are ABB (Switzerland), FANUC (Japan), Yaskawa Motoman (Japan), KUKA AG (Germany), Universal Robots (Denmark), Kawasaki Robotics (Japan), Mitsubishi Electric (Japan), Omron Automation (Japan), Stäubli Robotics (Switzerland), Comau Robotics (Italy), Epson Robots (Japan), Denso Robotics (Japan), Hyundai Robotics (South Korea), Techman Robot (Taiwan), Doosan Robotics (South Korea), and Others.