- Summary

- Table Of Content

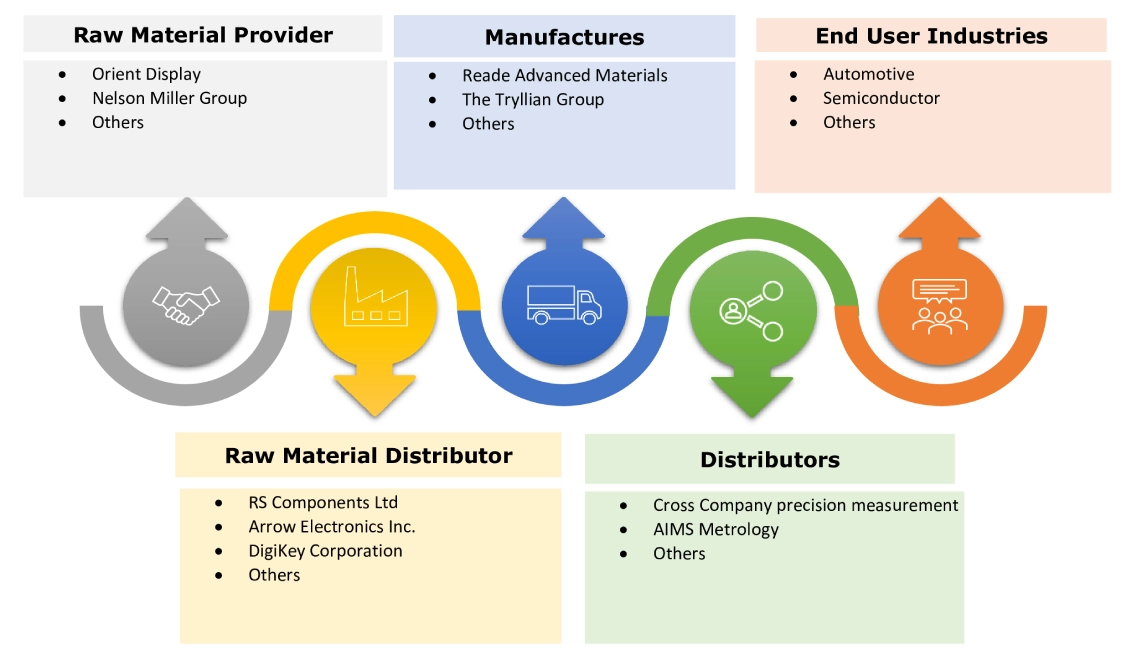

- Methodology

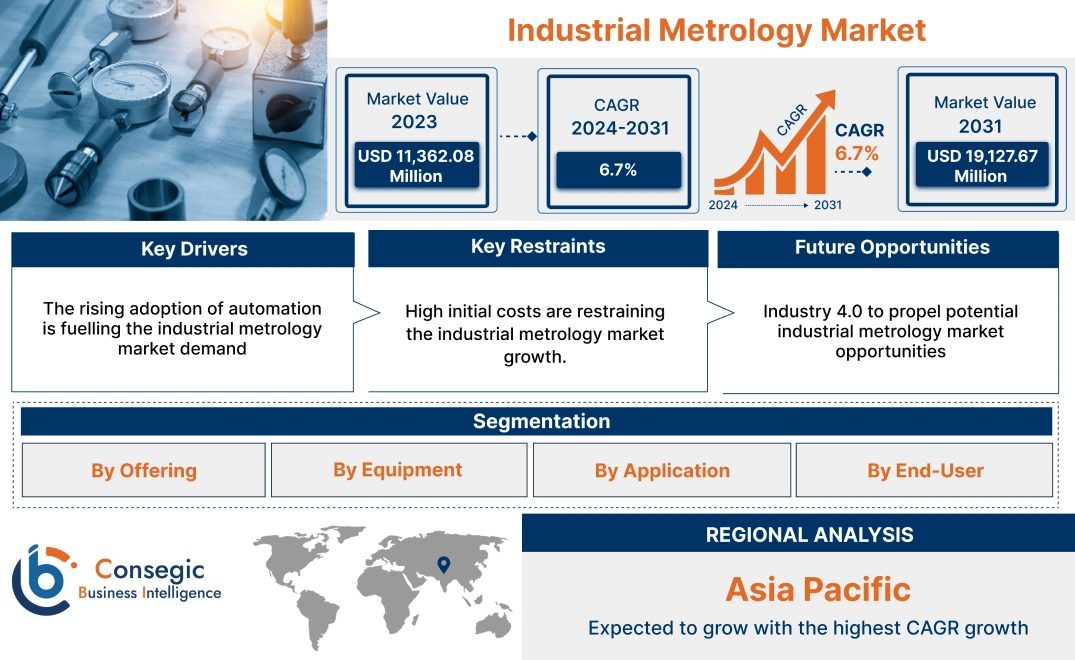

Industrial Metrology Market Size:

Industrial Metrology Market size is estimated to reach over USD 19,127.67 Million by 2031 from a value of USD 11,362.08 Million in 2023 and is projected to grow by USD 11,924.05 Million in 2024, growing at a CAGR of 6.7% from 2024 to 2031.

Industrial Metrology Market Scope & Overview:

Industrial metrology is the science of measurement applied in industrial and manufacturing processes to ensure that products meet specific quality, dimensional, and performance standards. It plays a crucial role in maintaining product consistency and accuracy, improving production efficiency, and reducing costs by minimizing defects and rework. By ensuring compliance with industry and enhancing the precision of manufacturing processes, industrial metrology supports high-quality outcomes and better decision-making. Applications of industrial metrology span a variety of industries, including the automotive sector for ensuring the precision of components, aerospace for accurate measurements of critical parts, consumer electronics for quality control of complex components, and healthcare for the production of precise medical devices.

Industrial Metrology Market Dynamics - (DRO) :

Key Drivers:

The rising adoption of automation is fuelling the industrial metrology market demand

Rising automation and digital connectivity are transforming manufacturing. Metrology systems are being integrated into automated production lines, allowing for real-time data collection, and feedback to optimize processes. Automated metrology solutions like robotic arms with measurement tools enable continuous quality checks without interrupting production, enhancing productivity and reducing human error. This shift allows manufacturers to adopt predictive maintenance, reducing downtime and ensuring operational efficiency.

- In December 2023, Nikon Metrology’s NEXIV product line introduced advanced automation solutions, enhancing precision in the electronics, automotive, and semiconductor industries.

Thus, the rising advancements in automation for enhancing precision in different industries are driving the industrial metrology market size.

Key Restraints :

High initial costs are restraining the industrial metrology market growth.

Advanced metrology systems, such as 3D scanners, coordinate measuring machines, and laser-based tools, require significant upfront costs. The cost of acquiring, installing, and maintaining these technologies can be a financial barrier, particularly for small and medium-sized enterprises. In addition, continuous modification, adjustment of equipment, and complex operation training add to the overall expenses, limiting widespread adoption.

Therefore, the high costs associated with the implementation of metrology solutions are restraining the growth of the industrial metrology industry.

Future Opportunities :

Industry 4.0 to propel potential industrial metrology market opportunities.

Industry 4.0 allows for smart manufacturing with the implementation of machine learning, AI, IoT, and various other technologies in factories to increase efficiency, productivity, and flexibility. Benefits include enhanced productivity due to smart decisions backed by data-based tools and quality control.

- In August 2024, Neilsoft, an engineering services and solution provider launched industry 4.0 solutions that automated quality control and inspection in assembly lines to increase efficiency through monitoring and real-time data analysis and processing.

Hence, the rising adoption of new technologies in factories is anticipated to drive industrial metrology market opportunities during the forecast period.

Industrial Metrology Market Segmental Analysis :

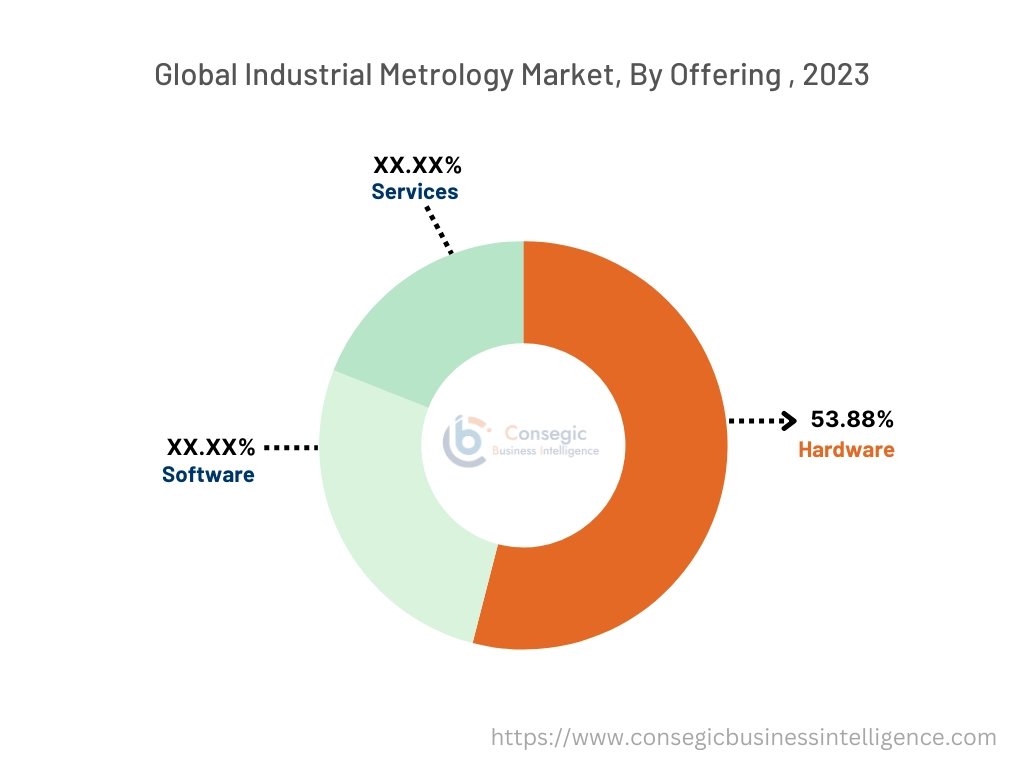

By Offering:

Based on the offerings, the market is segmented into hardware, software, and services.

Trends in the offering:

- The industrial metrology market is driven by factors such as increased hardware adoption for quality control.

- There is an increasing trend toward metrology software adoption in the market as companies are gradually focusing on improvements to minimize defects and errors in the assembly line.

The hardware offering accounted for the largest revenue of 53.88% in the industrial metrology market share in the year 2023.

- Hardware offerings include micrometers, Vernier’s and coordinate measuring machines, computing devices, and others. These offerings are provided by technology companies as part of a broader infrastructure solution.

- Hardware metrology components offer benefits such as performance, reliability, security, and various others.

- In December 2022, Witte introduced a rotary plate with a scale and Vernier grid to its ALUFIX modular fixturing system, allowing faster and more precise workpiece alignment.

- Thus, the advancements in vernier’s, coordinate measuring machines and various other hardware offerings are driving the industrial metrology market trends.

The software offering is anticipated to register the fastest CAGR during the forecast period.

- Software offerings include displaying, monitoring, controlling, and reporting aspects of the measuring process. Key benefits include improved operational efficiency, enhanced precision and accuracy, data interpretation and presentation, cost efficiency, and others.

- Moreover, metrology helps in the design process by ensuring items are created within standard margins of error. It also helps in the validation of products and testing solutions, ensuring they meet the required standards and specifications.

- In September 2024, Hexagon introduced the new Leica Absolute Tracker ATS800 combines laser tracking and radar functionality, speeding up large-scale manufacturing inspections.

- Therefore, the rising development of industrial metrology solutions along with advanced software technology is anticipated to boost the market during the forecast period.

By Equipment:

Based on the equipment, the market is segmented into coordinate measuring machines (CMM), optical digitizers and scanners (ODS), measuring instruments, x-ray and computed tomography, automated optical inspection, form measurement equipment, and 2D equipment.

Trends in the equipment:

- The equipment segment is driven by factors such as increased prioritization of quality and precision control in manufacturing processes using metrology equipment.

- There is a rising growth in non-contact metrology equipment such as optical scanners and digitizers which are used for obtaining coordinate points.

The optical digitizer and scanner (ODS) accounted for the largest revenue of industrial metrology market share in the year 2023.

- Optical digitizer and scanner (ODS) converts images, documents, and objects into digital records. Benefits include efficiency, and accuracy in healthcare, engineering, and various other sectors.

- Optical scanning applications include patient diagnosis, laboratory data, and others. It offers an efficient way to help enter information for later use in medical data analysis and retrieving important details.

- In December 2022, Revopoint launched the POP 3 PLUS 3D scanner, with 20% improved accuracy over the POP 3 with enhanced precision, upgraded algorithms, and new optical zoom, which ensures fast and more detailed scans.

- Thus, the advancement in digitizers and scanners for analysis purposes is driving the industrial metrology market trends.

The coordinate measuring machine (CMM) is anticipated to register the fastest CAGR during the forecast period.

- Coordinate Measuring Machine measures the geometry of physical objects by sensing discrete points of the physical object. The benefits of CMM include the measurement of 3D objects that are difficult to measure with high accuracy. It is often used in aircraft for testing and inspection applications.

- In February 2024, LK Metrology launched the new ALTERA C HA ultra-high accuracy CMM with reduced cost and tight tolerances.

- Therefore, the growing adoption of coordinate measuring machines along with growing advancements in precision measurement technology are expected to drive the industrial metrology market expansion during the forecast period.

By Application:

Based on the application, the market is segmented into quality control and inspection, reverse engineering, mapping and modeling, and others.

Trends in the application:

- There is a rising trend of advanced 3D scanning technologies which are used for scanning and inspection.

- Integration of IoT in metrology for real-time analysis and operations for data collection and improved operational efficiency.

Quality control and inspection accounted for the largest revenue share in the year 2023.

- Quality control and inspection play a crucial role as any incorrect measurement leads the degraded product quality. It helps products meet accurate specifications to create quality parts.

- The aerospace sector often requires crucial quality control and inspection processes in the alignment of airframe assembly, structural components, calibration of tooling, engine turbine, and landing gear among others.

- In November 2023, ZEISS Industrial Quality Solutions launched ZEISS INSPECT 3D metrology software with improved evaluation of functions and fast data acquisition, which ensures enhanced 3D measurement.

- Hence, the rising innovations in quality control equipment are driving the industrial metrology market size.

The reverse engineering is anticipated to register the fastest CAGR during the forecast period.

- The process of creating a data model from a script and a database is reverse engineering. The modeling tool helps to generate a visual diagram of chosen database objects, illustrating the connections and relationships between them. It helps to solve problems with existing products.

- Applications of reverse engineering include part replacement, part service and repair, failure prediction, parts improvement, diagnosis, and problem-solving.

- For instance, in August 2022, FARO introduced RevEng 2022 software, offering enhanced 3D scanning and reverse engineering capabilities for improved precision and efficiency in complex designs.

- Thus, as per the industrial metrology market analysis, the growing advancement in reverse engineering is anticipated to boost the market growth during the forecast period.

By End-User:

Based on the end user the market is segmented into aerospace and defense, automotive, semiconductor, manufacturing, and other.

Trends in the end user:

- Rising use of industry metrology solutions in automotive sectors such as 3D scanning, optical inspection, and others for quality control.

- Increasing demand for real-time data analysis and data processing in the aerospace and defense sector due to their functional requirements.

The automotive segment accounted for the largest revenue share in 2023, and it is anticipated to register the fastest CAGR during the forecast period.

- In the automotive sector, metrology is applied in design, prototyping, production, quality assurance and others. It offers conformity of design specifications and production efficiencies. Key benefits include quality control, safety, and cost efficiency.

- The measurements of components during the production stage with the help of 3D scanning and CAD/CAM software technology ensures quality standards.

- In April 2024, Cognex Corporation launched the In-Sight L38 3D Vision System, a combination of AI, 2D, and 3D vision technologies to improve inspection in assembly lines in automotive factories.

- Thus, the rising demand for safety and quality assurance in the automotive sector is driving the industrial metrology market demand.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

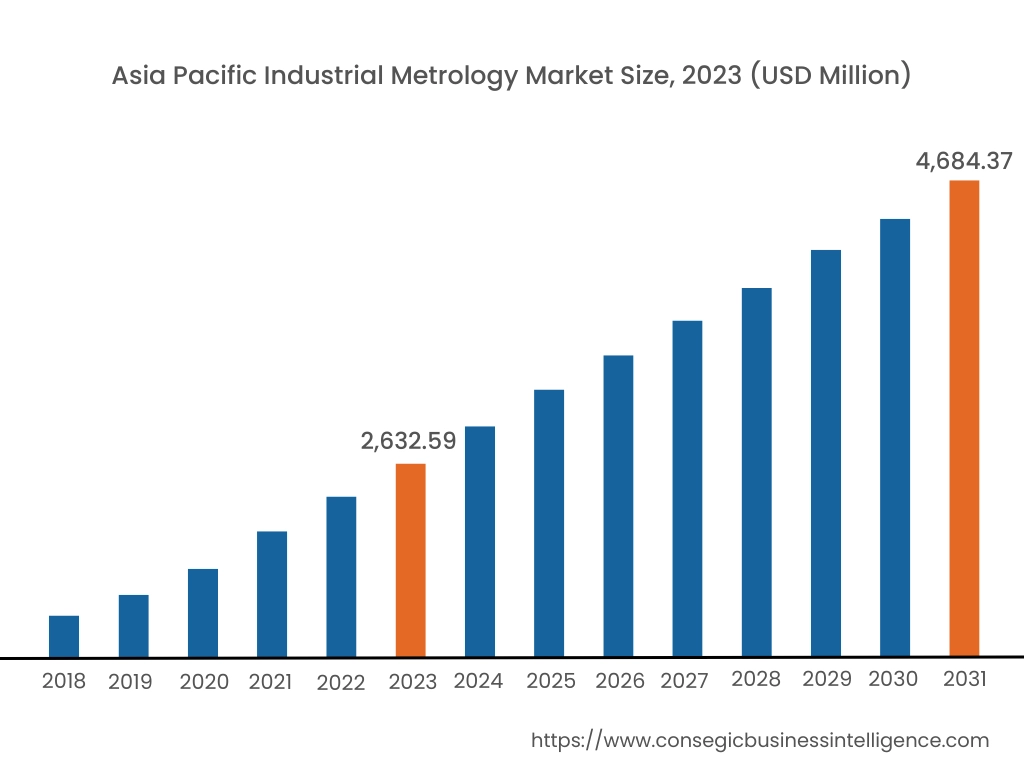

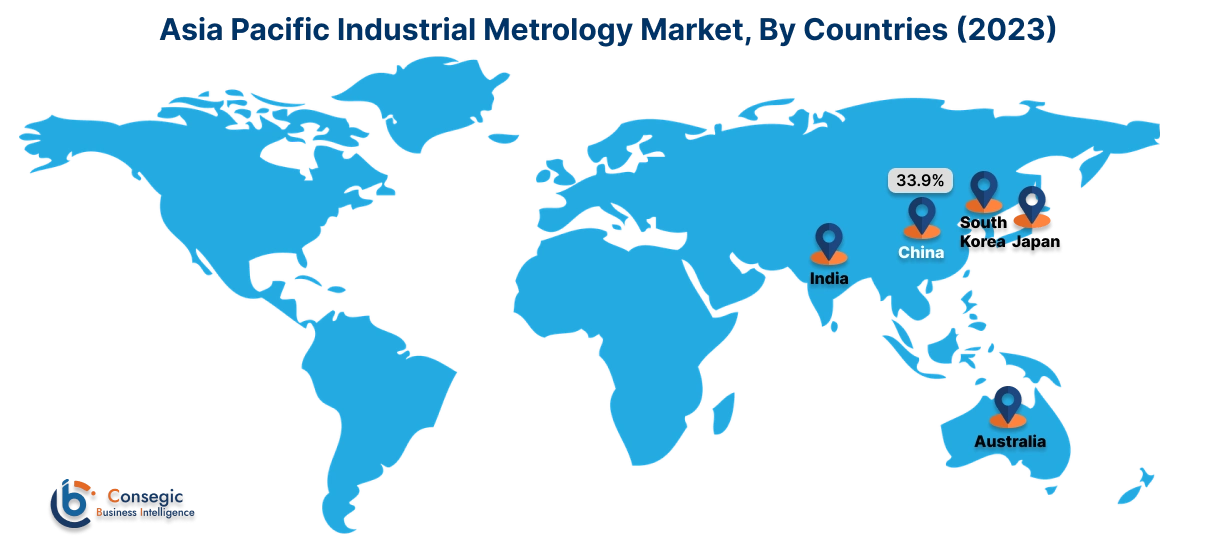

Asia Pacific region was valued at USD 2,632.59 Million in 2023. Moreover, it is projected to grow by USD 2,775.92 Million in 2024 and reach over USD 4,684.37 Million by 2031. Out of this, China accounted for the maximum revenue share of 33.9%. In the Asia-Pacific region, the rising need for quality control and inspection in the automotive and manufacturing sectors is driving the industrial metrology market growth.

- For instance, in July 2023, Hexagon's Manufacturing Intelligence division launched OPTIV scope, a vision Coordinate Measuring Machine (CMM) designed to streamline quality inspection and improve efficiency across several industries including automotive.

North America is estimated to reach over USD 7,467.44 Million by 2031 from a value of USD 4,434.71 Million in 2023 and is projected to grow by USD 4,654.15 Million in 2024. As per the analysis, the industrial metrology market expansion in North America is mainly driven by demand for quality control across various sectors, including aerospace and defense, automotive, semiconductor, and others, thereby, driving the market.

- In July 2024, Hyundai Motor North America enhances material and mechanism analysis with advanced Nikon X-ray CT technology, significantly reducing evaluation time.

Additionally, according to the industrial metrology market analysis, Europe is anticipated to witness substantial development. The region is backed by the growing manufacturing of automotive and others across the region. Moreover, the Middle East and Africa are poised for moderate development. The factors affecting the market are automotive and manufacturing in Saudi Arabia and UAE which are driving the industrial metrology market. Further, the Latin American region is experiencing growth due to rising production of semiconductors, automotive, and others. Countries such as Brazil, Argentina, and others are representing the cumulative expansion of the industrial metrology market in the region.

Top Key Players & Market Share Insights:

The global industrial metrology market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the industrial metrology industry include-

- FARO Technologies (Canada)

- Nikon Metrology (US)

- Automated Precision Inc. (US)

- KLA Corporation (US)

- Applied Materials Inc. (US)

- Carl Zeiss AG (Germany)

- Hexagon AB (Sweden)

- Renishaw PLC (UK)

- Jenoptik AG (Germany)

- Perceptron (US)

Recent Industry Developments :

Product launches:

- In May 2024, Nikon launched NEXIV AutoMeasure v14, which is the latest video measurement software, featuring new tools to streamline program creation and enhance accuracy for manufacturers. This update aims to boost productivity and improve user experience globally.

Partnerships and Collaborations:

- For instance, Siemens AG has acquired Inspekto GmbH, a startup known for its AI-driven visual inspection system, INSPEKTO S70. This acquisition enhances Siemens's automation capabilities with Inspekto’s cutting-edge machine Vision technology.

Industrial Metrology Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 19,127.67 Million |

| CAGR (2024-2031) | 6.7% |

| By Offering |

|

| By Equipment |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Industrial metrology system market? +

The Industrial metrology system market was valued at USD 11,362.08 Million in 2023 and is projected to grow to USD 19,127.67 Million by 2031.

Which is the fastest-growing region in the industrial metrology system market? +

Asia-Pacific is the region experiencing the most rapid growth in the Industrial metrology system market.

What specific segmentation details are covered in the industrial metrology system report? +

The industrial metrology system report includes specific segmentation details for system type, end user, and region.

Who are the major players in the industrial metrology system market? +

The key participants in the industrial metrology market are Hexagon AB (Sweden), Renishaw PLC (UK), FARO Technologies (Canada), Nikon Metrology (US), Carl Zeiss AG (Germany), Jenoptik AG (Germany), Perceptron (US), Automated Precision Inc. (US), KLA Corporation (US), Applied Materials Inc. (US).