- Summary

- Table Of Content

- Methodology

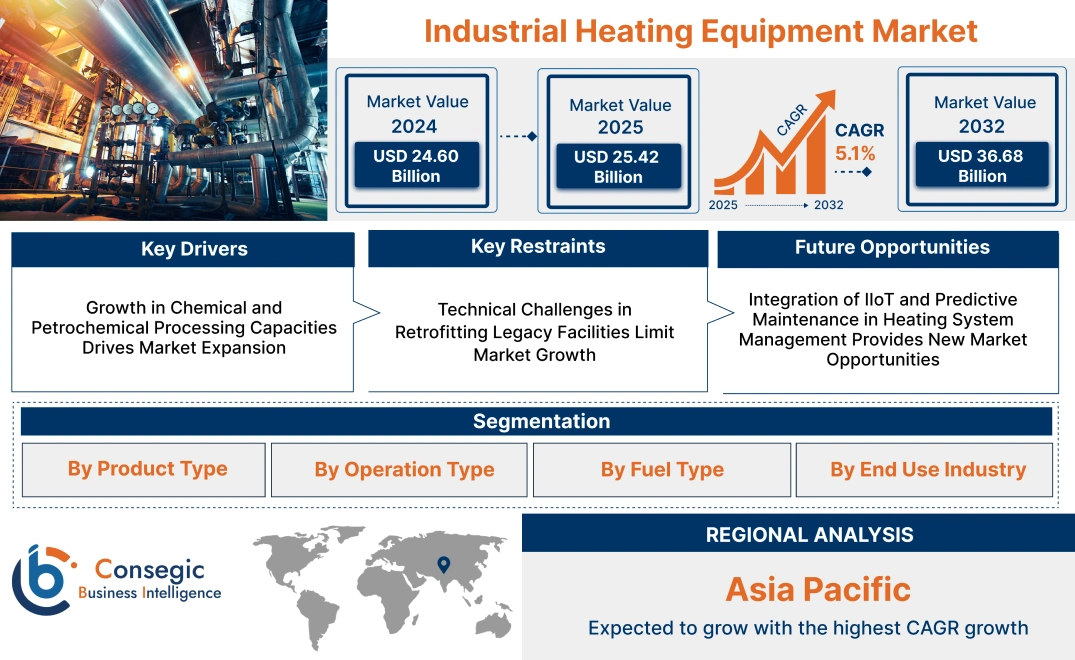

Industrial Heating Equipment Market Size:

Industrial Heating Equipment Market size is estimated to reach over USD 36.68 Billion by 2032 from a value of USD 24.60 Billion in 2024 and is projected to grow by USD 25.42 Billion in 2025, growing at a CAGR of 5.1% from 2025 to 2032.

Industrial Heating Equipment Market Scope & Overview:

Industrial heating equipment refers to machinery designed to produce and maintain controlled heat levels for various industrial processes such as metalworking, chemical processing, food production, and material fabrication. This equipment includes furnaces, boilers, heat exchangers, and infrared heaters, tailored to specific temperature requirements and operational environments.

Key features of this equipment include precise temperature regulation, energy efficiency, and integration with automated control systems. Such systems offer uniform heat distribution, durable construction, and adaptability to different fuel sources, including electricity, gas, and oil. Advanced configurations support continuous operation and real-time monitoring to ensure safety and process stability.

Manufacturers, processing plants, and fabrication facilities utilize industrial heating equipment to improve product quality, reduce thermal losses, and meet specific production standards. Its versatility across applications and consistent thermal performance make it a critical component in modern industrial infrastructure, supporting optimized process control and long-term operational reliability.

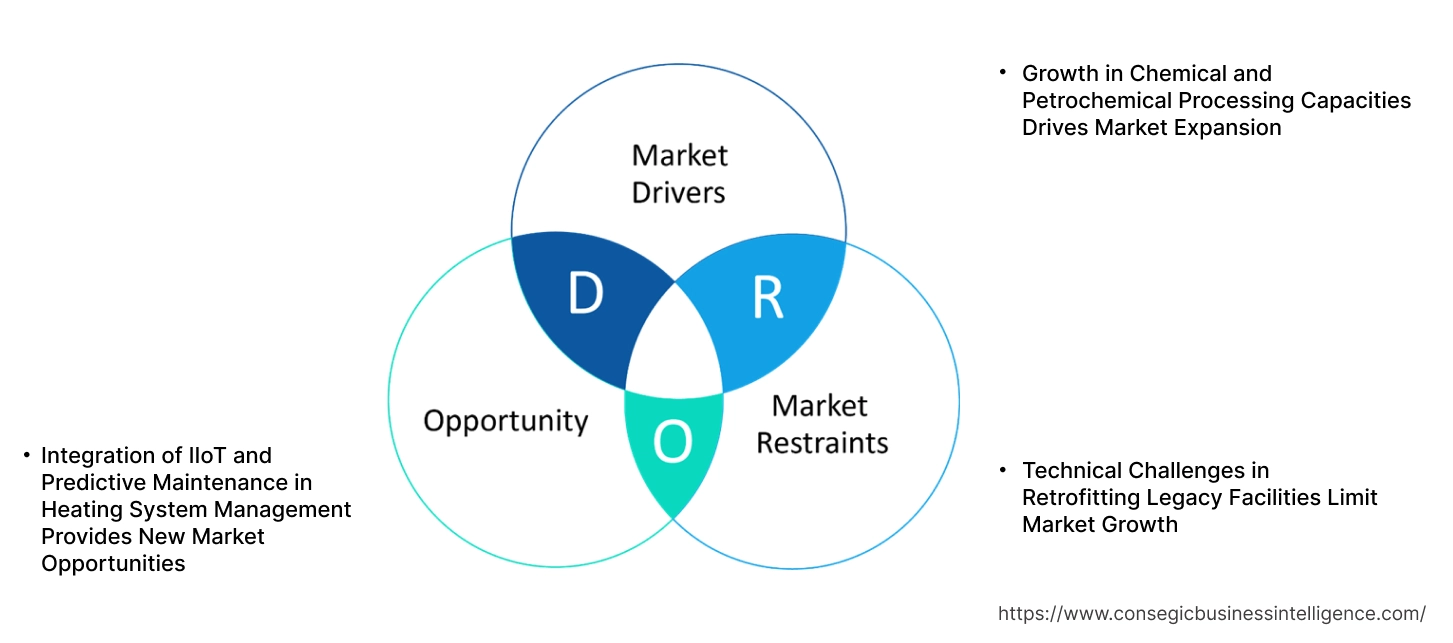

Industrial Heating Equipment Market Dynamics - (DRO):

Key Drivers:

Growth in Chemical and Petrochemical Processing Capacities Drives Market Expansion

Thermal processes such as catalytic reforming, cracking, polymerization, and distillation require consistent and precise heat delivery to maintain reaction efficiency and product quality. Fired heaters, electric process heaters, and heat exchangers are critical for these operations, operating under high-pressure and high-temperature environments. The rise in demand for downstream chemicals and polymers, coupled with new refinery investments, is driving the installation of both greenfield and brownfield thermal systems. Additionally, the move toward more efficient and automated processing plants is supporting the adoption of advanced heating technologies with integrated control systems. These developments are increasing procurement from EPC contractors, OEMs, and plant operators. The expanding footprint of high-throughput chemical production is a key driver of industrial thermal system adoption, leading to sustained industrial heating equipment market expansion.

Key Restraints:

Technical Challenges in Retrofitting Legacy Facilities Limit Market Growth

Many industrial plants operating today were built decades ago and rely on aging thermal infrastructure. Retrofitting these facilities with new-generation heating systems presents several engineering and operational challenges. Outdated plant layouts, limited electrical capacity and non-standardized control architectures often require extensive redesign and customization to accommodate modern thermal technologies. In certain cases, spatial constraints and structural limitations restrict the ability to install more efficient heating units or integrate safety upgrades. Furthermore, retrofitting involves factory downtime, which disrupts production and affects revenue, making facility operators hesitant to initiate modernization projects. Additionally, a shortage of skilled technicians familiar with both legacy and new systems hinders seamless implementation. This complexity increases project cost and timeline, reducing the appeal of system replacement in conservative industrial sectors. These barriers collectively restrict the pace of system upgrades, ultimately slowing industrial heating equipment market growth.

Future Opportunities:

Integration of IIoT and Predictive Maintenance in Heating System Management Provides New Market Opportunities

The adoption of Industrial Internet of Things (IIoT) technologies is transforming thermal system management across process industries. IIoT-enabled heating systems equipped with real-time sensors allow continuous monitoring of critical parameters such as burner efficiency, fuel-air ratio, and surface temperatures. These data streams support predictive maintenance models that identify performance degradation or component wear before failure occurs. This shift toward condition-based maintenance reduces unplanned downtime, lowers repair costs, and extends equipment life cycles. The demand for intelligent system control is rising among manufacturers focused on improving plant uptime, safety, and energy performance. Furthermore, remote monitoring capabilities enable centralized oversight across multi-site operations, improving response times and maintenance planning. These digital enhancements are gaining traction in industries undergoing automation, particularly in energy, metallurgy, and food processing. As the industry moves toward smart infrastructure, the integration of IIoT and predictive analytics is unlocking long-term industrial heating equipment market opportunities driven by both demand and growth.

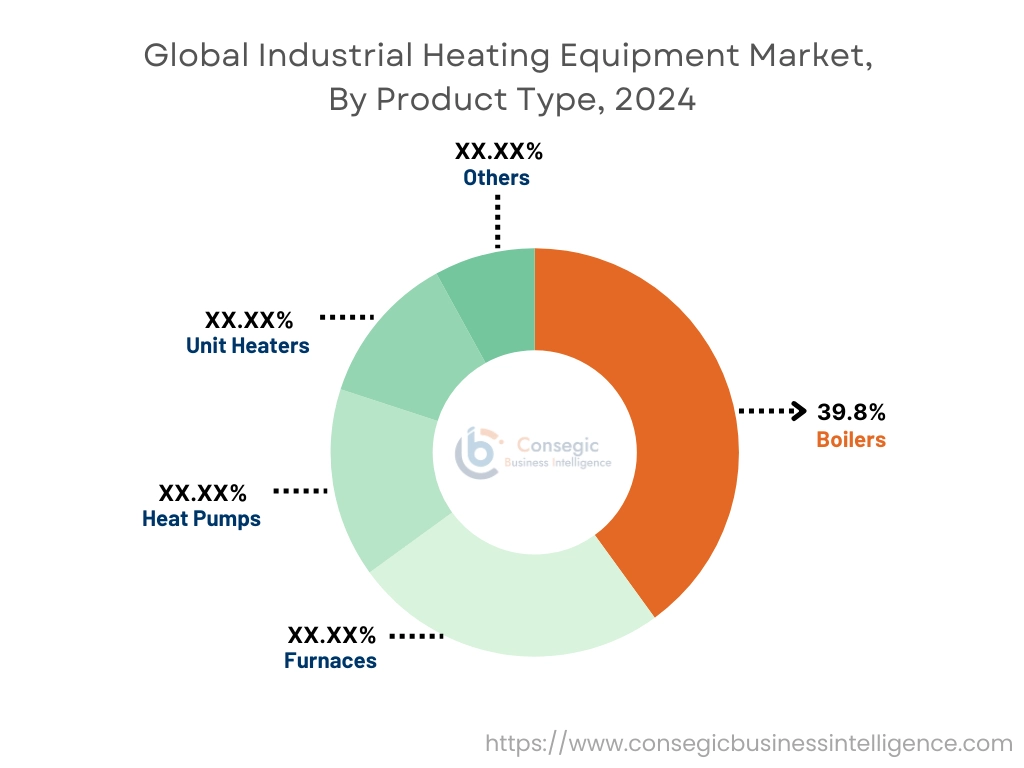

Industrial Heating Equipment Market Segmental Analysis :

By Product Type:

Based on product type, the industrial heating equipment market is segmented into boilers, furnaces, heat pumps, unit heaters (electric, gas-fired, oil-fired), and others.

The boilers segment held the largest market share of 39.8% in 2024.

- Boilers are critical in providing process heat and steam across food processing, chemical, and pharmaceutical industries.

- Integration of high-efficiency and condensing boiler technologies is a key market trend.

- Regulatory shifts toward energy-efficient systems have fueled boiler upgrades across North America and Europe.

- For instance, in September 2024, Babcock Wanson launched the new LV-Pack low-voltage industrial electric boiler. Its design specifications include steam outputs from 600 kg/h to 8400 kg/h and a design pressure of up to 18 barg. It does not require a chimney as it operates electronically.

- According to industrial heating equipment market analysis, stringent emission standards continue to support boiler replacement need.

The heat pumps segment is expected to grow at the fastest CAGR during the forecast period.

- Industrial heat pumps reduce fossil fuel dependency and are increasingly adopted for low to medium-temperature processes.

- Their suitability for heat recovery and renewable integration aligns with sustainability goals.

- Segmental trends reflect increased funding for electrified heat solutions in Europe and Asia-Pacific.

- For instance, in February 2025, Worksport Subsidiary Terravis Energy unveiled revolutionary heat pump AetherLux, which eliminates defrost cycles & shatters performance standards. The product has been tested to successfully work at temperatures as low as -57°F and as high as +131°F.

- The rising preference for low-carbon heating accelerates industrial heating equipment market expansion in the heat pump segment.

By Operation Type:

Based on operation type, the market is segmented into direct heating and indirect heating.

The direct heating systems segment accounted for the largest industrial heating equipment market share in 2024.

- These systems provide rapid heat transfer and are widely used in metal processing, glass, and forging industries.

- Fuel-fired furnaces and infrared heaters are dominant components in direct heating configurations.

- Industrial heating equipment market demand for high-temperature and localized heating applications reinforces segment strength.

- As per segmental analysis, process efficiency and fuel savings favor direct heating installations.

The indirect heating segment is projected to witness the fastest CAGR during the forecast period.

- Indirect systems minimize contamination risks, making them essential in food, pharmaceuticals, and cleanroom environments.

- Technologies include heat exchangers and jacketed vessels for controlled thermal operations.

- Industrial heating equipment market trends point to increased use of indirect heating in the biotechnology and electronics sectors.

- Furthermore, the push for cleaner production environments boosts the indirect heating segment across global manufacturing hubs.

By Fuel Type:

Based on fuel type, the market is segmented into electric, gas, oil, renewable energy, and others.

The gas-powered systems held the dominant market share in 2024.

- Natural gas remains the preferred fuel due to its availability, cost-effectiveness, and compatibility with high-efficiency systems.

- Gas-fired boilers and furnaces continue to serve as primary equipment across petrochemicals and textile plants.

- Ongoing upgrades in burner technology and emissions control fuel this segment’s relevance.

- Industrial heating equipment market analysis shows gas systems being optimized for hybrid operations with renewable backup.

Renewable energy-powered systems are projected to grow at the fastest CAGR during the forecast period.

- Biomass, solar thermal, and waste heat recovery systems align with decarbonization targets in industrial sectors.

- Its adoption is supported by policy incentives and net-zero emission frameworks across Europe and Asia.

- The market demand for sustainable technologies is driving the rapid transition to low-carbon fuels.

- The integration of hybrid systems with renewables is a key trend shaping industrial heating equipment market growth.

By End Use Industry:

Based on end-use industry, the industrial heating equipment market is segmented into chemicals, oil & gas, food & beverage, mining, automotive, power generation, electronics & semiconductors, pharmaceuticals, textiles, aerospace & defense, and others.

Chemicals held the largest industrial heating equipment market share in 2024.

- This sector relies heavily on boilers, furnaces, and heat exchangers for distillation, polymerization, and refining processes.

- Consistent capacity expansions in Asia-Pacific and the Middle East sustain equipment installation cycles.

- Industrial heating equipment market trends show that digital control systems are increasingly integrated for real-time monitoring.

- The drive to enhance thermal efficiency and reduce emissions sustains long-term market requirements.

The electronics & semiconductors segment is expected to grow at the fastest CAGR during the forecast period.

- Precise and contamination-free heating is essential in wafer fabrication, deposition, and cleanroom operations.

- Growth of chip manufacturing and semiconductor foundries in East Asia drives segment acceleration.

- Segmental analysis indicates rising investments in high-purity heating systems.

- Temperature-controlled thermal equipment in fabs and SMT lines supports the industrial heating equipment market demand.

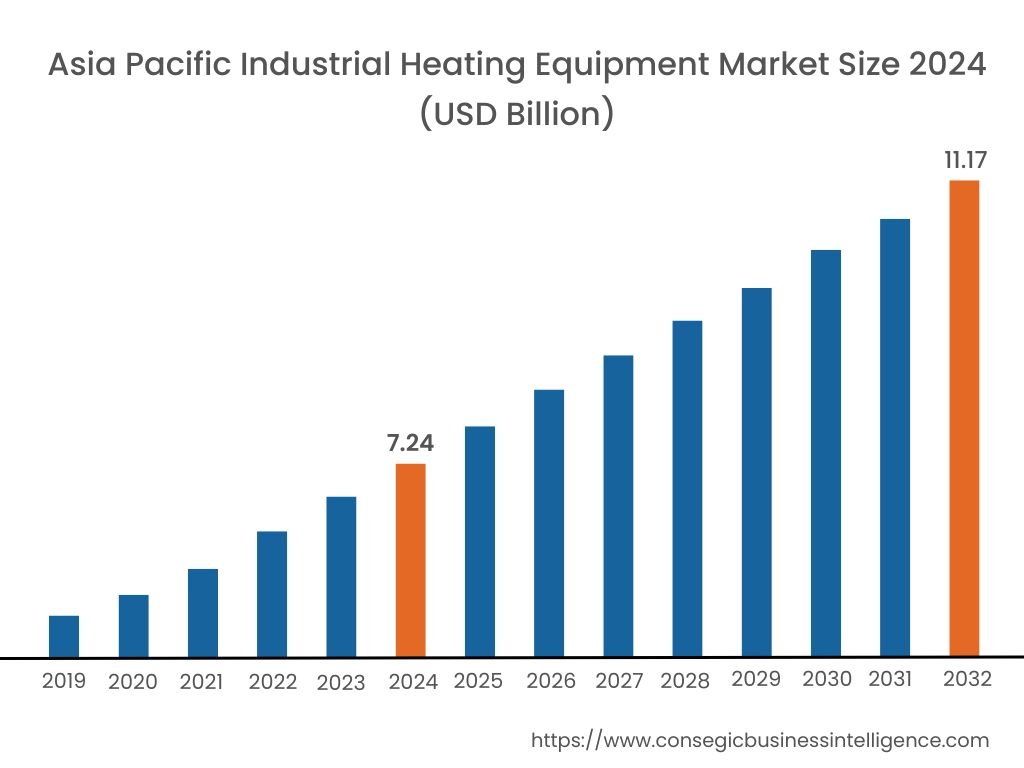

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

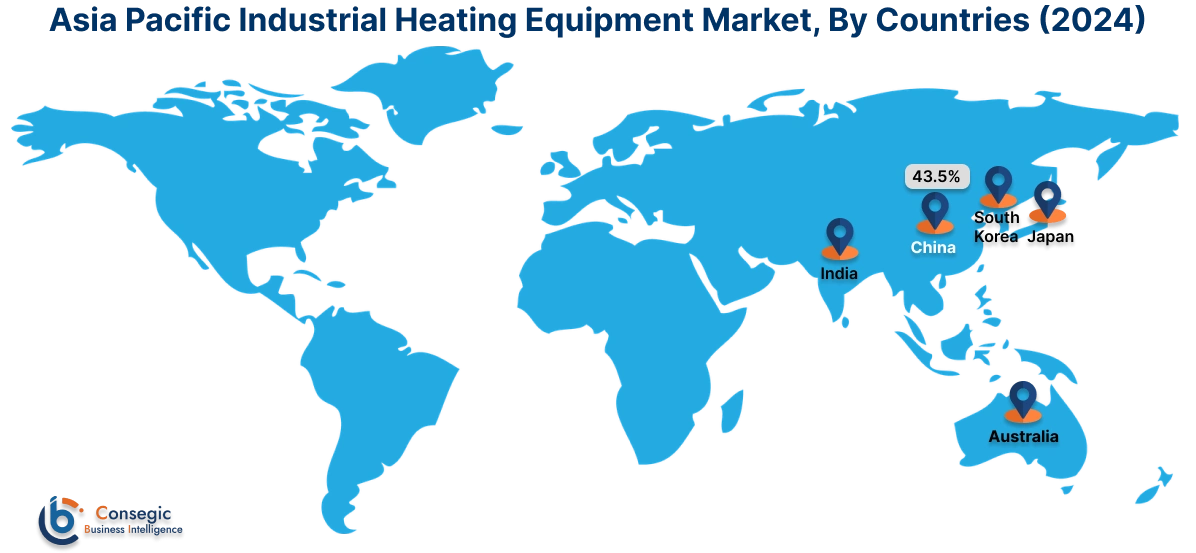

Asia Pacific region was valued at USD 7.24 Billion in 2024. Moreover, it is projected to grow by USD 7.51 Billion in 2025 and reach over USD 11.17 Billion by 2032. Out of this, China accounted for the maximum revenue share of 43.5%. Asia-Pacific is experiencing rapid growth in the industrial heating equipment industry, propelled by rapid industrialization, rising energy consumption, and growing domestic manufacturing output. China, India, Japan, and South Korea dominate the region, driven by strong government backing for industrial expansion and infrastructure development. The need to meet increasing production capacity while improving energy use efficiency has elevated the role of modern heating technologies across sectors such as textiles, mining, and petrochemicals. Regional analysis highlights significant investments in both electric and gas-fired systems, with growing interest in digital monitoring and predictive maintenance features. The combination of growing industrial footprints and environmental policy evolution creates a robust industrial heating equipment market opportunity across both developed and emerging markets in the region.

North America is estimated to reach over USD 10.06 Billion by 2032 from a value of USD 6.66 Billion in 2024 and is projected to grow by USD 6.89 Billion in 2025. North America maintains a leading position in the market, driven by strong industrial infrastructure, emphasis on energy efficiency, and robust investments in modernization. The United States and Canada benefit from high demand in sectors such as automotive, aerospace, and metal fabrication, where precise thermal control and sustainability are critical. Market analysis reveals increased integration of electric and induction-based heating solutions to support cleaner operations and reduce carbon emissions. Regulatory pressure on fossil-fueled heating systems, combined with incentives for clean energy adoption, continues to push the need for high-efficiency industrial heating technologies across new and retrofit applications.

Europe remains at the forefront of innovation in industrial heating technologies, largely due to stringent environmental regulations and a strong commitment to industrial decarbonization. Countries like Germany, France, Italy, and the Nordic nations are investing heavily in electrified heating systems, particularly in chemical processing, glass manufacturing, and food production. Analysis suggests that the region's market growth is supported by a clear policy direction toward carbon-neutral production, fostering the need for renewable-powered and hybrid heating solutions. Moreover, Europe’s focus on circular economy practices and digital automation further supports the integration of advanced thermal control systems in continuous manufacturing environments.

Latin America’s market is gradually expanding, particularly in countries like Brazil, Mexico, and Argentina, where food processing, cement production, and mining sectors play a major role in industrial output. While adoption of advanced systems is still evolving, regional growth is supported by modernization efforts, rising energy prices, and interest in renewable integration. Research indicates that demand is shifting from conventional heating equipment to more efficient and cleaner technologies, particularly in urban industrial centers. However, challenges such as financing limitations and fluctuating regulatory frameworks may moderate the adoption pace unless supported by long-term policy commitments and public-private partnerships.

In the Middle East and Africa, industrial heating equipment adoption is driven primarily by the expansion of industrial zones, petrochemical operations, and construction-related manufacturing. Gulf countries like the UAE and Saudi Arabia are deploying advanced heating solutions in energy-intensive sectors while simultaneously pursuing diversification away from oil dependency. In sub-Saharan Africa, infrastructure development and regional industrialization initiatives are fueling incremental market activity. Analysis points to growing interest in cost-effective and scalable thermal systems that can address local power constraints while supporting production resilience. The region’s long-term growth potential depends on improving access to capital, skilled labor, and technical support for advanced industrial systems.

Top Key Players & Market Share Insights:

The industrial heating equipment market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global industrial heating equipment market. Key players in the industrial heating equipment industry include -

- Robert Bosch GmbH (Germany)

- Daikin Industries Ltd. (Japan)

- Danfoss A/S (Denmark)

- Fujitsu Limited (Japan)

- Electrolux AB (Sweden)

- Viessmann Group (Germany)

- Vaillant Group (Germany)

- Ariston Thermo Group (Italy)

- Bharat Heavy Electricals Limited (BHEL) (India)

- Mitsubishi Electric Corporation (Japan)

Recent Industry Developments :

Acquisition:

- In September 2024, TransTech Group acquired the North American business, Koch Heat Transfer (KHT), a global leader in the design and manufacture of heat transfer equipment and technologies, through its subsidiary Metalforms. This decision elevates the ability of the company to deliver comprehensive heat transfer solutions to customers, including new, cutting-edge technologies.

Partnerships:

- In March 2023, the Viessmann Group and Keyter Technologies S.L. entered a strategic partnership for further growth opportunities, including investment in the construction of a new plant.

Industrial Heating Equipment Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 36.68 Billion |

| CAGR (2025-2032) | 5.1% |

| By Product Type |

|

| By Operation Type |

|

| By Fuel Type |

|

| By End Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Industrial Heating Equipment Market? +

Industrial Heating Equipment Market size is estimated to reach over USD 36.68 Billion by 2032 from a value of USD 24.60 Billion in 2024 and is projected to grow by USD 25.42 Billion in 2025, growing at a CAGR of 5.1% from 2025 to 2032.

What specific segmentation details are covered in the Industrial Heating Equipment Market report? +

The Industrial Heating Equipment market report includes specific segmentation details for product type, operation type, fuel type and end-use industry.

What are the end-use industries in the Industrial Heating Equipment Market? +

The end-use industries of the Industrial Heating Equipment Market are chemicals, oil & gas, food & beverage, mining, automotive, power generation, electronics & semiconductors, pharmaceuticals, textiles, aerospace & defense and others.

Who are the major players in the Industrial Heating Equipment Market? +

The key participants in the Industrial Heating Equipment market are Robert Bosch GmbH (Germany), Daikin Industries Ltd. (Japan), Viessmann Group (Germany), Vaillant Group (Germany), Ariston Thermo Group (Italy), Bharat Heavy Electricals Limited (BHEL) (India), Mitsubishi Electric Corporation (Japan), Danfoss A/S (Denmark), Fujitsu Limited (Japan) and Electrolux AB (Sweden).