- Summary

- Table Of Content

- Methodology

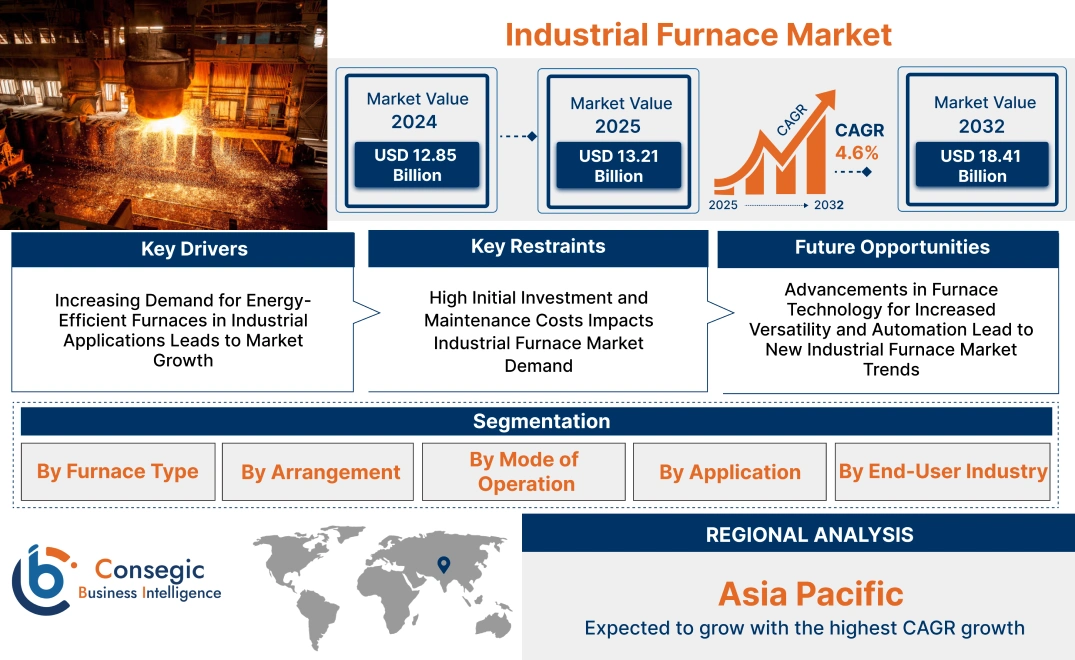

Industrial Furnace Market Size:

Industrial Furnace Market size is estimated to reach over USD 18.41 Billion by 2032 from a value of USD 12.85 Billion in 2024 and is projected to grow by USD 13.21 Billion in 2025, growing at a CAGR of 4.6% from 2025 to 2032.

Industrial Furnace Market Scope & Overview:

An industrial furnace is a high-temperature heating system used for metal processing, material treatment, and chemical reactions in manufacturing. It operates through combustion or electrical energy to generate controlled heat. These furnaces provide precise temperature control, energy efficiency, and durability, ensuring consistent performance in industrial applications.

The benefits of industrial furnaces include improved production efficiency, reduced operational costs, and enhanced material quality. They enable uniform heating, minimizing defects in processed materials. Their advanced automation features support optimized energy consumption and safer working conditions.

Industrial furnaces are widely used in steel, automotive, aerospace, and glass industries. They support applications such as metal casting, heat treatment, and smelting, ensuring high-performance output in manufacturing operations.

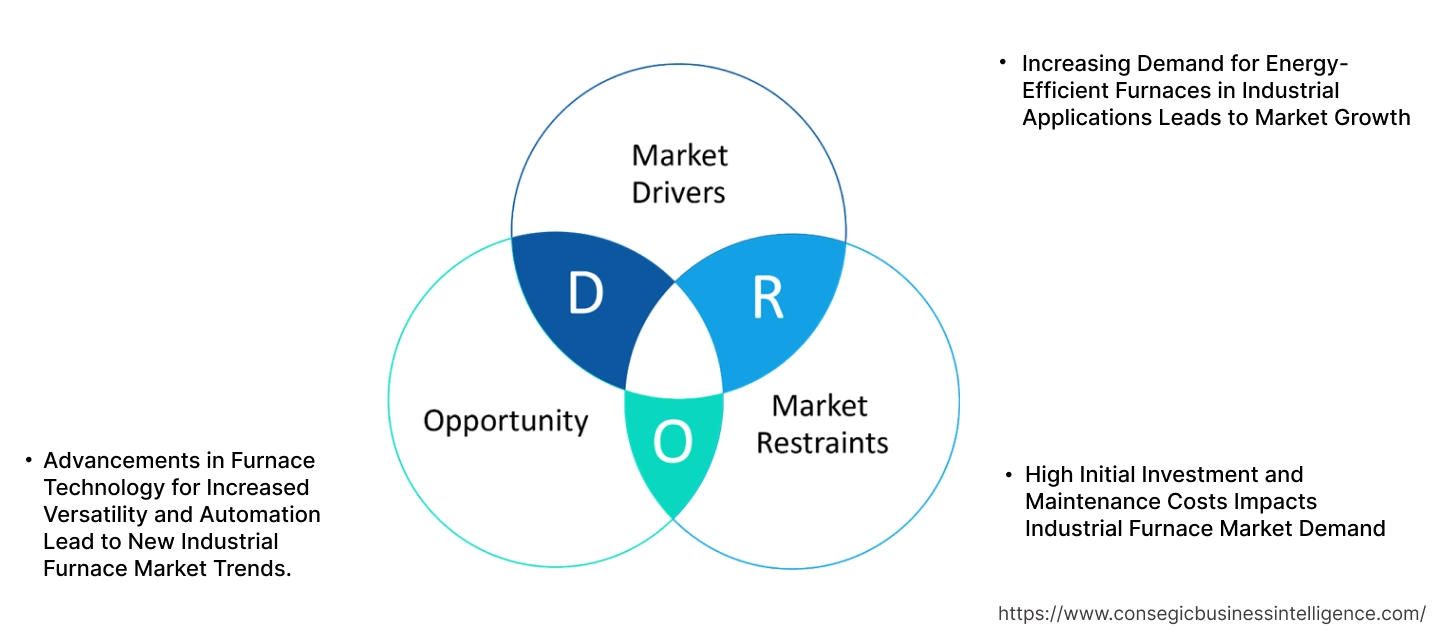

Industrial Furnace Market Dynamics - (DRO) :

Key Drivers:

Increasing Demand for Energy-Efficient Furnaces in Industrial Applications Leads to Market Growth

Energy efficiency is a critical factor for industries aiming to reduce operational costs and minimize environmental impact. Industrial furnaces, particularly those used in metal processing and ceramics manufacturing, are adopting advanced technologies that improve thermal efficiency, reduce energy consumption, and lower emissions. The integration of energy-saving solutions, such as regenerative burners and high-efficiency heat exchangers, allows industries to optimize fuel usage and minimize waste heat loss. As industries continue to prioritize sustainability and cost-efficiency, the demand for energy-efficient industrial furnaces is expected to rise.

Thus, the growing emphasis on energy efficiency across industrial sectors is driving the market forward.

Key Restraints:

High Initial Investment and Maintenance Costs Impacts Industrial Furnace Market Demand

Industrial furnaces often require substantial upfront investments due to their high-tech features, complex designs, and customizations tailored to specific industrial needs. This initial capital expenditure can be a significant hurdle, especially for small and medium enterprises (SMEs) with limited budgets. Furthermore, the ongoing maintenance and operational costs associated with these systems, including regular inspections, repairs, and spare parts, can deter potential customers from investing in industrial furnaces. The financial burden of both initial costs and maintenance requirements may limit adoption, particularly in regions with tight industrial budgets.

These high costs create a barrier to the widespread adoption of industrial furnaces, particularly among smaller players in the market.

Future Opportunities :

Advancements in Furnace Technology for Increased Versatility and Automation Lead to New Industrial Furnace Market Trends.

The market stands to benefit from continued technological advancements, particularly in automation and process control. The integration of smart technologies such as artificial intelligence (AI) and the Internet of Things (IoT) can improve furnace operation efficiency by enabling real-time monitoring, predictive maintenance, and process optimization. These innovations allow for more precise control over temperature, atmosphere, and energy use, which can significantly enhance productivity and reduce costs. As these technologies evolve, they are expected to open new industrial furnace market opportunities for industrial furnaces in various sectors, including aerospace, automotive, and construction materials.

Therefore, the continued development and integration of smart technologies into industrial furnaces present significant industrial furnace market opportunities for growth.

Industrial Furnace Market Segmental Analysis :

By Furnace Type:

Based on furnace type, the market is segmented into electric furnaces and gas/burner-operated furnaces.

The electric furnace sector accounted for the largest revenue industrial furnace market share in 2024.

- Electric furnaces utilize electrical energy to generate heat, eliminating the need for combustion-based fuel sources.

- These furnaces are widely used due to their high energy efficiency, lower carbon emissions, and precise temperature control, making them suitable for various industrial applications.

- They provide improved operational flexibility and reduced maintenance compared to gas-operated counterparts.

- Stringent environmental regulations favoring eco-friendly heating solutions contribute to their increased adoption.

- Therefore, according to industrial furnace market analysis, the trend for electric furnaces is significantly increasing across various industries.

The gas/burner-operated furnace sector is anticipated to register the fastest CAGR during the forecast period.

- Gas/burner-operated furnaces are preferred for high-temperature applications, offering robust performance in metallurgy, steel production, and other heavy industries.

- These furnaces provide faster heating cycles and high thermal efficiency, making them ideal for large-scale manufacturing operations.

- The availability of cost-effective fuel options and advancements in burner technology enhance their efficiency and operational capabilities.

- Thus, according to industrial furnace market analysis, the adoption of gas/burner-operated furnaces is increasing in industries requiring high-temperature processing.

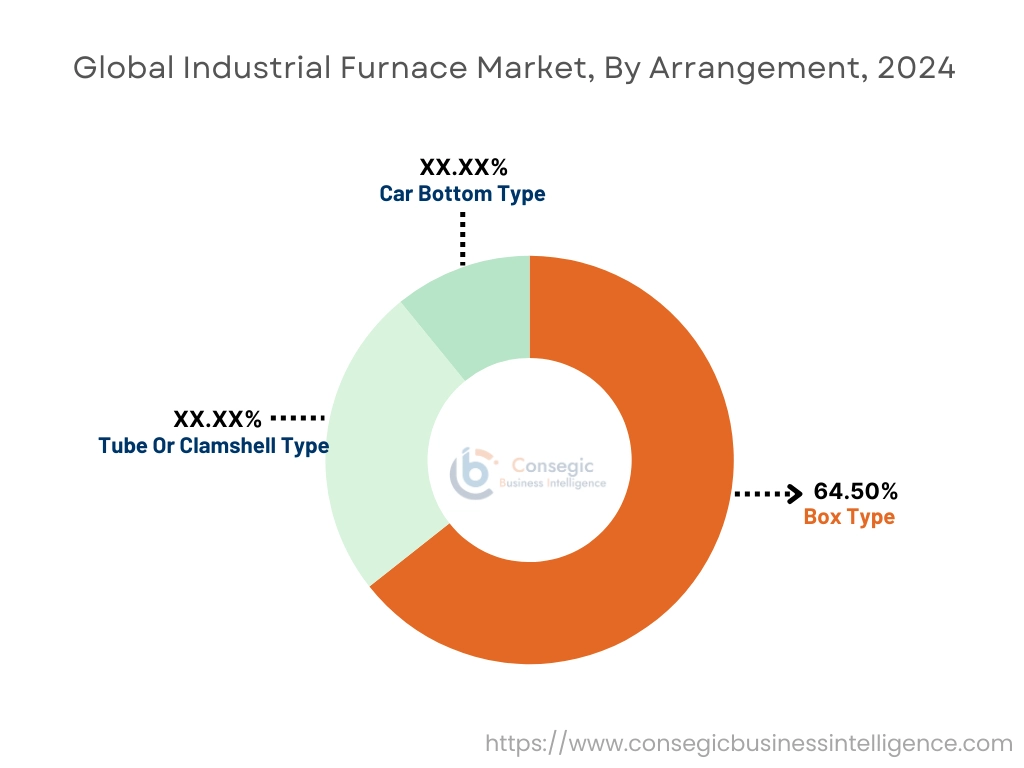

By Arrangement:

Based on arrangement, the market is segmented into box type, tube or clamshell type, and car bottom type.

The box-type furnace sector accounted for the largest revenue in industrial furnace market share by 64.50% in 2024.

- Box-type furnaces are enclosed heating chambers designed for uniform heat distribution, ensuring consistent processing of materials.

- They are widely used in heat treatment applications, such as annealing, tempering, and hardening in metallurgy and steel production.

- These furnaces provide better temperature uniformity and enhanced safety, making them a preferred choice in various industries.

- Therefore, according to the market analysis, increasing trend for reliable and efficient heat treatment processes contributes to the widespread adoption of box-type furnaces.

The tube or clamshell-type furnace sector is anticipated to register the fastest CAGR during the forecast period.

- Tube or clamshell-type furnaces offer high-temperature capabilities and precise control over thermal processes.

- These furnaces are extensively used in laboratory research, semiconductor manufacturing, and specialized industrial applications requiring controlled heating.

- Advancements in thermal processing technology and increasing industrial furnace market demand for precision heating solutions drive their adoption.

- Thus, according to the market analysis, the tube or clamshell-type furnace market is expected to expand at a rapid pace.

By Mode of Operation:

Based on mode of operation, the market is segmented into batch type and continuous type.

The continuous-type furnace sector accounted for the largest revenue share in 2024.

- Continuous-type furnaces enable uninterrupted processing, reducing operational downtime and enhancing efficiency in industrial applications.

- These furnaces are primarily used in large-scale manufacturing industries, including steel production and metallurgy, where high throughput is required.

- Automation integration in continuous-type furnaces enhances productivity and operational consistency.

- Therefore, according to the market analysis, the increasing emphasis on high-efficiency production processes supports the growth of continuous-type furnaces.

The batch-type furnace sector is anticipated to register the fastest CAGR during the forecast period.

- Batch-type furnaces allow processing of specific quantities of materials per cycle, making them suitable for specialized and custom production needs.

- They provide greater flexibility in handling various materials and applications, such as heat treatment, sintering, and annealing.

- Growing trend for customized and small-batch industrial processing contributes to the industrial furnace market expansion of batch-type furnaces.

- Thus, according to the market analysis, the batch-type furnace segment is witnessing rapid growth in industries requiring versatile thermal processing solutions.

By Application:

Based on application, the market is segmented into atmosphere and vacuum applications.

The atmosphere furnace sector accounted for the largest revenue share in 2024.

- Atmosphere furnaces operate under controlled gas environments, ensuring oxidation-free heating processes.

- These furnaces are used in various heat treatment applications, including carburizing, nitriding, and annealing in the automotive and metallurgy industries.

- Their ability to provide uniform heating while maintaining material integrity drives their adoption across multiple sectors.

- Therefore, according to the market analysis, the demand for atmosphere furnaces remains high in industrial applications.

The vacuum furnace sector is anticipated to register the fastest CAGR during the forecast period.

- Vacuum furnaces eliminate contamination and oxidation, offering superior quality for high-precision applications.

- They are widely used in aerospace, medical, and electronics industries for processing materials that require a high-purity environment.

- Advancements in vacuum furnace technology and increasing trend for high-performance materials drive industrial furnace market growth.

- Thus, according to the market analysis, the vacuum furnace sector is experiencing significant expansion in industrial applications.

By End-User Industry:

Based on end-user industry, the market is segmented into automotive manufacturing, oil and gas, metallurgy, steel and iron production, and food processing.

The steel and iron production sector accounted for the largest revenue share in 2024.

- Industrial furnaces play a crucial role in steelmaking, iron smelting, and refining processes.

- The ask for high-quality steel in construction, automotive, and infrastructure industries drives the need for efficient furnace solutions.

- Continuous advancements in furnace technology, including energy-efficient solutions, further boost adoption in this sector.

- Therefore, according to the market analysis, steel and iron production remains the dominant end-user segment for industrial furnaces.

The automotive manufacturing sector is anticipated to register the fastest CAGR during the forecast period.

- Automotive manufacturers use industrial furnaces for heat treatment of metal components, enhancing strength and durability.

- The shift towards electric vehicles (EVs) and lightweight materials requires advanced heat treatment solutions, increasing need for industrial furnaces.

- Growing investments in automotive production facilities further accelerate industrial furnace market growth in this segment.

- Thus, according to the market analysis, the automotive manufacturing sector is witnessing rapid expansion in industrial furnace applications.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

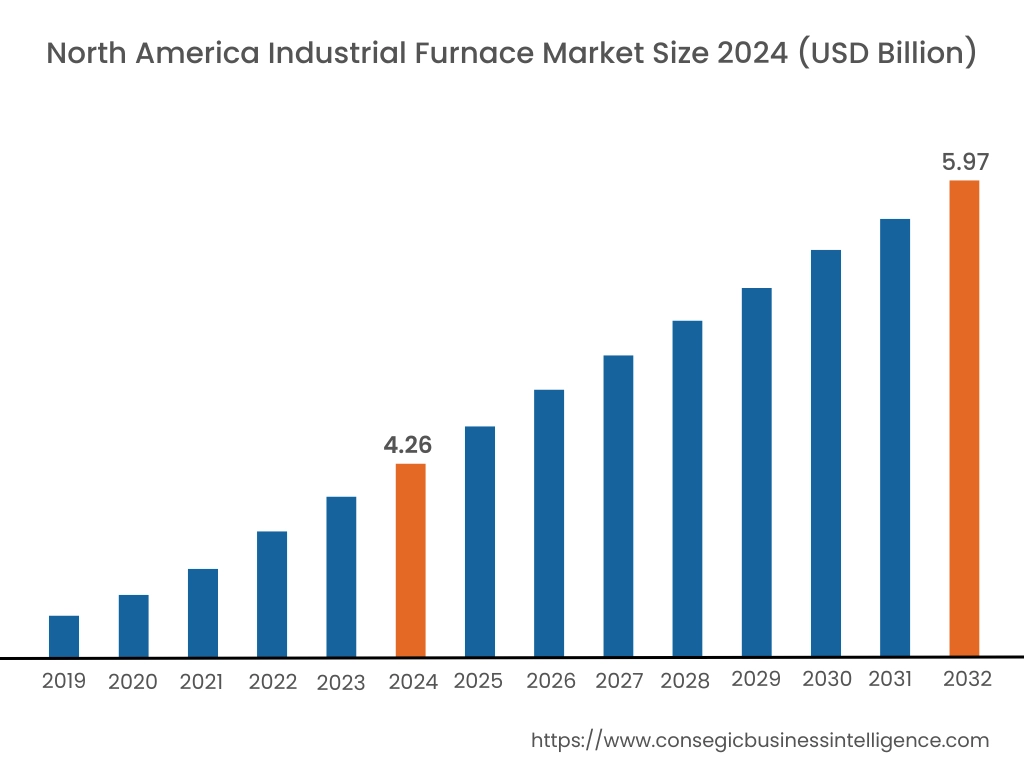

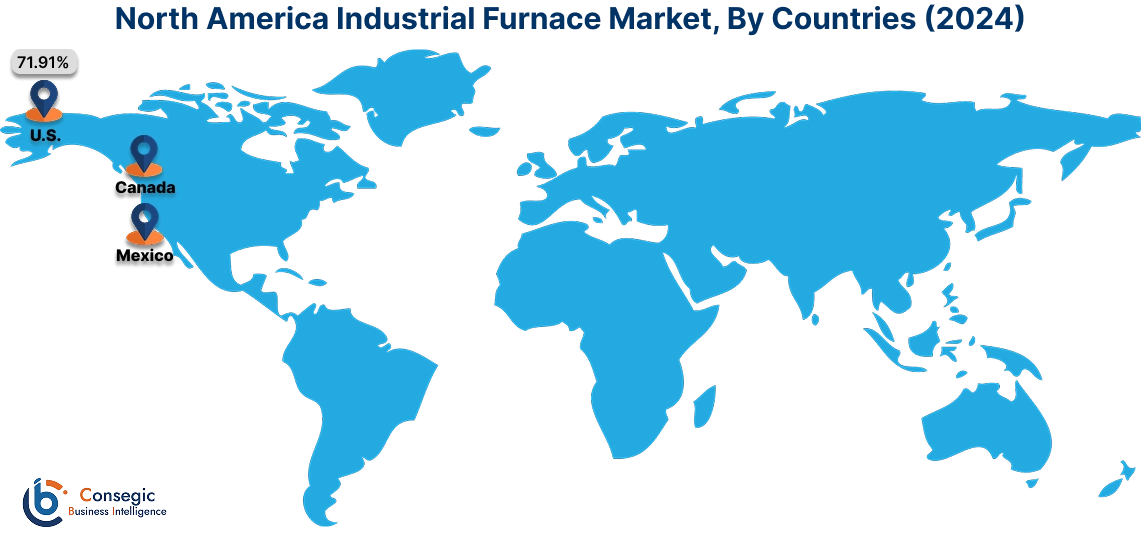

In 2024, North America was valued at USD 4.26 Billion and is expected to reach USD 5.97 Billion in 2032. In North America, the U.S. accounted for the highest share of 71.91% during the base year of 2024. The industrial furnace market in North America, particularly in the United States, is experiencing strong demand, mainly from the manufacturing and metal processing industries. The presence of key manufacturers and advanced technological solutions supports market development. The region's high investments in the automotive and aerospace sectors contribute to an increasing need for industrial furnaces. Additionally, stringent regulations related to energy efficiency and environmental concerns are prompting the adoption of more efficient and sustainable furnace technologies.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 5.0% over the forecast period. Asia-Pacific is the leading region in the industrial furnace market, driven by industrialization in countries like China, India, and Japan. The requirement for industrial furnaces is high in sectors such as steel production, automotive, and electronics. China, being a major manufacturer of steel and other metals, represents a significant portion of the market. Government initiatives to promote energy-efficient technologies and advancements in furnace design further stimulate market performance. The growing infrastructure sector across the region also supports the demand for industrial furnaces.

In Europe, countries like Germany, Italy, and the United Kingdom are key contributors to the industrial furnace market. The region’s demand for industrial furnaces is driven by its well-established industries, including automotive, metallurgy, and ceramics. Additionally, Europe’s focus on reducing carbon emissions and promoting energy efficiency is boosting the adoption of eco-friendly furnace technologies. The presence of major industrial furnace manufacturers in the region also supports a competitive market landscape, with continuous innovation and improvements in furnace performance.

The Middle East and Africa region is witnessing a growing need for industrial furnaces, particularly in countries like Saudi Arabia, the UAE, and South Africa. The ask is primarily fueled by sectors such as petrochemicals, metal manufacturing, and energy production. The ongoing industrialization in these regions, driven by diversification efforts in countries like Saudi Arabia and the UAE, has led to an increased focus on upgrading furnace technologies. The need for energy-efficient and cost-effective furnaces in these rapidly expanding industries enhances market performance.

In Latin America, the industrial furnace market is expanding, particularly in Brazil and Mexico, driven by the growth in the automotive, steel, and energy sectors. The increasing need for metal processing and manufacturing in these regions supports the adoption of advanced industrial furnaces. Additionally, Latin American countries are investing in infrastructure development and industrial upgrades, further contributing to the market’s performance. However, challenges such as economic instability and fluctuating demand from key sectors may influence overall industrial furnace market trends in the region.

Top Key Players & Market Share Insights:

The Global Industrial Furnace Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global Industrial Furnace Market. Key players in the Industrial Furnace industry include-

- Inductotherm Corp. (United States)

- Lindberg/MPH (United States)

- Elexxion GmbH (Germany)

- ANDRITZ AG (Austria)

- Erdemir Group (Turkey)

- SECO/WARWICK S.A. (Poland)

- Tenova S.p.A. (Italy)

- Fives Group (France)

- Cicada Industrial Furnace Co., Ltd. (China)

- L&L Special Furnace Co., Inc. (United States)

Industrial Furnace Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 18.41 Billion |

| CAGR (2025-2032) | 4.6% |

| By Furnace Type |

|

| By Arrangement |

|

| By Mode of Operation |

|

| By Application |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Industrial Furnace Market? +

In 2024, the Industrial Furnace Market was USD 12.85 Billion.

What will be the potential market valuation for the Industrial Furnace Market by 2032? +

In 2032, the market size of Industrial Furnace Market is expected to reach USD 18.41 Billion.

What are the segments covered in the Industrial Furnace Market report? +

The furnace type, arrangement, mode of operation, application, and end-user industry are the segments covered in this report.

Who are the major players in the Industrial Furnace Market? +

Inductotherm Corp. (United States), Lindberg/MPH (United States), SECO/WARWICK S.A. (Poland), Tenova S.p.A. (Italy), Fives Group (France), Cicada Industrial Furnace Co., Ltd. (China), L&L Special Furnace Co., Inc. (United States), Elexxion GmbH (Germany), ANDRITZ AG (Austria), Erdemir Group (Turkey) are the major players in the Industrial Furnace market.