- Summary

- Table Of Content

- Methodology

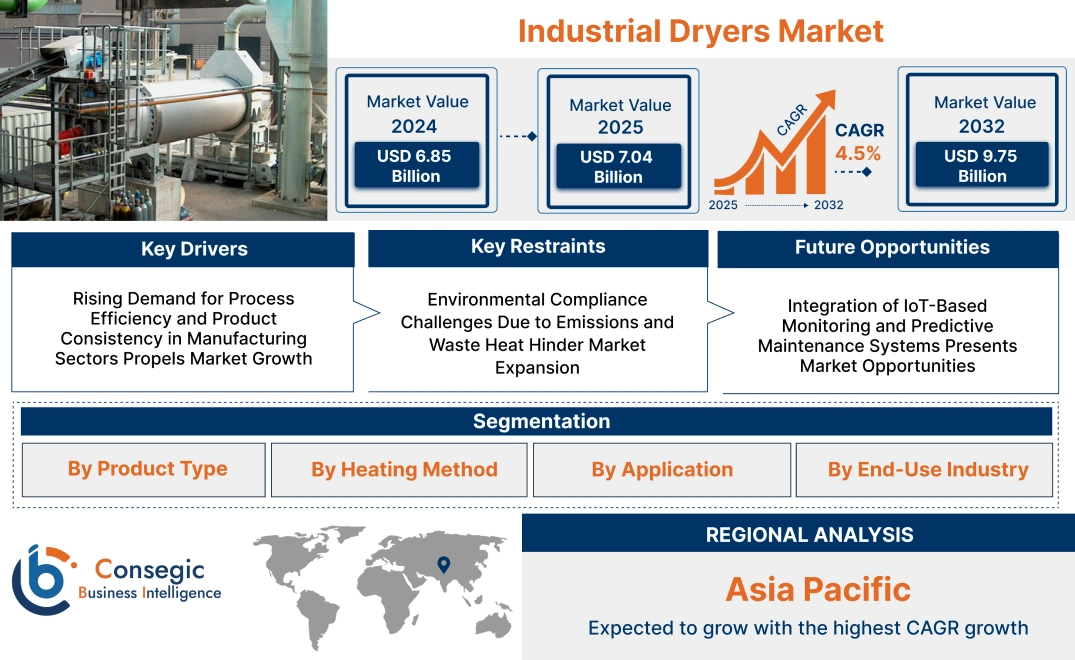

Industrial Dryers Market Size:

Industrial Dryers Market size is estimated to reach over USD 9.75 Billion by 2032 from a value of USD 6.85 Billion in 2024 and is projected to grow by USD 7.04 Billion in 2025, growing at a CAGR of 4.5% from 2025 to 2032.

Industrial Dryers Market Scope & Overview:

Industrial dryers are tailor-made machinery aimed at the drying of bulk products by evaporation or thermal processing. Common to industries like food processing, drugs, chemicals, textiles, and minerals, industrial dryers provide for controlled solids, liquids, or slurry material drying.

Major technologies are rotary, spray, fluidized bed, freeze, and tray dryers—each designed to accommodate particular material characteristics and process needs. Temperature control, airflow management, automated operation, and energy recovery systems add to operational accuracy and efficiency.

Industrial dryers provide advantages such as uniform moisture elimination, increased shelf life of products, and uniformity of process. Their design facilitates high flow rate, minimal heat degradation, and simple integration into continuous or batch production systems. Industrial dryers are an integral part of enhancing product quality, maximizing the use of resources, and ensuring industry-specific standard compliance, hence their importance to contemporary manufacturing and material processing operations.

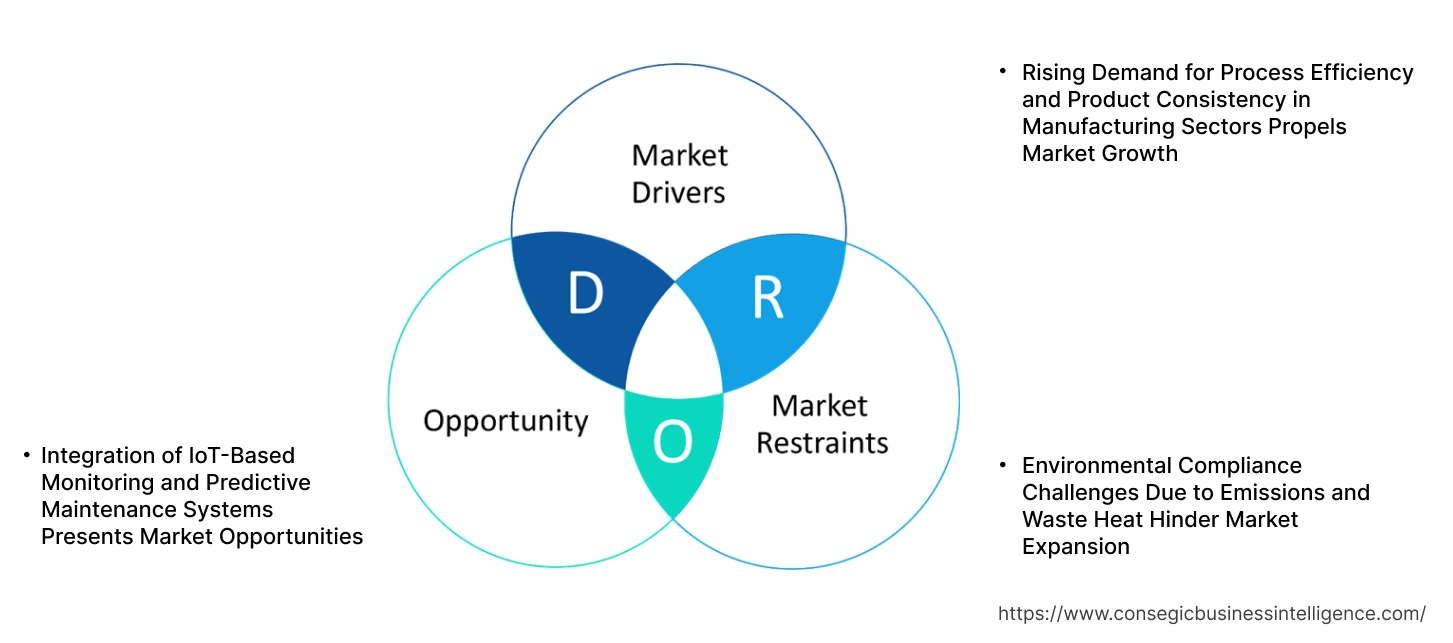

Industrial Dryers Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Process Efficiency and Product Consistency in Manufacturing Sectors Propels Market Growth

Industrial processes like food processing, chemicals, and pharmaceuticals need consistent and accurate moisture control to ensure product quality and process reliability. Industrial dryers are essential in eliminating moisture from raw materials, intermediates, and finished products, ensuring stability, shelf life, and conformity to product specifications. Rotary, fluidized bed, and spray dryers are progressively used for high throughput, continuous operation, and flexibility to handle different material texture and moisture contents. These plants enhance process yield, shorten drying time, and reduce manual involvement, which conform to lean manufacturing and quality control requirements. As production lines become longer and automation becomes the norm, manufacturers are investing in energy-efficient drying technology to improve operations. The need for scalable, consistent drying results is propelling long-term industrial dryers market expansion.

Hence, the rising advancements in 3D printing are proliferating the Industrial Dryers Market size.

Key Restraints:

Environmental Compliance Challenges Due to Emissions and Waste Heat Hinder Market Expansion

Drying operations produce particulate emissions, volatile organic compounds (VOCs), and high volumes of hot exhaust air that need to be controlled to satisfy environmental regulations. Plants without efficient heat recovery systems or emissions control technologies have trouble complying with air quality standards. The necessity of installing scrubbers, dust collectors, and thermal oxidizers raises capital and maintenance expenses, especially in older facilities. In applications like chemicals, textiles, and food ingredients where organic residues are involved, emissions control is even more challenging. Carbon reduction targets and regulatory pressure are encouraging industries to transition to cleaner drying technologies, but many operators cannot afford retrofitting time or costs. These compliance issues are limiting system deployment in high-emission applications, particularly in developing countries where enforcement infrastructure is limited. Even with increased demand for high-end drying systems, regulatory overhead and emissions-based limitations still hamper industrial dryers market growth.

Future Opportunities :

Integration of IoT-Based Monitoring and Predictive Maintenance Systems Presents Market Opportunities

IoT-enabled industrial dryers are revolutionizing process control by allowing real-time tracking of key parameters like inlet and outlet temperature, humidity, motor speed, and power consumption. The systems enable operators to dynamically manipulate drying conditions and identify anomalies prior to equipment failure. Predictive maintenance using sensor data and machine learning reduces unplanned downtime, decreases maintenance expenses, and increases asset utilization. Cloud connectivity enables centralized monitoring in multi-site operations, and trends in historical data assist with maximizing batch performance. There is increasing demand for more intelligent, networked drying solutions among producers seeking to maximize efficiency, minimize waste, and achieve Industry 4.0 standards. As automation grows in process industries, vendors with integrated control dashboards, remote diagnosis, and adaptive controls are gaining competitive momentum.

- For instance, in April 2023, Dialog Enterprise, in collaboration with the Rubber Research Institute of Sri Lanka & Dialog University of Moratuwa Research Laboratory, developed and launched an IoT-led implementation to assist local rubber plantations. The solution allows continuous real-time monitoring of temperature and humidity within drying chambers to maintain optimal conditions for best yield.

The intersection of thermal processing and digital monitoring is generating robust industrial dryers market opportunities fueled by both technological development and operational needs.

Industrial Dryers Market Segmental Analysis :

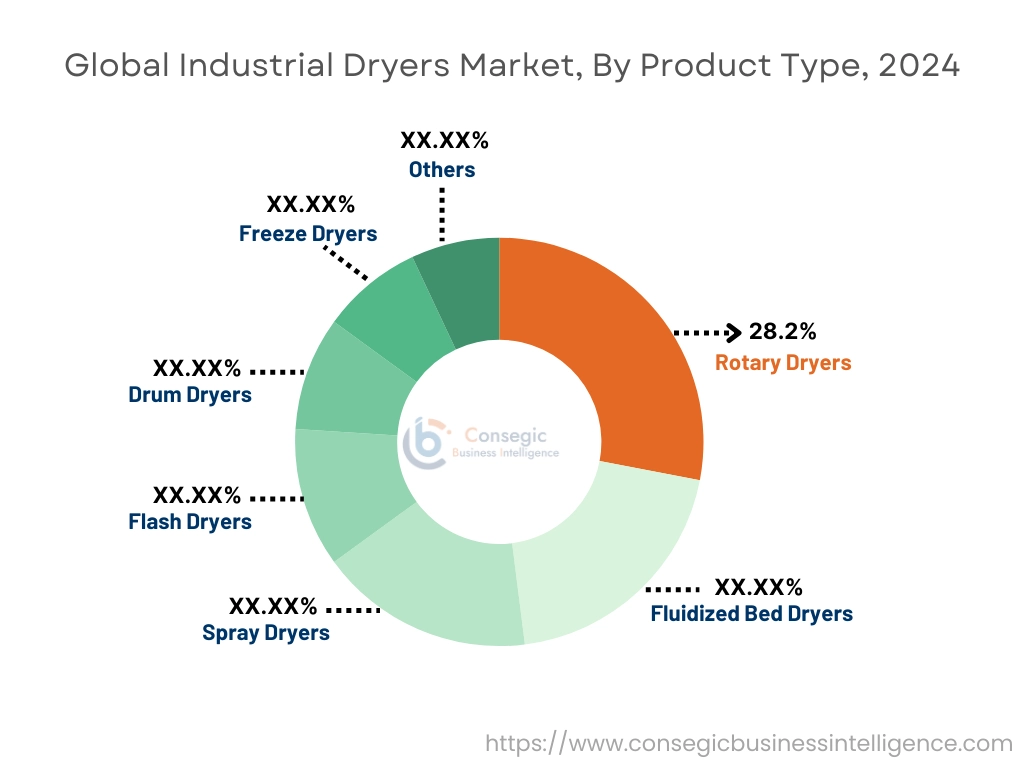

By Product Type:

Based on product type, the market is segmented into rotary dryers, fluidized bed dryers, spray dryers, flash dryers, drum dryers, freeze dryers, and others.

The rotary dryers segment accounted for the largest industrial dryers market share of 28.2% in 2024.

- Rotary dryers are extensively used across multiple industries for bulk solids processing due to their high capacity and operational flexibility.

- Their rugged construction and adaptability to various materials make them suitable for drying minerals, fertilizers, and biomass.

- These systems support both co-current and counter-current drying configurations, depending on the thermal sensitivity of the product.

- As per the industrial dryers market analysis, the segment maintains its lead due to widespread deployment in the cement, mining, and chemical sectors.

The spray dryers segment is projected to witness the fastest CAGR during the forecast period.

- Spray dryers are ideal for transforming liquid feed into dry powder, especially in food, dairy, and pharmaceutical applications.

- The rising need for powdered products such as infant formula, coffee, and pharmaceutical excipients is boosting adoption.

- Technological advancements in nozzle design and temperature control enhance product consistency and energy efficiency.

- According to industrial dryers market trends, increased demand for high-value powders with controlled particle size drives rapid growth in spray dryer systems.

By Heating Method:

Based on heating method, the industrial dryers market is segmented into direct heating, indirect heating, and hybrid heating.

The direct heating segment accounted for the largest market share in 2024.

- Direct dryers offer rapid heat transfer and lower installation costs, making them suitable for high-volume industrial processes.

- This method is extensively used in cement, mining, and food industries where speed and throughput are priorities.

- Gas-fired systems are common in direct heating, offering robust operation in continuous processes.

- As per the industrial dryers market analysis, direct heating dominates due to its simplicity and widespread adoption in heavy industries.

The hybrid heating segment is expected to grow at the fastest CAGR during the forecast period.

- Hybrid systems combine direct and indirect heat sources, enabling greater control over drying parameters for sensitive materials.

- These systems are particularly useful in applications requiring energy optimization and product quality consistency.

- Growing energy efficiency regulations and product-specific quality requirements are encouraging hybrid dryer development.

- Industrial dryers market expansion in the specialty chemical and pharmaceutical sectors is driving hybrid system innovation.

By Application:

Based on application, the market is segmented into granulation, moisture removal, solvent recovery, product preservation, and others.

The moisture removal segment held the largest industrial dryers market share in 2024.

- Moisture removal is the core function of industrial dryers, applicable across nearly all end-use industries.

- Effective drying extends product shelf life, enhances processing stability, and improves transportability.

- This segment includes diverse processes from dewatering in food to material conditioning in construction materials.

- As per industrial dryers market trends, continued improvements in energy-efficient drying systems support strong segment performance.

The solvent recovery segment is projected to see the fastest CAGR during the forecast period.

- Solvent recovery is essential in pharmaceutical and chemical manufacturing, where solvent reuse lowers costs and environmental impact.

- Dryers with integrated recovery systems reduce emissions and improve process sustainability.

- Vacuum and freeze dryers are particularly relevant in this application due to their controlled low-temperature environment.

- As regulations on VOC emissions tighten globally, the industrial dryers market demand for solvent recovery solutions is rising.

By End Use Industry:

Based on end-use industry, the industrial dryers market is segmented into food & beverage, pharmaceuticals, chemicals, fertilizers, cement, textiles, and others.

The food & beverage segment accounted for the largest revenue share in 2024.

- Dryers are used extensively in food processing for drying fruits, vegetables, dairy products, and ready-to-eat meals.

- The rising requirement for packaged and convenience foods supports continued investments in hygienic, high-capacity drying systems.

- Spray, drum, and freeze dryers are popular in this segment due to their ability to retain flavor, nutrition, and texture.

- Thus, the industrial dryers market demand is bolstered by changing consumer lifestyles, which require greater shelf life in consumable products.

The pharmaceuticals segment is projected to register the fastest CAGR during the forecast period.

- Pharmaceutical manufacturing relies on drying for product formulation, stabilization, and packaging of sensitive materials.

- Freeze drying (lyophilization) is gaining traction due to its efficacy in preserving biologicals and injectable drugs.

- Regulatory mandates for aseptic processing and material integrity are driving equipment upgrades and adoption.

- Therefore, rising R&D and biologics production are accelerating dryer usage in the sector and driving the industrial dryers market growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

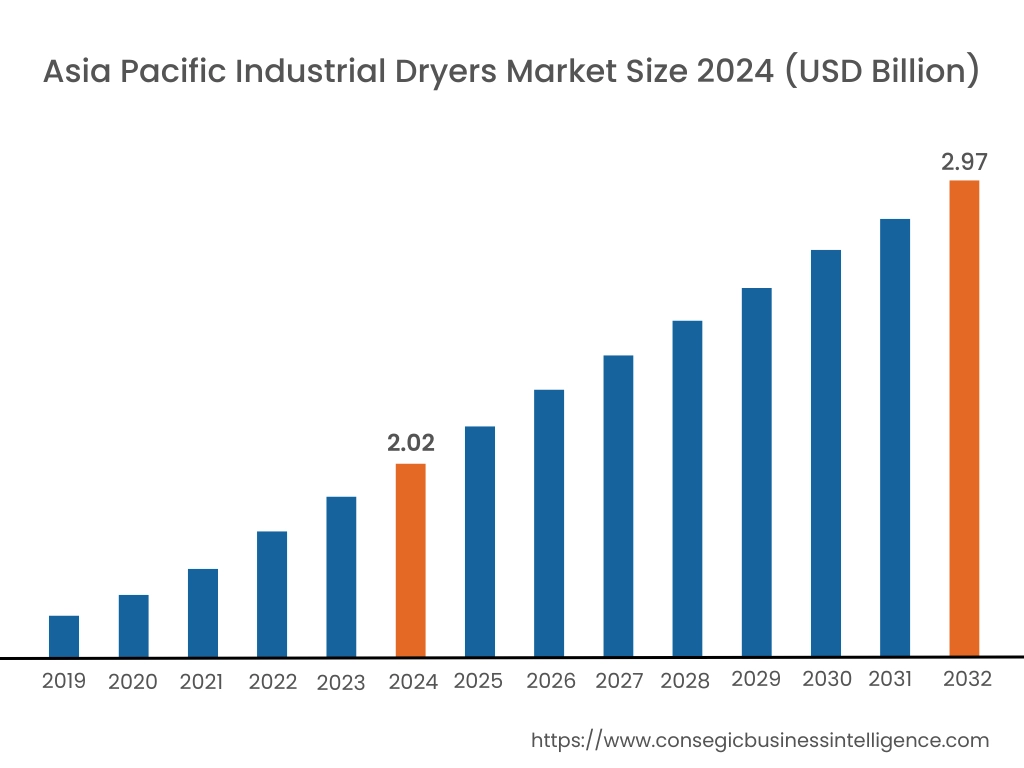

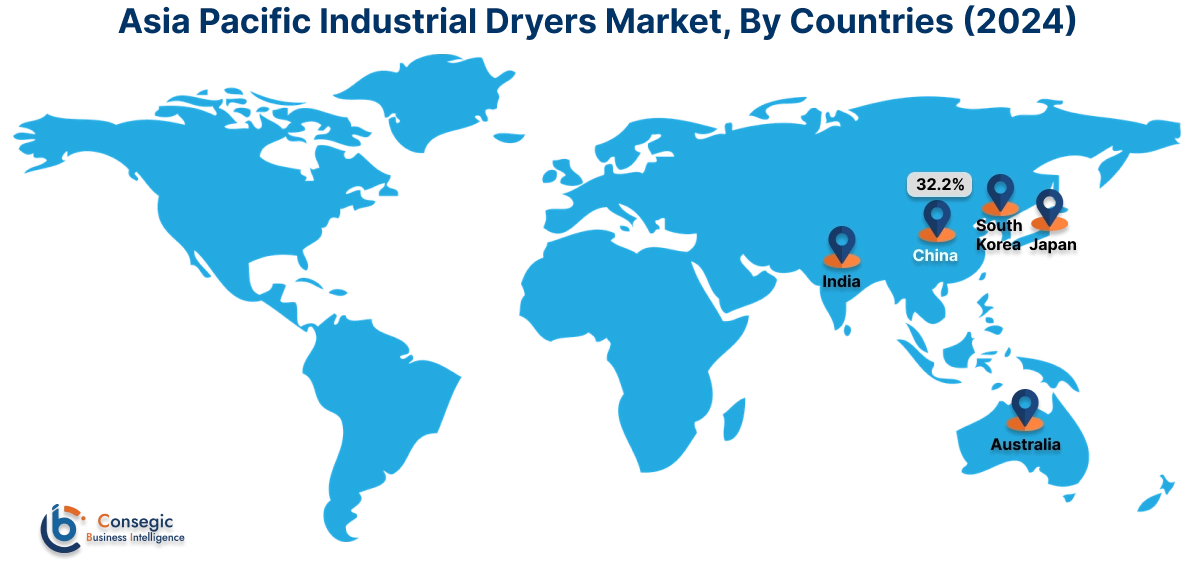

Asia Pacific region was valued at USD 2.02 Billion in 2024. Moreover, it is projected to grow by USD 2.08 Billion in 2025 and reach over USD 2.97 Billion by 2032. Out of this, China accounted for the maximum revenue share of 32.2%. Asia-Pacific is witnessing rapid development in the industrial dryers industry, fueled by rising industrialization, growing investment in manufacturing plants, and the trend toward automation. China, India, Japan, and South Korea are spearheading the region's adoption, particularly in textiles, fertilizer manufacturing, and chemical processing. Market research indicates that government initiatives encouraging clean manufacturing and energy efficiency are driving the adoption of high-efficiency drying systems. Furthermore, growing food exports and pharmaceutical production are generating long-term requirements for high-end drying equipment that can preserve product integrity with less processing time. Regional demand is also driven by local capability for local production and competitive prices offered by local producers.

North America is estimated to reach over USD 3.16 Billion by 2032 from a value of USD 2.27 Billion in 2024 and is projected to grow by USD 2.33 Billion in 2025. North America maintains a dominant position in the market as a result of the well-developed manufacturing and processing industries. Demand in the United States and Canada is driven primarily by technological advancements in the food and pharmaceutical industries, where accuracy and adherence to hygiene regulations are paramount. Market research indicates an increasing need for energy-saving and continuous drying systems with integrated IoT capabilities for real-time monitoring and process control. Environmental emissions and energy consumption regulations are also compelling businesses to invest in newer, more energy-efficient drying technologies. Growth continues as companies focus on operational efficiency and cost of production in regulated climates.

Europe is still a mature but innovation-driven market, where the focus of purchases is on efficiency, emissions reduction, and automation. Nations such as Germany, the Netherlands, and France are incorporating heat recovery, waste reduction, and moisture control technologies into their dryers. Market research indicates that tight energy directives and carbon reduction targets are driving the replacement of traditional thermal dryers with vacuum and freeze-drying systems, especially in biotech, ceramics, and agrochemical sectors. The market opportunity in industrial dryers here is in modernization of old systems and growth in specialty drying technologies appropriate for high-value, temperature-sensitive products.

Latin America is showing a consistent increase in adoption, particularly in Brazil, Argentina, and Chile, where mining, food processing, and agriculture are lead industries. Market research indicates growing interest for rotary and fluid bed dryers for high-volume materials such as fertilizers, minerals, and grains. With regional economies investing in upgrading industrial infrastructure, there is enhanced need for energy-efficient and automated solutions. The industrial dryers market opportunity in this region is directly associated with resource-intensive industries' efficiency enhancements and value-added manufacturing growth targeting regional and global markets.

The Middle East and Africa are emerging markets with a growing need for drying solutions, mainly in the petrochemical, food packaging, and construction materials industries. In nations such as the UAE, Saudi Arabia, and South Africa, industrial development and infrastructure growth are opening up new opportunities for thermal drying systems. Market research indicates that although cost is a constraint for most small-scale operations, large companies are investing in sophisticated dryers that provide longevity in high-temperature or high-humidity environments. Sustainable manufacturing programs and increased awareness of quality control are starting to influence equipment purchasing in targeted markets.

Top Key Players and Market Share Insights:

The industrial dryers market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global industrial dryers market. Key players in the industrial dryers industry include -

- ThyssenKrupp AG (Germany)

- Andritz AG (Austria)

- COMESSA (France)

- Mitchell Dryers Ltd. (United Kingdom)

- Yamato Sanko Mfg. Co., Ltd. (Japan)

- GEA Group (Germany)

- Metso Corporation (Finland)

- FLSmidth & Co. A/S (Denmark)

- Bühler Holding AG (Switzerland)

- ANIVI Ingeniería SA (Spain)

Recent Industry Developments :

Acquisitions:

- In January 2025, Dover acquired certain assets within the petrochemical division of Carter Day International, Inc. The assets became part of the MAAG business unit under Dover, expanding their pelletizing-system portfolio of dewatering and drying equipment for the plastics industry.

Industrial Dryers Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 9.75 Billion |

| CAGR (2025-2032) | 4.5% |

| By Product Type |

|

| By Heating Method |

|

| By Application |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Industrial Dryers Market? +

Industrial Dryers Market size is estimated to reach over USD 9.75 Billion by 2032 from a value of USD 6.85 Billion in 2024 and is projected to grow by USD 7.04 Billion in 2025, growing at a CAGR of 4.5% from 2025 to 2032.

What specific segmentation details are covered in the Industrial Dryers Market report? +

The Industrial Dryers market report includes specific segmentation details for product type, heating method, application and end-use industry.

What are the end-use industries of the Industrial Dryers Market? +

The end-use industries of the Industrial Dryers Market are food & beverage, pharmaceuticals, chemicals, fertilizers, cement, textiles, and others.

Who are the major players in the Industrial Dryers Market? +

The key participants in the Industrial Dryers market are ThyssenKrupp AG (Germany), Andritz AG (Austria), GEA Group (Germany), Metso Corporation (Finland), FLSmidth & Co. A/S (Denmark), Bühler Holding AG (Switzerland), ANIVI Ingeniería SA (Spain), COMESSA (France), Mitchell Dryers Ltd. (United Kingdom) and Yamato Sanko Mfg. Co., Ltd. (Japan).