- Summary

- Table Of Content

- Methodology

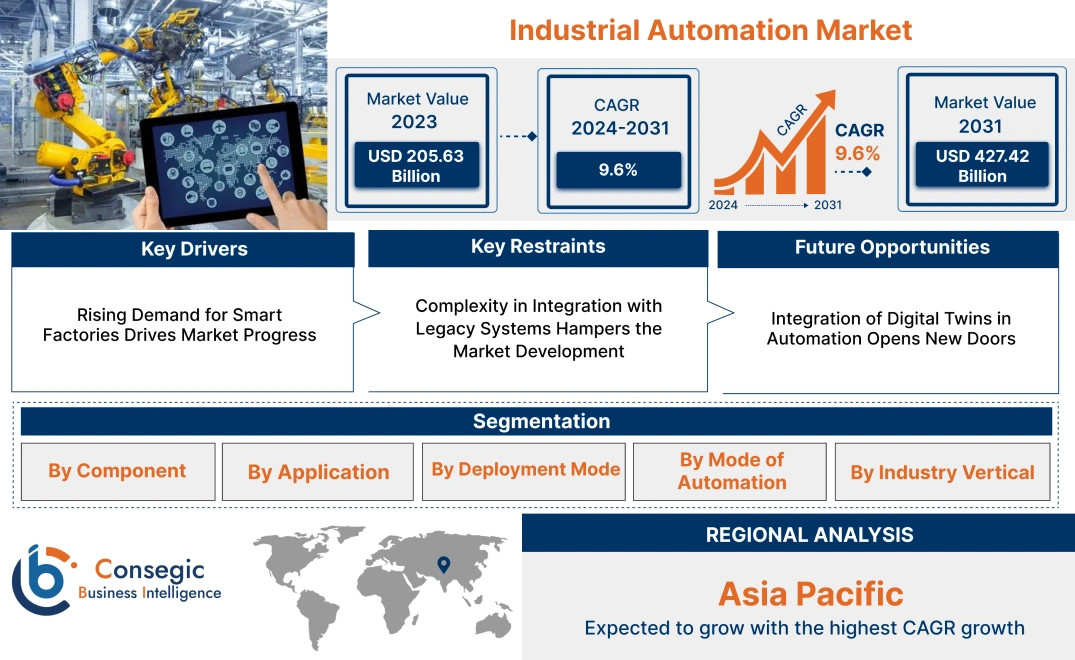

Industrial Automation Market Size:

Industrial Automation Market size is estimated to reach over USD 427.42 Billion by 2031 from a value of USD 205.63 Billion in 2023 and is projected to grow by USD 221.66 Billion in 2024, growing at a CAGR of 9.6% from 2024 to 2031.

Industrial Automation Market Scope & Overview:

Industrial automation refers to the use of control systems, such as robots, programmable logic controllers (PLCs), and supervisory control and data acquisition (SCADA), to operate machinery and processes with minimal human intervention. This technology enables precise control and monitoring of production lines, enhancing efficiency, accuracy, and safety in manufacturing and industrial operations. Automation solutions are widely adopted across industries including automotive, electronics, chemicals, and food and beverage for tasks such as assembly, packaging, quality control, and material handling.

These systems integrate advanced technologies such as robotics, sensors, and software platforms to provide real-time monitoring, predictive maintenance, and optimized workflows. Industrial automation solutions are customizable to meet specific operational requirements and are designed to function reliably in demanding environments, ensuring uninterrupted production. Modern automation systems also support seamless integration with enterprise systems, enabling better decision-making through data-driven insights.

End-users of automation solutions include manufacturing plants, energy providers, and logistics companies that rely on automated processes to maintain productivity, improve operational efficiency, and enhance overall system performance.

Industrial Automation MarketDynamics - (DRO) :

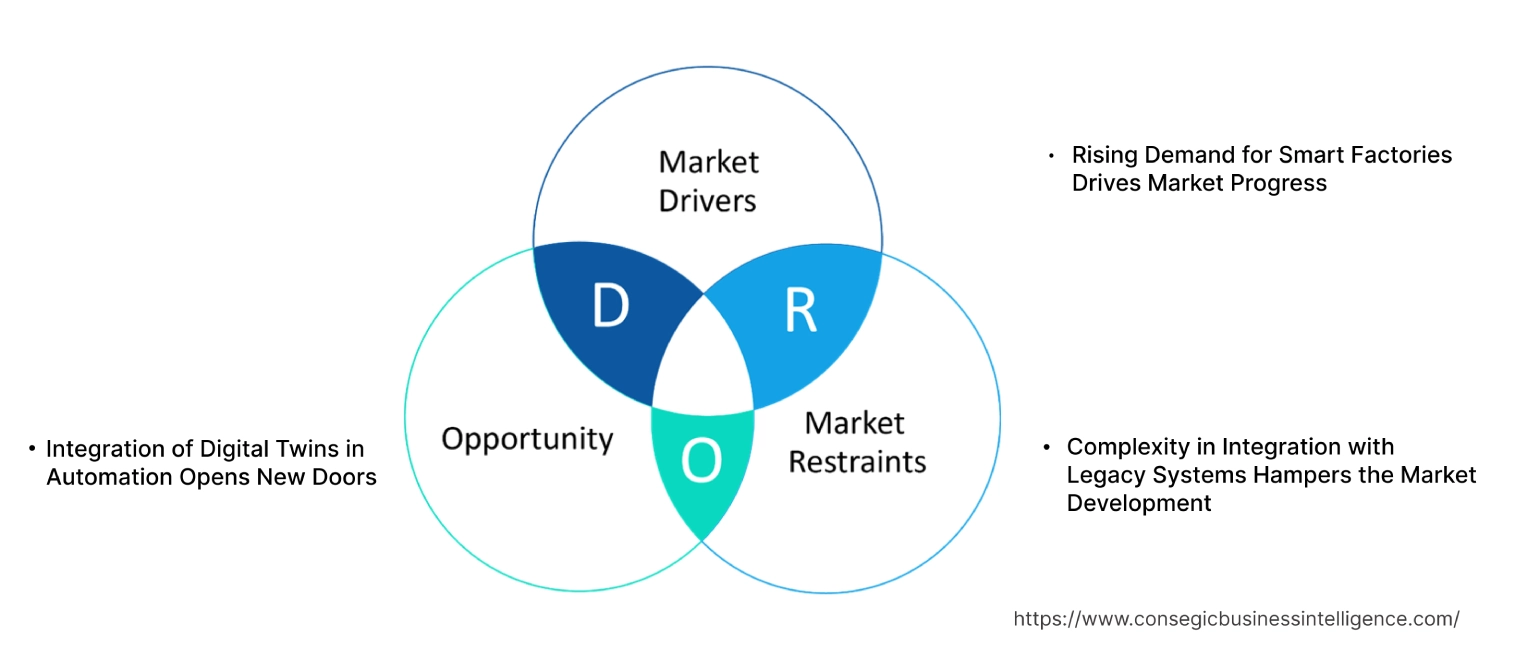

Key Drivers:

Rising Demand for Smart Factories Drives Market Progress

The growing adoption of smart factories is driving significant advancements in automation. Smart factories leverage cutting-edge technologies such as IoT, AI, machine learning, and robotics to streamline production, enhance operational efficiency, and reduce downtime. Automated systems in smart factories facilitate real-time monitoring, enabling predictive maintenance to preempt equipment failures and optimize resource utilization. These factories support seamless data flow across connected devices, allowing for dynamic decision-making and process adjustments, thereby improving productivity and product quality. Industries such as automotive, electronics, and consumer goods are increasingly implementing smart manufacturing practices to remain competitive and achieve cost efficiency.

Additionally, as trends in digital transformation accelerate, smart factories are becoming integral to global industrial strategies, driving demand for advanced automation technologies tailored to meet the complex needs of modern manufacturing. This shift aligns with the growing emphasis on data-driven operations and sustainability in production environments, contributing to the industrial automation market growth.

Key Restraints :

Complexity in Integration with Legacy Systems Hampers the Market Development

The integration of modern automation solutions with existing legacy systems presents a significant restraint for industries. Legacy infrastructure often lacks the flexibility and compatibility needed to seamlessly incorporate advanced technologies, such as IoT-enabled devices or AI-driven automation. This results in lengthy customization processes, requiring extensive time and resources to ensure interoperability between old and new systems. For industries with limited technical expertise or tight budgets, these integration complexities act as a deterrent, slowing down the adoption of automation technologies.

Furthermore, ensuring that legacy systems comply with modern cybersecurity and data standards adds another layer of complexity. These constraints are particularly prevalent in sectors like manufacturing, utilities, and oil & gas, where outdated systems are still widespread. As a result, the high costs and technical barriers associated with integration restrict the scalability of automation initiatives, limiting industrial automation market demand in certain applications and industries.

Future Opportunities :

Integration of Digital Twins in Automation Opens New Doors

The adoption of digital twin technology is revolutionizing automation by enabling real-time simulation, monitoring, and analysis of physical systems. Digital twins create virtual replicas of machinery, processes, or entire production lines, allowing industries to predict system behavior, optimize workflows, and prevent potential failures before they occur. This technology is particularly transformative in sectors such as manufacturing, energy, and aerospace, where precision and efficiency are paramount.

Automation systems integrated with digital twins provide actionable insights by analyzing real-time data, enabling proactive decision-making and predictive maintenance. These systems reduce downtime, enhance resource utilization, and improve overall operational efficiency. Additionally, digital twins facilitate the testing of new processes or configurations in a virtual environment, minimizing risks and costs associated with physical trials. As industries increasingly embrace data-driven approaches, the integration of digital twins with automation systems is becoming a cornerstone of modern industrial strategies, creating significant industrial automation market opportunities.

Industrial Automation Market Segmental Analysis :

By Component:

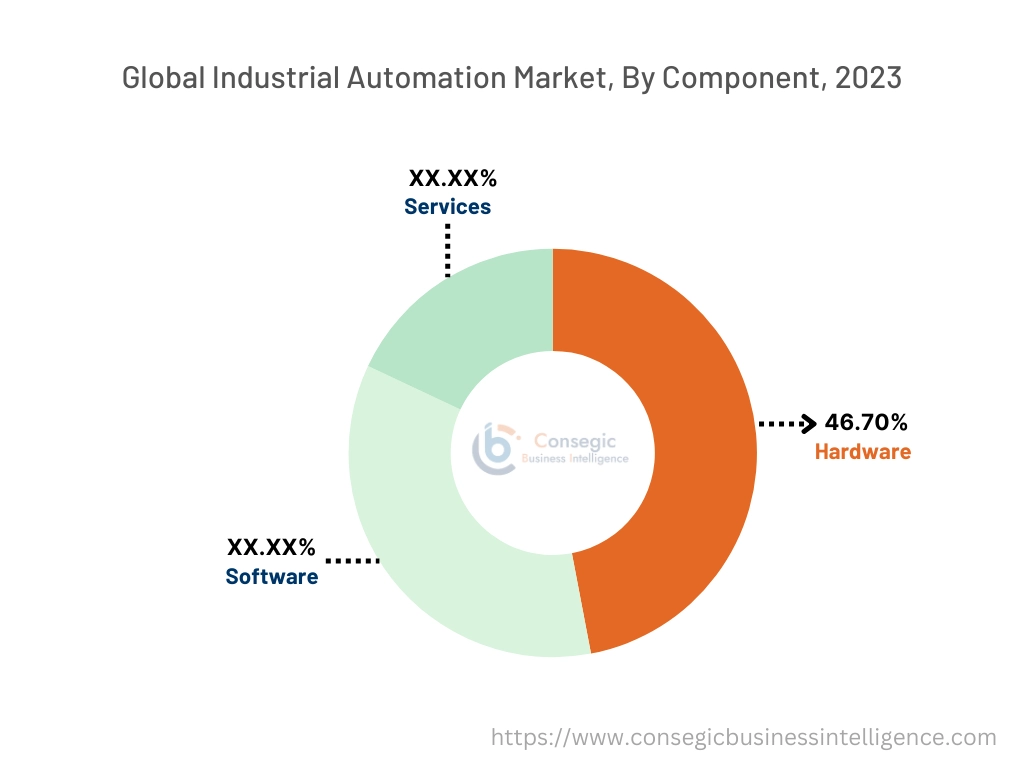

Based on component, the market is segmented into Hardware (Sensors, Controllers, Robots, Drives, Motors, Valves), Software (SCADA, PLC, DCS, HMI, MES), and Services (Consulting, Integration & Deployment, Support & Maintenance).

The Hardware segment held the largest revenue of 46.70% of the total industrial automation market share in 2023.

- Hardware components such as sensors and controllers are the backbone of industrial automation systems, enabling real-time monitoring and control of processes.

- Robots and drives are widely deployed in industries like automotive and electronics for precision operations and assembly tasks.

- Motors and valves are critical for regulating and controlling mechanical movements in automated systems, especially in energy and utility sectors.

- The dominance of hardware reflects its indispensable role in implementing automation solutions across various applications, fueling the industrial automation market expansion.

The Software segment is expected to grow at the fastest CAGR during the forecast period.

- Software solutions like SCADA, PLC, and DCS enable centralized control, monitoring, and analysis of complex industrial operations.

- MES software supports production planning, inventory tracking, and quality management, optimizing manufacturing workflows.

- Advancements in cloud-based SCADA and HMI solutions are driving the adoption of scalable and remote-accessible automation systems.

- Therefore, as per industrial automation market analysis, trends in real-time data analytics and predictive maintenance are fueling the demand for software in industrial automation.

By Application:

Based on application, the market is segmented into Manufacturing Operations, Quality Control, Inventory Management, Packaging & Processing, and Predictive Maintenance.

The Manufacturing Operations segment accounted for the largest revenue of the total industrial automation market share in 2023.

- Automation in manufacturing streamlines operations, reduces human intervention, and enhances production efficiency.

- Robots and programmable systems are widely used in assembly lines for repetitive and precision-driven tasks, especially in automotive and electronics industries.

- Automated solutions improve production throughput while ensuring compliance with safety and quality standards.

- As per industrial automation market trends, the dominance of this segment reflects its critical role in driving productivity and operational excellence in manufacturing environments.

The Predictive Maintenance segment is expected to register the fastest CAGR during the forecast period.

- Predictive maintenance leverages sensors and software to identify potential equipment failures before they occur, minimizing downtime and repair costs.

- Industries like energy, aerospace, and pharmaceuticals rely on predictive maintenance to ensure equipment reliability and operational safety.

- Market analysis highlights the increasing integration of AI and IoT in predictive maintenance solutions for enhanced diagnostic accuracy.

- The segment's rapid growth reflects its ability to optimize asset utilization and extend equipment lifespan, boosting the industrial automation market growth.

By Deployment Mode:

Based on deployment mode, the market is segmented into On-Premise, Cloud-Based, and Hybrid.

The On-Premise segment held the largest revenue share in 2023.

- On-premise automation systems offer complete control and customization, making them suitable for industries with stringent data security and compliance requirements.

- These solutions are preferred by large-scale manufacturing facilities with extensive automation infrastructure.

- The dominance of on-premise systems is attributed to their reliability and ability to operate in environments with limited internet connectivity.

- Therefore, industries like aerospace and defense heavily rely on on-premise solutions for critical operations requiring high precision which further fuels the industrial automation market demand.

The Cloud-Based segment is expected to register the fastest CAGR during the forecast period.

- Cloud-based solutions enable remote monitoring, scalability, and real-time data access, supporting operational efficiency in distributed environments.

- These solutions are increasingly adopted in sectors like food and beverage and pharmaceuticals for inventory tracking and compliance management.

- Market trends highlight the role of cloud-based automation in supporting Industry 4.0 initiatives and IoT-enabled operations.

- The rapid expansion of this segment is driven by advancements in cloud infrastructure and cybersecurity technologies, contributing to industrial automation market expansion.

By Mode of Automation:

Based on mode of automation, the market is segmented into Flexible, Fixed, Integrated, and Programmable.

The Flexible Automation segment held the largest revenue share in 2023.

- Flexible automation systems are widely used in industries requiring frequent product changes, such as electronics and consumer goods.

- These systems enable quick reprogramming and adaptation, reducing setup times and enhancing production agility.

- The segment’s dominance reflects its suitability for high-mix, low-volume manufacturing operations, especially in fast-changing markets.

- Trends in modular automation designs are further driving the adoption of flexible systems across various industries, driving industrial automation market opportunities.

The Integrated Automation segment is expected to register the fastest CAGR during the forecast period.

- Integrated automation systems combine hardware, software, and control mechanisms into a unified platform, streamlining workflows and improving efficiency.

- These systems are widely used in automotive and energy industries for end-to-end process automation and monitoring.

- Market analysis highlights the increasing focus on integrating automation with enterprise resource planning (ERP) systems for better data synchronization.

- As per segmental trends, the rapid growth of this segment is supported by its ability to optimize complex manufacturing processes and reduce operational silos.

By Industry Vertical:

Based on industry vertical, the market is segmented into Automotive, Food & Beverage, Pharmaceuticals, Oil & Gas, Energy & Utilities, Chemicals, Aerospace & Defense, and Electronics & Semiconductors.

The Automotive segment held the largest revenue share in 2023.

- Automotive manufacturers rely on automation for assembly lines, painting, welding, and quality inspection to ensure consistent output and product quality.

- Automation supports the production of electric vehicles (EVs) by enabling precision assembly of battery packs and electric drivetrains.

- The dominance of this segment is driven by the increasing adoption of robotics and smart manufacturing solutions in automotive plants.

- Therefore, as per industrial automation market analysis, autonomous vehicle manufacturing are further boosting the integration of advanced automation technologies.

The Electronics & Semiconductors segment is expected to register the fastest CAGR during the forecast period.

- Automation plays a critical role in semiconductor manufacturing, ensuring high precision and yield in wafer fabrication and chip assembly.

- The segment benefits from the rising demand for consumer electronics, 5G devices, and advanced computing systems.

- Market analysis highlights the increasing use of robotics and AI-driven automation in cleanrooms and high-tech manufacturing facilities.

- Thus, as per industrial automation market trends, the rapid growth of this segment is supported by innovations in miniaturization and advanced packaging technologies.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

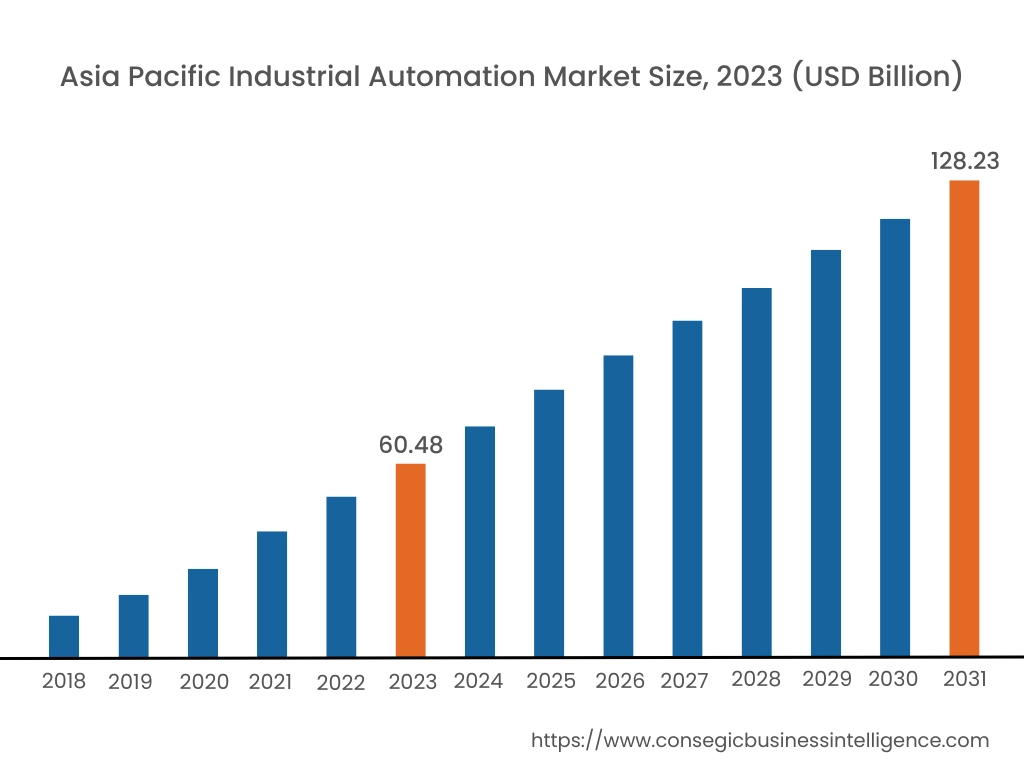

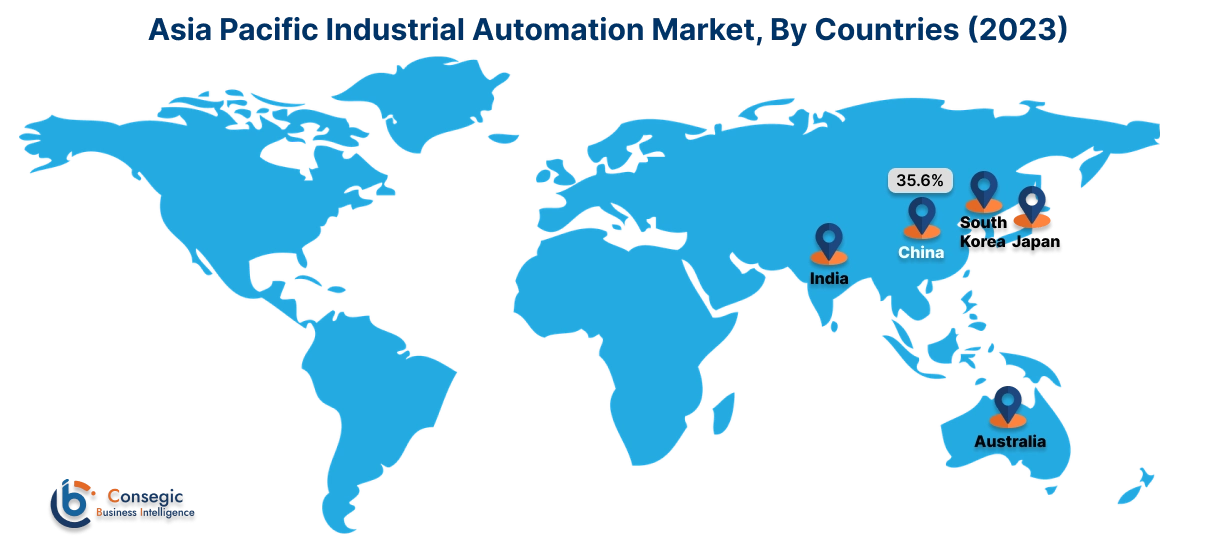

Asia Pacific region was valued at USD 60.48 Billion in 2023. Moreover, it is projected to grow by USD 65.31 Billion in 2024 and reach over USD 128.23 Billion by 2031. Out of which, China accounted for the largest share of 35.6% in 2023. The Asia-Pacific region is experiencing rapid growth in industrial automation, fueled by industrialization and urbanization in countries such as China, India, and Japan. The expansion of manufacturing activities and the adoption of smart factory initiatives are key trends driving the market. Government policies supporting automation and technological innovation further bolster this growth.

North America is estimated to reach over USD 140.62 Billion by 2031 from a value of USD 68.35 Billion in 2023 and is projected to grow by USD 73.62 Billion in 2024. This region maintains a significant position in the industrial automation sector, driven by a robust manufacturing base and early integration of advanced technologies. The United States, in particular, has seen substantial investments in automation to enhance productivity and maintain global competitiveness. The trend towards digitalization and the Industrial Internet of Things (IIoT) is prominent, with industries such as automotive and aerospace leading the charge.

Europe holds a substantial portion of the global industrial automation market, with countries like Germany, France, and the United Kingdom at the forefront. The region's strong emphasis on sustainability and energy efficiency has propelled the adoption of automation solutions, particularly in manufacturing and process industries. The analysis indicates a growing trend towards integrating artificial intelligence and machine learning to optimize operations.

The Middle East & Africa region is gradually embracing industrial automation, particularly in the oil & gas and manufacturing sectors. Countries like Saudi Arabia and the United Arab Emirates are investing in automation to diversify their economies and enhance operational efficiency. The analysis suggests an increasing trend towards adopting automation solutions to improve productivity and reduce reliance on manual labor.

Latin America is an emerging market for industrial automation, with Brazil and Mexico being key contributors. The region's focus on modernizing industrial operations and improving competitiveness has led to the adoption of automation technologies. Government initiatives aimed at enhancing manufacturing capabilities and attracting foreign investments influence market growth.

Top Key Players & Market Share Insights:

The Industrial Automation market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Industrial Automation market. Key players in the Industrial Automation industry include –

- ABB Ltd. (Switzerland)

- Siemens AG (Germany)

- Schneider Electric SE (France)

- Rockwell Automation, Inc. (USA)

- Honeywell International Inc. (USA)

- Mitsubishi Electric Corporation (Japan)

- Emerson Electric Co. (USA)

- Yokogawa Electric Corporation (Japan)

- Omron Corporation (Japan)

- General Electric Company (USA)

Recent Industry Developments :

Partnerships & Collaborations:

- In November 2024, ABB and SKF Industrial Indonesia formed a strategic partnership to advance industrial automation and energy efficiency across sectors like manufacturing, mining, and agriculture. The collaboration leverages ABB's automation expertise and SKF's industrial solutions to deliver cutting-edge technologies for enhanced operational performance.

- In October 2024, Honeywell and Google Cloud partnered to develop AI agents aimed at enhancing autonomous operations in the industrial sector. These AI-driven solutions will integrate with Honeywell Forge's IoT data, enabling real-time insights and automation. The collaboration seeks to improve asset efficiency, optimize workforce utilization, and streamline processes, addressing challenges such as labor shortages.

- In July 2024, Emerson has teamed up with MSTelcom to enhance Angola's energy sector through digital transformation. Combining Emerson’s automation technologies with MSTelcom's IT expertise, the partnership aims to optimize energy production, improve operational efficiency, and enable seamless data integration for better decision-making.

Product Launches:

- In November 2024, AWS IoT SiteWise introduced a Generative AI-Powered Industrial Assistant to enhance industrial operations. This tool uses generative AI to analyze IoT data, providing actionable insights and recommendations for equipment monitoring, predictive maintenance, and process optimization. The assistant integrates seamlessly with AWS IoT SiteWise, allowing industrial customers to gain real-time insights and streamline decision-making processes. It aims to improve operational efficiency and reduce downtime across manufacturing, energy, and other sectors.

Acquisitions & Mergers:

- In July 2024, Lear Corporation, a global leader in automotive seating and E-Systems, has finalized its acquisition of WIP Industrial Automation, a prominent provider of automation solutions for industrial manufacturing. This strategic move strengthens Lear's capabilities in automated manufacturing processes, enhancing production efficiency and flexibility. WIP Industrial Automation specializes in advanced robotics, software integration, and custom automation solutions. With this acquisition, Lear aims to leverage WIP's expertise to support its global operations and further integrate cutting-edge automation technologies into its manufacturing facilities.

Industrial Automation Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 427.42 Billion |

| CAGR (2024-2031) | 9.6% |

| By Component |

|

| By Application |

|

| By Deployment Mode |

|

| By Mode of Automation |

|

| By Industry Vertical |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Industrial Automation Market? +

Industrial Automation Market size is estimated to reach over USD 427.42 Billion by 2031 from a value of USD 205.63 Billion in 2023 and is projected to grow by USD 221.66 Billion in 2024, growing at a CAGR of 9.6% from 2024 to 2031.

What specific segmentation details are covered in the Industrial Automation Market report? +

The Industrial Automation Market report includes segmentation details by component (Hardware such as sensors, controllers, robots, drives, motors, valves; Software like SCADA, PLC, DCS, HMI, MES; Services like consulting, integration, support & maintenance), application (Manufacturing Operations, Quality Control, Inventory Management, Packaging & Processing, Predictive Maintenance), deployment mode (On-Premise, Cloud-Based, Hybrid), mode of automation (Flexible, Fixed, Integrated, Programmable), industry vertical (Automotive, Food & Beverage, Pharmaceuticals, Oil & Gas, Energy & Utilities, Chemicals, Aerospace & Defense, Electronics & Semiconductors), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which is the fastest-growing segment in the Industrial Automation Market? +

The Software segment is expected to grow at the fastest CAGR during the forecast period. The increasing adoption of cloud-based SCADA, HMI solutions, and MES software for real-time data analytics and predictive maintenance is fueling this growth.

Who are the major players in the Industrial Automation Market? +

The major players in the Industrial Automation Market include ABB Ltd. (Switzerland), Siemens AG (Germany), Schneider Electric SE (France), Rockwell Automation, Inc. (USA), Honeywell International Inc. (USA), Mitsubishi Electric Corporation (Japan), Emerson Electric Co. (USA), Yokogawa Electric Corporation (Japan), Omron Corporation (Japan), and General Electric Company (USA).