- Summary

- Table Of Content

- Methodology

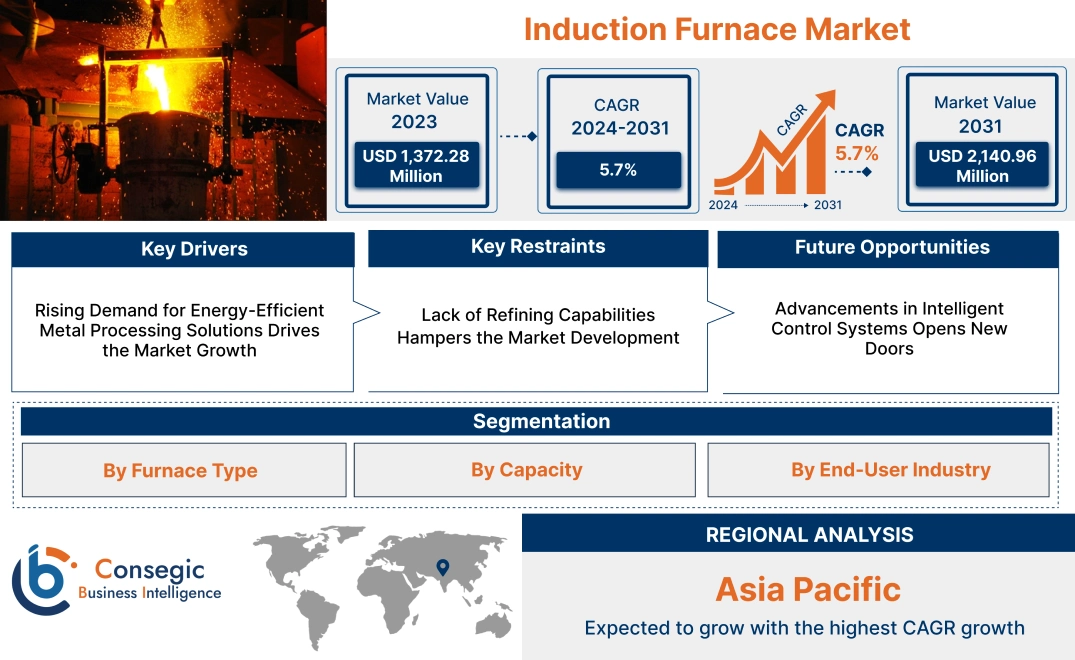

Induction Furnace Market Size:

Induction Furnace Market size is estimated to reach over USD 2,140.96 Million by 2031 from a value of USD 1,372.28 Million in 2023 and is projected to grow by USD 1,426.29 Million in 2024, growing at a CAGR of 5.7% from 2024 to 2031.

Induction Furnace Market Scope & Overview:

An induction furnace is an advanced heating device that uses electromagnetic induction to melt and refine metals. This technology is widely employed in industries such as metallurgy, foundries, automotive, and aerospace for processes including metal casting, alloy production, and heat treatment. These furnaces are designed to provide precise temperature control, energy efficiency, and reduced environmental impact, making them ideal for modern industrial applications.

These furnaces are available in different configurations, including coreless and channel designs, catering to various melting capacities and operational needs. They are compatible with a wide range of metals, including steel, aluminum, copper, and precious metals, ensuring versatility in manufacturing processes. Equipped with features like automated controls, real-time monitoring, and enhanced safety systems, they deliver reliable performance and optimized operations.

End-users of these furnaces include steel manufacturing plants, foundries, and specialized metal processing units, where efficient and precise melting solutions are critical for maintaining product quality and meeting production demands.

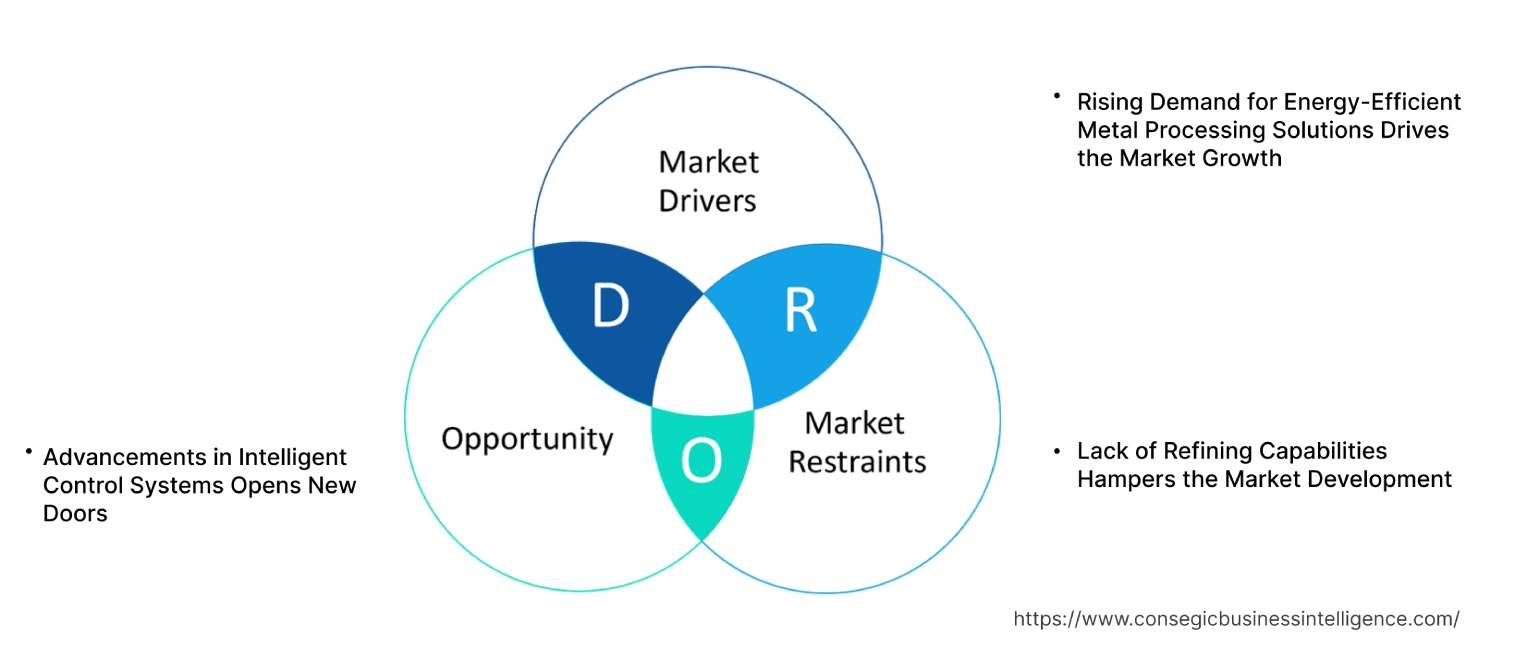

Induction Furnace Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Energy-Efficient Metal Processing Solutions Drives the Market Growth

The global push for sustainability and energy conservation is driving the adoption of energy-efficient solutions in metal processing industries. Induction-based systems stand out for their superior energy efficiency, enabling faster heating and significantly reducing energy consumption compared to traditional methods like arc or blast furnaces. These systems also minimize waste generation and emissions, making them an environmentally friendly alternative. Industries such as steel, aluminum, and copper manufacturing benefit from the precise temperature control and uniform heating provided by induction technology, improving overall production efficiency. The increasing regulatory focus on reducing carbon footprints further boosts the need for these systems, as they align with global sustainability initiatives. Additionally, their ability to lower operational costs while maintaining high-quality output makes them a preferred choice across a range of applications, from recycling scrap metals to producing advanced alloys, driving their adoption in modern manufacturing landscapes. Thus, the aforementioned factors are driving the induction furnace market growth.

Key Restraints:

Lack of Refining Capabilities Hampers the Market Development

Induction furnaces, while highly efficient for melting metals, lack the capability for refining processes such as impurity removal or composition adjustment. Unlike other furnace technologies, induction systems rely on pre-cleaned and accurately composed materials, making them unsuitable for operations requiring in-furnace refining. This limitation restricts their application in industries that demand precise control over metal purity, such as aerospace and medical device manufacturing.

Additionally, the need for pre-treatment processes adds operational complexity and costs, deterring their adoption in facilities where refining is integral to production. This shortcoming reduces their competitiveness compared to other furnace technologies capable of handling both melting and refining tasks, hindering induction furnace market demand.

Future Opportunities :

Advancements in Intelligent Control Systems Opens New Doors

The integration of intelligent control systems in induction furnaces is revolutionizing operational efficiency. By employing smart sensors, real-time data analytics, and machine learning algorithms, these systems monitor and adapt to changing conditions during operation. This automation enables precise adjustments to parameters such as temperature, power input, and melting time, optimizing energy consumption and reducing waste.

Additionally, predictive maintenance features help identify potential issues before they lead to downtime, ensuring uninterrupted productivity. Industries adopting intelligent control systems will achieve significant cost savings while enhancing process reliability, making this a promising growth avenue as manufacturers prioritize automation and sustainability. Therefore, the above mentioned factors are driving the induction furnace market opportunities.

Induction Furnace Market Segmental Analysis :

By Furnace Type:

The market is segmented into coreless induction furnaces and channel induction furnaces.

Coreless induction furnaces held the largest revenue of the total induction furnace market share in 2023.

- Coreless induction furnaces are versatile and widely used across multiple industries for melting various metals, including steel, aluminum, and copper alloys.

- Their compact size and ability to provide rapid melting cycles make them suitable for small-scale and high-precision operations.

- These furnaces are commonly employed in applications requiring high-temperature uniformity, such as automotive component manufacturing and aerospace parts production.

- The analysis of segmental trends depicts that the segment's dominance is attributed to the growing adoption in industries focusing on custom alloy production and precision manufacturing, fueling the induction furnace market expansion.

Channel induction furnaces are expected to register the fastest CAGR during the forecast period.

- Channel induction furnaces are highly efficient in maintaining molten metal at constant temperatures for extended periods.

- These furnaces are preferred for large-scale industrial applications, including continuous casting and alloy processing.

- The segment's growth is driven by increasing requirement from the construction and electronics sectors for high-volume metal production.

- As per the induction furnace market analysis, advancements in energy-efficient designs and their ability to handle larger batches of molten metal further enhance their adoption in heavy industries.

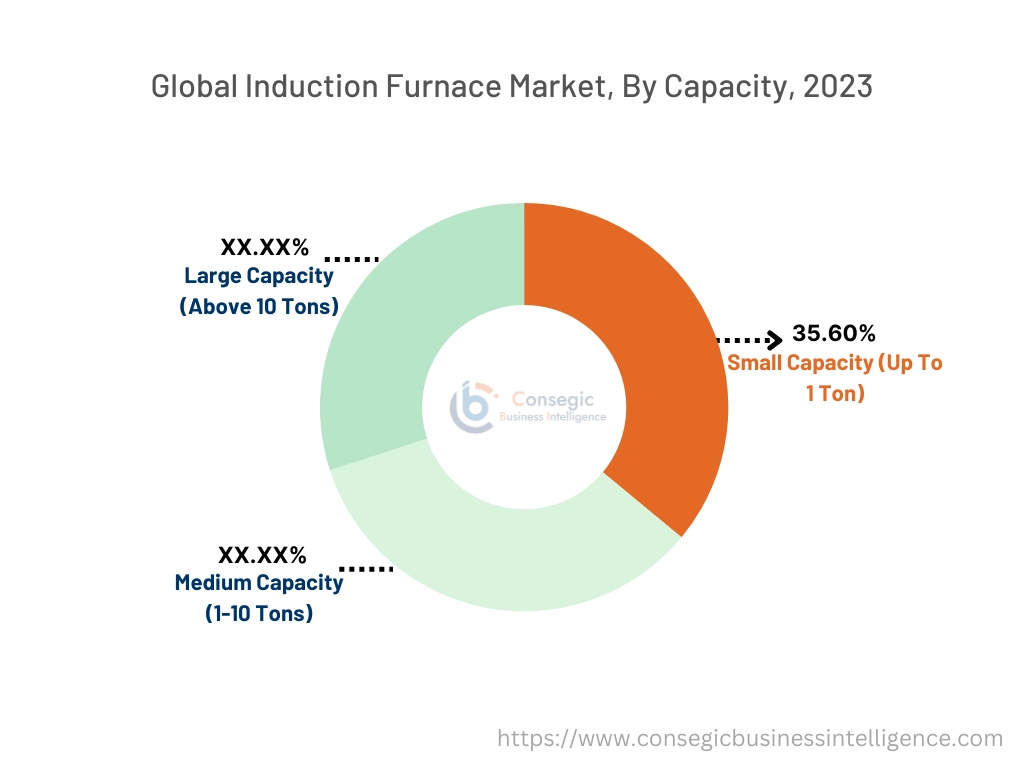

By Capacity:

The market is segmented based on furnace capacity into small capacity (up to 1 ton), medium capacity (1-10 tons), and large capacity (above 10 tons).

Small-capacity furnaces accounted for the largest revenue of 35.60% of the total induction furnace market share in 2023.

- Small-capacity furnaces are extensively used in small and medium enterprises (SMEs) due to their affordability and operational flexibility.

- These furnaces are ideal for precision applications, including jewelry making, dental alloy production, and prototyping in industrial manufacturing.

- The segment's dominance is supported by growing adoption in industries requiring low-volume but high-quality metal production.

- As per the induction furnace market trends, innovations in compact furnace designs with enhanced energy efficiency drive their appeal in cost-sensitive markets.

Large-capacity furnaces are projected to grow at the fastest CAGR during the forecast period.

- Large-capacity furnaces are integral to heavy industrial applications, such as steel production, aerospace component manufacturing, and automotive casting.

- Their ability to handle high-volume production cycles makes them essential for industries focusing on bulk manufacturing.

- The rapid expansion of infrastructure projects globally fuels the demand for large-capacity furnaces in the construction sector.

- Increasing investments in industrial manufacturing and advanced metallurgy contribute to the strong growth of this segment, boosting the overall induction furnace market demand.

By End-User Industry:

The market is segmented into automotive, aerospace, electronics, construction, industrial manufacturing, and others.

The automotive segment held the largest revenue share in 2023.

- Induction furnaces are widely used in the automotive sector for manufacturing high-precision components, including engine blocks, gears, and suspension systems.

- The growing adoption of electric vehicles (EVs) is driving need for lightweight alloy production, which relies on these furnaces.

- The segment's dominance is attributed to the continuous need for high-quality cast and forged parts in automotive production.

- The analysis of segmental trends shows, innovations in automotive alloy materials further enhance the demand for the furnaces tailored for specialized applications, contributing to the induction furnace market growth.

The aerospace segment is expected to grow at the fastest CAGR during the forecast period.

- Induction furnaces play a critical role in the aerospace industry for producing high-performance alloys and components used in aircraft engines and structural parts.

- The segment's growth is fueled by increasing investments in aerospace projects and the development of advanced materials, such as titanium alloys.

- Stringent quality standards in the aerospace sector necessitate the use of precision melting and casting processes provided by these furnaces.

- As per the induction furnace market analysis, rising global need for air travel and military aircraft contributes to the accelerated adoption of furnaces in aerospace manufacturing.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

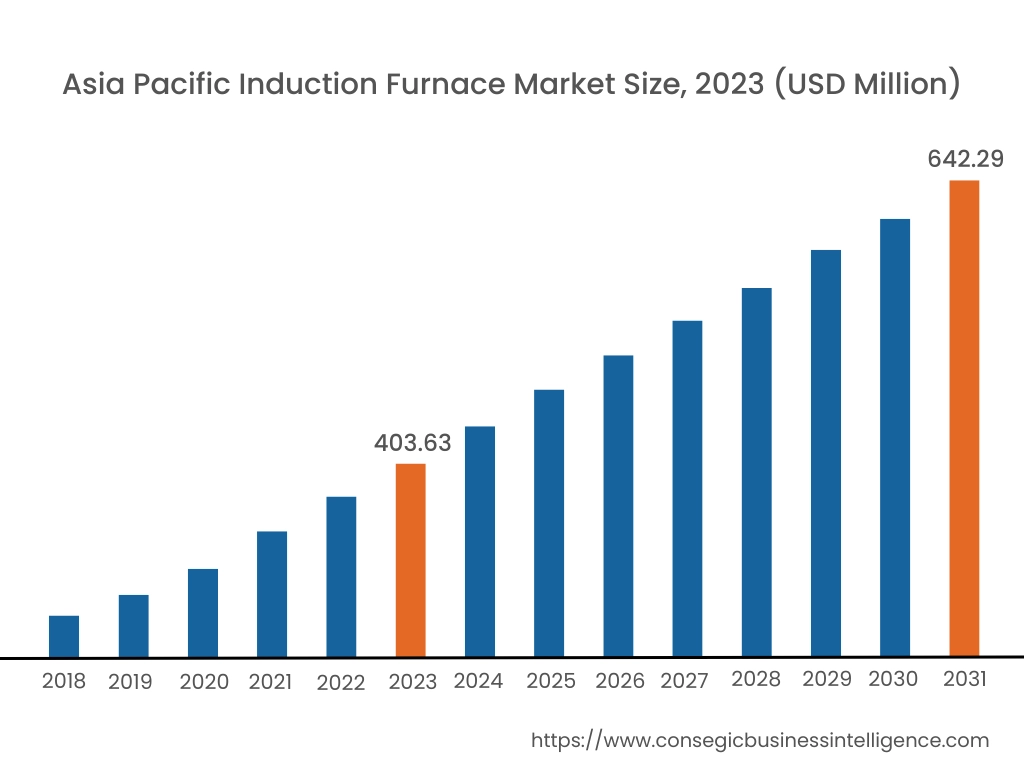

Asia Pacific region was valued at USD 403.63 Million in 2023. Moreover, it is projected to grow by USD 420.22 Million in 2024 and reach over USD 642.29 Million by 2031. Out of these, China accounted for the largest share of 27.4% in 2023. The Asia-Pacific region is experiencing rapid development in the induction furnace market, driven by industrialization and technological advancements in countries such as China, India, and Australia. The region is the world's largest producer of steel, aluminum, and other metals that require furnaces. Government initiatives promoting industrial activities further influence induction furnace market opportunities.

North America is estimated to reach over USD 704.38 Million by 2031 from a value of USD 456.13 Million in 2023 and is projected to grow by USD 473.68 Million in 2024. This region holds a significant share of the induction furnace market, driven by the expanding manufacturing and packaging industries. The United States, in particular, has seen extensive adoption of these furnaces across sectors such as automotive and steel production. A notable trend is the increasing need for metals like aluminum and steel, propelled by rising per capita income and surging automobile requirement.

Europe represents a substantial portion of the global induction furnace market, with countries like Germany, Italy, and France leading in adoption and innovation. The region's emphasis on renewable energy and industrial automation has propelled the utilization of the furnaces. Analysis indicates a growing trend towards the deployment of induction furnaces in the renewable energy sector, driving induction furnace market expansion.

The Middle East & Africa region shows a growing interest in induction furnace solutions, particularly in the construction and industrial sectors. Countries like Saudi Arabia and South Africa are investing in advanced furnace technologies to support industrial revolution efforts. Analysis suggests an increasing trend towards adopting the furnaces in metal processing industries, enhancing production efficiency.

Latin America is an emerging market with Brazil and Mexico being key contributors. The region's growing industrial activities and initiatives to promote technological innovation have spurred the adoption of advanced furnace solutions. As per induction furnace market trends, government policies aimed at modernizing infrastructure and enhancing industrial capabilities influence market trends.

Top Key Players and Market Share Insights:

The Induction Furnace market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Induction Furnace market. Key players in the Induction Furnace industry include –

- Inductotherm Corp. (USA)

- Ambrell (USA)

- Surface Combustion, Inc. (USA)

- CHE Furnaces (USA)

- Ultraflex Power Technologies (USA)

- Lepel Corporation (USA)

- AFC-Holcroft (USA)

Induction Furnace Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 2,140.96 Million |

| CAGR (2024-2031) | 5.7% |

| By Furnace Type |

|

| By Capacity |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Induction Furnace Market? +

Induction Furnace Market size is estimated to reach over USD 2,140.96 Million by 2031 from a value of USD 1,372.28 Million in 2023 and is projected to grow by USD 1,426.29 Million in 2024, growing at a CAGR of 5.7% from 2024 to 2031.

What specific segmentation details are covered in the Induction Furnace Market report? +

The market is segmented based on furnace type (Coreless Induction Furnace, Channel Induction Furnace), capacity (Small Capacity (Up to 1 Ton), Medium Capacity (1-10 Tons), Large Capacity (Above 10 Tons)), end-user industry (Automotive, Aerospace, Electronics, Construction, Industrial Manufacturing, Others), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which is the fastest-growing segment in the Induction Furnace Market? +

The large-capacity furnaces segment is expected to grow at the fastest CAGR during the forecast period, driven by the increasing demand in heavy industrial applications such as steel production, aerospace component manufacturing, and automotive casting.

Who are the major players in the Induction Furnace Market? +

Major players in the Induction Furnace Market include Inductotherm Corp. (USA), Ambrell (USA), Ultraflex Power Technologies (USA), Lepel Corporation (USA), AFC-Holcroft (USA), Surface Combustion, Inc. (USA), CHE Furnaces (USA).