- Summary

- Table Of Content

- Methodology

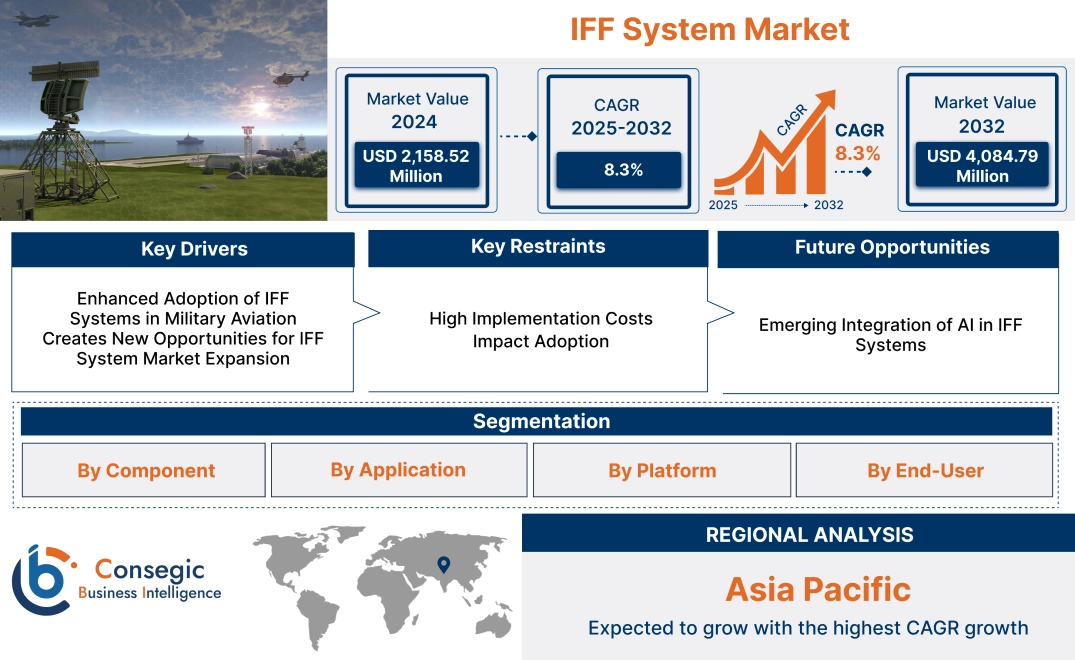

IFF System Market Size:

IFF System Market size is estimated to reach over USD 4,084.79 Million by 2032 from a value of USD 2,158.52 Million in 2024 and is projected to grow by USD 2,299.22 Million in 2025, growing at a CAGR of 8.3% from 2025 to 2032.

IFF System Market Scope & Overview:

Identification Friend or Foe (IFF) systems are advanced security and identification technologies used to differentiate friendly assets from potential threats. These systems operate through interrogators and transponders, ensuring precise communication and identification in critical environments. They feature high accuracy, encryption capabilities, and robust performance in challenging conditions. IFF systems provide enhanced situational awareness, reduced risks of misidentification, and increased operational efficiency. Their ability to ensure secure identification supports seamless collaboration across defense and aviation operations. These systems improve mission success rates while maintaining safety and security standards.

Applications of IFF systems are widespread in defense, aviation, and naval sectors. In defense, they are deployed in military aircraft, vehicles, and personnel. In aviation, IFF systems ensure secure air traffic management and collision avoidance. End-use industries include aerospace, military, and homeland security, highlighting their vital role in maintaining secure operational frameworks.

IFF System Market Dynamics - (DRO) :

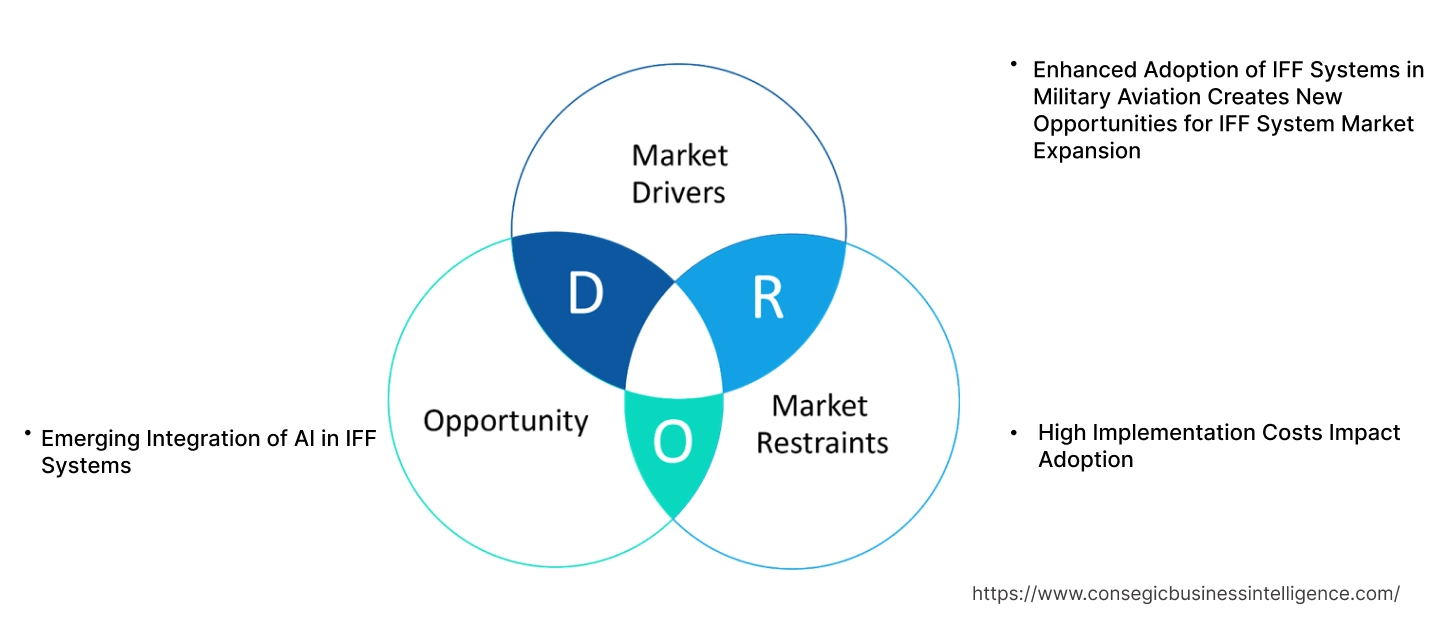

Key Drivers:

Enhanced Adoption of IFF Systems in Military Aviation Creates New Opportunities for IFF System Market Expansion

The IFF system market demand for Identification Friend or Foe (IFF) systems in military aviation has surged due to their ability to prevent friendly fire incidents. IFF systems enable accurate identification of allied and enemy aircraft, ensuring operational efficiency and enhanced battlefield safety. For instance, the installation of advanced Mode 5 IFF systems in fighter jets improves their capability to differentiate between friend and foe with encrypted communication protocols.

The growing use of IFF systems in modern military aviation is a significant factor boosting the global IFF system market.

Key Restraints:

High Implementation Costs Impact Adoption

The installation and integration of IFF systems involve substantial costs, including the expense of advanced radar systems, encryption modules, and compliance with stringent military standards. This financial barrier is particularly challenging for developing nations with limited defense budgets. For example, upgrading to advanced Mode 5 systems requires significant investment in both hardware and software components, making it difficult for cost-sensitive countries to adopt.

These high implementation costs act as a key restraint to the widespread adoption of IFF systems across the defense sector.

Future Opportunities :

Emerging Integration of AI in IFF Systems

The future integration of artificial intelligence (AI) into IFF systems is expected to revolutionize the market. AI algorithms can enhance real-time data processing and decision-making, significantly improving the accuracy of threat identification. For example, AI-powered systems could analyze complex flight patterns and environmental data to provide more reliable identification of friend or foe in high-stress combat scenarios.

The advancement of AI technologies presents substantial IFF system market opportunities for the evolution and growth in the coming years.

IFF System Market Segmental Analysis :

By Component:

Based on the component, the IFF system market is segmented into IFF software and IFF hardware (IFF transponder, IFF interrogator, crypto computers, IFF antenna, IFF test equipment, and others).

The IFF hardware sector accounted for the largest revenue in IFF system market share in 2024.

- IFF hardware includes transponders, interrogators, crypto computers, antennas, and test equipment, essential for the functionality of IFF systems.

- These components are crucial for identifying and distinguishing between friendly and enemy aircraft, vehicles, and ships.

- The IFF system market demand for advanced and reliable IFF hardware is driven by the need for enhanced situational awareness and secure identification in military operations.

- Therefore, according to Continuous technological advancements and the integration of IFF systems with modern defense platforms contribute to the revenue share of IFF hardware.

The IFF software sector is anticipated to register the fastest CAGR during the forecast period.

- IFF software is responsible for processing and managing the data received from IFF hardware components, ensuring accurate identification and communication.

- The increasing complexity of modern defense systems and the need for real-time data processing drive the trend for advanced IFF software solutions.

- Ongoing developments in software technologies and the integration of artificial intelligence and machine learning enhance the capabilities of IFF software.

- The rising adoption of digital and software-based solutions in defense systems fuels the rapid IFF system market growth of the IFF software sector.

By Application:

Based on the application, the IFF system market is segmented into surveillance and identification, air traffic control (ATC), combat operations, search and rescue (SAR), and navigation.

The surveillance and identification sector accounted for the largest revenue in IFF system market share in 2024.

- IFF systems play a critical role in surveillance and identification, enabling military and defense organizations to accurately identify friendly and enemy forces.

- These systems enhance situational awareness, reduce the risk of friendly fire incidents, and improve decision-making in combat scenarios.

- The growing emphasis on national security and the need for reliable identification systems drive the trend for IFF systems in surveillance and identification applications.

- The strategic importance of surveillance and identification in defense operations contributes significantly to the revenue share of this sector.

The combat operations sector is anticipated to register the fastest CAGR during the forecast period.

- IFF systems are essential in combat operations, providing real-time identification and communication capabilities to military forces.

- These systems enable secure and accurate identification of targets, enhancing the effectiveness of military operations.

- The increasing focus on modernizing defense forces and improving combat readiness drives the trend for advanced IFF systems in combat operations.

- Ongoing technological advancements and the integration of IFF systems with various defense platforms enhance their capabilities in combat scenarios.

- The growing emphasis on defense modernization and operational efficiency fuels the rapid IFF system market growth of the combat operations sector.

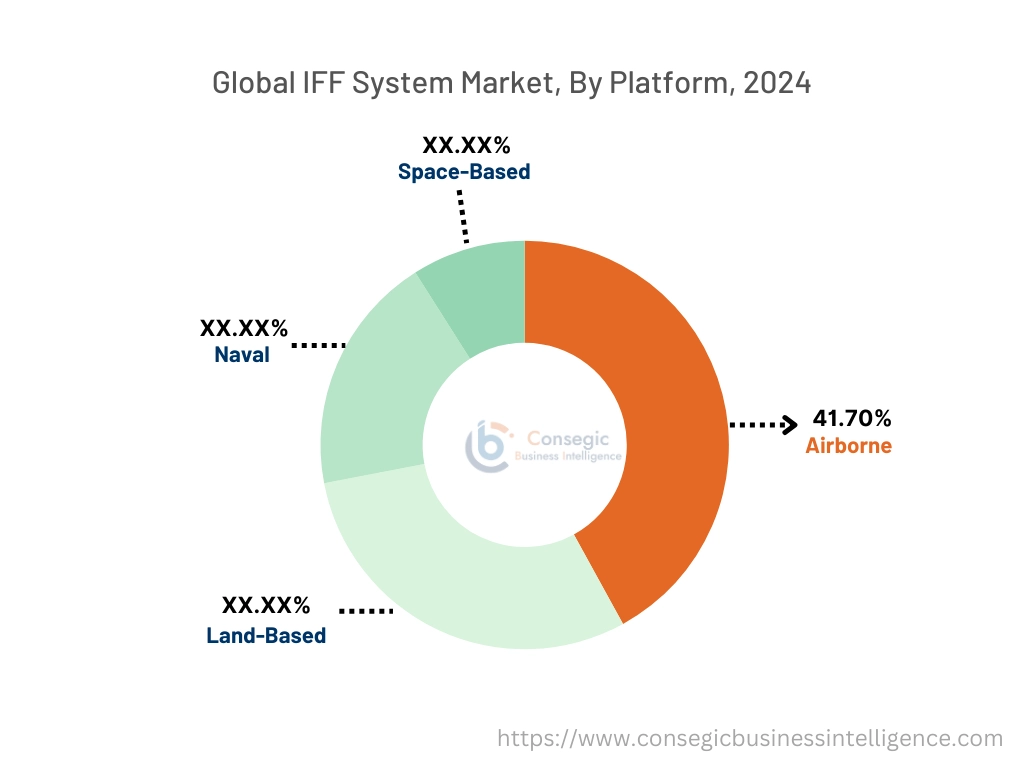

By Platform:

Based on the platform, the IFF system market is segmented into airborne, land-based, naval, and space-based.

The airborne sector accounted for the largest revenue share of 41.70% in 2024.

- IFF systems are extensively used in airborne platforms, including fighter jets, transport aircraft, and unmanned aerial vehicles (UAVs).

- These systems provide critical identification and communication capabilities, ensuring the safe and efficient operation of airborne assets.

- The increasing deployment of advanced aircraft and the need for secure identification in air combat and surveillance missions drive the demand for IFF systems in the airborne sector.

- The strategic importance and widespread use of IFF systems in airborne platforms contribute significantly to their revenue share.

The space-based sector is anticipated to register the fastest CAGR during the forecast period.

- Space-based IFF systems are designed for use in satellites and other space platforms, providing global coverage and enhanced identification capabilities.

- These systems enable secure and reliable communication and identification in space missions, supporting various defense and surveillance applications.

- The growing emphasis on space defense and the development of advanced satellite technologies drive the demand for space-based IFF systems.

- Ongoing advancements in space technology and the increasing focus on space security fuel the rapid IFF system market trend of the space-based sector.

By End User:

Based on the end user, the IFF system market is segmented into defense organizations, commercial aviation operators, security agencies, and others.

The defense organizations sector accounted for the largest revenue share in 2024.

- IFF systems are primarily used by defense organizations to enhance situational awareness, secure identification, and communication capabilities in military operations.

- These systems play a crucial role in national defense and security, supporting various military missions and activities.

- The increasing defense budgets and the need for advanced identification systems drive the demand for IFF systems in defense organizations.

- The strategic importance and widespread use of IFF systems in military operations contribute significantly to their revenue share.

The commercial aviation operators sector is anticipated to register the fastest CAGR during the forecast period.

- IFF systems are also used by commercial aviation operators to ensure safe and efficient air traffic control and navigation.

- These systems provide accurate identification and communication capabilities, supporting the safe operation of commercial aircraft.

- The increasing focus on aviation safety and the growing air traffic drive the demand for advanced IFF systems in commercial aviation.

- Ongoing advancements in aviation technology and the need for reliable identification and communication solutions fuel the rapid IFF system market trend of the commercial aviation operators sector.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

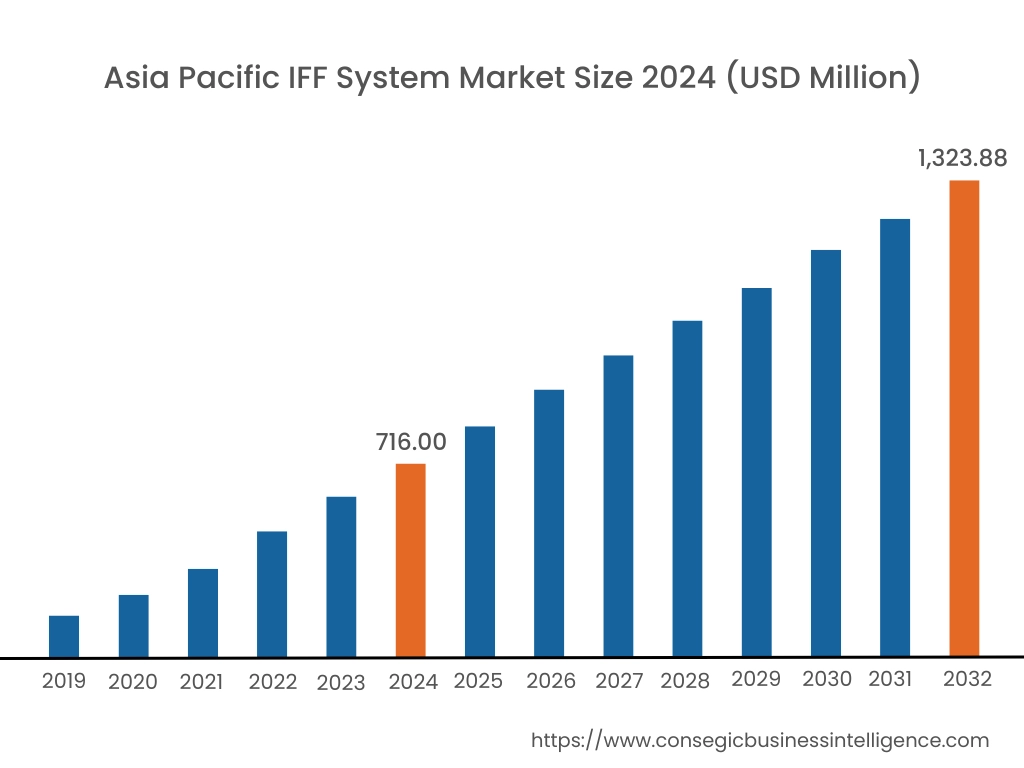

In 2024, North was valued at USD 716.00 Million and is expected to reach USD 1,323.88 Million in 2032. In North America, the U.S. accounted for the highest share of 73.50% during the base year of 2024. The United States and Canada have significantly invested in advanced military technologies, including IFF systems, to enhance situational awareness and prevent friendly fire incidents. The presence of leading defense contractors and substantial defense budgets support market growth. Regulatory support for defense modernization also contributes to the region's dominance.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 8.8% over the forecast period. Countries like China, India, and Japan are actively developing IFF systems to strengthen their military capabilities. The region's focus on defense modernization and technological advancements drives significant investments in IFF systems. Increasing defense expenditure and geopolitical tensions further boost market trend.

Europe has shown steady trend in the IFF system market. Nations like France, Germany, and the United Kingdom are investing in advanced military technologies, including IFF systems, to enhance their defense capabilities. Collaborative defense projects within the European Union contribute to the region's advancements in IFF technology. The emphasis on interoperability and defense modernization supports market trend.

The Middle East and Africa region has experienced moderate growth in the IFF system market. Countries like Saudi Arabia and the United Arab Emirates are investing in advanced defense systems, including IFF technology, to enhance their military capabilities. The region's strategic importance and the need for advanced weaponry drive the adoption of IFF systems. However, economic challenges and geopolitical instability pose barriers to IFF system market expansion.

Latin America has shown potential for growth in the IFF system market. Countries like Brazil and Argentina are exploring advanced military technologies, including IFF systems, to strengthen their defense capabilities. The region's focus on modernizing military forces and enhancing national security drives investments in IFF systems. Collaborations with global defense contractors and advancements in defense research support market growth.

Top Key Players and Market Share Insights:

The Global IFF System Market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global IFF System Market. Key players in the IFF System industry include-

- BAE Systems plc (United Kingdom)

- Raytheon Technologies Corporation (United States)

- Northrop Grumman Corporation (United States)

- General Dynamics Corporation (United States)

- Saab AB (Sweden)

- Thales Group (France)

- Leonardo S.p.A. (Italy)

- HENSOLDT AG (Germany)

- Indra Sistemas, S.A. (Spain)

- Elbit Systems Ltd. (Israel)

IFF System Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 4,084.79 Million |

| CAGR (2025-2032) | 8.3% |

| By Component |

|

| By Application |

|

| By Platform |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the IFF System Market? +

In 2024, the IFF System Market was USD 2,158.52 million.

What will be the potential market valuation for the IFF System Market by 2032? +

In 2032, the market size of IFF System Market is expected to reach USD 4,084.79 million.

What are the segments covered in the IFF System Market report? +

The component, application, platform, and end-user are the segments covered in this report.

Who are the major players in the IFF System Market? +

BAE Systems plc (United Kingdom), Raytheon Technologies Corporation (United States), Northrop Grumman Corporation (United States), Thales Group (France), Leonardo S.p.A. (Italy), HENSOLDT AG (Germany), Indra Sistemas, S.A. (Spain), General Dynamics Corporation (United States), Saab AB (Sweden), Elbit Systems Ltd. (Israel) are the major players in the IFF System market.