- Summary

- Table Of Content

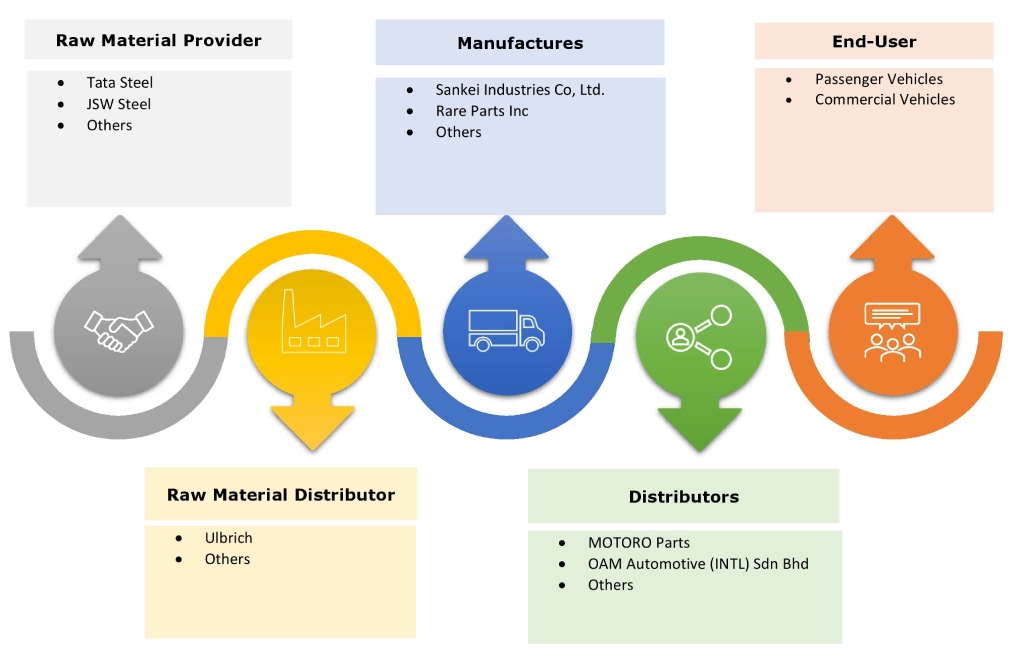

- Methodology

Idler Arm Market Size:

Idler Arm Market Size is estimated to reach over USD 5,569.77 Million by 2032 from a value of USD 3,900.43 Million in 2024 and is projected to grow by USD 4,051.37 Million in 2025, growing at a CAGR of 4.1% from 2025 to 2032.

Idler Arm Market Scope & Overview:

The idler arm is essential for the stability and smooth functioning of a vehicle's steering and suspension systems. It serves as a critical component that links the steering linkage to the vehicle's frame, facilitating controlled movement and proper alignment of the front wheels. Therefore, these systems are vital for ensuring vehicle safety, stability, and overall driving performance. The automotive idler arm market is influenced by several factors, including the rising sales and production of vehicles worldwide, along with an increasing focus on vehicle safety and comfort.

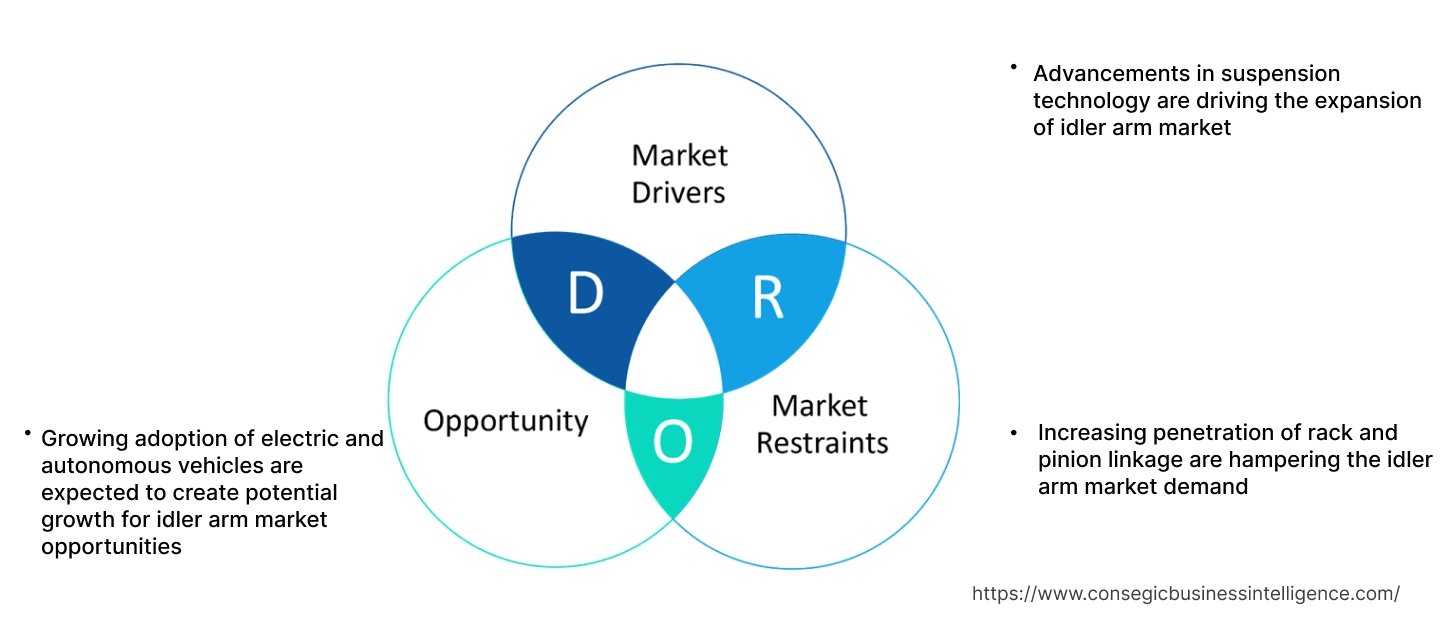

Idler Arm Market Dynamics - (DRO) :

Key Drivers:

Advancements in suspension technology are driving the expansion of idler arm market

Advancements in suspension technology have been instrumental in transforming the idler arm market, greatly enhancing vehicle handling, comfort, and safety. Continuous innovation has led to the evolution of suspension systems from traditional mechanical designs to advanced electronic systems that adapt dynamically to road conditions and driver inputs. These improvements have resulted in enhanced performance and stability, thereby enriching the overall driving experience for consumers. In relation to steering and suspension systems, which serve as essential components of the steering linkage system, these technological innovations contribute to smoother steering operations and improved control. Another important trend in suspension technology involves the integration of advanced materials and manufacturing methods to enhance the strength, durability, and weight efficiency of suspension components. Lightweight materials such as aluminum alloys and high-strength steel alloys are increasingly supplanting traditional cast iron and steel components, effectively reducing overall vehicle weight while preserving structural integrity. This transition not only boosts fuel efficiency and lowers emissions but also improves suspension responsiveness and agility.

- For instance, in July 2023, ZF Commercial Vehicle Solutions announced the agreement with Volvo Trucks, to provide core systems and components in the electric volta Zero. ZF has been chosen as the main provider for several crucial systems in the Volta Zero electric truck, including suspension, braking, and steering functions.

Thus, according to the idler arm market analysis, the rise in developments and trends in suspension technology are driving the idler arm market size.

Key Restraints:

Increasing penetration of rack and pinion linkage are hampering the idler arm market demand

The growing prevalence of rack and pinion steering linkage systems presents a challenge to the growth of the automotive idler arm sector. Rack and pinion systems have become favored for their precision, responsiveness, and efficiency in contemporary vehicles. These systems enhance handling and provide a more direct link between the driver's input and the vehicle's movement, thereby improving the overall driving experience. Consequently, automotive manufacturers are integrating rack and pinion systems in a variety of vehicles, particularly passenger cars and light trucks. This transition towards rack and pinion systems diminishes the demand for traditional steering systems, including those that utilize idler arm. Thus, growing penetration of rack pinion linkage and above analysis are hampering the global market.

Future Opportunities :

Growing adoption of electric and autonomous vehicles are expected to create potential growth for idler arm market opportunities

As the automotive industry progresses towards electric and autonomous vehicles, the global market is experiencing a notable transformation. Idler arms, essential components of steering systems, are being redesigned to meet the specific needs of electric and autonomous vehicles. These vehicles require precise and efficient steering mechanisms to support their advanced functionalities, leading to a demand for advanced automotive solutions and systems with improved durability, responsiveness, and compatibility with electric powertrains.

Moreover, the transition to electric and autonomous vehicles presents new challenges in suspension systems design and manufacturing. Electric vehicles, characterized by their unique power delivery systems and diminished reliance on traditional internal combustion engines, necessitate steering systems that can endure higher torque loads and operate effectively within electric drivetrains. Likewise, autonomous vehicles, equipped with advanced sensors and control systems, require advanced steering systems that seamlessly integrate with autonomous driving technologies while ensuring superior steering performance and safety.

- For instance, according to IEA, electric car sales experienced variation across regions and powertrains, yet China remained the dominant player. In 2022, battery electric vehicle (BEV) sales in China rose by 60% compared to 2021, reaching 4.4 million units, while plug-in hybrid electric vehicle (PHEV) sales nearly tripled to 1.5 million units.

Thus, based on the above analysis and trends, the growing adoption of electric vehicles is driving the idler arm market opportunities.

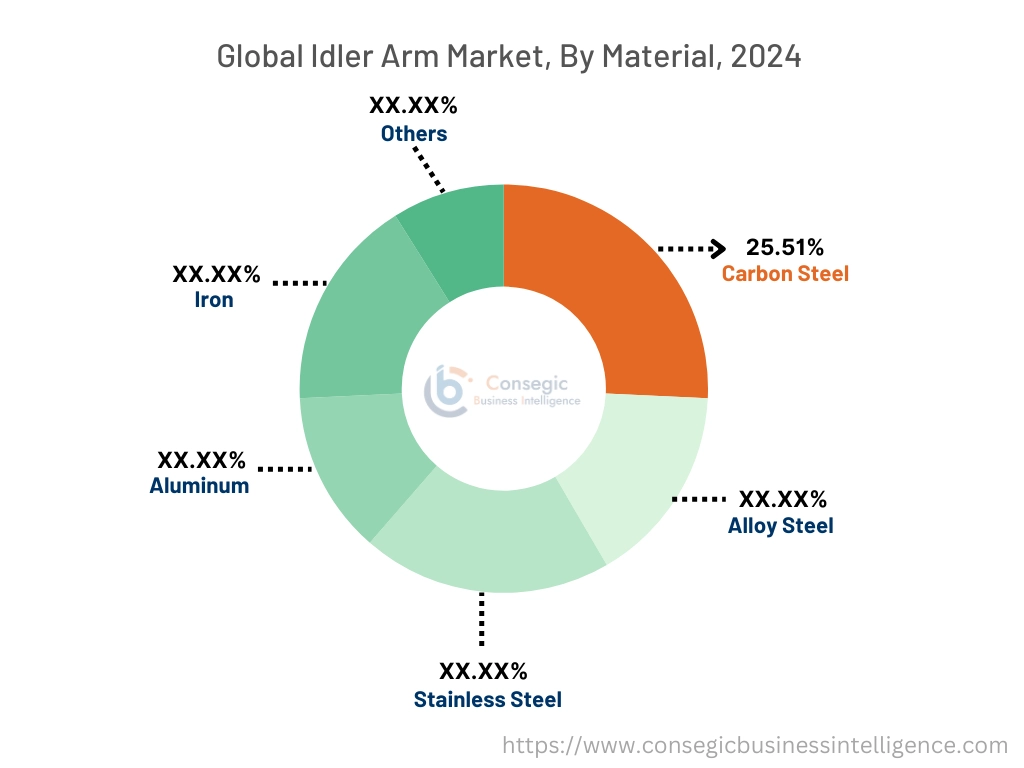

Idler Arm Market Segmental Analysis :

By Material:

Based on the material, the market is segmented into carbon steel, alloy steel, stainless steel, aluminum, iron, and others.

Trends in the material:

- Minimizing the weight of steering and suspension systems can enhance vehicle fuel efficiency and handling. This is accomplished by utilizing lightweight materials and advanced manufacturing techniques.

- Manufacturers are consistently seeking methods to reduce the production costs of steering and suspension without compromising quality and performance. This may include optimizing designs, streamlining manufacturing processes, and sourcing materials efficiently.

alloy steel segment accounted for the largest revenue share of 25.51% in the year 2024 and is expected to register the highest CAGR during the forecast period.

- Alloy steel is distinguished as a preferred material due to its remarkable strength, durability, and resistance to wear. Idler arms made from alloy steel demonstrate superior performance in challenging operating conditions, ensuring long-lasting reliability and stability within vehicle suspension systems.

- The high tensile strength of alloy steel guarantees optimal steering response and precise control, thereby enhancing the overall driving experience and safety.

- The rising performance expectations of modern vehicles necessitate components capable of withstanding higher stresses and functioning in more demanding environments. Alloy steels deliver the required strength and durability to fulfil these needs.

- For instance, Moog’s arms are designed for steering support and safer operations. The MOOG steering system facilitates smooth, predictable steering and enhances performance even in the most challenging conditions. Its premium one-piece forged steel housing provides increased durability.

- Recent advancements in steelmaking and manufacturing techniques have resulted in the creation of higher-strength and more cost-effective alloy steels, further positioning them as an appealing choice for automotive manufacturers.

- These trends, factors, analysis, and developments in the alloy steel segment would further drive the idler arm market size during the forecast period.

By Vehicle Type:

Based on the vehicle type, the market is segmented into passenger vehicles and commercial vehicles.

Trends in the vehicle type:

- The growth of the global automotive industry directly influences the demand for advanced automotive products and solutions. The rise in vehicle production across all segments leads to an increased need for original equipment and replacement parts.

- Older vehicles tend to experience greater wear and tear, resulting in an increased probability of requiring steering systems replacements. This factor drives a consistent need for replacement parts in the aftermarket.

The passenger vehicle segment accounted for the largest revenue share in the year 2024.

- Passenger vehicles constitute a significant segment of the global market, which includes sedans, hatchbacks, SUVs, and crossovers. These systems are essential for sustaining steering stability, which facilitates smooth handling and control for both drivers and passengers.

- To cater driver comfort and vehicle dynamics, automotive manufacturers are eager to incorporate advanced suspension components, such as steering systems, to enhance handling characteristics and reduce vibrations.

- For instance, in October 2022, Hitachi Astemo, Ltd. has unveiled a prototype for an advanced steer-by-wire steering system. This innovative technology eliminates the need for traditional steering wheels, thereby increasing cabin space. Such advancements are essential for the development of future-generation vehicles and autonomous cars.

- Thus, factors such as focus on driver comfort would further supplement the idler arm market growth during the forecast period.

The commercial vehicles segment is anticipated to register the fastest CAGR during the forecast period.

- The global market in the realm of commercial vehicles is experiencing increased need due to the development of the commercial transportation sector and the rise of heavy-duty vehicles. Commercial vehicles such as trucks, buses, and utility vehicles operate under harsh conditions and face greater loads and stress more than passenger vehicles. The arm plays a vital role in sustaining steering accuracy and stability, which is essential for safe and efficient operation.

- As fleet operators and logistics companies prioritize vehicle safety, reliability, and operational efficiency, there is a growing need for strong and durable suspension components, leading to the adoption of advanced automotive solutions in the commercial vehicle sector.

- Manufacturers of steering systems are under pressure to create products that can withstand tough operating conditions while providing optimal performance and durability.

- Thus, emphasis on durability, reliability, and customizable performance presents prospects for innovation and product differentiation within the commercial vehicle segment, driving the trends of the idler arm market growth.

By Sales Channel:

Based on the sales channel, the market is segmented into OEMs and aftermarket.

Trends in the sales channel:

- Online sales platforms are becoming increasingly prominent, providing convenient access to a diverse selection of automotive products for consumers and repair shops. This trend is anticipated to persist, further disrupting traditional distribution channels.

- Both OEMs and aftermarket suppliers are placing greater emphasis on quality and reliability. This shift is influenced by consumer expectations and the necessity to uphold vehicle safety and performance.

OEMs segment accounted for the largest revenue share in the year 2024.

- OEMs, which include vehicle manufacturers, are pivotal in the initial integration of steering systems into new vehicles throughout the production process. These collaborations with OEMs typically involve long-term contracts to guarantee the integration of steering systems that comply with rigorous quality standards and specifications.

- The OEM segment gains from the consistent requirement for automotive products, fuelled by rising vehicle production volumes and the ongoing necessity for suspension components that promote vehicle safety, stability, and performance.

- Technological innovations in suspension systems and an increasing focus on driving comfort further enhance the demand for high-quality steering systems from OEMs.

- Thus, rise in technological innovations would further supplement the global market during the forecast period.

The aftermarket segment is anticipated to register the fastest CAGR during the forecast period.

- The aftermarket segment is driven by factors including vehicle age, wear and tear, and the necessity for component replacements due to damage or malfunction. As vehicles age and accrue mileage, components like suspension parts, may experience wear and need replacement to ensure optimal vehicle performance and safety.

- In this segment, a varied ecosystem of distributors, retailers, and e-commerce platforms primarily facilitates the distribution and sale of steering systems to end consumers. These channels provide a broad selection of automotive products, accommodating different vehicle makes and models as well as the budgetary needs of vehicle owners.

- Aftermarket suppliers frequently emphasize value-added services such as product warranties, technical support, and installation assistance to distinguish themselves in a competitive market environment.

- For instance, in March 2021, SKF India’s automotive aftermarket segment launched three new products designed to meet the evolving needs of customers across various sectors in India. The new offerings include Steering and Suspension Systems for 4-wheelers, Timing Belts, and Chain and Sprockets for 2-wheelers. This innovative product range features high quality, superior strength, and long-lasting durability.

- As the automotive industry continues to evolve, aftermarket sales channel expected to remain essential contributor to the continued development and innovation within the global market share.

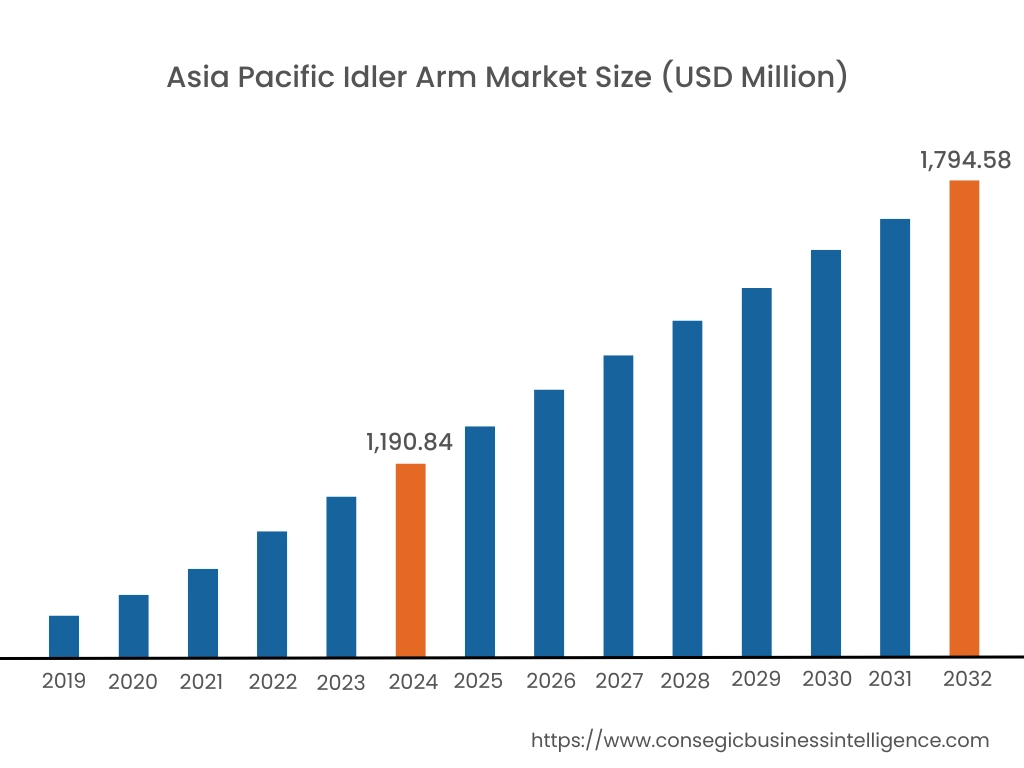

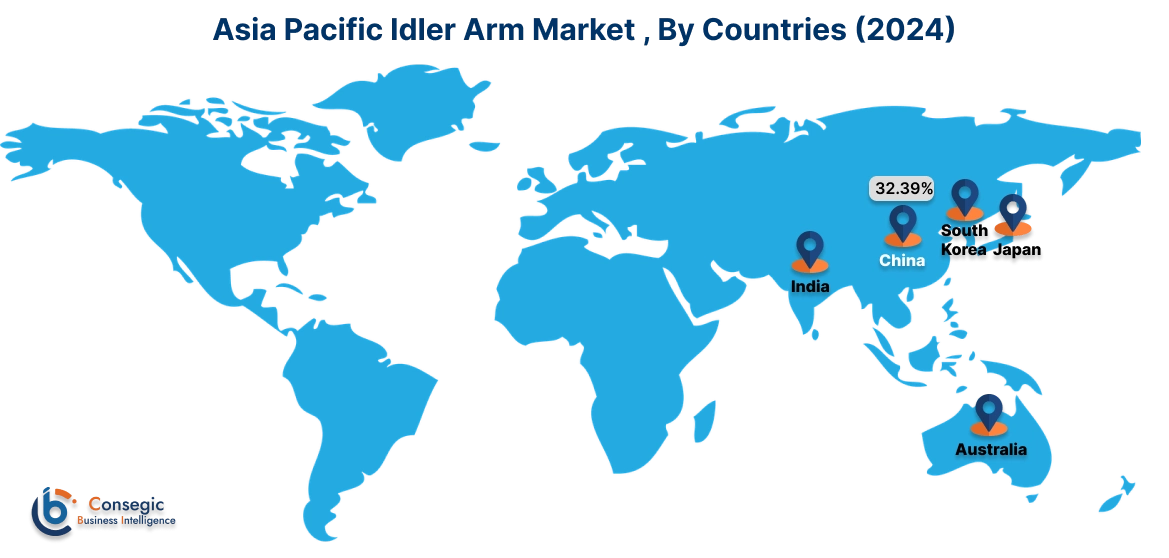

Regional Analysis:

The global market has been classified by region into North America, Europe, Asia-Pacific, MEA, and Latin America.

Asia Pacific idler arm market expansion is estimated to reach over USD 1,794.58 million by 2032 from a value of USD 1,190.84 million in 2024 and is projected to grow by USD 1,242.63 million in 2025. Out of this, the Chinese market accounted for the maximum revenue split of 32.39%. The Asia Pacific region is expected to become a profitable market for automotive products, influenced by rapid urbanization, increasing disposable incomes, and growing vehicle production. Countries such as China, Japan, and India are experiencing notable development in automotive manufacturing and sales, providing significant prospects for market participants. Further, the heightened focus on vehicle safety and comfort, along with the development of aftermarket sales channels, supports market growth in the region. Furthermore, the transition to electric vehicles (EVs) in countries such as China is accelerating market development, as EV manufacturers focus on developing lightweight and durable steering components to enhance vehicle performance and efficiency. These factors are expected to further drive the regional idler arm market share in the coming years.

- For instance, in December 2024, BYD, the Chinese car manufacturer, sold 509,440 electric passenger vehicles and plug-in hybrid vehicles, which includes 207,734 EVs, bringing the total annual sales of battery-powered cars to 1.76 million. The company's overall annual sales rose by 41% compared to the previous year.

North America idler arm market is estimated to reach over USD 1,948.31 million by 2032 from a value of USD 1,379.45 million in 2024 and is projected to grow by USD 1,431.43 million in 2025. The regional development is driven by technological advancements in the automotive sector and the presence of key automotive players. The increasing number of vehicles on the road and the rising average age of these cars, the need for replacement parts remains strong in the region. Additionally, the shift towards more advanced vehicle designs, including enhanced steering systems, is prompting manufacturers to innovate and enhance the performance of automotive products. The development of e-commerce has also expanded access for consumers and automotive service providers to a broader range of automotive products, contributing to market expansion. Moreover, the growing adoption of automated driving systems, which require precise wheel alignment and stability, is further boosting market requirements. In addition to this, advances in materials science are facilitating the creation of lighter and more durable automotive products, thus enhancing vehicle performance and fuel efficiency. These factors would further drive the regional idler arm market share during the forecast period.

- For instance, in November 2022, Apollo Funds announced the acquisition of Tenneco, a leading designer, manufacturer, and marketer of automotive products for OEMs and aftermarket customers. Tenneco Inc., a US-based firm focused on manufacturing automotive components and aftermarket ride control solutions, notably features products like idler arm and emissions solutions in its portfolio. This acquisition supports Apollo's strategic goals of fostering innovation and strengthening Tenneco's position in the automotive sector.

According to the idler arm industry analysis, the European market is set to experience consistent progression due to the region's strong automotive manufacturing sector and rigorous regulatory standards. The focus on emission reduction and enhanced fuel efficiency has led to the incorporation of advanced suspension systems, including idler arm, in vehicles. Further, innovations in suspension design and the presence of key market players are vital to this growth. However, competitive pressures and market saturation in developed economies may pose challenges to the market's advancement in Europe.

Additionally, Latin American market offer both opportunity and challenges for the regional market. Countries like Brazil and Mexico boast dynamic automotive industries and rising vehicle sales, but economic uncertainties and political instability may affect market progression. The increasing emphasis on vehicle safety standards, along with the development of after-market sales channels, presents opportunities for market participants. Moreover, technological advancements and partnerships with local manufacturers could further stimulate market development in Latin America throughout the forecast period.

Furthermore, in MEA region, the market is anticipated to witness moderate growth during the forecast period. Factors such as infrastructure development, urbanization, and escalating investments in the automotive sector are driving market development. The rising need for commercial vehicles, particularly in the construction and logistics sectors, is fueling the adoption of idler arm. Thus, based on the above idler arm market analysis and trends, the rise in commercial vehicles and urbanization would further drive the regional market during the forecast period.

Top Key Players and Market Share Insights:

The global idler arm market is highly competitive with major players providing solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the idler arm industry includes-

- Dorman Products (U.S.)

- DRiV Incorporated (Moog) (U.S.)

- Chase Steering Parts Co. (Taiwan)

- Mevotech (U.S.)

- JCBL Auto Moto (India)

- CJ MANUFACTURING COMPANY LIMITED (Thailand)

- Sankei Industries Co, Ltd (Japan)

- Highlink Auto Parts Co., Ltd. (Taiwan)

- GMB Corporation (Japan)

- Rare Parts Inc (U.S.)

Recent Industry Developments :

Product Launch:

- In May 2024, Mevotech launched the addition of 188 new part numbers, including TTX steering idler and pitman arms, which features 3 new part numbers applicable to wide range of light and medium duty pickup trucks, SUVs, and vans. These components are developed using patented technology and are designed as superior alternatives for vehicles frequently utilized in a professional capacity.

Idler Arm Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 5,569.77 Million |

| CAGR (2025-2032) | 4.1% |

| By Material |

|

| By Vehicle Type |

|

| By Sales Channel |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Idler Arm market? +

Idler Arm Market Size is estimated to reach over USD 5,569.77 Million by 2032 from a value of USD 3,900.43 Million in 2024 and is projected to grow by USD 4,051.37 Million in 2025, growing at a CAGR of 4.1%from 2025 to 2032.

Which is the fastest-growing region in the Idler Arm market? +

Asia-Pacific is the region experiencing the most rapid growth in the market. Technological advancements, including the incorporation of sensors and actuators in idler arms, are driving innovation in the sector. Government regulations pertaining to vehicle safety standards and emissions influence product design and manufacturing processes. The concentration of end-users is significant, with automotive OEMs and aftermarket parts suppliers as the primary consumers.

What specific segmentation details are covered in the Idler Arm report? +

The idler arm report includes specific segmentation details for material, vehicle type, sales channel, and region.

Who are the major players in the Idler Arm market? +

The key participants in the market are Dorman Products (U.S.), DRiV Incorporated (Moog) (U.S.), CJ MANUFACTURING COMPANY LIMITED (Thailand), Sankei Industries Co, Ltd (Japan), Highlink Auto Parts Co., Ltd. (Taiwan), GMB Corporation (Japan) Rare Parts Inc (U.S.), Chase Steering Parts Co. (Taiwan), Mevotech (U.S.), JCBL Auto Moto (India), and others.