- Summary

- Table Of Content

- Methodology

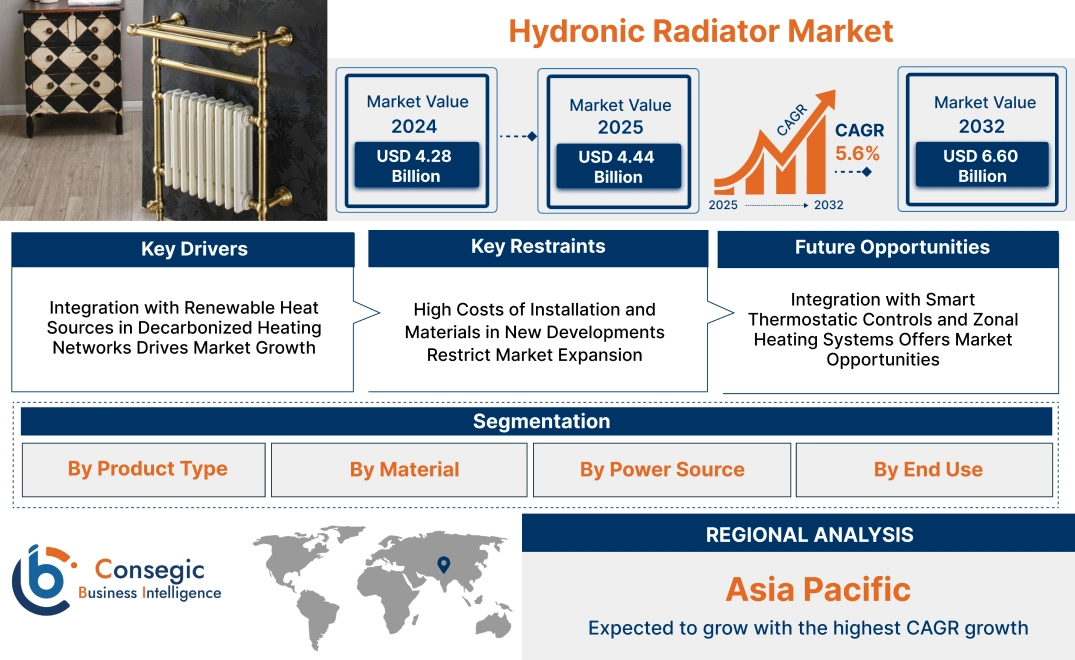

Hydronic Radiator Market Size:

Hydronic Radiator Market size is estimated to reach over USD 6.60 Billion by 2032 from a value of USD 4.28 Billion in 2024 and is projected to grow by USD 4.44 Billion in 2025, growing at a CAGR of 5.6% from 2025 to 2032.

Hydronic Radiator Market Scope & Overview:

Hydronic radiator is a unit for distribution of heat using hot water in a closed-loop system, which is typically connected to a central boiler or heat pump. It releases radiant and convective heat, giving a steady indoor warmth in domestic, commercial, and institutional buildings. The system runs quietly and economically, which makes it ideal for spaces that need comfort and control.

Made of such materials as steel, aluminum, or cast iron, such radiators are preferred for their long life, heat conduction properties, and visual versatility. They usually have programmable thermostatic valves, corrosion-resistant coatings, and modularized designs to suit different room capacities and configurations.

They facilitate even heat distribution and reduce energy loss, increase room comfort and decrease dependency on forced-air systems. Being adaptable to high- and low-temperature systems, it remains a go-to solution for rooms looking for effective, quiet, and low-maintenance heating performance.

Hydronic Radiator Market Dynamics - (DRO):

Key Drivers:

Integration with Renewable Heat Sources in Decarbonized Heating Networks Drives Market Growth

Hydronic radiators are increasingly being embraced as components of low-temperature renewable energy-driven heating systems, including solar thermal, biomass, and geothermal. These efficiently work with water supply temperatures from 35°C to 55°C, corresponding to the operating profile of hydronic radiators. They can distribute heat uniformly without dependency on high-temperature fuels and are beneficial to both comfort and energy efficiency. In decarbonizing district heating networks, hydronic emitters provide compatibility with centralized renewable heat infrastructure. This is also essential in residential buildings embracing air-to-water heat pumps, where low-temperature performance on a consistent basis is paramount. With national policies driving fossil fuel phaseouts and backing renewable heat growth, such systems are being integrated in public and private building developments. The coincidence of these heating systems with green building regulations and energy transformation objectives is fueling steady demand, resulting in long-term hydronic radiator market expansion.

Key Restraints:

High Costs of Installation and Materials in New Developments Restrict Market Expansion

The use of hydronic radiator systems in new developments involves heavy spending on plumbing networks, thermostatic controls, and heat sources like boilers or heat pumps. Such systems tend to cost more in material and labor to install than electric heaters, which are simpler to install and less demanding of building trades coordination. In residential and mid-rise commercial construction under severe capital constraints, builders tend to favor alternatives offering simple functionality at lower initial expense. This fiscal prioritization slows adoption of complex hydronic systems, even where their eventual efficiency is better. Furthermore, the stringent project timelines deter technologies that enhance design coordination or installation labor. Though developers acknowledge the efficiency advantages, the upfront cost remains a deterrent, especially in budget-sensitive areas or entry-level housing. Such economic deterrents limit the adoption of water-based heating systems in new projects, decelerating the overall hydronic radiator market growth.

Future Opportunities:

Integration with Smart Thermostatic Controls and Zonal Heating Systems Offers Market Opportunities

Smart thermostatic radiator valve (TRV) and room-by-room heating controls are creating new opportunities for the optimization of hydronic radiator performance. Digital components enable end-users to configure individual room temperatures, monitor consumption data, and integrate heating schedules with smart home platforms. Energy savings through optimized heating only where required fit within larger energy conservation objectives. Commercial buildings and multifamily residences are also embracing these systems to offer tenant-level control while enabling centralized energy management. There is growing demand for intelligent, responsive, and user-friendly heating systems, especially in areas with dynamic electricity pricing or stringent energy efficiency standards. These smart controls not only increase comfort but also enhance the energy performance profile of the overall heating system. The union of hydronic heating efficiency with digital control potential is generating new growth prospects in both new-build and retrofit markets, adding to long-term hydronic radiator market opportunities.

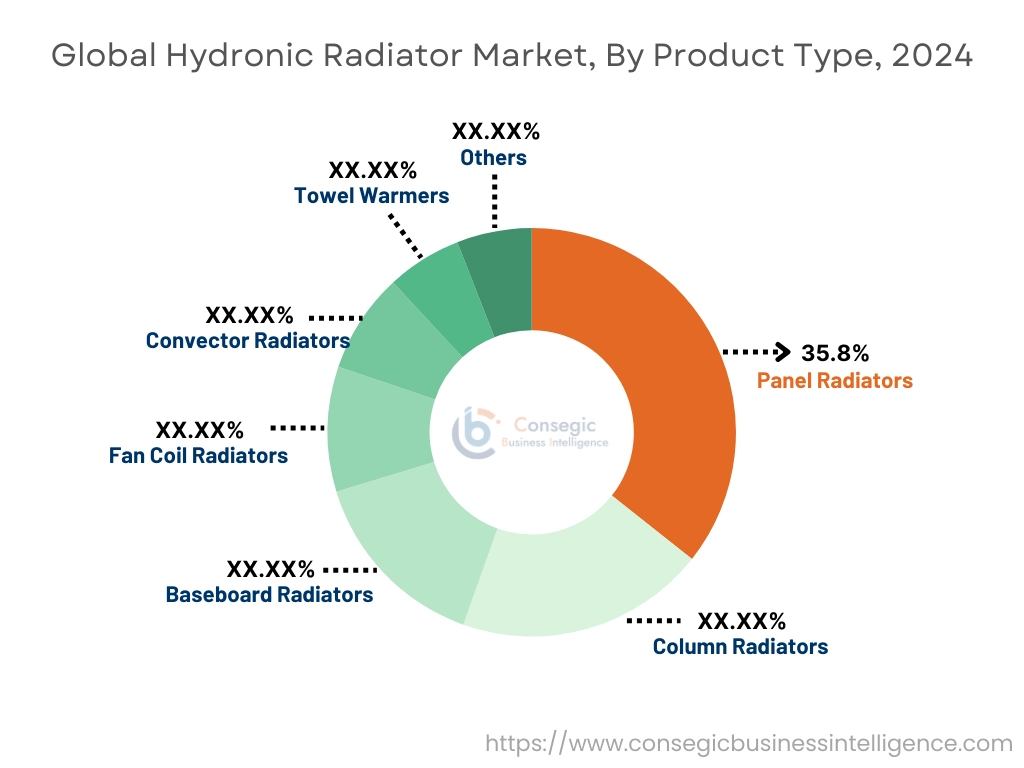

Hydronic Radiator Market Segmental Analysis :

By Product Type:

Based on product type, the hydronic radiator market is segmented into panel radiators, column radiators, baseboard radiators, fan coil radiators, convector radiators, towel warmers, and others.

The panel radiator segment accounted for the largest revenue share of 35.8% in 2024.

- Panel radiators are preferred due to their compact size and effective heat distribution across residential and commercial properties.

- Their flat profile and double-panel design allow for even heating and high energy efficiency.

- According to segmental analysis, their affordability and easy installation make them popular.

- Owing to the increased energy efficiency requirements in residential building construction, the hydronic radiators market demand for panel types is increasingly rising.

The fan coil radiator segment is projected to register the fastest CAGR during the forecast period.

- Fan coil radiators make use of fans to improve heat transfer, which makes them apt for dynamic temperature control in contemporary HVAC systems.

- These units provide fine control and quick response, which is perfect for commercial and institutional uses.

- Advances in technology have resulted in an increase in the integration of fan coil units with smart thermostats and automation systems.

- According to the hydronic radiator market trends, demand is increasing because of the growth in energy-efficient building projects and retrofitting existing buildings.

By Material:

Based on material, the hydronic radiator market is segmented into steel, aluminum, cast iron, copper, and others.

The steel segment accounted for the largest hydronic radiator market share in 2024.

- Steel radiators provide a compromise of strength, value, and quick thermal response, making them ideal for light commercial and residential applications.

- Steel radiators are produced in many sizes and coatings, which satisfy modern interior style requirements.

- The corrosion resistance of steel leads to long life on the job, aiding market growth.

- Current trends in environmentally friendly manufacturing also support recyclable steel solutions, which continue to fuel the hydronic radiator market growth.

The aluminum segment is expected to grow at the fastest CAGR during the forecast period.

- Aluminum radiators are light in weight and warm up rapidly, offering energy efficiency and user comfort.

- They can be used in low-temperature systems and integration with renewable energy sources, such as solar heating.

- Growing usage in green buildings is propelling the hydronic radiator market demand for aluminum-based systems.

- With increasing green consciousness, aluminum's recyclability is a factor in its increasing popularity in Europe and North America.

By Power Source:

Based on power source, the hydronic radiator market is segmented into electricity and fossil fuel.

The electricity segment accounted for the largest revenue share in 2024.

- Electric hydronic radiators find extensive applications in areas with renewable electricity availability and energy-efficient building codes.

- They provide accurate control of temperature and zoning features with minimal installation needs.

- Hydronic radiator market analysis shows popularity in retrofits and modular homes for simplicity of installation.

- With growing electrification and sustainability initiatives, the segment is also aided by favorable policies.

The fossil fuel segment is expected to grow at the fastest CAGR during the forecast period.

- Fossil fuel radiators, usually hooked up to oil or gas boilers, continue to be common in aged infrastructures and rural settings.

- Advancements in boiler technologies and hybrid systems expand the applicability of this segment in mixed-energy systems.

- Irrespective of decarbonization, its demand continues in areas with inadequate electrical grid infrastructure.

- According to hydronic radiator market trends, its integration with condensing boilers and heat exchangers to realize increased efficiency is on the upswing.

By End Use:

Based on end-use, the market is segmented into residential, commercial, industrial, and institutional.

The residential segment accounted for the largest hydronic radiator market share in 2024.

- Growing urbanization and consumer concern with energy efficiency are key drivers in the residential segment.

- Incentives offered by the government on energy-efficient heating systems have promoted their installation in new residences.

- According to hydronic radiator market analysis, compatibility with smart thermostats maximizes energy savings in the residential area.

- For instance, in February 2024, S. Boiler Company launched the new Ambient Air-to-Water Hydronic Heat Pump. The 5-ton capacity pump is able to provide reliable space heating with outdoor temperatures as low as -13°F. Its features include easy installation, environmentally friendly R-32 refrigerant for high efficiency and quiet operation.

- The move toward comfort-based living and green home infrastructure continues to drive segment growth.

The commercial segment is projected to register the fastest CAGR during the forecast period.

- Offices, hotels, and schools are switching from old-fashioned heating systems to efficient hydronic alternatives.

- The hydronic radiator market expansion is facilitated by smart building technologies that provide centralized control and predictive maintenance.

- Aesthetic and modular radiator choices suit architectural flexibility in commercial buildings.

- Steadily growing emphasis on indoor air quality and green certifications such as LEED continues to drive adoption in this market.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

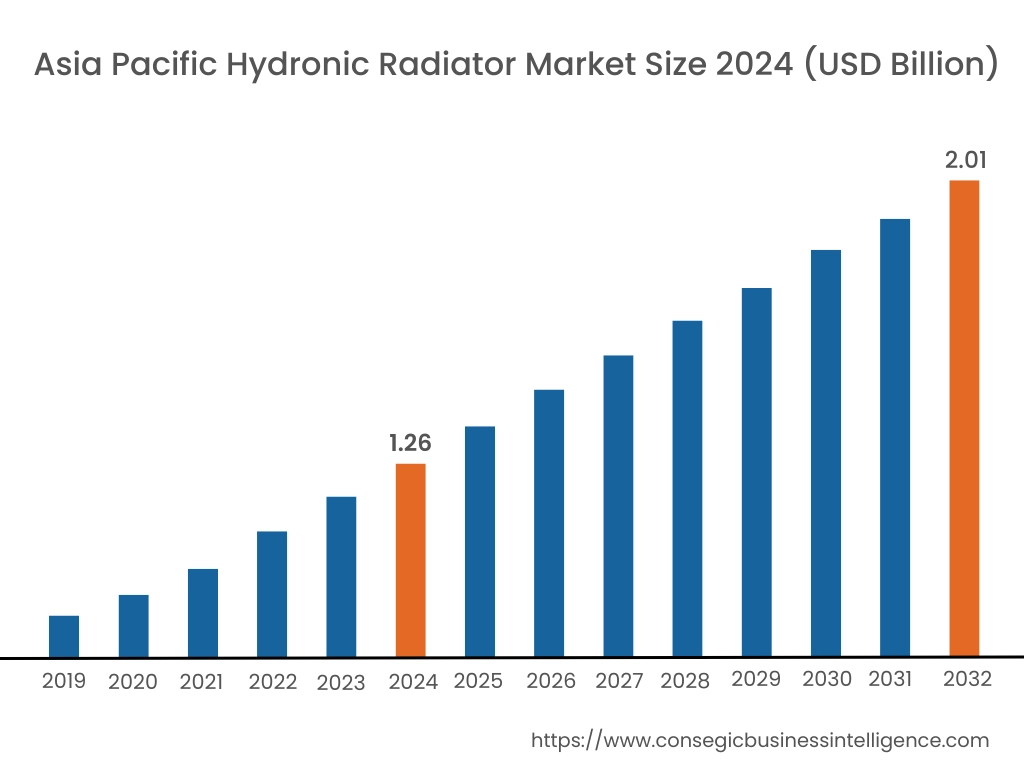

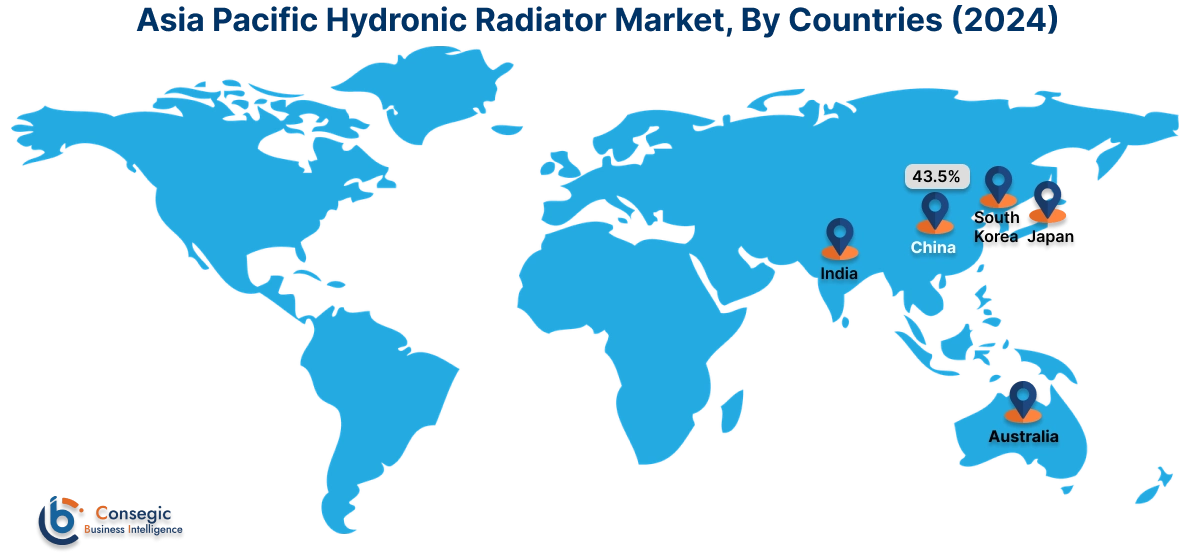

Asia Pacific region was valued at USD 1.26 Billion in 2024. Moreover, it is projected to grow by USD 1.31 Billion in 2025 and reach over USD 2.01 Billion by 2032. Out of this, China accounted for the maximum revenue share of 43.5%. Asia-Pacific is the most rapidly growing region, driven by increasing construction work and greater focus on indoor climate control in countries such as China, Japan, and South Korea. Market research indicates that radiant floor heating prevails in certain market segments but is being gradually replaced by hydronic radiators in urban dwellings, hospitals, and schools. Urbanization, improved living standards, and energy efficiency campaigns by governments are propelling product acceptance. Local producers are also committing to localized manufacturing and distribution networks to address increasing demand. The demand for greater sustainability, comfort, and noise reduction in heating products also enhances long-term prospects.

North America is estimated to reach over USD 1.81 Billion by 2032 from a value of USD 1.16 Billion in 2024 and is projected to grow by USD 1.20 Billion in 2025. North America registers moderate but consistent demand, mainly in cold areas of the United States and Canada. Application of hydronic heating systems is most focused in retrofitted residential complexes and institutional buildings with the objective of lowering operating heating expenses. Market research identifies escalating use of panel and baseboard radiators in green building projects that are emphasizing quiet operation and thermal comfort. Urban residences becoming increasingly smaller and tighter energy codes strengthen the demand for low-profile, high-efficiency heating systems. The area's transition to electrification and demand for energy-saving solutions offer long-term growth potential in both residential and light commercial markets.

Europe is the most developed and technologically advanced region for the hydronic radiator industry, aided by extensive district heating infrastructure, ambitious energy efficiency measures, and cultural affinity for radiant heating systems. Nations like Germany, France, Italy, and the UK continue to fund low-temperature heating networks, where new radiator designs are heat pump and condensing boiler compatible. Market analysis in detail indicates an increasing trend towards aluminum and hybrid radiators that have faster heat-up times and greater sustainability.

- For instance, in November 2024, tado° X launched all its products in the UK. This included Wireless Smart Thermostat X, Smart Radiator Thermostat X, Wireless Temperature Sensor X, Wired Smart Thermostat X and the Heat Pump Optimizer X with upgrades. Compatible with Amazon Alexa, Google Assistant or Apple HomeKit, these products ensure energy savings and lower a home’s carbon footprint.

Additionally, comprehensive renovation projects in Europe's older building inventories provide manufacturers of aesthetically sophisticated and performance-enhanced products with a significant hydronic radiator market opportunity.

Latin America is a maturing market in which acceptance is slowly picking up in regions with higher altitudes and colder climates like southern Brazil, Argentina, and the more temperate zones of Chile. The interest in radiant heating in the region is highly associated with luxury housing developments and tourist-oriented infrastructure emphasizing comfort and energy efficiency. Research shows that even though existing market penetration is restricted, increased knowledge of hydronic heating advantages and increasing green building are anticipated to spur demand. Market potential lies in propagating compact and modular radiator solutions appropriate for lower residential footprints.

The Middle East and Africa region is presently characterized by the lack of widespread application of hydronic radiators, largely owing to the prevalence of cooling systems and the warm climate trend of the region. Demand is, however, starting to pick up in regions of high altitude or winter susceptible locations like the areas of Turkey, Iran, and South Africa. Institutional projects, luxury housing, and luxury hospitality developments in colder climates drive adoption, as per market research. With the introduction or strengthening of building energy codes, the opportunity for effective heating solutions will increase, but at a diminishing rate. Long-term growth will depend on localized education and access to locally adapted product forms appropriate to varied climatic and infrastructure conditions.

Top Key Players & Market Share Insights:

The hydronic radiator market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global hydronic radiator market. Key players in the hydronic radiator industry include -

- Purmo Group (Finland)

- Zehnder Group (Switzerland)

- Korado Group (Czech Republic)

- IRSAP S.p.A. (Italy)

- Jaga N.V. (Belgium)

- Stelrad Radiator Group (United Kingdom)

- Kermi GmbH (Germany)

- Vasco Group (Belgium)

- Arbonia AG (Switzerland)

- De'Longhi Radiators (Italy)

Recent Industry Developments :

Product Launches:

- In February 2024, ITR launched a new hydronic heating system, OASIS SCH33. It features a 33,000 True Output BTU burner, a 1,500-watt AC electric element as well as an optional on-demand hot water. Its tank design provides freeze protection and operates silently.

Hydronic Radiator Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 6.60 Billion |

| CAGR (2025-2032) | 5.6% |

| By Product Type |

|

| By Material |

|

| By Power Source |

|

| By End Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Hydronic Radiator Market? +

Hydronic Radiator Market size is estimated to reach over USD 6.60 Billion by 2032 from a value of USD 4.28 Billion in 2024 and is projected to grow by USD 4.44 Billion in 2025, growing at a CAGR of 5.6% from 2025 to 2032.

What specific segmentation details are covered in the Hydronic Radiator Market report? +

The Hydronic Radiator market report includes specific segmentation details for product type, material, power source and end-use.

What are the end-uses of the Hydronic Radiator Market? +

The end-uses of the Hydronic Radiator Market are residential, commercial, industrial and institutional.

Who are the major players in the Hydronic Radiator Market? +

The key participants in the Hydronic Radiator market are Purmo Group (Finland), Zehnder Group (Switzerland), Stelrad Radiator Group (United Kingdom), Kermi GmbH (Germany), Vasco Group (Belgium), Arbonia AG (Switzerland), De'Longhi Radiators (Italy), Korado Group (Czech Republic), IRSAP S.p.A. (Italy) and Jaga N.V. (Belgium).