- Summary

- Table Of Content

- Methodology

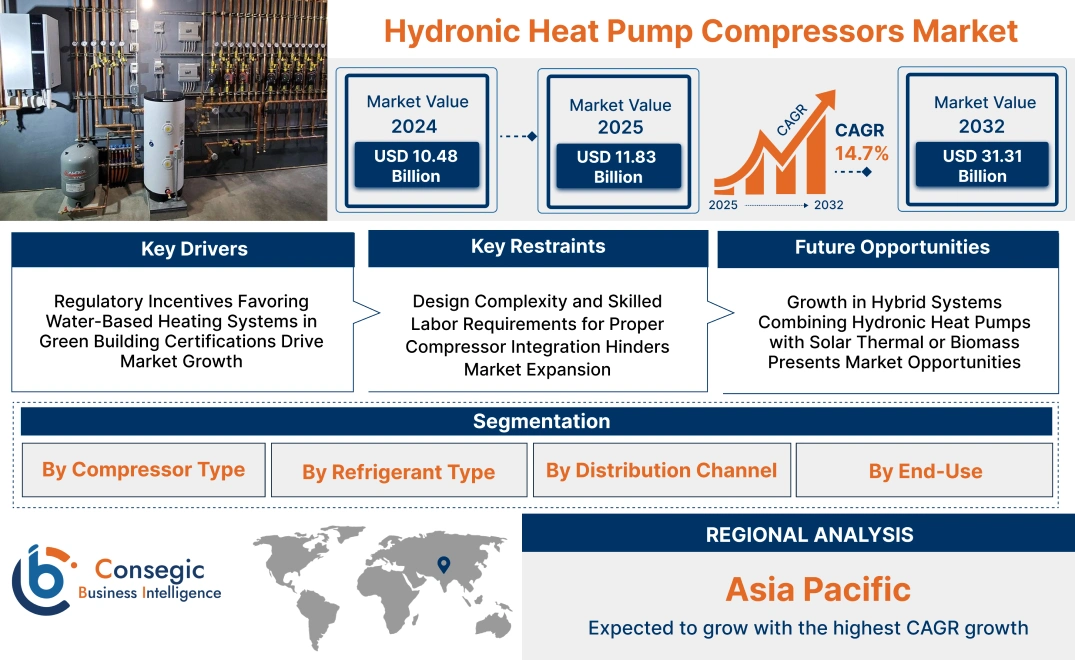

Hydronic Heat Pump Compressors Market Size:

Hydronic Heat Pump Compressors Market size is estimated to reach over USD 31.31 Billion by 2032 from a value of USD 10.48 Billion in 2024 and is projected to grow by USD 11.83 Billion in 2025, growing at a CAGR of 14.7% from 2025 to 2032.

Hydronic Heat Pump Compressors Market Scope & Overview:

Hydronic heat pump compressors are specialized components used in water-based heating and cooling systems to ensure efficient thermal energy transfer using refrigerant compression. These compressors form the core of hydronic heat pumps, enabling circulation of heated or cooled water to radiators, underfloor systems, or fan coils in residential, commercial, and institutional buildings.

Available in scroll, rotary, and screw configurations, they feature variable-speed operation, compact form factors, and optimized thermal output. Their design ensures precise modulation, reduced mechanical stress, and stable performance across varying load conditions.

Hydronic heat pump compressors contribute to enhanced energy efficiency, consistent indoor comfort, and lower operating costs. Their integration allows seamless connection to both low- and high-temperature distribution systems. Furthermore, they fulfil modern building standards focused on sustainability, control precision, and long-term thermal performance by ensuring quiet operation and flexible installation.

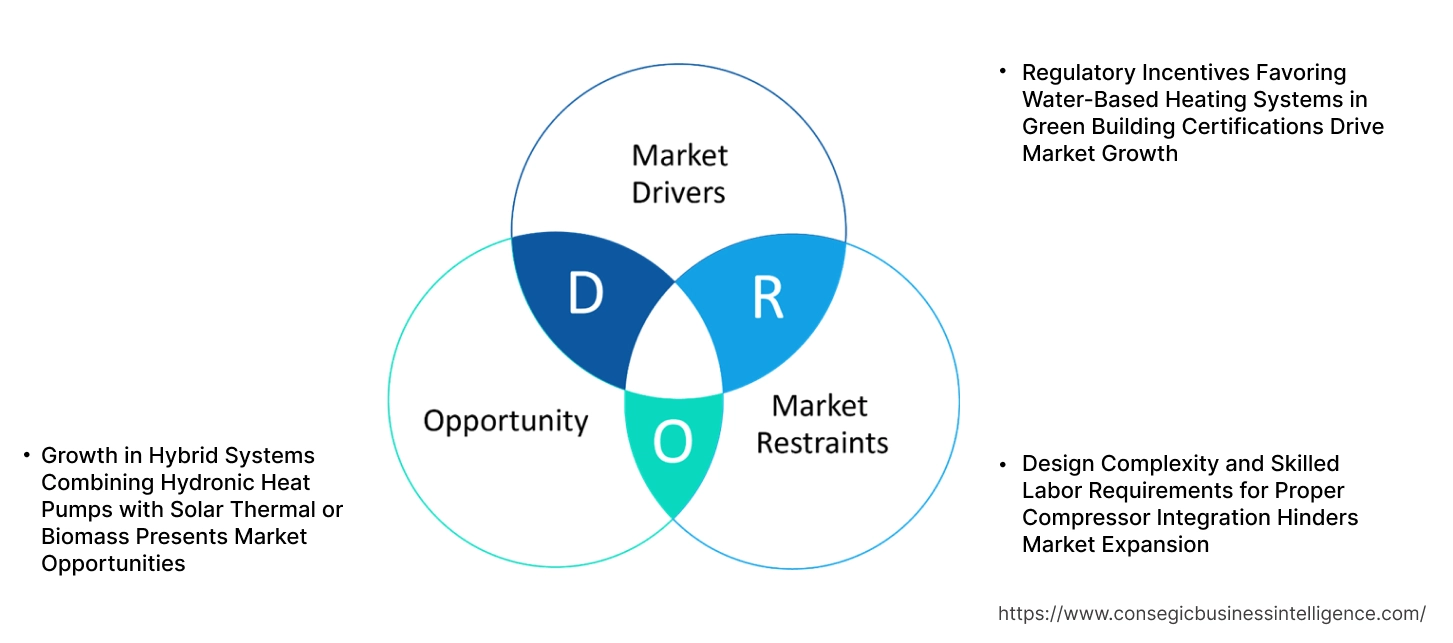

Hydronic Heat Pump Compressors Market Dynamics - (DRO) :

Key Drivers:

Regulatory Incentives Favoring Water-Based Heating Systems in Green Building Certifications Drive Market Growth

Green building standards like LEED, BREEAM, and DGNB are pushing developers toward HVAC systems that are both energy-efficient and low-emission. Hydronic heat pumps, supported by advanced compressors, check all the boxes—providing efficiency, quiet operation, and seamless integration with renewable energy sources. These systems are becoming a go-to solution in projects aiming for sustainability certifications or compliance with regional energy codes. In Europe, North America, and other markets where net-zero targets are gaining momentum, the use of water-loop-based heating is being actively encouraged through financial incentives and favorable permitting.

- For instance, in February 2024, KfW opened applications for funding for the installation of climate-friendly heating in owner-occupied single-family homes in Germany. This is an effort to encourage the transition to better heating solutions that reduce greenhouse gas emissions. The maximum limit of eligible costs is EUR 30,000. Installing heat pumps with water or wastewater-based based attracts a 5% efficiency bonus.

Public and private sector projects alike are responding to these drivers by upgrading to electrified hydronic systems. As this shift continues, demand for reliable, high-performance compressors is climbing steadily, fueling the hydronic heat pump compressors market expansion.

Key Restraints:

Design Complexity and Skilled Labor Requirements for Proper Compressor Integration Hinders Market Expansion

Setting up a hydronic heat pump system isn’t as straightforward as plugging in a standard HVAC unit. It involves matching compressor output to water loop flow rates, accounting for system dynamics, and managing control logic, all requiring technical expertise. Unfortunately, that isn’t always readily available, especially in regions without a mature hydronics market. Improper sizing or configuration often leads to inefficiency, system faults, or maintenance headaches. This creates hesitation among building owners and contractors, particularly for retrofits or mixed-use buildings where design constraints are tight. Without a reliable network of trained professionals, even the most advanced compressor technology struggles to reach its full potential. This limits the expansion of the market, slowing the hydronic heat pump compressors market growth despite rising demand for clean energy systems.

Future Opportunities :

Growth in Hybrid Systems Combining Hydronic Heat Pumps with Solar Thermal or Biomass Presents Market Opportunities

Hybrid systems that integrate hydronic heat pumps with solar thermal collectors or biomass boilers are gaining traction in net-zero energy buildings, eco-communities, and off-grid commercial projects. These configurations offer improved energy flexibility, reduced reliance on the grid, and optimal year-round heating performance. Compressors in such systems must adapt to variable source temperatures and load demands, supporting dynamic energy balancing across multiple inputs. Manufacturers are now developing advanced compressors that operate efficiently in hybrid setups with integrated control logic and variable-speed modulation. The need for these systems is increasing across Europe and parts of Asia, where thermal storage and renewable integration are prioritized.

- For instance, in March 2022, Panasonic launched a new air-source solar heat pump solution for water heating in Japan. The Eco Cute solution consists of a heat pump and hot water storage unit to save energy and water.

As green building policies and energy independence initiatives expand, compressor technologies that support hybrid heat architectures are gaining a competitive advantage, unlocking long-term hydronic heat pump compressors market opportunities in sustainability-focused and innovation-driven segments.

Hydronic Heat Pump Compressors Market Segmental Analysis :

By Compressor Type:

Based on compressor type, the hydronic heat pump compressors market is categorized into scroll compressors, reciprocating compressors, screw compressors, and rotary compressors.

The scroll compressors segment accounted for the largest revenue share in 2024.

- Scroll compressors are widely used in hydronic heat pump systems due to their high efficiency, minimal vibration, and compact design.

- They are preferred in residential and light commercial systems, offering quieter operation and better energy savings compared to other types.

- Their simplicity in design leads to lower maintenance costs and enhanced reliability, making them a popular choice in residential heat pump installations.

- As per hydronic heat pump compressors market analysis, the dominance of scroll compressors is driven by their application in both heating and cooling systems, making them versatile across various climates.

The screw compressors segment is expected to witness the fastest CAGR during the forecast period.

- Screw compressors are widely used in industrial and commercial systems that require high cooling and heating capacity for large areas.

- These compressors are highly efficient, capable of handling larger capacities, and are known for their ability to work efficiently at higher pressures.

- Increasing energy efficiency standards in industrial applications are pushing the requirement for screw compressors, as they provide higher performance and stability.

- According to hydronic heat pump compressors market trends, the growth in industrial and commercial applications is driving the adoption of screw compressors due to their robust performance.

By Refrigerant Type:

Based on refrigerant type, the market is segmented into R410A, R32, R134A, R744, CO₂, propane (R290), and others.

The R410A segment held the largest hydronic heat pump compressors market share in 2024.

- R410A refrigerant is widely used due to its high thermal efficiency and lower environmental impact compared to older refrigerants like R22.

- This refrigerant is the standard in residential and light commercial hydronic heat pump systems, offering stable performance in varying temperature conditions.

- As regulations around refrigerants tighten globally, R410A continues to dominate due to its balance between performance and reduced environmental footprint.

- As per hydronic heat pump compressors market analysis, R410A’s continued market dominance is due to its adaptability across various HVAC systems and its compliance with regulatory standards.

The CO₂ segment is projected to grow at the fastest CAGR during the forecast period.

- CO₂ (R744) is gaining popularity as a natural refrigerant due to its low global warming potential (GWP) and high efficiency in extreme temperatures.

- The rise in sustainability-focused building projects and the adoption of low-GWP refrigerants in commercial and industrial applications are key drivers.

- CO₂ is increasingly used in systems where energy efficiency and environmental compliance are top priorities, particularly in European markets.

- According to hydronic heat pump compressors market trends, CO₂ adoption is expected to increase significantly as more countries implement strict refrigerant laws.

By Distribution Channel:

Based on distribution channel, the hydronic heat pump compressors market is segmented into OEMs, aftermarket, online retail, and distributors & dealers.

The OEM segment accounted for the largest revenue share in 2024.

- Original Equipment Manufacturers (OEMs) produce compressors that are directly integrated into new hydronic heat pump systems, driving the initial market need.

- These compressors are provided as part of complete systems, sold through HVAC suppliers and manufacturers, ensuring brand compatibility and system integration.

- The OEM market is crucial for setting industry standards, and collaborations with large HVAC manufacturers enhance product distribution.

- As per hydronic heat pump compressors market demand, OEMs continue to lead due to their strong relationships with manufacturers of complete hydronic systems and the increasing adoption of new technologies.

The aftermarket segment is expected to grow at the fastest CAGR during the forecast period.

- As the number of hydronic heat pump installations increases globally, the need for replacement parts, maintenance, and repairs is boosting the aftermarket segment.

- Aftermarket distributors offer a variety of compressors, including replacements for older systems, and provide specialized services, which support their growth.

- The rise in equipment longevity and service contracts, along with the need for regular maintenance, supports aftermarket expansion.

- Thus, the need for spare parts and services in installed systems is driving the hydronic heat pump compressors market growth, especially in mature markets like North America and Europe.

By End-Use:

Based on end-use, the market is segmented into residential, commercial, and industrial.

The residential segment held the largest hydronic heat pump compressors market share of 45.3% in 2024.

- Hydronic heat pumps are increasingly used in homes due to their energy efficiency, reduced operating costs, and ability to provide both heating and cooling.

- As energy prices rise and consumers seek sustainable alternatives, hydronic systems offer significant long-term savings, making them popular in modern residential developments.

- The residential segment is also supported by incentives and government rebates that encourage the adoption of eco-friendly systems.

- For instance, in February 2024, U.S. Boiler Company unveiled the Ambient Air-to-Water Hydronic Heat Pump for residential purposes. With a capacity of 5-ton, the heat pump provides reliable space heating with low outdoor temperatures of -13°F. Additionally, it uses an environmentally friendly refrigerant- R-32.

- Hence, residential adoption continues to bolster the hydronic heat pump compressors market expansion, particularly in regions with cold climates and high electricity costs.

The commercial segment is projected to grow at the fastest CAGR during the forecast period.

- Commercial buildings such as hotels, offices, and hospitals require large-scale, efficient systems to maintain optimal temperatures across multiple zones.

- Hydronic heat pumps’ ability to be integrated with renewable energy sources and their adaptability to various building designs make them attractive for commercial installations.

- The increasing need for energy-efficient, low-carbon systems in large buildings is fueling the adoption of hydronic heat pump compressors in this segment.

- The hydronic heat pump compressors market demand is accelerated by the adoption of strict building energy regulations and corporate sustainability goals.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

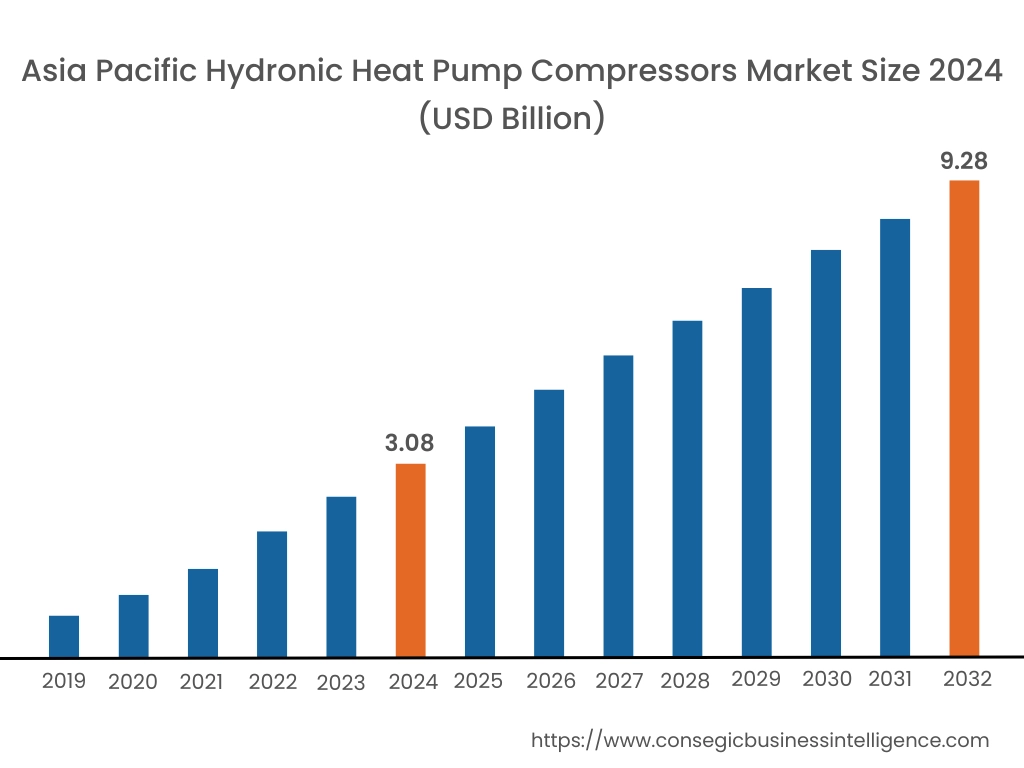

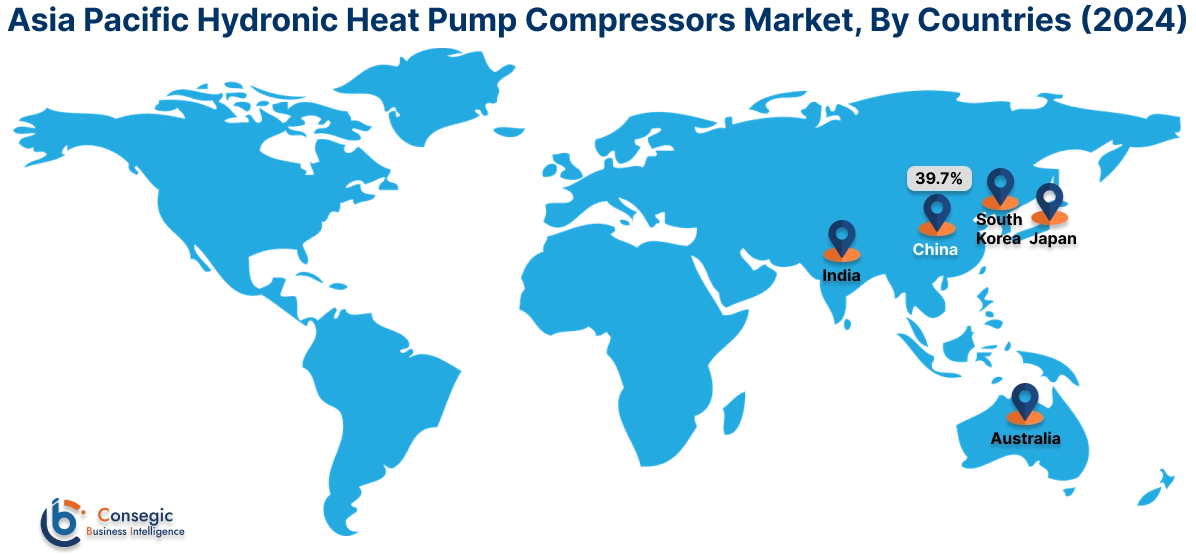

Asia Pacific region was valued at USD 3.08 Billion in 2024. Moreover, it is projected to grow by USD 3.48 Billion in 2025 and reach over USD 9.28 Billion by 2032. Out of this, China accounted for the maximum revenue share of 39.7%. Asia-Pacific is witnessing fast-paced growth in the hydronic heat pump compressors industry, driven by a mix of policy, urban development, and technology innovation. In China, heat pump adoption is central to clean heating reforms across northern provinces, where hydronic systems are replacing centralized coal-fired heating. Japan and South Korea are leveraging advanced compressor designs for compact and efficient residential applications, with market analysis pointing to strong R&D investment in low-noise and high-efficiency solutions. Additionally, Australia is adopting hydronic heat pumps in high-performance homes and commercial green buildings, particularly in climate zones where year-round comfort is needed. Local manufacturing strength and rising demand for energy independence are accelerating adoption.

North America is estimated to reach over USD 8.51 Billion by 2032 from a value of USD 2.84 Billion in 2024 and is projected to grow by USD 3.20 Billion in 2025. North America is experiencing steady adoption of hydronic systems in commercial and institutional buildings, particularly in areas prioritizing energy-efficient renovations and net-zero performance goals. In the United States and Canada, market analysis shows an increased requirement for variable-speed compressors integrated with multi-zone distribution systems, commonly used in schools, government buildings, and mixed-use developments. Electrification policies, combined with building performance standards, are encouraging the shift from traditional boilers to heat pump-based hydronic heating. Growth is further driven by utility rebate programs, as well as growing familiarity among HVAC contractors with low-temperature hydronic design principles.

Europe continues to lead in terms of both deployment and policy alignment. Countries such as Germany, Sweden, and the Netherlands are extensively incorporating hydronic systems into residential and commercial applications, supported by robust subsidies and building retrofit mandates. Market analysis indicates a strong emphasis on integrating low-GWP refrigerants, advanced inverter compressors, and smart control interfaces for district-scale and building-level heating solutions. The hydronic heat pump compressors market opportunity in Europe is underpinned by ambitious decarbonization targets, the phase-out of gas-based systems, and the rapid development of building energy codes that prioritize radiant and low-temperature hydronic distribution networks.

Latin America remains an emerging market with selective adoption, particularly in Chile, Brazil, and Argentina. Hydronic systems are being explored in premium residential developments and commercial buildings aiming to reduce energy usage and align with green building standards. Market analysis suggests that demand is influenced by the need for flexible heating and cooling in regions with varied climate profiles. While infrastructure limitations exist, growing awareness of energy-efficient alternatives to conventional HVAC systems is paving the way for gradual adoption. Long-term growth will depend on improved training for installation professionals and the availability of cost-competitive system components.

The Middle East and Africa are in early stages of adoption, though interest is growing in high-efficiency systems that offer operational cost savings and better indoor climate control. In the UAE and Saudi Arabia, new construction projects in smart cities and hospitality sectors are experimenting with radiant cooling and hydronic designs. Market analysis highlights increasing interest in systems that integrate hydronic compressors with solar thermal and thermal storage solutions. In South Africa and parts of North Africa, demand is slowly building in eco-housing and institutional projects. However, market growth is currently constrained by high upfront costs and limited supply chain access.

Top Key Players and Market Share Insights:

The hydronic heat pump compressors market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global hydronic heat pump compressors market. Key players in the hydronic heat pump compressors industry include -

- Danfoss A/S (Denmark)

- Mitsubishi Electric Corporation (Japan)

- Fujitsu General Ltd. (Japan)

- Climaveneta S.p.A. (Italy)

- Viessmann Group (Germany)

- Panasonic Holdings Corporation (Japan)

- LG Electronics Inc. (South Korea)

- Bosch Thermotechnology GmbH (Germany)

- Bitzer SE (Germany)

- GEA Group Aktiengesellschaft (Germany)

Recent Industry Developments :

Product Launches:

- In July 2024, Danfoss launched new compressors for comfort and industrial heat pumps for natural and low GWP refrigerants, PSH scroll and BOCK semi-hermetic reciprocating HGX56 CO2 T.

Hydronic Heat Pump Compressors Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 31.31 Billion |

| CAGR (2025-2032) | 14.7% |

| By Compressor Type |

|

| By Refrigerant Type |

|

| By Distribution Channel |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Hydronic Heat Pump Compressors Market? +

Hydronic Heat Pump Compressors Market size is estimated to reach over USD 31.31 Billion by 2032 from a value of USD 10.48 Billion in 2024 and is projected to grow by USD 11.83 Billion in 2025, growing at a CAGR of 14.7% from 2025 to 2032.

What specific segmentation details are covered in the Hydronic Heat Pump Compressors Market report? +

The Hydronic Heat Pump Compressors market report includes specific segmentation details for compressor type, refrigerant type, distribution channel and end-use.

What are the end-use of the Hydronic Heat Pump Compressors Market? +

The end-use of the Hydronic Heat Pump Compressors Market are residential, commercial, and industrial.

Who are the major players in the Hydronic Heat Pump Compressors Market? +

The key participants in the Hydronic Heat Pump Compressors market are Danfoss A/S (Denmark), Mitsubishi Electric Corporation (Japan), Panasonic Holdings Corporation (Japan), LG Electronics Inc. (South Korea), Bosch Thermotechnology GmbH (Germany), Bitzer SE (Germany), GEA Group Aktiengesellschaft (Germany), Fujitsu General Ltd. (Japan), Climaveneta S.p.A. (Italy) and Viessmann Group (Germany).