- Summary

- Table Of Content

- Methodology

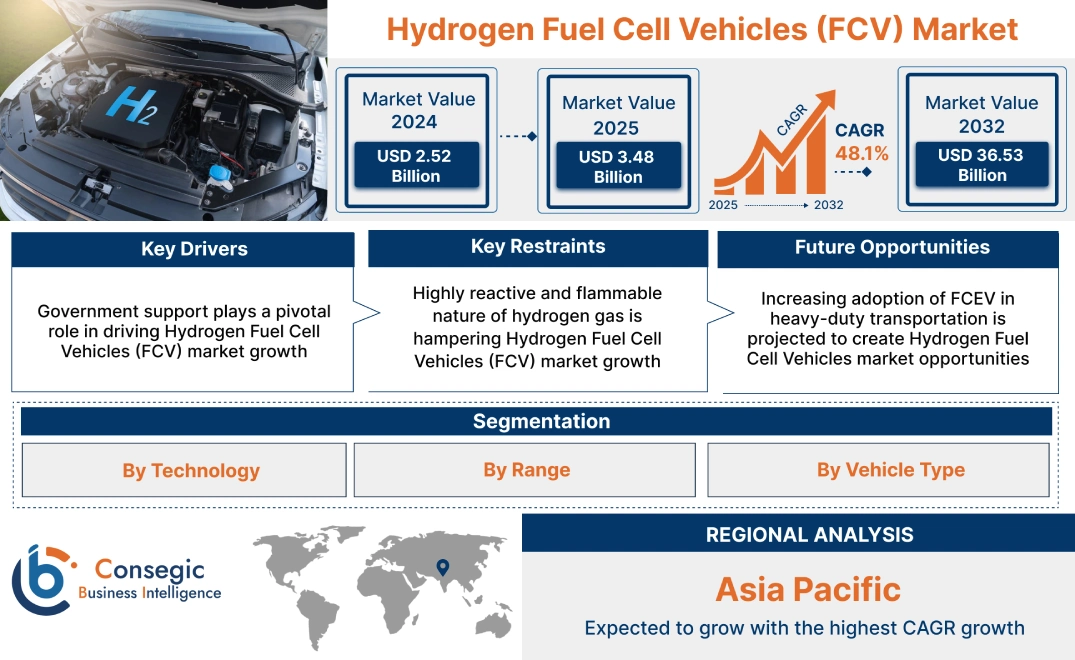

Hydrogen Fuel Cell Vehicles (FCV) Market Size:

Hydrogen Fuel Cell Vehicles (FCV) Market Size is estimated to reach over USD 36.53 Billion by 2032 from a value of USD 2.52 Billion in 2024 and is projected to grow by USD 3.48 Billion in 2025, growing at a CAGR of 48.1% from 2025 to 2032.

Hydrogen Fuel Cell Vehicles (FCV) Market Scope & Overview:

Hydrogen Fuel Cell Vehicles (FCVs) are electric vehicles that utilize fuel cells to generate electricity rather than relying on a battery pack. These vehicles combine hydrogen gas with oxygen from the air within the fuel cell, producing electricity to power the electric motor, with water vapor and heat as the only byproducts. Hydrogen is stored onboard in high-pressure tanks, and the electricity generated powers the vehicle's electric motor. Additionally, FCVs offer longer ranges and faster refueling times compared to BEVs, a potential alternative for long-haul transportation and heavy-duty applications.

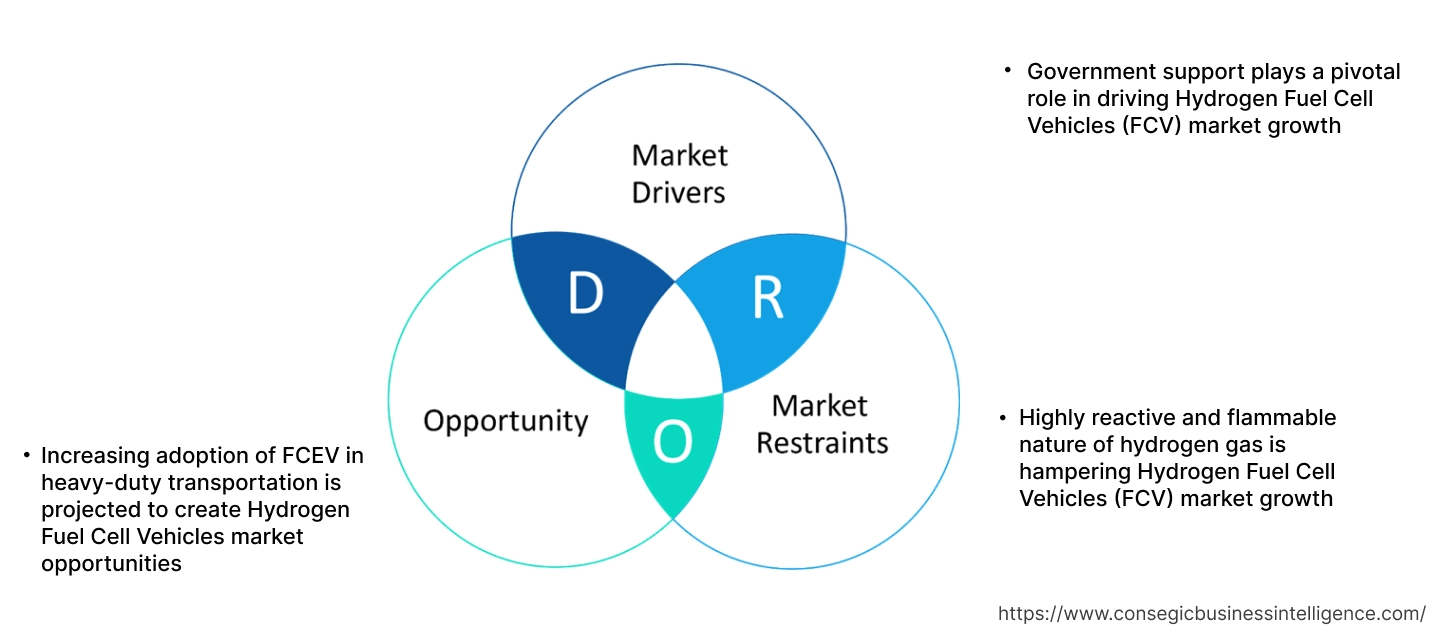

Hydrogen Fuel Cell Vehicles (FCV) Market Dynamics - (DRO):

Key Drivers:

Government support plays a pivotal role in driving Hydrogen Fuel Cell Vehicles (FCV) market growth

Governments offer financial incentives, including tax credits, subsidies, and rebates, to reduce the upfront cost of FCVs, which makes these vehicles economically competitive with traditional gasoline-powered vehicles and battery electric vehicles. The government also provides funding for research and development, which helps to accelerate technological advancements and reduce the cost of fuel cell technology. Governments are also investing in the development of hydrogen refueling stations to create a network that supports FCEV deployment. Moreover, governments are implementing stricter emission regulations to reduce greenhouse gas emissions, which creates a demand for zero-emission vehicles like FCVs. They also establish standards and regulations for hydrogen production, storage, and distribution, which ensure safety, hence boosting the Hydrogen Fuel Vehicles (FCV) market size.

- For instance, the California Energy Commission is promoting hydrogen fuel cell electric cars (FCVs) by investing in the extension of the state's hydrogen refueling infrastructure. By funding the development of 100 public hydrogen stations, California aims to overcome a key barrier to FCEV adoption: the lack of refueling options. The initiative is necessary for California to meet its ambitious zero-emission vehicle targets and achieve its broader climate and air quality goals, reducing the state's dependence on fossil fuels.

Consequently, increasing government initiatives is driving the Hydrogen Fuel Cell Vehicles (FCV) market expansion.

Key Restraints:

Highly reactive and flammable nature of hydrogen gas is hampering Hydrogen Fuel Cell Vehicles (FCV) market growth

Hydrogen's high flammability creates concerns about potential leaks and explosions, particularly in vehicle storage and refueling infrastructure. Storing hydrogen requires high-pressure tanks or cryogenic conditions, adding complexity and cost to vehicle design and refueling infrastructure. In addition, transporting hydrogen, whether in gaseous or liquid form, requires specialized infrastructure and safety protocols, increasing distribution costs. Moreover, the lack of widespread hydrogen pipelines necessitates alternative transportation methods, which are expensive, further restraining the growth of the global Hydrogen Fuel Cell Vehicles (FCV) market.

Therefore, as per the analysis, these combined factors are significantly hindering Hydrogen Fuel Cell Vehicles (FCV) market expansion.

Future Opportunities:

Increasing adoption of FCEV in heavy-duty transportation is projected to create Hydrogen Fuel Cell Vehicles market opportunities

Heavy-duty transportation, such as long-haul trucking and shipping, requires long ranges and quick refueling times, FCVs offer comparable refueling times to traditional diesel vehicles and provide longer ranges, making them a viable alternative for BEVs. Additionally, heavy-duty transportation is a major contributor to greenhouse gas emissions. The shift to FCVs offers a pathway to significantly reduce these emissions, aligning with global decarbonization goals. Moreover, the fast-refueling times of FCVs minimize downtime for fleet operators, enhancing operational efficiency, thus boosting the Hydrogen Fuel Cell Vehicles (FCV) market demand.

- For instance, in May 2024, PACCAR and Toyota partnered to accelerate the development and production of hydrogen fuel cell electric (FCV) trucks. The collaboration will focus on integrating Toyota's next-generation hydrogen fuel cell modules into Kenworth T680 and Peterbilt 579 truck models, aiming to commercialize zero-emission heavy-duty transportation. The companies plan to begin delivering these FCEV trucks to customers in 2024, representing a significant step towards decarbonizing the trucking industry.

Hence, based on the analysis, increasing adoption of FCEV in heavy-duty transportation is expected to create Hydrogen Fuel Cell Vehicles (FCV) market opportunities.

Hydrogen Fuel Cell Vehicles (FCV) Market Segmental Analysis :

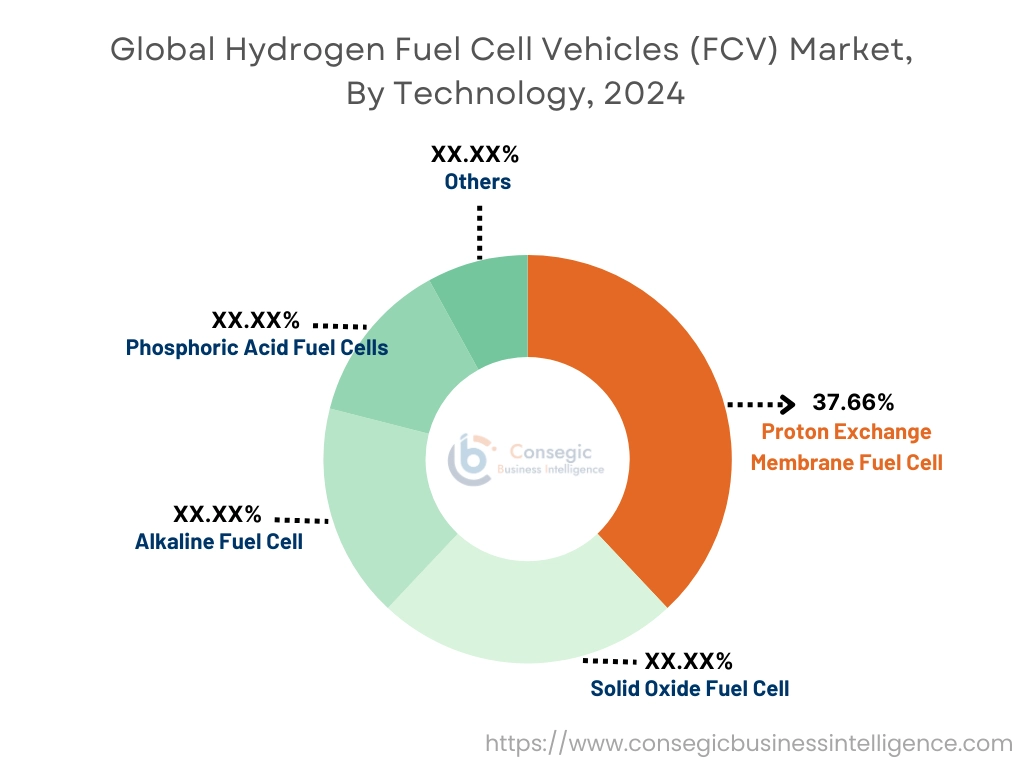

By Technology:

Based on the technology, the market is classified into alkaline fuel cell, phosphoric acid fuel cells, proton exchange membrane fuel cell, solid oxide fuel cell, and others.

Trends in the Technology:

- Growing trend towards adoption of Solid Oxide Fuel Cells (SOFCs) in stationary power generation.

- Alkaline Fuel Cells offer high efficiency and are sensitive to carbon dioxide contamination, limiting their use in typical air-breathing applications.

Proton Exchange Membrane Fuel Cell accounted for the largest revenue share of 37.66% in 2024 and is also projected to witness the fastest CAGR during the forecast period.

- Increasing focus on reducing greenhouse gas emissions and transitioning to clean energy sources is fueling proton exchange membrane fuel cell segment growth.

- Ongoing research and development efforts are leading to significant improvements in PEMFC technology, including increased efficiency, reduced costs, and enhanced durability.

- PEMFCs are ideal for use in fuel cell electric vehicles (FCVs) due to their low operating temperatures, high power density, and rapid start-up times, further boosting the Hydrogen Fuel Cell Vehicles (FCV) market.

- For instance, in April 2022, Cummins Inc. announced to offer PEM fuel cell systems to Scania, a major step in the extension of hydrogen-powered heavy-duty transportation. Scania will integrate these fuel cells into 20 of their electric truck platforms, delivering them to HyTrucks in the Netherlands in 2024. This initiative is part of HyTrucks' ambitious plan to deploy 1,000 hydrogen trucks and establish 25 refueling stations by 2025, demonstrating a significant push towards zero-emission freight transport.

- Thus, as per the Hydrogen Fuel Cell Vehicles (FCV) market analysis, the aforementioned factors are driving the proton exchange membrane segment demand.

By Range:

Based on the range, the market is categorized into 0-250 miles, 251-500 miles, and above 500 miles.

Trends in Range:

- Increasing trend for longer ranges (above 500 miles), particularly in heavy-duty applications including trucking and long-haul transport.

- Growing trend towards adopting vehicles in the range 0-250 miles offer a balance between range and refueling time, suitable for commuting and longer trips.

251-500 Miles accounted for the largest revenue share in 2024.

- This range mitigates "range anxiety," a major concern for potential FCEV adopters and provides a balance between the range of traditional gasoline-powered vehicles and the benefits of zero-emission technology.

- Vehicles in this range are suitable for a variety of applications, including daily commuting, regional travel, fleet operations, and corporate vehicles, thus driving the Hydrogen Fuel Cell Vehicles (FCV) market demand.

- Further, compared to Battery Electric Vehicles (BEVs), FCVs in this range offer faster refueling times, thereby spurring the Hydrogen Fuel Cell Vehicles (FCV) market size.

- For instance, in June 2024, Honda begun producing its 2025 CR-V e: FCEV at its Performance Manufacturing Center in Ohio. It boasts an EPA-rated 270-mile range and offers 29 miles of electric-only driving for urban commutes, complemented by the quick refueling of hydrogen for extended journeys, aligning with zero-emission mobility goals.

- Therefore, as per the market analysis, the aforementioned benefits are bolstering the Hydrogen Fuel Cell Vehicles (FCV) market trend.

Above 500 Miles is predicted to register the fastest CAGR during the forecast period.

- Heavy-duty applications require extended ranges to minimize downtime and maximize operational efficiency. FCVs with ranges exceeding 500 miles are ideal for these sectors, offering an alternative to diesel-powered vehicles.

- FCVs with extended ranges are ideal for long-distance freight transport, where battery electric vehicles (BEVs) are less suitable due to charging times and weight.

- Also, advancements in hydrogen storage technology, including high-pressure tanks and cryogenic storage, are enabling vehicles to carry larger quantities of hydrogen, crucial for achieving ranges above 500 miles.

- Therefore, the above-mentioned factors are contributing notably in spurring the Hydrogen Fuel Cell Vehicles (FCV) industry growth.

By Vehicle Type:

Based on the vehicle type, the market is bifurcated into commercial vehicles and passenger vehicles.

Trends in the Vehicle Type:

- Growing trend towards adoption of commercial FCVs in logistics and fleet operators to reduce their carbon footprint and comply with emissions regulations.

- Increasing emphasis on providing a zero-emission alternative to traditional gasoline-powered cars, with the advantage of faster refueling compared to battery electric vehicles (BEVs).

Passenger Vehicles accounted for the largest revenue share in 2024.

- Growing environmental awareness and stringent government regulations aimed at reducing greenhouse gas emissions are pushing consumers towards zero-emission vehicles, driving the market demand.

- FCVs offer an alternative to traditional gasoline-powered cars, with zero tailpipe emissions, thus fueling the Hydrogen Fuel Cell Vehicles (FCV) market share.

- FCVs provide a significant advantage over battery electric vehicles (BEVs) in terms of range and refueling time, thus boosting the market size.

- For instance, India's passenger vehicle market experienced increase in the fiscal year 2023-24, with total sales rising to 42.19 lakh units from 38.90 lakh units in the previous year. This increase was primarily driven by a significant surge in utility vehicle sales, which climbed from 20.04 lakh to 25.21 lakh units.

- Thus, as per the analysis, the aforementioned factors are driving the Hydrogen Fuel Cell Vehicles (FCV) market share.

Commercial Vehicles are predicted to register the fastest growth during the forecast period.

- Heavy-duty trucks, bus, and shipping industries are under pressure to reduce their carbon footprint and FCVs offer a viable zero-emission solution for this industry.

- Commercial vehicles require long ranges and high utilization rates, making FCVs an alternative to diesel-powered vehicles. Fast refueling times minimize downtime, which is crucial for efficient fleet operations.

- For instance, according to Society of Indian Automobile Manufacturers (SIAM), in the fiscal year 2023-24, India's commercial vehicle market saw a marginal overall increase in sales, rising from 9.62 lakh to 9.68 lakh units. This growth was driven by a notable uptick in Medium and Heavy Commercial Vehicle sales, which climbed from 3.59 lakh to 3.73 lakh units.

- Subsequently, the aforementioned factors are collectively responsible in driving the Hydrogen Fuel Cell Vehicles (FCV) market trend.

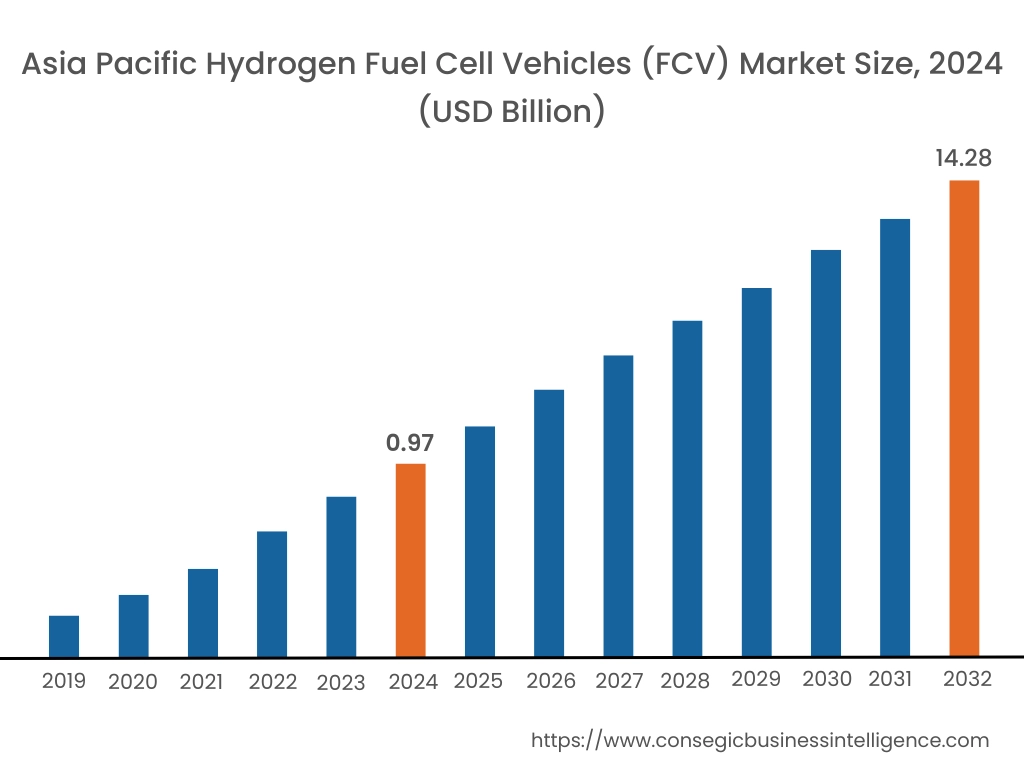

Regional Analysis:

The global Hydrogen Fuel Cell Vehicles (FCV) market has been classified by region into North America, Europe, Asia-Pacific, MEA, and Latin America.

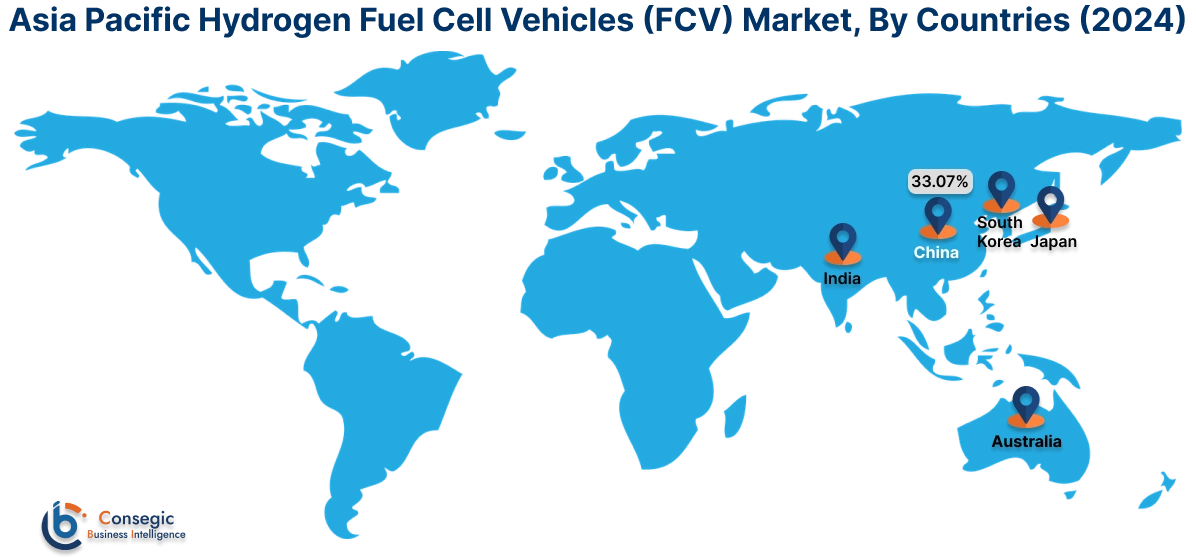

Asia Pacific region was valued at USD 0.97 Billion in 2024. Moreover, it is projected to grow by USD 1.34 Billion in 2025 and reach over USD 14.28 Billion by 2032. Out of these, China accounted for the largest revenue share of 33.07% in 2024.

Countries including Japan, South Korea, and China are heavily investing in hydrogen infrastructure and providing incentives to promote FCV adoption. These governments recognize hydrogen as a crucial component of their decarbonization strategies. Additionally, major automotive manufacturers like Toyota and Hyundai are heavily investing in FCV development and deployment. These companies are also undergoing innovations to improve mileage, further contributing to market expansion.

- For instance, in May 2021, Hyundai NEXO, driven by a Hyundai Australia team, achieved a new world record for the longest distance traveled by a hydrogen fuel cell vehicle on a single tank, covering 887.5 kilometers. This zero-emissions journey from Melbourne to beyond Broken Hill surpassed the previous record, also held by a NEXO, and highlighted the potential of hydrogen as a clean fuel source.

North America was valued at USD 0.64 Billion in 2024. Moreover, it is projected to grow by USD 0.88 Billion in 2025 and reach over USD 9.22 Billion by 2032. The United States and Canada are implementing policies to promote clean energy and reduce emissions including funding for hydrogen infrastructure development and incentives for FCV adoption. Specifically, California is a leading state in FCV adoption, with significant investments in hydrogen refueling stations and zero-emission vehicle mandates.

- For instance, in December, the U.S. Environmental Protection Agency (EPA) has allocated over USD 735 million to 70 applicants across 27 states, Tribal Nations, and a territory, through its inaugural Clean Heavy-Duty Vehicles Grant Program. This funding aims to facilitate the purchase of over 2,400 zero-emission vehicles, specifically heavy-duty vehicles, marking a significant step towards reducing emissions from the transportation sector and promoting cleaner air.

As per the Hydrogen Fuel Cell Vehicles (FCV) market analysis, Europe’s strong government support, coupled with stringent emission regulations and a growing focus on sustainability, is driving the market. Latin American FCV market holds significant potential due to the region's vast renewable energy resources. While infrastructure development is limited, growing environmental concerns and increasing interest in sustainable transportation are creating opportunities. Further, oil-rich nations in the Middle East are exploring hydrogen as a diversification strategy, investing in large-scale green hydrogen production projects, and considering FCVs for specific applications like public transportation and logistics.

Top Key Players & Market Share Insights:

The market is highly competitive with major players providing Hydrogen Fuel Cell Vehicles (FCV) to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the Hydrogen Fuel Cell Vehicles (FCV) industry include-

Recent Industry Developments :

Partnerships and Collaborations:

- In September 2024, BMW and Toyota collaborated to accelerate the development and adoption of Fuel Cell Electric Vehicles (FCEVs). BMW aims to launch its first production FCEV passenger car by 2028, offering customers a zero-emission alternative. By combining their expertise and resources, both companies are working to advance hydrogen fuel cell technology and promote the growth of the hydrogen economy.

Achievements:

- In June 2024, Hyundai's XCIENT Fuel Cell trucks achieved a significant milestone, surpassing 10 million kilometers of real-world usage in Switzerland.

Hydrogen Fuel Cell Vehicles (FCV) Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 36.53 Billion |

| CAGR (2025-2032) | 48.1% |

| By Technology |

|

| By Range |

|

| By Vehicle Type |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Hydrogen Fuel Cell Vehicles (FCV) market? +

The Hydrogen Fuel Cell Vehicles (FCV) market size is estimated to reach over USD 36.53 Billion by 2032 from a value of USD 2.52 Billion in 2024 and is projected to grow by USD 3.48 Billion in 2025, growing at a CAGR of 48.1% from 2025 to 2032.

What specific segmentation details are covered in the Hydrogen Fuel Cell Vehicles (FCV) report? +

The Hydrogen Fuel Cell Vehicles (FCV) report includes specific segmentation details for technology, range, vehicle type, and regions.

Which is the fastest segment anticipated to impact the market growth? +

In the Hydrogen Fuel Cell Vehicles (FCV) market, commercial vehicles are the fastest-growing segment during the forecast period.

Who are the major players in the Hydrogen Fuel Cell Vehicles (FCV) market? +

The key participants in the Hydrogen Fuel Cell Vehicles (FCV) market are Toyota (Japan), Hyundai (South Korea), Honda (Japan), BMW (Germany), Ashok Leyland (India), Tata Motors (India), Nikola Corporation (United States), Hino Motors (Japan), Iveco (Italy), Riversimple (United Kingdom), and Others.