- Summary

- Table Of Content

- Methodology

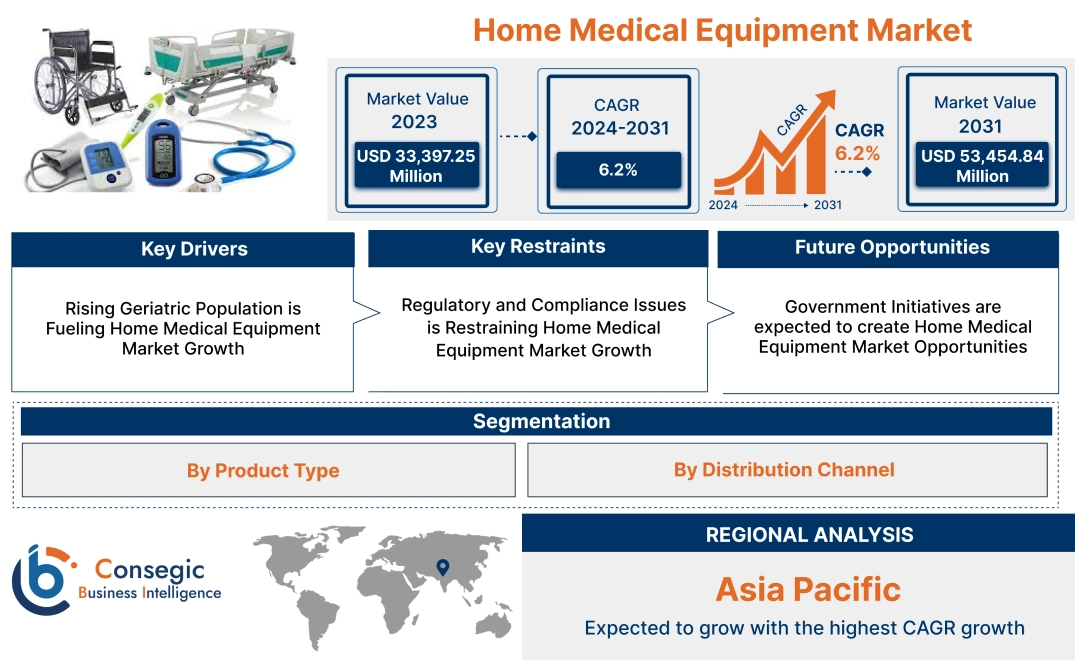

Home Medical Equipment Market Size:

Home medical equipment market size is estimated to reach over USD 53,454.84 Million by 2031 from a value of USD 33,397.25 Million in 2023, growing at a CAGR of 6.2% from 2024 to 2031.

Home Medical Equipment Market Scope & Overview:

Home medical equipment (HME) refers to a category of devices used by patients to manage their healthcare needs in a home setting. These devices are designed to be durable, safe, and easy for patients or caregivers to use. There are various types of this equipment such as therapeutic equipment, monitoring and diagnostic equipment, mobility assistance equipment, and others. Further, therapeutic equipment includes oxygen concentrators, ventilators, CPAP (Continuous positive airway pressure) machines, nebulizers, dialysis machines, and others. Various features of this equipment include portability, user-friendly design, real-time health monitoring, and others. This equipment offers various benefits such as eliminating the need for expensive medical procedures, helping in the monitoring of chronic diseases, increasing patient safety, and more. Recent developments in telemedicine and remote patient monitoring have enhanced the adoption of this equipment in hospitals and homecare settings.

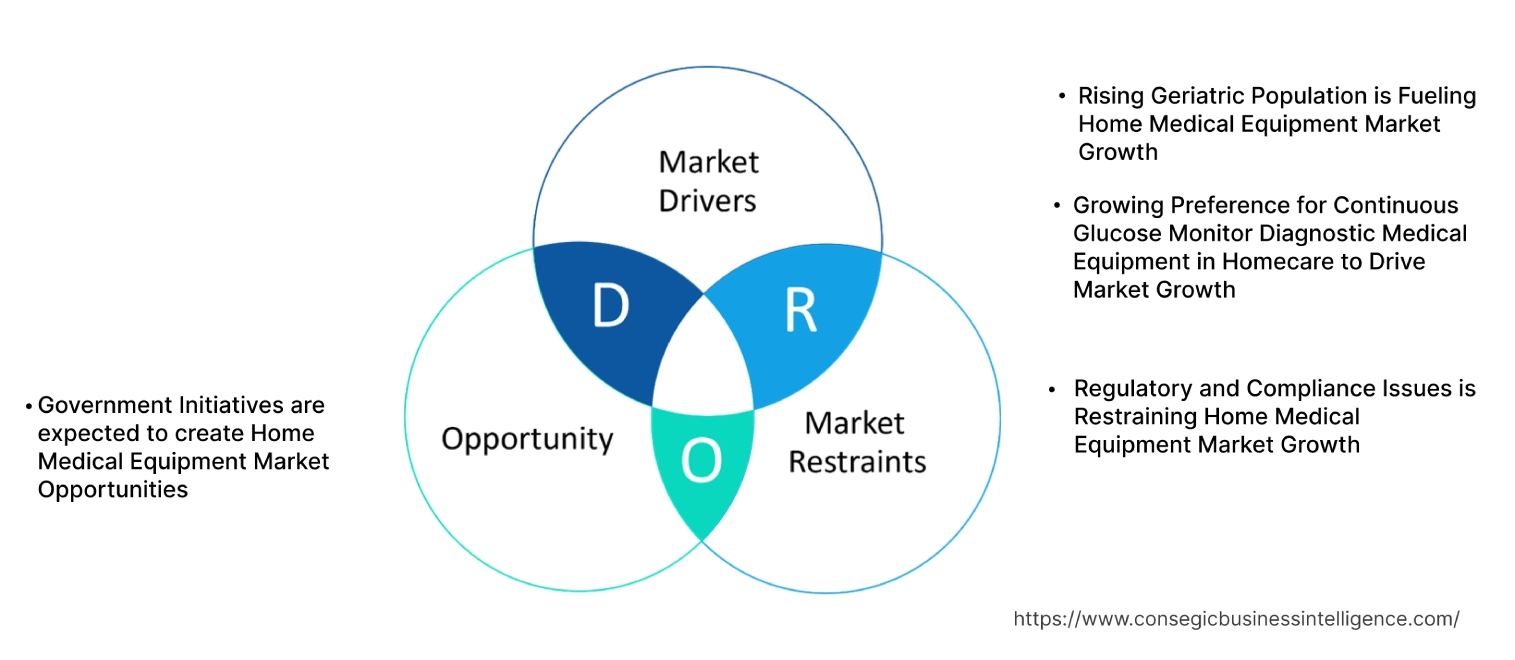

Home Medical Equipment MarketDynamics - (DRO) :

Key Drivers:

Rising Geriatric Population is Fueling Home Medical Equipment Market Growth

The rising geriatric population globally is creating demand for the market that caters to the unique needs of elderly individuals. The population aged 65 and above is more susceptible to chronic illnesses like cancer, asthma, and other age-related health conditions like osteoporosis, arthritis, and more. This makes them primary consumers of this medical equipment. Equipment such as glucose monitors, blood pressure monitors, and others are used in the treatment of age-related conditions such as arthritis, diabetes, osteoporosis, and more.

- In 2022, according to the United Nations, the global population aged 65 and above is expected to rise from 10% in 2022 to 16% in 2050. This shift is expected to drive the market. As the elderly population prefers to receive medical care at home and monitor their health continuously, the market for home medical devices is poised for substantial growth.

Thus, the rising aging population is expected to drive home medical equipment market demand by offering more convenience and continuous health monitoring.

Growing Preference for Continuous Glucose Monitor Diagnostic Medical Equipment in Homecare to Drive Market Growth

The escalating need for home-based healthcare and remote patient monitoring is propelling the market. As individuals prioritize convenience, affordability, and privacy in their healthcare regimens, the adoption of at-home diagnostic devices is surging. These devices empower individuals to take control of their health, enabling early disease detection, proactive management of chronic conditions, and timely interventions.

One such device is the continuous glucose monitor (CGM) which is used to continuously measure blood glucose levels of diabetic patients. This development of continuous glucose monitor is advancing the market by increasing patient outcomes. It allows patients to monitor their glucose levels at home without the need for frequent visits to medical facilities. These devices enable timely detection of health issues, leading to better management of chronic conditions like diabetes, kidney diseases, and others.

- In 2023, Medtronic plc launched Simplera™ continuous glucose monitor (CGM) in Europe. It is integrated with the InPen™ smart insulin pen, which provides real-time, personalized dosing guidance to help simplify diabetes management. It is creating home medical equipment market demand in the European region, by continuously measuring blood glucose levels of diabetic patients in their homes.

Thus, this development of continuous glucose monitor is accelerating home medical equipment market expansion by enabling real-time and continuous monitoring of the blood glucose levels of patients at home.

Key Restraints :

Regulatory and Compliance Issues is Restraining Home Medical Equipment Market Growth

Regulatory and compliance factors significantly hinder the growth and adoption of the market. Medical devices intended for home use must adhere to stringent safety, performance, and quality standards. These standards are set by regulatory authorities like the United States Food and Drug Administration, European CE (Conformité Européenne), and regional agencies. Due to these regulatory and compliance issues, manufacturers face lengthy approval processes for new products. Additionally, extensive trials, documentation, and inspections delay the introduction of innovative equipment. Meeting regulatory standards involves significant costs for testing, certification, and ongoing audits. Different countries have varying compliance requirements, forcing manufacturers to modify products for specific markets.

Thus, these regulatory hurdles increase costs for manufacturers and limit the availability of this equipment for end-users.

Future Opportunities :

Government Initiatives are expected to create Home Medical Equipment Market Opportunities

Government initiatives aimed at promoting home-based patient care are poised to create significant market opportunities for the market. By encouraging the shift from traditional hospital-centric models to home-based care, governments are fostering an environment that favors the adoption of home medical devices. These initiatives often include reimbursement policies, tax incentives, and telemedicine programs, which incentivize both healthcare providers and patients to embrace home-based care solutions. Government organizations like the United States Food and Drug Administration, National Health Mission, and others are launching initiatives to promote home-based patient care to alleviate the pressure on hospitals and clinics.

- In 2024, the S. Food and Drug Administration launched an initiative, Home as a Health Care Hub, to help improve home-based patient care. This partnership includes collaboration with patient groups, healthcare providers, and the medical device industry to build the Home as a Health Care Hub. It will lead to home medical equipment market expansion by promoting home-based patient care in the U.S.

Thus, government initiatives are expected to create home medical equipment market opportunities by promoting home-based care for patients.

Home Medical Equipment Market Segmental Analysis :

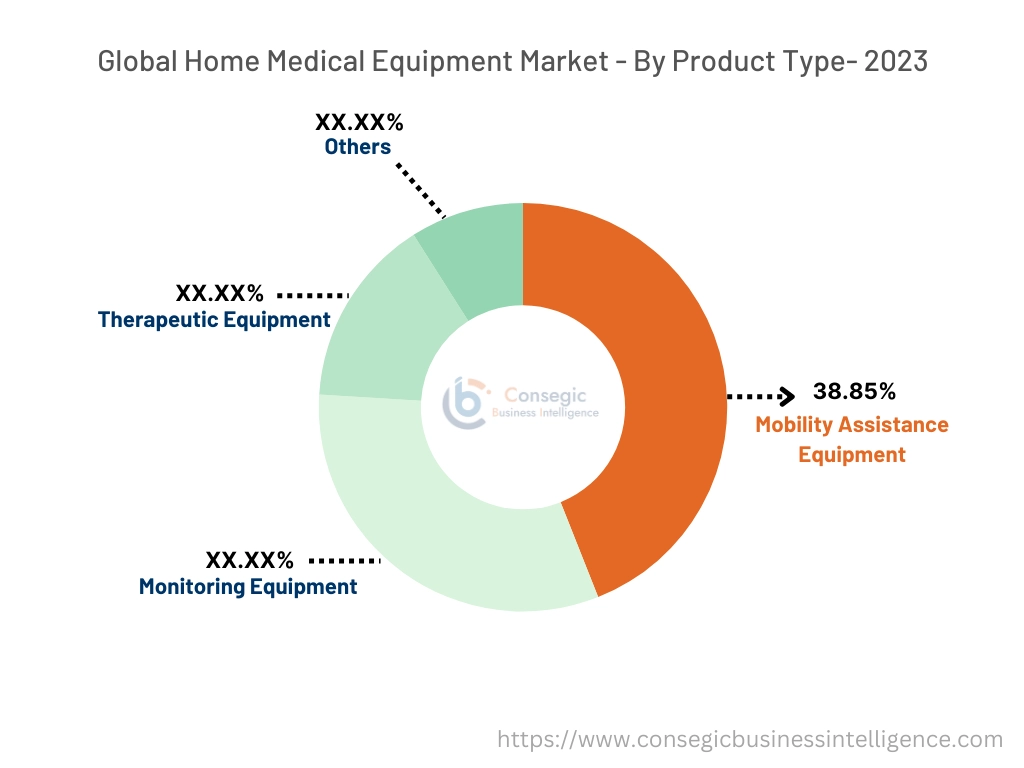

By Product Type:

By product type, the market is divided into therapeutic equipment, monitoring equipment, mobility assistance equipment, and others.

Trends in Product Type:

- According to home medical equipment market trends, portable mobility assistance equipment has enhanced patient convenience, making them more suitable for home use.

- Monitoring equipment is rapidly used for regular health monitoring at home as per the latest trends.

The mobility assistance equipment accounted for the largest market share of 38.85% in the year 2023.

- The rising global geriatric population and the increasing prevalence of chronic diseases are driving the demand for mobility assistance equipment.

- As healthcare systems shift towards home-based care, the need for devices like wheelchairs, walkers, and canes is growing.

- Moreover, technological advancements in mobility aids are enhancing their functionality and user experience.

- Government initiatives and favorable reimbursement policies further contribute to the dominance of mobility assistance equipment in the market.

- For instance, in November 2024, Paiseec, a brand operating in innovative mobility solutions, launched W3, a 3-in-1 device that enhances the mobility experience for wheelchair users. The W3 electric wheelchair is specifically designed to cater to the varied needs of wheelchair users across different environments including homecare settings. The W3 seamlessly switches between three modes: a power wheelchair for daily mobility, an intelligent transport device, and a rollator for extended use, thus embodying the versatility of a single device serving multiple purposes.

- As healthcare shifts towards home-based care, mobility assistance equipment is leading to market proliferation as per current trends.

The monitoring equipment of the product type is expected to grow at the fastest CAGR over the forecast period.

- Monitoring Equipment growth is primarily driven by the aging population, the rising prevalence of chronic diseases, and advancements in technology.

- As the need for continuous health monitoring increases, the adoption of portable and user-friendly devices like blood pressure monitors, glucose meters, and pulse oximeters is on the rise.

- Additionally, the shift towards home-based care and telehealth services is further fueling the need for remote monitoring capabilities.

- Government initiatives and favorable reimbursement policies are also contributing to the market proliferation.

- Overall, the combination of these factors is expected to drive substantial growth in the monitoring equipment segment in the coming years.

By Distribution Channel:

By Distribution Channel, the market is divided into hospital pharmacies, retail pharmacies, and online pharmacies.

Trends in Distribution Channel:

- According to home medical equipment market trends, Retail pharmacies remain a significant distribution channel, especially for complex medical equipment requiring specialized handling and patient education.

- Online pharmacies are increasingly becoming a major distribution channel for this medical equipment. They offer convenience and accessibility for consumers, especially for simple devices like blood pressure monitors, glucose meters, and inhalers as per the latest trends.

The retail pharmacies accounted for the largest revenue share in the year 2023.

- Retail pharmacies have become a dominant force in the market due to their strategic positioning and customer-centric approach.

- Their widespread accessibility, strong brand recognition, and expert consultation services make them a preferred choice for consumers.

- By offering a diverse range of products, from simple devices like blood pressure monitors to complex equipment like CPAP machines, retail pharmacies cater to a wide spectrum of healthcare needs.

- Additionally, their integration with telehealth services enables remote consultations and personalized advice, enhancing the overall customer experience.

- Effective marketing strategies, including in-store promotions and digital marketing campaigns, further drive sales and brand awareness.

- As a result, retail pharmacies are well-positioned to maintain their dominance in the market, providing convenience and accessibility to consumers worldwide.

The online pharmacies in the end-user are expected to grow at the fastest CAGR over the forecast period.

- Online pharmacies are poised to experience the most rapid growth within the market.

- Their ability to offer unparalleled convenience, competitive pricing, and a vast array of products has significantly contributed to their increasing popularity.

- Advanced algorithms enable personalized product recommendations, while seamless checkout processes and efficient delivery services enhance the overall customer experience.

- Furthermore, the integration of telehealth services allows for remote consultations and personalized advice, solidifying the position of online pharmacies as a preferred choice for consumers seeking medical equipment for home care.

- For Instance, in a survey conducted by ASOP Global Foundation, over half of Americans aged 18 and older have used online pharmacies, with a majority starting within the past three years. These users rely on online platforms for a significant portion of their prescription medication needs, highlighting the growing popularity and convenience of online pharmacies for home-based medical equipment.

- Thus, the market is experiencing rapid distribution in online pharmacies as per current trends.

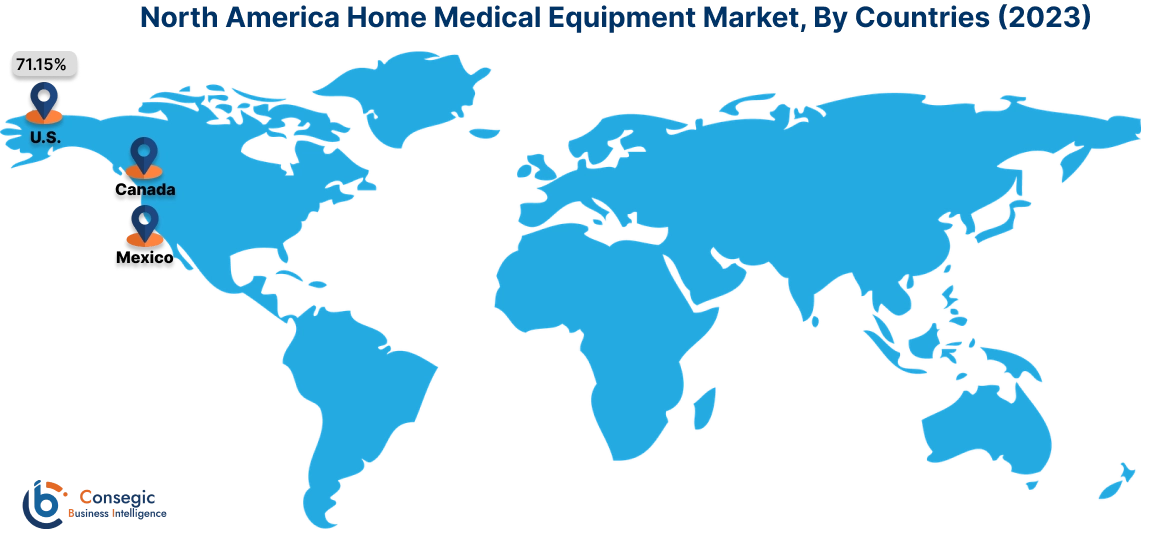

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

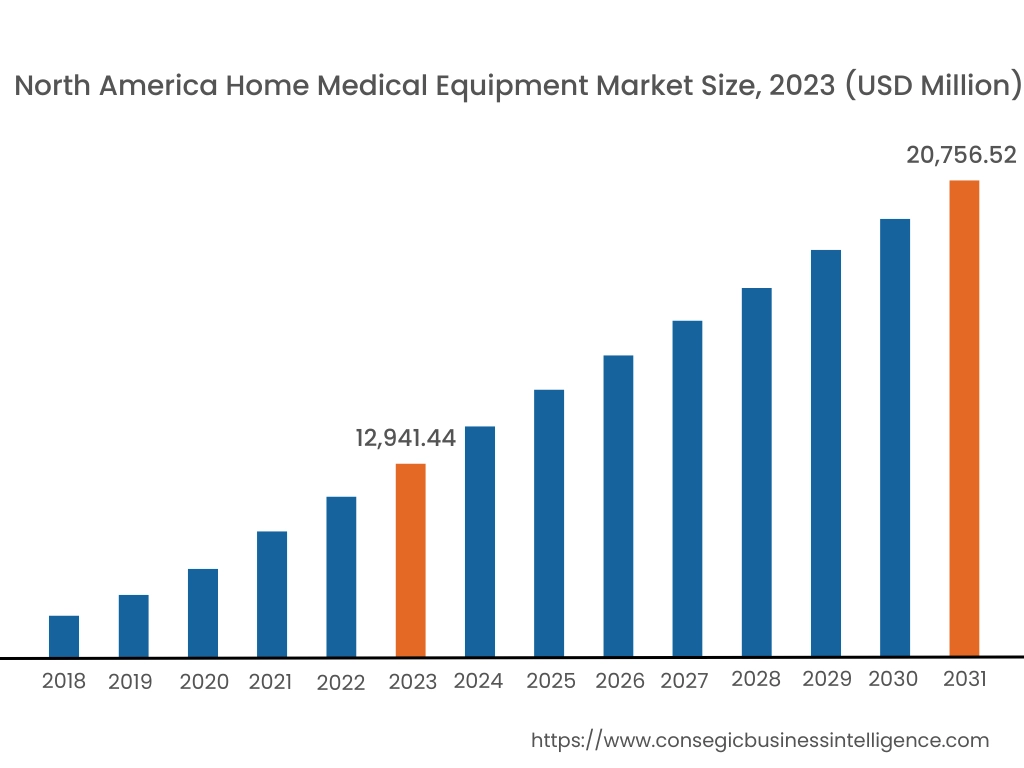

In 2023, North America accounted for the highest market share at 38.75% and was valued at USD 12,941.44 Million and is expected to reach USD 20,756.52 Million in 2031. In North America, the U.S. accounted for the highest market share of 71.15% during the base year of 2023. As per market analysis, the home medical equipment market share in North America is driven by advanced healthcare infrastructure, technological innovations, and high patient awareness. The region benefits from a robust demand for this equipment due to the rising prevalence of chronic diseases such as diabetes, cardiovascular disorders, and respiratory conditions like chronic obstructive pulmonary disease. Companies in this region are investing in this equipment due to the growing demand for home-based patient care.

- In 2024, HelathTap partnered with AeroFlow allowing patients to more easily access primary care and home medical equipment. The partnership will allow Aeroflow customers to connect with a licensed HealthTap physician to receive home medical equipment-related consultations. This will lead to the proliferation of home-based patient care, thereby leading to the market proliferation in the U.S.

Thus, home medical equipment in North America is expected to dominate due to the high prevalence of chronic diseases and technological advancements as per the analysis.

Asia-Pacific is expected to witness the fastest CAGR over the forecast period of 6.8% during 2024-2031. According to the home medical equipment market analysis, the home medical equipment in the Asia-pacific region is experiencing significant proliferation due to increasing demand for convenient healthcare solutions. The rapid aging population particularly in countries like China, India, and Japan, is a key driver, as older adults often require long-term care and chronic disease management. Further in India, companies like Philips, and ResMed are offering cost-effective home medical equipment such as glucose monitors, portable oxygen concentrators, and others. Additionally, the rise in lifestyle diseases, such as diabetes and hypertension, is further increasing the need for home-based medical equipment. Governments in the region are also supporting the proliferation of the market through policies, reimbursements, and healthcare infrastructure improvements. Technological advancements in telemedicine, personalized medicine, and remote monitoring are boosting the home medical equipment market share in this region.

As per the home medical equipment market analysis, this market in the Middle East and Africa region is steadily growing, driven by elderly populations, particularly in countries like Saudi Arabia, UAE, and South Africa. Rising incidences of chronic diseases, such as diabetes and cardiovascular conditions, are also fueling the need for medical equipment for home use. Moreover, improvements in healthcare infrastructure and government initiatives such as insurance coverage for medical devices are promoting home healthcare, further fueling the market. Technological advancements along with increased awareness and affordability, are expected to continue driving the market proliferation in this region. The market is expected to grow further in this region due to government support and the presence of global companies such as Medtronic, GE Healthcare, and more as per market analysis.

As per analysis, the market in Latin America is witnessing increasing proliferation. It is driven by factors such as a rapidly aging population and rising prevalence of chronic diseases and the increasing shift towards home healthcare. Countries like Brazil, Mexico, and Argentina are experiencing a growing need for home-based medical devices to manage conditions such as diabetes, hypertension, and respiratory diseases. The region’s healthcare systems are also evolving, with the government investing in telemedicine and home care infrastructure, improving access to home medical equipment. Additionally, the rising awareness of the benefits of home healthcare, coupled with the affordability of medical devices, is further supporting the market expansion.

Top Key Players & Market Share Insights:

The home medical equipment industry is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global home medical equipment market. Key players in the home medical equipment industry include-

- Rotech Healthcare Inc. (United States)

- ResMed (United States)

- Fresenius kabi (Germany)

- 3M (United States)

- Siemens Healthineers (Germany)

- Medtronic (United States)

- Medline Industries (United States)

- OMRON Healthcare (Japan)

- Johnson & Johnson Private Limited (United States)

- Abbott (United States)

Recent Industry Developments :

Launches:

- In 2024, The Food and Drug Administration’s (FDA's) device center launched an initiative to promote at-home medical equipment development with a focus on health equity in at-home care. For this initiative, the FDA has paid nearly USD 1.2 million to Dallas-based architectural firm HKS Inc. to build a virtual reality model of a home. It will lead to the development of the market in the United States.

- In 2024, Roche launched an AI-powered diabetes tracker to predict blood sugar highs and lows. They launched a continuous glucose monitoring system, a home medical equipment featuring artificial intelligence-powered forecasts of blood sugar highs and lows. It will enhance the home care for diabetic patients, fostering innovation in this equipment.

Mergers and Acquisitions:

- In 2024, WellSky acquired Bonafide, an enterprise resource planning (ERP) software solution for home medical equipment (HME) companies. This combination of WellSky and Bonafide will enable more home medical equipment companies to improve operations and streamline ordering and administrative processes. This will lead to the proliferation of the market.

Home Medical Equipment Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 53,454.84 Million |

| CAGR (2024-2031) | 6.2% |

| By Product Type |

|

| By Distribution Channel |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the home medical equipment Market? +

Home medical equipment market size is estimated to reach over USD 53,454.84 Million by 2031 from a value of USD 33,397.25 Million in 2023, growing at a CAGR of 6.2% from 2024 to 2031.

What specific segmentation details are covered in the home medical equipment market report? +

The home medical equipment market report includes specific segmentation details for product type and distribution channel.

Which is the fastest-growing region in-home medical equipment Market? +

Asia-Pacific is the fastest-growing region in the home medical equipment market.

Who are the major players in the home medical equipment Market? +

The key participants in the home medical equipment market are Rotech Healthcare Inc. (United States), ResMed (United States), Medtronic (United States), Medline Industries (United States), OMRON Healthcare (Japan), Johnson & Johnson Private Limited (United States), Abbott (United States), Fresenius Kabi (Germany), 3M (United States), Siemens Healthineers (Germany)